|

市場調查報告書

商品編碼

2072907

代幣化證券:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Tokenized Securities - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

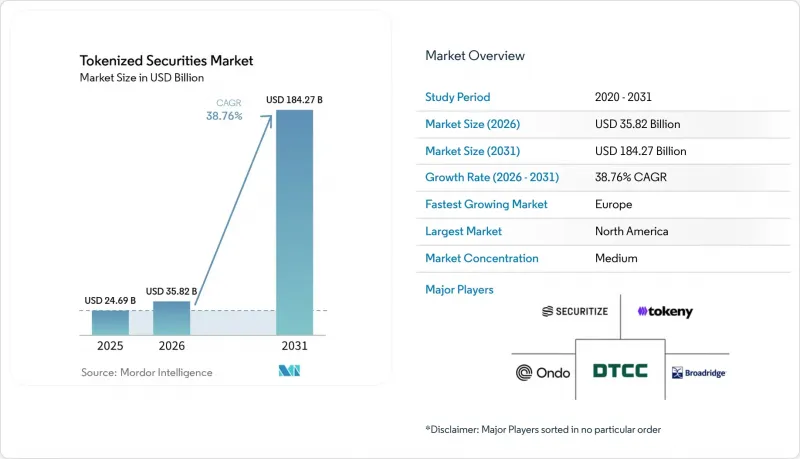

根據 Mordor Intelligence 預測,代幣化證券市場規模預計將從 2025 年的 246.9 億美元成長到 2026 年的 358.2 億美元,到 2031 年達到 1842.7 億美元,2026 年至 2031 年的複合年成長率為 38.76%。

本報告按資產類別(例如,代幣化股權證券)、投資者類型(機構投資者、個人投資者)、代幣化形式(例如,原生代幣化證券)、發行人類型(例如,傳統金融機構、企業發行人)和地區(例如,北美、南美)進行分類。市場預測以美元計價。

全球代幣化證券市場的趨勢與洞察

明確主要金融中心的相關規定

美國證券交易委員會(SEC)和商品期貨交易委員會(CFTC)於2026年3月發布的解釋性指南,透過將數位證券定義為必須完全遵守美國證券法義務的加密資產類別,解決了代幣化證券市場的一個重大法律不確定性。隔日,SEC批准納斯達克在統一的訂單簿上交易代幣化股票和傳統股票,並賦予其相同的執行不確定性。這表明,在受監管的交易基礎設施中,鏈上證券和鏈下證券將在功能上等同。在新加坡,修訂後的《資本市場產品代幣化指南》提高了對證券在發行、交易、託管和結算等各個階段合規性的預期,從而加強了尋求端到端合規性指導的機構的運營框架。總而言之,這些進展意味著主要金融中心現在提供更清晰的規則和更可靠的營運環境,削弱了監管較少的離岸市場傳統上所具有的成本優勢。這種轉變正在加速銀行、資產管理公司和長期機構投資者對代幣化證券市場的內部核准流程。

機構投資者增加對代幣化基金和公開發行證券的配置

隨著大型企業不再局限於試點項目,而是推出受監管的產品,機構投資者正日益湧入代幣化證券市場。 2025年12月,摩根大通資產管理公司推出了首隻代幣化貨幣市場基金“MONY”,隨後在2026年推出了“JLTXX”,進一步拓展了合格投資者可獲得的代幣化流動性產品範圍。高盛和紐約銀行也於2025年7月推出了代幣化貨幣市場基金解決方案,顯示大型金融機構將代幣化基金持股視為切實可行的資本市場基礎設施,而不僅僅是實驗性的「包裝」。推動市場需求的不僅是產品的可及性,還源於機構投資者尋求能夠在其抵押品管理、財務管理和結算流程中更有效率地管理的代幣化證券。因此,代幣化證券市場正在吸引來自傳統投資組合配置框架之外的投資職能部門的資金。

不同司法管轄區之間的法規碎片化

代幣化證券市場仍面臨重大的跨國限制。這是因為各個司法管轄區內部法規結構的完善速度快於確保跨司法管轄區相容性的速度。 2025年1月,經合組織指出,不同市場法律待遇的差異可能會威脅結算的確定性,並將流動性困於國家和地區壁壘之中,從而直接削弱代幣化效率的主要基礎之一。此外,2025年6月,新加坡金融管理局(MAS)宣布,新加坡管理體制的下一階段將對數位代幣服務供應商施加更嚴格的許可要求。這表明,即使是創新友善的中心也可能面臨合規障礙的急劇增加。因此,公司往往需要設立獨立的法律實體、授權結構和控制框架,才能在不同地區銷售類似產品。這增加了成本,減緩了部署速度,並限制了代幣化證券市場跨國擴張的速度。

