|

市場調查報告書

商品編碼

2073084

反芻動物飼料添加劑:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Ruminant Feed Additives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

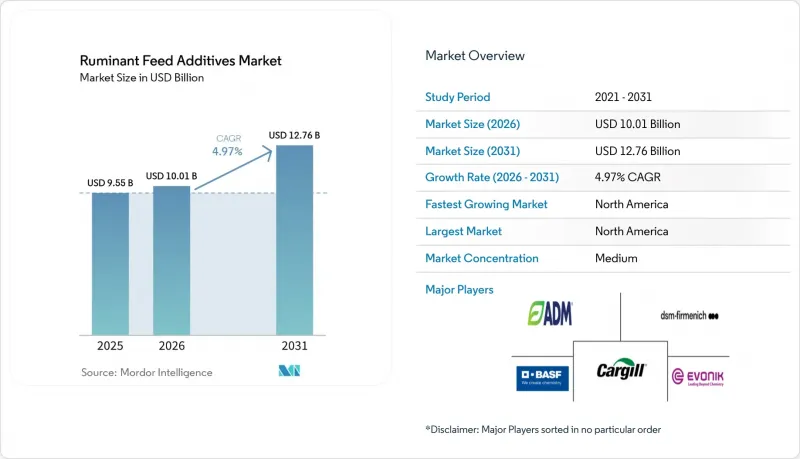

據 Mordor Intelligence 稱,2025 年反芻動物飼料添加劑市值為 95.5 億美元,預計到 2031 年將達到 127.6 億美元,而 2026 年為 100.1 億美元,預測期(2026-2031 年)的複合年成長率為 4.97%。

本報告按添加劑類型(酸化劑、胺基酸、抗生素、抗氧化劑、礦物質、粘合劑、酵素及其他)、牲畜類型(牛、牛及其他反芻動物)和地區(非洲、亞太地區、歐洲、中東、北美和南美)進行細分。市場預測以價值(美元)和數量(噸)兩種單位呈現。

全球反芻動物飼料添加劑市場趨勢及洞察

對提高牛奶和肉類生產力的需求日益成長

反芻動物飼料添加劑市場持續維持強勁成長勢頭,主要得益於商業牛對提高產乳量、乳固態、生長速度和飼料轉換率的需求。根據Alltek預測,到2025年,全球複合飼料產量預計將超過14.4億噸,而反芻動物飼料仍然是特種添加劑比標準配方更具附加價值的領域之一。在酪農系統中,高產量乳牛的遺傳改良正在縮小飼料營養與飼料所需營養之間的差距,從而帶動了對保護性胺基酸、礦物質、維生素和瘤胃支持產品的強勁需求。此外,單產的提高降低了每公斤牛奶或肉類的排放強度,進一步加強了生產力和永續性目標之間的連結。這種協同效應強化了優質營養方案的作用,使反芻動物飼料添加劑市場不僅與短期飼料週期緊密相關,而且與結構效率目標也息息相關。

不使用抗生素的生產方式正在推動對功能性食品添加劑的需求。

反芻動物飼料添加劑市場正受惠於乳牛和肉牛養殖業日益轉向無抗生素生產體系的轉變。隨著抗生素生長促進劑的逐步淘汰或使用限制的加強,生產者正在尋求替代方案,以支持消化、腸道健康、免疫力和穩定的生產性能。 2025年發表在《高級研究雜誌》(Journal of Advanced Research)上的一項Meta分析報告稱,無抗生素飼料添加劑的組合顯著改善了多種牲畜的生長性能和免疫功能。這一趨勢促使益生菌、益生元、植物萃取物、酵素、產酸劑和多成分組合藥物在市售反芻動物飼料中的使用量增加。值得注意的是,生產者正在摒棄單一成分替代,轉而採用結合多種功能機制的綜合方案。這種方法增加了許多以組織培養為主的畜群的平均單頭支出,反芻動物飼料添加劑市場也正在從單純補充基礎礦物質和維生素發展成為更為多元化的市場。

