|

市場調查報告書

商品編碼

2065622

南美洲灌溉幫浦:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)South America Irrigation Pumps - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

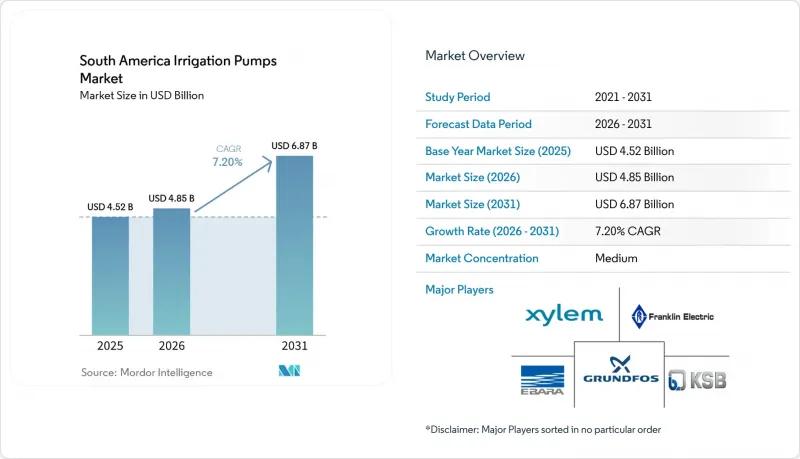

據 Mordor Intelligence 稱,2025 年南美灌溉泵市場價值為 45.2 億美元,預計到 2031 年將從 2026 年的 48.5 億美元成長至 68.7 億美元,預測期(2026-2031 年)複合年成長率為 7.20%。

本報告按產品類型(離心式幫浦、潛水泵、容積式泵、渦流泵)、動力來源(商用動力泵、柴油泵、太陽能泵、太陽能-柴油混合泵、太陽能-電池混合泵)和地區(巴西、阿根廷、智利、秘魯、哥倫比亞及其他南美國家)進行細分。市場預測以美元計價。

南美洲灌溉幫浦市場趨勢與洞察

灌溉網路的擴建與現代化

在南美洲,灌溉面積的擴張仍是灌溉幫浦市場最顯著的成長要素。這是因為新建的管道、抽水站和農田系統從一開始就需要各種各樣的水泵。聯合國糧食及農業組織(糧農組織)的報告顯示,過去十年間,南美洲的灌溉面積穩步成長,為作物輪作和出口導向農業的灌溉設施長期規劃提供了支持。秘魯政府已宣布了22個灌溉項目,主要主導官民合作關係(PPP)模式實施,目標是到2025年新增100萬公頃灌溉面積,總投資額達240億美元。巴西也正在透過新的公共計畫和州級框架擴大灌溉投資的製度基礎,這使得商業農場和小規模的水泵採購更加穩定。此外,每個新建的灌溉網路都會形成一個長期的服務週期,用於泵站升級、控制系統維護和設備更換。這使得垂直整合的供應商能夠比那些只專注於初始銷售的公司獲得更穩定的售後市場機會。這一趨勢意味著南美洲灌溉幫浦市場不僅與新計畫密切相關,而且與持續的維護支出也密切相關。

水資源短缺正在推動對灌溉基礎設施的需求。

水資源短缺正使許多農場的灌溉支出從單純提高產量的選項轉變為風險管理的必要措施,這正在改變南美洲灌溉水泵的需求結構。根據評估能力計畫(ACAPS)的數據,2023-2024年期間,巴西59%的地區將受到乾旱影響,凸顯了生產者為何更加重視穩定的供水和已安裝的抽水能力。在巴西,2023年至2025年的持續乾旱將促使更多易受乾旱影響的州的農民轉向全灌溉或部分灌溉的生產系統,從而增加了他們對鑽井泵和潛水泵的需求。秘魯沿海地區和阿根廷乾旱地區也面臨類似的壓力,可靠的抽水設備正成為種植規劃的核心要素,而不僅僅是備用方案。另一個不利的影響是:含水層水位下降可能會縮短潛水泵浦設備的使用壽命,從而可能增加每年的更換需求。換句話說,雖然乾旱會促進短期設備銷售,但也會為某些泵送系統帶來更惡劣的運作環境。