細分市場分析

2025年,債券和固定收益產品將佔代幣化證券市場的61.36%,遙遙領先其他資產類別。這一領域之所以能夠率先擴張,是因為短期美國國債和貨幣市場產品更容易評估和監管,也更容易被機構投資者視為合格抵押品。 DTCC試驗計畫已於2025年下半年獲批,該計畫涵蓋美國國債和主要ETF,進一步強化了固定收益產品作為現有交易後系統與代幣化發行模式之間橋樑的作用。摩根大通資產管理、高盛和紐約銀行推出的產品也進一步推動了這一趨勢,代幣化貨幣市場和美國國債掛鉤結構已被用於改善流動性管理和結算柔軟性。事實上,固定收益產品仍然是代幣化證券產業的基礎,為從概念驗證(PoC) 到持續的機構使用提供了最清晰的途徑。

股票是成長最快的資產類別,預計到2031年,該領域的代幣化證券市場將以46.21%的複合年成長率成長。隨著訂單簿整合、股東溝通和公司行為處理等必要基礎設施的日益可靠和標準化,這一成長速度正在加快。美國證券交易委員會(SEC)批准納斯達克允許在統一訂單簿上交易代幣化股票和傳統股票,這是一個重要的里程碑,它為在熟悉的交易所環境中進行上市股票代幣化建立了一種模式。代理投票的支持也得到了改善,Ondo Finance與博德瑞(Broadridge)合作,為超過250隻代幣化股票和ETF提供支持,解決了先前阻礙股票代幣化普及的實際難題之一。共同基金受益人權益和集體投資產品也受益於此基礎設施的完善。相較之下,其他代幣化證券,例如私募信貸和實體資產掛鉤產品,在二級市場交易和法律轉讓標準改善之前,成長速度可能會放緩。

到2025年,機構投資者將佔代幣化證券市場91.48%的佔有率,凸顯了初始需求主要集中在合格且受監管的參與者中。代幣化證券市場的產品結構仍然體現了其基礎,許多產品在投資者購買或轉讓其持有的代幣之前,都需要進行KYC(了解你的客戶)和AML(洗錢防制)審核、錢包白名單註冊以及持續的合規性檢查。摩根大通資產管理公司的「MONY」和「JLTXX」就是典型的例子,它們均在受控的銷售和報告環境下運營,旨在滿足全面的流動性管理需求,而非面向普通零售投資者。此外,機構投資者仍然佔據主導地位,因為對於大規模資產配置而言,清晰的法律所有權、抵押品合格和營運連續性比新穎性更為重要。目前,代幣化證券行業仍然由能夠承受合規複雜性並要求穩健營運管理的機構投資者所主導。

散戶投資者是成長最快的投資者群體,預計到2031年,他們在代幣化證券市場的參與度將以48.72%的複合年成長率成長。這一轉變主要由面向消費者的平台推動,這些平台允許用戶透過錢包和應用程式購買上市證券和基金的部分所有權。幣安計劃於2026年推出美國股票的部分所有權交易,起價5美元,併計劃推出「bStocks」機制,這些都顯示散戶銷售正從概念階段邁向實際產品設計階段。散戶業務的擴張也將增加發行方和平台的營運負擔,因為他們需要處理更多投資者的溝通、合格篩選和身份驗證等工作,以應對大規模的用戶群。隨著用戶群體的擴大,代幣化證券市場將需要更嚴格的規則,包括資訊揭露、交易週期、糾紛解決以及企業對待非機構投資者的行為規範。

區域分析

到2025年,北美將佔據代幣化證券市場67.34%的佔有率,成為該領域當之無愧的區域中心。該地區受益於美國強大的市場基礎設施、眾多大型資產管理公司和市場基礎設施運營商的聚集,以及一系列法規核准,這些核准為發行、交易和結算提供了更穩定的支持。 DTCC於2025年12月獲得代幣化服務授權,並已確認將於2026年啟動試點交易和商業化運營,從而為北美市場建立起強大的機構投資者基礎。美國證券交易委員會(SEC)和商品期貨交易委員會(CFTC)於2026年3月發布的解釋性指南以及納斯達克的批准,進一步鞏固了DTCC在該地區的領先地位,並增強了法律和交易所層面的透明度。這些因素共同推動北美代幣化證券市場從試點階段走向全面運作。