特殊添加劑與傳統預混合料高成本對比

在反芻動物飼料添加劑市場,特種產品與傳統礦物質和維生素預混合料相比,價格障礙依然存在。贏創工業集團宣布,其MetAMINO產品將於2026年3月全球淨價調高10%。這表明,保護性氨基酸和合成營養品領域仍然面臨生產成本壓力。對於飼料預算緊張、難以單獨評估產品效果的小規模農戶和半商業性生產系統而言,這種價格差異所帶來的問題尤其突出。在這些生產系統中,即使特種配方能顯著提高生產效率,生產者往往仍選擇使用較簡單的預混合料。商業性挑戰不僅在於價格,還在於如何在農場層級證明產品的價值,尤其是在諮詢支援有限的情況下。簡而言之,為了使反芻動物飼料添加劑市場在成本敏感地區實現更快成長,供應商需要將高附加價值產品與實用服務、更清晰的有效性指標以及便捷的包裝相結合。

細分市場分析

到2025年,胺基酸將佔反芻動物飼料添加劑市場佔有率的20.7%,成為業界最大的添加劑類別。這一主導地位反映了在對蛋白質平衡進行嚴格控制的高產乳牛飼料配方中,瘤胃保護劑離胺酸和甲硫胺酸的持續使用。此類別的主要產品包括贏創工業集團的「Mepron」、安迪蘇法國公司的「Smartamine」和「Metasmart」以及味之素株式會社的「Azipro-L」。此外,維生素、益生菌和植物性添加劑也佔據重要地位,因為它們在促進健康穩定、支持新陳代謝以及在各種畜牧養殖系統中實現無抗生素飼餵方面發揮著重要作用。類別組成的變化表明,反芻動物飼料添加劑市場的發展不再僅僅依賴通用配方產品,而是越來越依賴旨在支持特定生產力和健康結果的成分。

預計到2031年,酸度調節劑將成為反芻動物飼料添加劑市場中所有添加劑類型中成長最快的,複合年成長率將達到5.8%。這一成長主要得益於無抗生素配方方法的推廣應用,以及牛開食料方案的日益普及,這些方案旨在改善腸道環境並減輕早期消化器官系統壓力。混合酸添加劑因其兼具衛生管理和瘤胃適應的雙重優勢而日益受到歡迎,使其在生產週期的各個階段都具有價值。此外,隨著氣候變遷影響飼料質量,以及先進的飼餵系統能夠更精確地量化消化率的提升,黴菌毒素管理和酵素製劑的使用也變得越來越重要。因此,該產業正從單一用途的原料轉向多功能產品系列。這一趨勢正在推動更廣泛的高級產品線的開發,而成長的重點也日益集中在與健康、精準飼餵和永續性目標相符的產品類別上。

區域分析

到2025年,北美將佔據反芻動物飼料添加劑市場38.0%的佔有率,預計到2031年將以6.1%的複合年成長率成長,成長速度在所有地區中最高。對於一個成熟的地區而言,這無疑是卓越的領先地位,但也與反芻動物飼料添加劑市場的結構相符。北美地區擁有大規模酪農、大規模育肥場、較高的添加劑滲透率以及對特殊產品的高度接受度。美國是該地區需求的主要驅動力,這得益於其龐大的牛規模、商業性營養服務和環境壓力等因素。加拿大憑藉其完善的酪農體系和監管框架,進一步增強了該地區的市場實力,促進了特種添加劑的普及應用。墨西哥仍然是重要的成長中心,因為酪農和肉牛牛業的商業化程度越來越高,並且與正規的預混合料供應聯繫日益緊密。因此,北美地區持續扮演反芻動物飼料添加劑市場規模最大、成長最快的雙重角色。

亞太地區是全球第二大區域市場。中國、印度和澳洲憑藉大規模的畜牧業規模以及產量成長、養殖現代化和標準化飼料使用量增加等持續成長要素,推動了市場需求。 2025年8月,帝斯曼-菲美尼奇在印度賈德切拉開設了一家新的動物營養與健康工廠,為該地區建立了「Mycofix」的在地化生產系統。這體現了公司對長期市場需求的信心以及在地化供應鏈優勢。由於動物飼料量的成長和畜群現代化,該地區的商業基礎正從先進的酪農系統擴展到其他領域,因此在反芻動物飼料添加劑市場中扮演著重要角色。雖然不同規模農場的採用情況有所不同,但整體趨勢是正面的,有組織的生產規模不斷擴大,越來越多的生產者正從基礎補充劑轉向功能性營養方案。