高昂的初始投資成本

高昂的初始投資成本仍然是抑制需求的一大因素,尤其對於那些需要高揚程博霍爾灌溉系統或大型離心式幫浦的農民而言,他們往往無法獲得補貼貸款。實際上,這個問題在哥倫比亞和阿根廷的中小農戶中最為嚴重,因為在這些國家,水泵投資經常與營運資金需求和季節性融資壓力相衝突。因此,在南美洲灌溉幫浦市場,即使缺水導致灌溉需求增加,並非所有潛在需求都能轉化為實際購買。在巴西一些公共貸款計畫較為完善的地區,這種資金籌措缺口並不那麼明顯,但如果借款人超過優惠項目的門檻或無法提供貸款機構要求的抵押品,仍然會阻礙產品的普及。因此,存在著區域差異,大規模商業農場更早升級設備,而小規模企業則推遲設備更換或新安裝。儘管大型農場的需求強勁,但這種不平衡正在減緩基本客群的成長。

細分市場分析

到2025年,離心式幫浦將佔據最大的市場佔有率,達到49.9%,這一主導地位反映了其與巴西和阿根廷等糧食和甘蔗大規模產區廣泛採用的地面灌溉系統和管道連接佈局的兼容性。在南美洲灌溉幫浦市場,端吸式和剖分式離心式幫浦仍然是高流量和水平輸水優先於緊湊安裝的應用領域的標準選擇。立式渦輪泵在秘魯沿海的灌溉計畫中也發揮著重要作用,這些系統通常需要從河流取水口或含水層抽水並將其輸送到管道網路。潛水泵在地下水開發不斷擴大的地區,尤其是在秘魯的山谷和巴西東北部的乾旱地區,使用量正在增加。雖然渦流泵的市場規模仍然較小,但在水中含有泥沙且傳統地面泵運作受限的地區,它們仍然發揮著至關重要的作用。

在南美洲灌溉幫浦市場,容積式幫浦預計到2031年將以5.2%的複合年成長率成長,成為預測期內成長最快的產品類型。這一成長與施肥灌溉、滴灌系統和地下灌溉系統密切相關,在這些系統中,精確的流量控制比品質傳遞更為重要。秘魯在2025年批准了15個區域灌溉項目,重點是技術灌溉。這推動了對適用於可控噴灑系統的泵浦的需求。秘魯和智利的出口導向園藝農業也使容積式泵浦受益,這兩個國家對高用水效率的追求推動了高價值灌溉設備的應用。因此,在供水精度與作物品質和肥料管理密切相關的應用領域,南美洲灌溉泵浦產業正經歷更快速的成長。此外,在水力發電性能認證至關重要的專案中,符合國際標準化組織(ISO)9906標準變得越來越重要,這使主要供應商在具有嚴格規格要求的競標中獲得了競爭優勢。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 灌溉網路的擴建與現代化

- 水資源短缺正在推動對灌溉基礎設施的需求。

- 政府支持的泵浦融資支持計劃

- 在離網農場引進太陽能發電和混合水泵系統

- 從柴油泵過渡到太陽能泵

- 公私合營模式主導的農村水利基礎建設聯合投資

- 市場限制因素

- 高昂的初始設備投資成本

- 農村電網的限制阻礙了電動水泵的推廣應用。

- 流域形狀和水文限制

- 水權分配與監管障礙

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 依產品類型

- 離心式幫浦

- 潛水泵

- 容積式泵

- 渦流泵

- 透過動力來源

- 商用電源泵

- 柴油泵

- 太陽能水泵

- 混合式(太陽能/柴油)和太陽能/電池驅動水泵

- 按地區

- 巴西

- 阿根廷

- 智利

- 秘魯

- 哥倫比亞

- 其他南美國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Franklin Electric Co., Inc.

- KSB SE & Co. KGaA

- Grundfos Holding A/S

- Xylem Inc.

- Ebara Corporation

- Wilo SE

- Flowserve Corporation

- Sulzer Ltd

- ITT Inc.

- Jimenez Motores e Sistemas de Irrigacao Ltda

- Pentair plc

- Ruhrpumpen GmbH

- Dover Corporation

- IDEX Corporation

- Hidromecanica Germek Ltda.

第7章 市場機會與未來展望

According to Mordor Intelligence, the south america irrigation pumps market size was valued at USD 4.52 billion in 2025 and is estimated to grow from USD 4.85 billion in 2026 to reach USD 6.87 billion by 2031, at a CAGR of 7.20% during the forecast period (2026-2031).

