|

市場調查報告書

商品編碼

2072953

歐洲灌溉幫浦:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年)Europe Irrigation Pumps - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

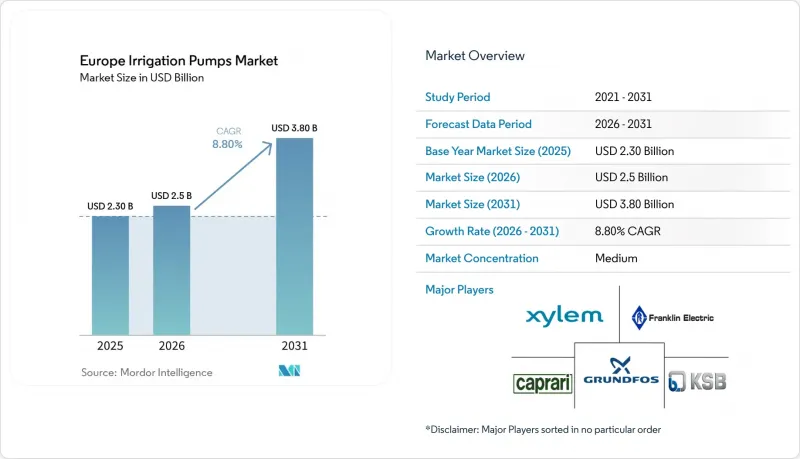

根據 Mordor Intelligence 預測,歐洲灌溉幫浦市場規模預計在 2025 年達到 23 億美元,2026 年達到 25 億美元,到 2031 年達到 38 億美元,2026 年至 2031 年的複合年成長率為 8.80%。

本報告按產品類型(離心式幫浦、潛水泵、容積式泵、渦流泵)、動力來源(商用電源、柴油、太陽能、太陽能-柴油混合動力、太陽能-電池混合動力)和地區(德國、英國、法國、西班牙、義大利、俄羅斯和其他歐洲國家)進行細分。市場預測以美元計價。

歐洲灌溉幫浦市場趨勢與洞察

為因應缺水問題,對老舊灌溉水泵維修。

在歐洲灌溉幫浦市場,水資源壓力不再被視為季節性的運作問題。在水資源本已緊張的流域,水資源壓力正成為推動設備現代化改造的行政觸發因素。歐盟聯合研究中心(JRC)在2026年2月發布的報告顯示,在歐洲大部分地區,人類活動將消耗10%至50%的可再生淡水資源,其中南部和地中海地區的過度用水壓力尤其巨大。在這種情況下,亟需更換那些缺乏流量測量功能、難以滿足當前監控需求的過時恆速幫浦。事實上,生產商並非僅僅購買新泵,而是用能夠追蹤流量、支援控制功能並符合更嚴格的流域管理法規的系統來替換過時的灌溉設備。

在通用農業政策(CAP)支持下,用於灌溉現代化的支出

通用農業政策(CAP)的支出週期仍然是歐洲灌溉幫浦市場最主要的支撐力量之一。 2021年至2027年期間,該框架下的計畫投資額達314億歐元(339億美元),涵蓋歐盟和各國根據第73條和第74條對農業和灌溉項目提供的聯合融資。 2025年的提案在下一個政策週期中繼續強調水資源管理和土壤健康,顯示支持將具有連續性,而非僅限於單一時期。法國、西班牙、德國和義大利仍然是國家資金投入最活躍的中心,因為它們從通用農業政策(CAP)獲得了最多的支持,並正在推動大規模的灌溉現代化計畫。關鍵在於,在獲得補貼之前,通常必須安裝水錶裝置。這項規定確保了老舊泵浦設備的更換遵循既定的計劃,而不是完全自願的支出週期。

中小農場幫浦系統的前期資本投入較高

在歐洲灌溉幫浦市場,資本成本仍是限制需求的最大因素。升級包括水泵、變頻驅動裝置、計量設備和安裝在內的整個系統,對於面臨季節性現金流緊張的農場來說,仍然是一筆不小的負擔。儘管歐盟法規2021/2115為符合條件的投資成本提供補貼,但剩餘的自付費用仍給許多中小農場的實際機械購置預算帶來壓力,尤其是在中歐和東歐成員國。補貼的償還時間也是一個問題,因為補貼有時會在做出安裝決定很久之後才會發放。供應商正在透過模組化泵站方案來解決這個問題,但成本降低仍然不足,而且小規模企業難以獲得承包升級服務。因此,模組化泵站的普及主要集中在大規模生產商、合作社和灌溉組織能夠分攤資本成本的地區,因為這些地區擁有更多的灌溉面積和用戶。