預計歐洲市場將保持穩定成長,這主要得益於其對飼料安全、動物健康和環境績效的嚴格監管。這些因素使得歐洲成為優質飼料添加劑的主要市場,因為合規通常需要強大技術支援和經證實有效性的產品。南美洲市場也預計將維持穩定成長,其中以巴西和阿根廷為首,兩國以出口為導向的牛肉和乳牛生產體係正在推動效率和規模的提升。儘管面臨基礎設施不足和進口依賴度高等挑戰,中東和非洲市場預計仍將保持適度成長。然而,這些地區的一些酪農和育肥產業叢集正在逐步發展。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對牛奶和肉類的需求增加以及生產力提高

- 由於無抗生素生產方式的出現,對功能性食品添加劑的需求正在增加。

- 減少甲烷排放帶來的經濟效益正在提高特種添加劑的盈利。

- 酪農和育肥牧場精準飼餵技術的推廣

- 擴大商業農場幼畜營養計劃

- 擴大管腔健康和微生物組調控解決方案的應用

- 市場限制因素

- 特殊添加劑與傳統預混合料的成本比較

- 飼料原料價格的波動給飼料攪拌商的利潤率帶來了壓力。

- 這些動物在大規模養殖群體之外的商業性推廣進展緩慢。

- 新活性成分的核准和標籤要求延長

- 技術展望

- 監理情勢

- 波特五力分析

第5章 市場規模與成長預測

- 添加劑

- 抗氧化劑

- 富馬酸

- 乳酸

- 丙酸

- 其他抗氧化劑

- 胺基酸

- 離胺酸

- 甲硫胺酸

- 蘇胺酸

- 色氨酸

- 其他胺基酸

- 抗生素

- 巴氏桿菌

- 青黴素

- 四環黴素抗生素

- 泰樂菌素

- 其他抗生素

- 抗氧化劑

- 丁基Hydroxyanisole(BHA)

- 二丁基羥基甲苯(BHT)

- 檸檬酸

- 乙氧喹

- 沒食子酸丙酯

- 生育酚

- 其他抗氧化劑

- 粘合劑

- 天然黏合劑

- 合成黏合劑

- 酵素

- 碳水化合物消化酶

- 植酸酶

- 其他酵素

- 調味劑和甜味劑

- 香味

- 甜味劑

- 礦物

- 主要礦物

- 微量礦物質

- 黴菌毒素清除劑

- 粘合劑

- 生物轉化劑

- 植物來源成分

- 精油

- 香草和香辛料

- 其他植物源性物質

- 顏料

- 類胡蘿蔔素

- 薑黃素和螺旋藻

- 益生元

- 果寡糖

- 半乳寡糖

- 菊糖

- 乳果糖

- 甘露聚醣

- 木寡糖

- 其他益生元

- 益生菌

- 雙歧桿菌

- 腸球菌

- 乳酸菌

- 片球菌

- 鏈球菌

- 其他益生菌

- 維他命

- 維生素A

- 維生素B

- 維生素C

- 維生素E

- 其他維生素

- 酵母菌

- 新鮮酵母

- 硒酵母

- 用過的酵母

- 托魯拉乾酵母

- 乳清酵母

- 酵母衍生成分

- 抗氧化劑

- 畜牧業

- 牛

- 牛

- 其他反芻動物

- 按地區

- 非洲

- 埃及

- 肯亞

- 南非

- 其他非洲國家

- 亞太地區

- 澳洲

- 中國

- 印度

- 印尼

- 日本

- 菲律賓

- 韓國

- 泰國

- 越南

- 其他亞太國家

- 歐洲

- 法國

- 德國

- 義大利

- 荷蘭

- 俄羅斯

- 西班牙

- 土耳其

- 英國

- 其他歐洲國家

- 中東

- 伊朗

- 沙烏地阿拉伯

- 其他中東國家

- 北美洲

- 加拿大

- 墨西哥

- 美國

- 其他北美國家

- 南美洲

- 阿根廷

- 巴西

- 智利

- 南美洲其他地區

- 非洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Cargill, Incorporated

- Archer Daniels Midland Company

- DSM-Firmenich

- Evonik Industries AG

- BASF SE

- Alltech, Inc.

- Nutreco NV

- Adisseo France SAS

- Kemin Industries, Inc.