This report is Segmented by Product Typem(Centrifugal Pumps, Submersible Pumps, Positive Displacement Pumps, and Vortex Pumps), by Power Source (Grid-Electric Pumps, Diesel Pumps, Solar Pumps, and Hybrid Solar-Diesel and Solar-Battery Pumps), and by Geography (Brazil, Argentina, Chile, Peru, Colombia, and Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

South America Irrigation Pumps Market Trends and Insights

Irrigation Network Expansion and Modernization

Expansion of irrigated land remains the clearest growth driver for the South America irrigation pumps market because new canals, lift stations, and field systems require a broad mix of pump types from the start. The Food and Agriculture Organization (FAO) showed that South America sustained strong irrigated area growth over the last decade, which supports long planning cycles for irrigation equipment across row crops and export agriculture. Peru's government presented 22 irrigation projects in 2025 with total investment of USD 24 billion, a target of 1 million additional hectares, and a delivery model led mainly by public-private partnerships (PPPs). Brazil also expanded the institutional base for irrigation investment through new public programs and state-level frameworks, which makes pump procurement more repeatable across both commercial farms and smaller operations. Each new network also creates a long service cycle for station upgrades, controls, and replacement units, which gives vertically integrated suppliers a steadier aftermarket opportunity than firms focused only on first-time sales. That pattern is keeping the South America irrigation pumps market tied not only to greenfield projects, but also to recurring maintenance spending.

Water Scarcity Driving Demand for Irrigation Infrastructure

Water stress is shifting irrigation spending from a yield improvement choice into a risk management requirement for many farms, and that is changing the demand profile of the South America irrigation pumps market. According to Assessment Capacities Project (ACAPS), drought conditions affected 59% of Brazil during the 2023 to 2024 cycle, which underlines why producers are placing more weight on secure water access and installed pumping capacity. In Brazil, recurring drought from 2023 through 2025 pushed more farms in exposed states toward fully irrigated or partially irrigated production systems, which increased interest in borehole and submersible units. The same pressure is visible in Peru's coastal belts and in drier parts of Argentina, where dependable pumping is becoming central to crop planning rather than a backup option. A second effect is less favorable, because aquifer drawdown can reduce the working life of submersible installations and raise annual replacement demand. That means drought is supporting near-term equipment sales while also creating a harder operating environment for some pump assets.

High Upfront Capital Costs

High capital cost remains a clear brake on demand, especially where growers need high-head borehole systems or larger centrifugal units and do not qualify for subsidized financing. In practical terms, the issue is strongest for smallholders and medium farms in Colombia and Argentina, where pump investment often competes with working capital needs and seasonal cash flow pressure. The South America irrigation pumps market therefore does not convert all latent demand into purchases, even when water stress makes irrigation more necessary. This funding gap is less severe in parts of Brazil, where public credit programs are more developed, but it still limits adoption where borrowers exceed concessional program thresholds or cannot provide the supporting structure required by lenders. The result is a tiered regional pattern in which larger commercial farms upgrade sooner while smaller operators delay replacement and postpone new installations. That imbalance slows the broadening of the customer base even as demand from large farms remains resilient.

Other drivers and restraints analyzed in the detailed report include:

- Subsidized Government Pump Financing Programs

- Solar and Hybrid Pumping Adoption on Off-Grid Farms

- Rural Grid Limitations Constraining Electric Pump Deployment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Centrifugal pumps held the largest market share at 49.9% in 2025, and that leadership reflects their fit with the surface irrigation systems and canal-linked layouts used across large grain and sugarcane areas in Brazil and Argentina. In the South America irrigation pumps market, end-suction and split-case centrifugal models remain the standard choice where high volumes and horizontal delivery matter more than compact installation. Vertical turbine units also hold an important place in Peru's coastal irrigation projects because those systems often need water lifted from river intakes or aquifers into canal networks. Submersible pumps are gaining use where groundwater development is expanding, especially in Peru's valleys and in drier parts of northeastern Brazil. Vortex pumps remain smaller in volume, but they retain relevance where water carries sediment and basic surface units face operating limits.