歐洲是成長最快的區域市場,預計到2031年,代幣化證券市場將以44.25%的複合年成長率成長。這一成長得益於在批發市場代幣化、基金代幣化和數位資產基礎設施方面更為積極的政策議程。在英國,金融行為監理局(FCA)於2026年5月發布了PS26/7號文件,概述了代幣化持牌基金營運的「藍圖」模式。這為企業提供了更清晰的推出和監管路線圖。同樣在2026年5月,英格蘭銀行和FCA提出了批發市場代幣化的通用願景,旨在推動結算和支付基礎設施的長期轉型。儘管歐洲在分類和互通性方面仍面臨挑戰,但政策方向正使該地區成為代幣化證券市場日益有吸引力的地區。

儘管亞太地區目前市場佔有率較小,但它仍然是代幣化證券市場未來擴張最重要的地區之一。新加坡在2025年修訂了代幣化指南並明確了數位代幣服務供應商的許可製度,建立了高合規標準,並成為機構投資者發行和服務的標竿市場。在日本,SBI控股公司於2026年2月宣布推出首個針對個人投資者的安全符記債券系列,顯示面向普通投資者的安全符記產品正在國內監管框架下開始發展。中東地區也正透過與阿布達比全球市場(ADGM)相連的銷售系統嶄露頭角,例如幣安計畫推出的bStocks平台。同時,南美洲在代幣化證券市場仍處於探索的早期階段。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 明確主要金融中心的相關規定

- 機構投資者對代幣化基金及公開發行證券的配置增加

- 對多元化優質證券和基金持有的需求

- 擴大代幣化政府債券作為抵押品和基金管理工具的使用範圍

- 市場基礎設施供應商、銀行和數位資產平台之間的基礎設施融合

- 數位原生投資者在二級市場的需求全天候不斷

- 市場限制因素

- 不同司法管轄區之間的法規差異

- 智慧合約、Oracle和代管服務

- 法律所有權和轉讓權的標準化程度不夠。

- 除部分主打產品外,所有產品的流動性都很低。

- 價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按資產類別

- 代幣化股票證券

- 代幣化債務/固定利率證券

- 代幣化投資信託帳戶/集合投資計劃

- 其他代幣化證券

- 按投資者類型

- 機構投資者

- 個人投資者

- 標記化

- 原生代幣化證券

- 非母語人士/代表類型/饒舌類型

- 混合結構

- 按發射器類型

- 傳統金融機構

- 加密原生/專業代幣化平台

- 公共部門和發展機構

- 公司發行人

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 秘魯

- 其他南美國家

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 比荷盧經濟聯盟(比利時、荷蘭、盧森堡)

- 北歐國家(丹麥、芬蘭、冰島、挪威、瑞典)

- 其他歐洲國家

- 亞太地區

- 印度

- 中國

- 日本

- 澳洲

- 韓國

- 東南亞(新加坡、馬來西亞、泰國、印尼、越南、菲律賓)

- 其他亞太國家

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 奈及利亞

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Securitize

- Ondo Finance

- Broadridge Financial Solutions, Inc.

- DTCC

- tZERO Technologies, LLC

- Tokeny Solutions SA

- INX Digital Company, Inc.

- Fireblocks Inc.

- Chainlink Labs, Inc.

- Polymesh Association

- ADDX Pte. Ltd.

- Apex Group Ltd.

- BlackRock, Inc.

- Franklin Resources, Inc.

- JPMorgan Chase and Co.

- Goldman Sachs Group, Inc.

- BNY

- Citi

- Nasdaq, Inc.

- HSBC Holdings plc

- Deutsche Borse AG

第7章 市場機會與未來展望

According to Mordor Intelligence, the tokenized securities market size is expected to increase from USD 24.69 billion in 2025 to USD 35.82 billion in 2026 and reach USD 184.27 billion by 2031, growing at a CAGR of 38.76% over 2026-2031.