- Ajinomoto Co., Inc.

- Novonesis

- Lallemand Inc.

- Zinpro Corporation

- Elanco Animal Health Incorporated

- FutureFeed

第7章 市場機會與未來展望

According to Mordor Intelligence, the ruminant feed additives market size was valued at USD 9.55 billion in 2025 and is projected to grow from USD 10.01 billion in 2026 to reach USD 12.76 billion by 2031, at a CAGR of 4.97% during the forecast period (2026-2031).

This report is Segmented by Additive (Acidifiers, Amino Acids, Antibiotics, Antioxidants, Minerals, Binders, Enzymes, and More), by Animal (Beef Cattle, Dairy Cattle, and Other Ruminants), and by Geography (Africa, Asia-Pacific, Europe, Middle East, North America, and South America). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Global Ruminant Feed Additives Market Trends and Insights

Rising Demand for Milk and Meat Productivity Gains

The ruminant feed additives market continues to draw its most stable support from the need to improve milk yield, milk solids, growth rates, and feed conversion in commercial herds. Alltech reported that global compound feed production exceeded 1.44 billion metric tons in 2025, and ruminant feed remains one of the areas where specialty additives offer a higher value per ton than standard formulations . In dairy systems, higher-yielding genetics narrow the nutritional gap between what forage can supply and what the animal needs, keeping demand firm for protected amino acids, minerals, vitamins, and rumen support products. Productivity targets are also becoming more closely linked to sustainability targets because higher output per animal lowers the emissions intensity of each kilogram of milk or meat produced. That combination reinforces the role of premium nutrition programs and keeps the ruminant feed additives market tied to structural efficiency goals rather than short-term feed cycles alone.

Antibiotic-Free Production Shifting Demand Toward Functional Additives

The ruminant feed additives market is benefiting from the growing shift toward antibiotic-free production systems in both dairy and beef operations. With the removal or strict limitation of antibiotic growth promoters, producers are seeking alternative solutions to support digestion, gut health, immunity, and consistent performance. A 2025 meta-analysis published in the Journal of Advanced Research reported that non-antibiotic feed additive combinations resulted in statistically significant improvements in livestock growth performance and immune function across various species. This trend is driving increased use of probiotics, prebiotics, phytogenics, enzymes, acidifiers, and multi-component formulations in commercial ruminant diets. The shift is notable as producers are moving away from replacing single ingredients with another single ingredient, instead adopting integrated programs that combine multiple functional modes of action. This approach is increasing the average expenditure per animal in many organized herds and is steering the ruminant feed additives market beyond basic mineral and vitamin supplementation.

High Cost of Specialty Additives Versus Conventional Premixes

The ruminant feed additives market still faces a clear price barrier when specialty products are compared with conventional mineral and vitamin premixes. Evonik Industries AG announced a 10% global net price increase for MetAMINO in March 2026, indicating that protected amino acids and synthetic nutrition remain exposed to production pressures. In smallholder and semi-commercial systems, that price gap matters more because feed budgets are tighter and product returns are harder to measure on an animal-by-animal basis. Producers in those systems often stay with simpler premixes even when performance benefits from specialty formulations are known. The commercial issue is not only affordability, but also proof of value at the farm level, especially where advisory support is limited. This means the ruminant feed additives market can grow faster in cost-sensitive regions only when suppliers pair higher-value products with practical service, clearer response metrics, and more accessible packaging.

Other drivers and restraints analyzed in the detailed report include:

- Methane-Reduction Economics Improving Return on Specialty Additives

- Growth of Young Animal Nutrition Programs in Commercial Herds

- Slower Commercial Adoption Outside Large-Scale Herds

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Amino acids accounted for 20.7% of the ruminant feed additives market share in 2025, making them the largest additive category in the industry. This dominance reflects the consistent use of rumen-protected lysine and methionine in high-producing dairy rations, where protein balance is carefully managed. Key products in this category include Mepron from Evonik Industries AG, Smartamine and MetaSmart from Adisseo France SAS, and AjiPro-L from Ajinomoto Co., Inc. Additionally, vitamins, probiotics, and phytogenics hold significant positions due to their roles in promoting health stability, supporting metabolism, and enabling antibiotic-free feeding practices across diverse herd systems. The evolving category mix indicates that the ruminant feed additives market is increasingly driven by ingredients designed to support specific production or health outcomes, rather than solely by broad inclusion products.