The South America irrigation pumps market size for positive displacement pumps is projected to grow at a 5.2% CAGR through 2031, making them the fastest product category over the forecast period. That growth is tied to fertigation, drip systems, and subsurface irrigation layouts where accurate flow control matters more than bulk transfer. Peru approved irrigation projects across 15 regions in 2025 with a technified irrigation focus, which supports demand for pump types suited to controlled application systems. Positive displacement equipment is also benefiting from export-oriented horticulture in Peru and Chile, where water efficiency supports the case for higher-value irrigation hardware. The South America irrigation pumps industry is therefore seeing faster growth in applications where water delivery precision is closely linked to crop quality and fertilizer management. International Organization for Standardization (ISO) 9906 compliance is also becoming more relevant in projects that favor certified hydraulic performance, which gives larger suppliers an advantage in specification-heavy tenders.

List of Companies Covered in this Report:

- Franklin Electric Co., Inc.

- KSB SE & Co. KGaA

- Grundfos Holding A/S

- Xylem Inc.

- Ebara Corporation

- Wilo SE

- Flowserve Corporation

- Sulzer Ltd

- ITT Inc.

- Jimenez Motores e Sistemas de Irrigacao Ltda

- Pentair plc

- Ruhrpumpen GmbH

- Dover Corporation

- IDEX Corporation

- Hidromecanica Germek Ltda.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Irrigation network expansion and modernization

- 4.2.2 Water scarcity driving demand for irrigation infrastructure

- 4.2.3 Subsidized government pump financing programs

- 4.2.4 Solar and hybrid pumping adoption on off-grid farms

- 4.2.5 Diesel-to-solar pump transitions

- 4.2.6 PPP-led co-investment in rural water infrastructure

- 4.3 Market Restraints

- 4.3.1 High upfront capital costs

- 4.3.2 Rural grid limitations constraining electric pump deployment

- 4.3.3 Basin configuration and hydrology constraints

- 4.3.4 Water-right allocation and regulatory barriers

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Centrifugal Pumps

- 5.1.2 Submersible Pumps

- 5.1.3 Positive Displacement Pumps

- 5.1.4 Vortex Pumps

- 5.2 By Power Source

- 5.2.1 Grid-electric Pumps

- 5.2.2 Diesel Pumps

- 5.2.3 Solar Pumps

- 5.2.4 Hybrid Solar-Diesel and Solar-Battery Pumps

- 5.3 By Geography

- 5.3.1 Brazil

- 5.3.2 Argentina

- 5.3.3 Chile

- 5.3.4 Peru

- 5.3.5 Colombia

- 5.3.6 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Franklin Electric Co., Inc.

- 6.4.2 KSB SE & Co. KGaA

- 6.4.3 Grundfos Holding A/S

- 6.4.4 Xylem Inc.

- 6.4.5 Ebara Corporation

- 6.4.6 Wilo SE

- 6.4.7 Flowserve Corporation

- 6.4.8 Sulzer Ltd

- 6.4.9 ITT Inc.

- 6.4.10 Jimenez Motores e Sistemas de Irrigacao Ltda

- 6.4.11 Pentair plc

- 6.4.12 Ruhrpumpen GmbH

- 6.4.13 Dover Corporation

- 6.4.14 IDEX Corporation

- 6.4.15 Hidromecanica Germek Ltda.

7 Market Opportunities and Future Outlook

北美灌溉幫浦:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年)歐洲灌溉幫浦:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年)

北美灌溉幫浦:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年)歐洲灌溉幫浦:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年) 農業泵浦市場-全球產業規模、佔有率、趨勢、機會和預測:按類型、材料類型、動力來源、馬力、揚程、最終用戶、地區和競爭格局分類,2021-2031年

農業泵浦市場-全球產業規模、佔有率、趨勢、機會和預測:按類型、材料類型、動力來源、馬力、揚程、最終用戶、地區和競爭格局分類,2021-2031年 電動背負式噴霧器市場:按動力來源、應用、最終用戶和分銷管道分類 - 全球預測(2026-2032 年)

電動背負式噴霧器市場:按動力來源、應用、最終用戶和分銷管道分類 - 全球預測(2026-2032 年) 可調式流量微型噴灌:全球市佔率和排名、總銷售額和需求預測(2025-2031 年)

可調式流量微型噴灌:全球市佔率和排名、總銷售額和需求預測(2025-2031 年) 全球灌溉幫浦市場

全球灌溉幫浦市場 2030 年農業泵浦市場預測:按類型、材料類型、馬力、泵浦頭尺寸、動力來源、最終用戶和地區進行的全球分析全球農用幫浦市場

2030 年農業泵浦市場預測:按類型、材料類型、馬力、泵浦頭尺寸、動力來源、最終用戶和地區進行的全球分析全球農用幫浦市場