This report is Segmented by Asset Class (Tokenized Equity Securities, and More), by Investor Type (Institutional Investors, Retail Investors), by Tokenization (Native Tokenized Securities, and More), Issuer Type (Traditional Financial Institutions, Corporate Issuers, and More), and Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Tokenized Securities Market Trends and Insights

Regulatory Clarity in Major Financial Centers

The March 2026 SEC and CFTC interpretive release resolved a central legal uncertainty in the tokenized securities market by defining digital securities as the crypto-asset category subject to full United States securities law obligations. One day later, the SEC approved Nasdaq to trade tokenized and traditional shares on unified order books with identical execution priority, signaling that on-chain and off-chain securities can be treated with functional parity within regulated exchange infrastructure. In Singapore, the revised Guide on the Tokenization of Capital Markets Products raised securities compliance expectations across issuance, trading, custody, and settlement, thereby strengthening the operating framework for institutions seeking end-to-end compliance clarity. Taken together, these actions narrow the old cost advantage of loosely regulated offshore venues because major financial centers now offer clearer rules and more credible operating conditions. That shift is accelerating internal approval cycles across banks, asset managers, and long-term institutional allocators in the tokenized securities market.

Rising Institutional Allocation to Tokenized Funds and Public Securities

Institutional participation in the tokenized securities market is rising because large firms are now launching regulated products rather than limiting activity to pilots. J.P. Morgan Asset Management launched MONY in December 2025 as its first tokenized money market fund, and it followed that with JLTXX in 2026, which broadened the range of tokenized liquidity products available to qualified investors. Goldman Sachs and BNY also launched a tokenized money market fund solution in July 2025, demonstrating that large financial institutions are treating tokenized fund shares as usable capital-market infrastructure rather than as experimental wrappers. The demand driver is not only about product access; institutions also want tokenized securities that can move more efficiently through collateral, treasury, and settlement workflows. As a result, the tokenized securities market is drawing capital from operating functions that sit outside traditional portfolio allocation buckets.

Regulatory Fragmentation Across Jurisdictions

The tokenized securities market still faces a major cross-border limit because regulatory frameworks are becoming clearer within jurisdictions faster than they are becoming compatible across jurisdictions. The OECD noted in January 2025 that differing legal treatments across markets threaten settlement finality and can trap liquidity within national or regional silos, thereby directly weakening one of the main efficiency claims behind tokenization. MAS also clarified in June 2025 that digital token service providers would face a stricter licensing bar under the next phase of Singapore's regime, which shows that compliance thresholds can rise sharply even in innovation-friendly centers. The practical result is that firms often need separate legal entities, licensing structures, and control frameworks to distribute similar products into different regions. That raises cost, slows rollout, and limits how quickly the tokenized securities market can scale across borders.

Other drivers and restraints analyzed in the detailed report include:

- Demand for Fractional Access to Premium Securities and Funds

- Growing Use of Tokenized Treasuries as Collateral and Cash Management Instruments

- Smart-Contract, Oracle, and Custody Risk

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Debt and fixed income accounted for 61.36% of the tokenized securities market in 2025, making it the leading asset class by a wide margin. This segment gained scale first because short-duration Treasuries and money market instruments are easier to value, regulate, and position as collateral-grade assets within institutional workflows. The DTCC pilot authorized in late 2025 includes United States Treasuries and major ETFs, which reinforces the role of fixed income as the operational bridge between existing post-trade systems and tokenized issuance models. Product launches from J.P. Morgan Asset Management, Goldman Sachs, and BNY also support this pattern, as tokenized money-market and Treasury-linked structures are already being used to improve liquidity management and settlement flexibility. In practice, fixed income remains the anchor of the tokenized securities industry because it offers the clearest path from proof of concept into repeat institutional use.

Equity securities are the fastest-growing asset class, and the tokenized securities market size for this segment is projected to expand at 46.21% CAGR through 2031. Growth is accelerating because the required infrastructure for order-book integration, shareholder communications, and corporate action handling is now becoming more credible at a regulated scale. The SEC approval that allows Nasdaq to trade tokenized and traditional shares on a unified order book is a major step because it creates a template for listed equity tokenization within a familiar exchange environment. Proxy voting support is also improving, as shown by Ondo Finance's integration with Broadridge for more than 250 tokenized stocks and ETFs, which addresses one of the practical gaps that had slowed equity adoption. Fund shares and collective investment products also benefit from this infrastructure buildout. In contrast, other tokenized securities, such as private credit and real-asset-linked products, are likely to grow more gradually until secondary trading and legal transfer standards improve.