Acidifiers are projected to grow at a compound annual growth rate (CAGR) of 5.8%, the fastest among additive types in the ruminant feed additives market through 2031. This growth is attributed to the adoption of antibiotic-free formulation practices and the increased use of calf starter programs to improve gut health and reduce early digestive stress. Acidifier blends are gaining popularity due to their dual benefits of hygiene control and rumen adaptation, making them valuable across various stages of the production cycle. Additionally, the importance of mycotoxin management and enzyme use is rising as climate variability impacts feed quality and as advanced feeding systems enable better quantification of digestibility improvements. Consequently, the industry is shifting towards multi-functional product portfolios rather than single-purpose ingredients. This trend is driving the development of a broader premium product mix, with growth increasingly focused on categories aligned with health, precision feeding, and sustainability objectives.

Complete Report Scope:

- By Additive

- Acidifiers

- Fumaric Acid

- Lactic Acid

- Propionic Acid

- Other Acidifiers

- Amino Acids

- Lysine

- Methionine

- Threonine

- Tryptophan

- Other Amino Acids

- Antibiotics

- Bacitracin

- Penicillins

- Tetracyclines

- Tylosin

- Other Antibiotics

- Antioxidants

- Butylated Hydroxyanisole (BHA)

- Butylated Hydroxytoluene (BHT)

- Citric Acid

- Ethoxyquin

- Propyl Gallate

- Tocopherols

- Other Antioxidants

- Binders

- Natural Binders

- Synthetic Binders

- Enzymes

- Carbohydrases

- Phytases

- Other Enzymes

- Flavors & Sweeteners

- Flavors

- Sweeteners

- Minerals

- Macrominerals

- Microminerals

- Mycotoxin Detoxifiers

- Binders

- Biotransformers

- Phytogenics

- Essential Oil

- Herbs & Spices

- Other Phytogenics

- Pigments

- Carotenoids

- Curcumin & Spirulina

- Prebiotics

- Fructo Oligosaccharides

- Galacto Oligosaccharides

- Inulin

- Lactulose

- Mannan Oligosaccharides

- Xylo Oligosaccharides

- Other Prebiotics

- Probiotics

- Bifidobacteria

- Enterococcus

- Lactobacilli

- Pediococcus

- Streptococcus

- Other Probiotics

- Vitamins

- Vitamin A

- Vitamin B

- Vitamin C

- Vitamin E

- Other Vitamins

- Yeast

- Live Yeast

- Selenium Yeast

- Spent Yeast

- Torula Dried Yeast

- Whey Yeast

- Yeast Derivatives

- Acidifiers

- By Animal

- Beef Cattle

- Dairy Cattle

- Other Ruminants

- By Geography

- Africa

- Egypt

- Kenya

- South Africa

- Rest of Africa

- Asia-Pacific

- Australia

- China

- India

- Indonesia

- Japan

- Philippines

- South Korea

- Thailand

- Vietnam

- Rest of Asia-Pacific

- Europe

- France

- Germany

- Italy

- Netherlands

- Russia

- Spain

- Turkey

- United Kingdom

- Rest of Europe

- Middle East

- Iran

- Saudi Arabia

- Rest of Middle East

- North America

- Canada

- Mexico

- United States

- Rest of North America

- South America

- Argentina

- Brazil

- Chile

- Rest of South America

- Africa

Geography Analysis

North America held 38.0% of the ruminant feed additives market share in 2025 and is also projected to grow with the fastest regional CAGR of 6.1% through 2031. That leadership is unusual for a mature region, but it aligns with the structure of the ruminant feed additives market, as North America combines large dairy farms, large feedlots, high additive penetration, and greater readiness for specialty products. The United States drives most of that demand because herd scale, commercial nutrition services, and environmental pressure have all moved in the same direction. Canada adds further depth to the region, as organized dairy systems and regulatory development support the adoption of specialty additives. Mexico remains an important growth pocket because dairy and beef operations are becoming more commercial and more connected to formal premix supply. These conditions keep North America in a dual role as the largest and fastest-growing regional contributor to the ruminant feed additives market.