細分市場分析

到2025年,離心式幫浦將佔據最大的市場佔有率,達到歐洲灌溉泵市場的71.2%。這一地位反映了離心泵在農田作物和園藝應用中的廣泛使用,包括地表取水、明渠灌溉以及與水井相結合的農田灌溉系統。在那些需要熟悉且靈活的解決方案,能夠適應各種揚程和流量條件,且不局限於特定作物系統的地區,離心泵的需求最為旺盛。離心式幫浦,特別是垂直渦輪泵和分離式離心泵,將繼續被應用於大規模公共和聯合灌溉工程。 Caprari SpA公司在2024年透過義大利Scigliati水廠計畫展示了離心幫浦的這項優勢。該計畫安裝了五台客製化的立式軸系離心泵,使流域的灌溉流量提高了50%以上。

在歐洲灌溉幫浦市場,容積式幫浦市場預計將在2026年至2031年間以8.2%的複合年成長率成長。這一成長主要與比主流離心泵類別更為專業的應用領域相關。葡萄園、漿果園、果園和溫室系統的精準施肥灌溉需要可控的小流量計量,這推動了隔膜泵和單軸螺旋泵浦的普及。此外,歐洲灌溉泵市場對再生水灌溉的興趣日益濃厚,這促進了渦流泵和固態物料應用等特殊應用場景的發展,因為標準葉輪系統在這些場景下容易快速磨損。潛水泵浦保持著穩定的第二大市場佔有率,因為深井灌溉在西班牙和義大利仍然十分重要。然而,更換需求正轉向更有效率、更耐用的機型。總而言之,產品需求正在分化為兩個細分市場:主流的大流量離心式幫浦,以及快速成長的、以精準計量、再生水和保護性栽培為中心的專業應用領域。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 因缺水而對老舊灌溉水泵維修。

- 通用農業政策(CAP)下的灌溉現代化支出

- 精準灌溉和與變頻驅動裝置相連的水泵自動化。

- 太陽能發電和抽水蓄能混合發電的經濟效益正在提高。

- 利用再生水進行灌溉正在催生維修的需求。

- 葡萄園、果園和溫室的灌溉強度

- 市場限制因素

- 中小農場幫浦系統的初始資本投資成本較高

- 地下水取水許可證和取水限制

- 各國電網和混合系統合規性的複雜性。

- 由於節水效應,淨用水量的成長將受到抑制。

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 依產品類型

- 離心式幫浦

- 端吸式地面泵

- 分離式泵浦

- 直立式渦輪泵

- 潛水泵

- 博霍爾泵

- 潛水式多級泵

- 容積式泵

- 隔膜泵

- 螺桿泵

- 渦流泵

- 離心式幫浦

- 透過動力來源

- 商用電源泵

- 柴油泵

- 太陽能水泵

- 混合式(太陽能/柴油)和太陽能/電池驅動水泵

- 按地區

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 其他歐洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Grundfos Holding A/S

- Xylem Inc.

- KSB SE & Co. KGaA

- Franklin Electric Co., Inc.

- Caprari SpA

- Wilo SE

- Calpeda SpA

- Pentair plc

- Ebara Corporation

- Flowserve Corporation

- Sulzer Ltd.

- Pedrollo SpA

- DAB Pumps SpA

- SAER Elettropompe SpA

- ANDRITZ AG

第7章 市場機會與未來展望

According to Mordor Intelligence, the europe irrigation pumps market size is projected to be USD 2.30 billion in 2025, USD 2.5 billion in 2026, and reach USD 3.80 billion by 2031, growing at a CAGR of 8.80% from 2026 to 2031.

This report is Segmented by Product Type (Centrifugal Pumps, Submersible Pumps, Positive Displacement Pumps, and Vortex Pumps), by Power Source (Grid-Electric, Diesel, Solar, and Hybrid Solar-Diesel and Solar-Battery), and by Geography (Germany, United Kingdom, France, Spain, Italy, Russia, and Rest of Europe). The Market Forecasts are Provided in Terms of Value in USD.

Europe Irrigation Pumps Market Trends and Insights

Water-Scarcity-Driven Retrofit of Legacy Irrigation Pumps

Water stress is no longer treated as a seasonal operating issue in the Europe irrigation pumps market. It is becoming an administrative trigger for equipment renewal in basins where abstraction is already under pressure. The Joint Research Centre reported in February 2026 that human activity appropriates 10% to 50% of renewable freshwater in most European regions, while southern and Mediterranean areas face the greatest overuse pressure. These conditions favor replacement of older fixed-speed assets that lack metering and cannot easily meet current monitoring needs. In practice, growers are not just buying a new pump. They are replacing an older irrigation setup with a system that can track flow, support control functions, and fit within stricter basin management rules.