Institutional investors held 91.48% of the tokenized securities market in 2025, underscoring the concentration of early demand among qualified and regulated participants. The product structure of the tokenized securities market still reflects that base, because many offerings require KYC and AML screening, wallet allowlisting, and ongoing compliance checks before investors can subscribe or transfer holdings. J.P. Morgan Asset Management's MONY and JLTXX are clear examples, as both products sit within controlled distribution and reporting environments aimed at serious liquidity management use cases rather than open retail access. Institutional dominance also persists because legal ownership clarity, collateral eligibility, and operational continuity matter more to large allocators than novelty. For now, the tokenized securities industry remains led by institutions that can absorb compliance complexity and demand robust operational controls.

Retail investors are the fastest-growing investor group, and their participation in the tokenized securities market is forecast to rise at 48.72% CAGR through 2031. This shift is being supported by consumer-facing platforms that are opening fractional exposure to public securities and funds through wallet-based or app-based channels. Binance's 2026 launch of fractional United States stock access at USD 5 and its planned bStocks structure illustrate how retail distribution is moving from concept to live product design. Retail expansion also increases the operating burden on issuers and platforms, as investor communication, suitability reviews, and identity verification must scale across a much larger user base. As that user base grows, the tokenized securities market will need stronger rules around disclosures, trading windows, dispute resolution, and treatment of corporate actions for non-institutional holders.

Complete Report Scope:

- By Asset Class

- Tokenized Equity Securities

- Tokenized Debt / Fixed Income Securities

- Tokenized Fund Shares / Collective Investment Schemes

- Other Tokenized Securities

- By Investor Type

- Institutional Investors

- Retail Investors

- By Tokenization

- Native Tokenized Securities

- Non-Native / Represented / Wrapped

- Hybrid Structures

- By Issuer Type

- Traditional Financial Institutions

- Crypto-Native / Specialized Tokenization Platforms

- Public Sector & Development Institutions

- Corporate Issuers

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Peru

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, and Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- Rest of Asia-Pacific

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East and Africa

- North America

Geography Analysis

North America captured 67.34% of the tokenized securities market share in 2025, which made it the clear regional center of activity. The region benefits from the depth of the United States market infrastructure, the concentration of major asset managers and market utilities, and a sequence of regulatory approvals that now support issuance, trading, and settlement more coherently. DTCC received authorization for its tokenization service in December 2025 and confirmed live-pilot trading and commercial-launch milestones in 2026, which will give North America a strong institutional operating base. The SEC and CFTC interpretive release and the Nasdaq approval in March 2026 added legal and exchange-level clarity, which further strengthened the region's first-mover position. This combination means the tokenized securities market in North America is already moving from pilot activity toward production-grade implementation.

Europe is the fastest-growing regional segment, and the tokenized securities market size in this geography is projected to expand at 44.25% CAGR through 2031. Growth is being supported by a more active policy agenda around wholesale market tokenization, fund tokenization, and digital asset infrastructure. In the United Kingdom, the FCA issued PS26/7 in May 2026 and set the Blueprint model as the operating framework for tokenized authorized funds, providing firms with a clearer path to launch and supervision. The Bank of England and FCA also set out a shared vision for tokenization in wholesale markets in May 2026, which supports longer-term changes in settlement and payments infrastructure. Europe still faces classification and interoperability frictions, but the policy direction is making the region more attractive for the tokenized securities market.

Asia-Pacific accounts for a smaller share today, but it remains one of the most important regions for future expansion in the tokenized securities market. Singapore set a high compliance benchmark with its revised tokenization guide and the 2025 clarification of the licensing regime for digital token service providers, making it a reference market for institutional-grade issuance and servicing. In Japan, SBI Holdings announced its first security token bond series for individual investors in February 2026, indicating that retail-facing security token products are also beginning to develop under regulated local structures. The Middle East is also emerging through ADGM-linked distribution structures such as Binance's planned bStocks framework. At the same time, South America remains at an earlier exploratory stage in the tokenized securities market.

- Securitize

- Ondo Finance

- Broadridge Financial Solutions, Inc.