Asia-Pacific is the second-largest regional market. China, India, and Australia drive demand due to their large herd bases and steady growth factors, including output expansion, modernization, and increased use of formal feed. In August 2025, DSM-Firmenich inaugurated a new Animal Nutrition and Health plant in Jadcherla, India, to locally produce Mycofix for the region, demonstrating confidence in long-term demand and the benefits of a localized supply chain. The region plays a significant role in the ruminant feed additives market, as rising animal protein consumption and herd modernization are expanding the commercial base beyond advanced dairy systems. While adoption varies across farm sizes, the overall trend is positive, with organized production growing and more producers transitioning from basic supplementation to functional nutrition programs.

Europe is projected to grow steadily, driven by stringent regulations on feed safety, animal health, and environmental performance. These factors make Europe a key market for premium additives, as compliance often requires products with robust technical support and proven efficacy. South America is also projected to experience steady growth, led by Brazil and Argentina, where export-oriented beef and dairy systems are enhancing efficiency and scale. Africa and the Middle East are projected to grow at a moderate pace, though both regions face challenges such as limited infrastructure and higher import dependency. However, selected dairy and feedlot clusters in these regions are gradually developing.

- Cargill, Incorporated

- Archer Daniels Midland Company

- DSM-Firmenich

- Evonik Industries AG

- BASF SE

- Alltech, Inc.

- Nutreco N.V.

- Adisseo France SAS

- Kemin Industries, Inc.

- Ajinomoto Co., Inc.

- Novonesis

- Lallemand Inc.

- Zinpro Corporation

- Elanco Animal Health Incorporated

- FutureFeed

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for milk and meat productivity gains

- 4.2.2 Antibiotic-free production shifting demand toward functional additives

- 4.2.3 Methane-reduction economics improving return on specialty additives

- 4.2.4 Expansion of precision feeding in dairy and feedlot operations

- 4.2.5 Growth of young animal nutrition programs in commercial herds

- 4.2.6 Rising use of rumen health and microbiome modulation solutions

- 4.3 Market Restraints

- 4.3.1 High cost of specialty additives versus conventional premixes

- 4.3.2 Feed ingredient price volatility compressing formulator margins

- 4.3.3 Slower commercial adoption outside large-scale herds

- 4.3.4 Lengthy approval and labeling requirements for novel actives

- 4.4 Technological Outlook

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Buyers

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Additive

- 5.1.1 Acidifiers

- 5.1.1.1 Fumaric Acid

- 5.1.1.2 Lactic Acid

- 5.1.1.3 Propionic Acid

- 5.1.1.4 Other Acidifiers

- 5.1.2 Amino Acids

- 5.1.2.1 Lysine

- 5.1.2.2 Methionine

- 5.1.2.3 Threonine

- 5.1.2.4 Tryptophan

- 5.1.2.5 Other Amino Acids

- 5.1.3 Antibiotics

- 5.1.3.1 Bacitracin

- 5.1.3.2 Penicillins

- 5.1.3.3 Tetracyclines

- 5.1.3.4 Tylosin

- 5.1.3.5 Other Antibiotics

- 5.1.4 Antioxidants

- 5.1.4.1 Butylated Hydroxyanisole (BHA)

- 5.1.4.2 Butylated Hydroxytoluene (BHT)