Common Agricultural Policy (CAP)-Backed Irrigation Modernization Spending

The Common Agricultural Policy spending cycle remains one of the clearest supports for the Europe irrigation pumps market. Planned investment under the 2021 to 2027 framework reached EUR 31.4 billion (USD 33.9 billion), covering European Union and national co-financing for farm and irrigation projects under Articles 73 and 74. The 2025 proposal also kept water management and soil health visible in the next policy cycle, signaling continuity rather than a one-period support window. France, Spain, Germany, and Italy remain the most active national funding centers because they are the largest recipients of Common Agricultural Policy support and also run sizable irrigation modernization pipelines. A key point is that metering is often required before subsidy approval. That rule pushes older pump fleets onto a regulatory replacement schedule rather than a purely voluntary spending cycle.

High Upfront Pump-System Capital Expenditure for Small and Mid-Size Farms

Capital cost remains the clearest demand restraint in the Europe irrigation pumps market. A full system upgrade that includes the pump, variable frequency drive, metering hardware, and installation can still place a heavy burden on farms that operate with tight seasonal cash flow. Regulation (European Union) 2021/2115 allows support for eligible investment costs, but the remaining co-payment still stretches practical machinery budgets in many small and mid-size farms, especially in central and eastern member states. The timing of reimbursement is part of the problem because support can arrive well after installation decisions must be made. Suppliers have responded with modular pump station formats, but the cost reduction has not yet been enough to bring turnkey upgrades within easy reach for the smallest operators. As a result, adoption is strongest where larger growers, cooperatives, and irrigation bodies can spread capital costs across more hectares or more users.

Other drivers and restraints analyzed in the detailed report include:

- Precision Irrigation and Variable Frequency Drive-Linked Pump Automation

- Solar and Hybrid Pumping Economics Improving

- Groundwater Permitting and Abstraction Caps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Centrifugal pumps held the largest market share and accounted for 71.2% of the Europe irrigation pumps market share in 2025. Their position reflects broad utility across surface abstraction, open-channel irrigation, and borehole-linked farm systems in both field crops and horticulture. Demand is strongest where operators need a familiar and flexible solution that can serve different heads and flow conditions without narrowing use to one crop system. Large public and consortium irrigation schemes also continue to rely on centrifugal formats, especially vertical turbine and split-case designs. Caprari S.p.A. illustrated this role in 2024 through its Scigliati plant project in Italy, which lifted basin irrigation flow capacity by more than 50% with 5 customized vertical lineshaft units.

The Europe irrigation pumps market size for positive displacement pumps is projected to expand at an 8.2% CAGR from 2026 to 2031. This growth is tied to uses that are more specialized than the main centrifugal category. Precision fertigation in vineyards, berry crops, orchards, and greenhouse systems needs controlled low-volume dosing, and that favors diaphragm and progressive cavity pump formats. The Europe irrigation pumps market is also seeing wider interest in reclaimed-water irrigation, and that supports niche use cases for vortex and solids-tolerant applications where standard impeller systems can wear faster. Submersible pumps remain a stable second-tier category because deep-well irrigation still matters in Spain and Italy, even as replacement demand shifts toward higher-efficiency and better-protected units. Taken together, product demand is separating into a high-volume mainstream centrifugal base and a faster specialty layer built around precision dosing, reclaimed water, and protected cultivation.

Complete Report Scope:

- By Product Type

- Centrifugal Pumps

- End-suction Surface Pumps

- Split-case Pumps

- Vertical Turbine Pumps

- Submersible Pumps

- Borehole Pumps

- Submersible Multistage Pumps

- Positive Displacement Pumps

- Diaphragm Pumps

- Progressive Cavity Pumps

- Vortex Pumps

- Centrifugal Pumps

- By Power Source

- Grid-electric Pumps

- Diesel Pumps

- Solar Pumps

- Hybrid Solar-Diesel and Solar-Battery Pumps

- By Geography

- Germany

- United Kingdom

- France

- Spain

- Italy

- Russia

- Rest of Europe

List of Companies Covered in this Report:

- Grundfos Holding A/S

- Xylem Inc.

- KSB SE & Co. KGaA

- Franklin Electric Co., Inc.

- Caprari S.p.A.

- Wilo SE

- Calpeda S.p.A.

- Pentair plc

- Ebara Corporation

- Flowserve Corporation

- Sulzer Ltd.

- Pedrollo S.p.A.

- DAB Pumps S.p.A.

- SAER Elettropompe S.p.A.

- ANDRITZ AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Water-scarcity-driven retrofit of legacy irrigation pumps

- 4.2.2 Common Agricultural Policy (CAP)-backed irrigation modernization spending

- 4.2.3 Precision irrigation and variable frequency drive-linked pump automation

- 4.2.4 Solar and hybrid pumping economics improving

- 4.2.5 Reclaimed-water irrigation creates retrofit demand

- 4.2.6 Vineyard, orchard, and greenhouse irrigation intensity

- 4.3 Market Restraints

- 4.3.1 High upfront pump-system capital expenditure for small and mid-size farms

- 4.3.2 Groundwater permitting and abstraction caps

- 4.3.3 Country-by-country grid and hybrid-system compliance complexity

- 4.3.4 Water-savings rebound limits net pumping-volume growth

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Centrifugal Pumps

- 5.1.1.1 End-suction Surface Pumps

- 5.1.1.2 Split-case Pumps

- 5.1.1.3 Vertical Turbine Pumps

- 5.1.2 Submersible Pumps

- 5.1.2.1 Borehole Pumps

- 5.1.2.2 Submersible Multistage Pumps

- 5.1.3 Positive Displacement Pumps

- 5.1.3.1 Diaphragm Pumps

- 5.1.3.2 Progressive Cavity Pumps

- 5.1.4 Vortex Pumps

- 5.1.1 Centrifugal Pumps

- 5.2 By Power Source

- 5.2.1 Grid-electric Pumps

- 5.2.2 Diesel Pumps

- 5.2.3 Solar Pumps

- 5.2.4 Hybrid Solar-Diesel and Solar-Battery Pumps

- 5.3 By Geography

- 5.3.1 Germany

- 5.3.2 United Kingdom

- 5.3.3 France

- 5.3.4 Spain

- 5.3.5 Italy

- 5.3.6 Russia

- 5.3.7 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Grundfos Holding A/S

- 6.4.2 Xylem Inc.

- 6.4.3 KSB SE & Co. KGaA

- 6.4.4 Franklin Electric Co., Inc.

- 6.4.5 Caprari S.p.A.

- 6.4.6 Wilo SE

- 6.4.7 Calpeda S.p.A.

- 6.4.8 Pentair plc

- 6.4.9 Ebara Corporation

- 6.4.10 Flowserve Corporation

- 6.4.11 Sulzer Ltd.

- 6.4.12 Pedrollo S.p.A.

- 6.4.13 DAB Pumps S.p.A.

- 6.4.14 SAER Elettropompe S.p.A.

- 6.4.15 ANDRITZ AG

7 Market Opportunities and Future Outlook

南美洲灌溉幫浦:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

南美洲灌溉幫浦:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年) 農業泵浦市場-全球產業規模、佔有率、趨勢、機會和預測:按類型、材料類型、動力來源、馬力、揚程、最終用戶、地區和競爭格局分類,2021-2031年

農業泵浦市場-全球產業規模、佔有率、趨勢、機會和預測:按類型、材料類型、動力來源、馬力、揚程、最終用戶、地區和競爭格局分類,2021-2031年 電動背負式噴霧器市場:按動力來源、應用、最終用戶和分銷管道分類 - 全球預測(2026-2032 年)

電動背負式噴霧器市場:按動力來源、應用、最終用戶和分銷管道分類 - 全球預測(2026-2032 年) 可調式流量微型噴灌:全球市佔率和排名、總銷售額和需求預測(2025-2031 年)

可調式流量微型噴灌:全球市佔率和排名、總銷售額和需求預測(2025-2031 年) 全球灌溉幫浦市場

全球灌溉幫浦市場 2030 年農業泵浦市場預測:按類型、材料類型、馬力、泵浦頭尺寸、動力來源、最終用戶和地區進行的全球分析全球農用幫浦市場到 2030 年全球農用泵市場預測:按產品、動力來源、應用、最終用戶和地區進行分析

2030 年農業泵浦市場預測:按類型、材料類型、馬力、泵浦頭尺寸、動力來源、最終用戶和地區進行的全球分析全球農用幫浦市場到 2030 年全球農用泵市場預測:按產品、動力來源、應用、最終用戶和地區進行分析