- 5.1.4.3 Citric Acid

- 5.1.4.4 Ethoxyquin

- 5.1.4.5 Propyl Gallate

- 5.1.4.6 Tocopherols

- 5.1.4.7 Other Antioxidants

- 5.1.5 Binders

- 5.1.5.1 Natural Binders

- 5.1.5.2 Synthetic Binders

- 5.1.6 Enzymes

- 5.1.6.1 Carbohydrases

- 5.1.6.2 Phytases

- 5.1.6.3 Other Enzymes

- 5.1.7 Flavors & Sweeteners

- 5.1.7.1 Flavors

- 5.1.7.2 Sweeteners

- 5.1.8 Minerals

- 5.1.8.1 Macrominerals

- 5.1.8.2 Microminerals

- 5.1.9 Mycotoxin Detoxifiers

- 5.1.9.1 Binders

- 5.1.9.2 Biotransformers

- 5.1.10 Phytogenics

- 5.1.10.1 Essential Oil

- 5.1.10.2 Herbs & Spices

- 5.1.10.3 Other Phytogenics

- 5.1.11 Pigments

- 5.1.11.1 Carotenoids

- 5.1.11.2 Curcumin & Spirulina

- 5.1.12 Prebiotics

- 5.1.12.1 Fructo Oligosaccharides

- 5.1.12.2 Galacto Oligosaccharides

- 5.1.12.3 Inulin

- 5.1.12.4 Lactulose

- 5.1.12.5 Mannan Oligosaccharides

- 5.1.12.6 Xylo Oligosaccharides

- 5.1.12.7 Other Prebiotics

- 5.1.13 Probiotics

- 5.1.13.1 Bifidobacteria

- 5.1.13.2 Enterococcus

- 5.1.13.3 Lactobacilli

- 5.1.13.4 Pediococcus

- 5.1.13.5 Streptococcus

- 5.1.13.6 Other Probiotics

- 5.1.14 Vitamins

- 5.1.14.1 Vitamin A

- 5.1.14.2 Vitamin B

- 5.1.14.3 Vitamin C

- 5.1.14.4 Vitamin E

- 5.1.14.5 Other Vitamins

- 5.1.15 Yeast

- 5.1.15.1 Live Yeast

- 5.1.15.2 Selenium Yeast

- 5.1.15.3 Spent Yeast

- 5.1.15.4 Torula Dried Yeast

- 5.1.15.5 Whey Yeast

- 5.1.15.6 Yeast Derivatives

- 5.1.1 Acidifiers

- 5.2 By Animal

- 5.2.1 Beef Cattle

- 5.2.2 Dairy Cattle

- 5.2.3 Other Ruminants

- 5.3 By Geography

- 5.3.1 Africa

- 5.3.1.1 Egypt

- 5.3.1.2 Kenya

- 5.3.1.3 South Africa

- 5.3.1.4 Rest of Africa

- 5.3.2 Asia-Pacific

- 5.3.2.1 Australia

- 5.3.2.2 China

- 5.3.2.3 India

- 5.3.2.4 Indonesia

- 5.3.2.5 Japan

- 5.3.2.6 Philippines

- 5.3.2.7 South Korea

- 5.3.2.8 Thailand

- 5.3.2.9 Vietnam

- 5.3.2.10 Rest of Asia-Pacific

- 5.3.3 Europe

- 5.3.3.1 France

- 5.3.3.2 Germany

- 5.3.3.3 Italy

- 5.3.3.4 Netherlands

- 5.3.3.5 Russia

- 5.3.3.6 Spain

- 5.3.3.7 Turkey

- 5.3.3.8 United Kingdom

- 5.3.3.9 Rest of Europe

- 5.3.4 Middle East

- 5.3.4.1 Iran

- 5.3.4.2 Saudi Arabia

- 5.3.4.3 Rest of Middle East

- 5.3.5 North America

- 5.3.5.1 Canada

- 5.3.5.2 Mexico

- 5.3.5.3 United States

- 5.3.5.4 Rest of North America

- 5.3.6 South America

- 5.3.6.1 Argentina

- 5.3.6.2 Brazil

- 5.3.6.3 Chile

- 5.3.6.4 Rest of South America

- 5.3.1 Africa

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Cargill, Incorporated

- 6.4.2 Archer Daniels Midland Company

- 6.4.3 DSM-Firmenich

- 6.4.4 Evonik Industries AG

- 6.4.5 BASF SE

- 6.4.6 Alltech, Inc.

- 6.4.7 Nutreco N.V.

- 6.4.8 Adisseo France SAS

- 6.4.9 Kemin Industries, Inc.

- 6.4.10 Ajinomoto Co., Inc.

- 6.4.11 Novonesis

- 6.4.12 Lallemand Inc.

- 6.4.13 Zinpro Corporation

- 6.4.14 Elanco Animal Health Incorporated

- 6.4.15 FutureFeed

7 Market Opportunities and Future Outlook

2026-2030年全球反芻動物甲烷減量市場

2026-2030年全球反芻動物甲烷減量市場 2026-2034年反芻動物甲烷減量全球市場規模、佔有率、趨勢和成長分析報告

2026-2034年反芻動物甲烷減量全球市場規模、佔有率、趨勢和成長分析報告 全球反芻動物甲烷減量市場

全球反芻動物甲烷減量市場 反芻動物甲烷減量市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

反芻動物甲烷減量市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測