- DTCC

- tZERO Technologies, LLC

- Tokeny Solutions SA

- INX Digital Company, Inc.

- Fireblocks Inc.

- Chainlink Labs, Inc.

- Polymesh Association

- ADDX Pte. Ltd.

- Apex Group Ltd.

- BlackRock, Inc.

- Franklin Resources, Inc.

- JPMorgan Chase and Co.

- Goldman Sachs Group, Inc.

- BNY

- Citi

- Nasdaq, Inc.

- HSBC Holdings plc

- Deutsche Borse AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory Clarity in Major Financial Centers

- 4.2.2 Rising Institutional Allocation to Tokenized Funds and Public Securities

- 4.2.3 Demand for Fractional Access to Premium Securities and Funds

- 4.2.4 Growing Use of Tokenized Treasuries as Collateral and Cash Management Instruments

- 4.2.5 Infrastructure Convergence Between Market Utilities, Banks, and Digital Asset Platforms

- 4.2.6 24/7 Secondary Market Demand from Digitally Native Investors

- 4.3 Market Restraints

- 4.3.1 Regulatory Fragmentation Across Jurisdictions

- 4.3.2 Smart-Contract, Oracle, and Custody Risk

- 4.3.3 Limited Standardization of Legal Ownership and Transfer Rights

- 4.3.4 Thin Liquidity Outside a Few Flagship Products

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS

- 5.1 By Asset Class

- 5.1.1 Tokenized Equity Securities

- 5.1.2 Tokenized Debt / Fixed Income Securities

- 5.1.3 Tokenized Fund Shares / Collective Investment Schemes

- 5.1.4 Other Tokenized Securities

- 5.2 By Investor Type

- 5.2.1 Institutional Investors

- 5.2.2 Retail Investors

- 5.3 By Tokenization

- 5.3.1 Native Tokenized Securities

- 5.3.2 Non-Native / Represented / Wrapped

- 5.3.3 Hybrid Structures

- 5.4 By Issuer Type

- 5.4.1 Traditional Financial Institutions

- 5.4.2 Crypto-Native / Specialized Tokenization Platforms

- 5.4.3 Public Sector & Development Institutions

- 5.4.4 Corporate Issuers

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Peru

- 5.5.2.5 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.5.3.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 India

- 5.5.4.2 China

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Securitize

- 6.4.2 Ondo Finance

- 6.4.3 Broadridge Financial Solutions, Inc.

- 6.4.4 DTCC

- 6.4.5 tZERO Technologies, LLC

- 6.4.6 Tokeny Solutions SA

- 6.4.7 INX Digital Company, Inc.

- 6.4.8 Fireblocks Inc.

- 6.4.9 Chainlink Labs, Inc.

- 6.4.10 Polymesh Association

- 6.4.11 ADDX Pte. Ltd.

- 6.4.12 Apex Group Ltd.

- 6.4.13 BlackRock, Inc.

- 6.4.14 Franklin Resources, Inc.

- 6.4.15 JPMorgan Chase and Co.

- 6.4.16 Goldman Sachs Group, Inc.

- 6.4.17 BNY

- 6.4.18 Citi

- 6.4.19 Nasdaq, Inc.

- 6.4.20 HSBC Holdings plc

- 6.4.21 Deutsche Borse AG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

代幣化證券市場預測至2034年:按證券類型、代幣標準、發行方式、應用、最終用戶和地區分類的全球分析

代幣化證券市場預測至2034年:按證券類型、代幣標準、發行方式、應用、最終用戶和地區分類的全球分析 支付安全市場:2026-2032年全球市場預測(依解決方案類型、組件、最終用途產業、最終用戶和部署模式分類)數位證券和安全符記發行市場預測至2034年-按代幣類型、資產類別、區塊鏈協議、發行形式、技術、最終用戶和地區分類的全球分析

支付安全市場:2026-2032年全球市場預測(依解決方案類型、組件、最終用途產業、最終用戶和部署模式分類)數位證券和安全符記發行市場預測至2034年-按代幣類型、資產類別、區塊鏈協議、發行形式、技術、最終用戶和地區分類的全球分析 行動支付代幣化市場分析與預測(至2035年):按類型、產品、服務、技術、組件、應用、部署方式、最終用戶、解決方案和模式分類

行動支付代幣化市場分析與預測(至2035年):按類型、產品、服務、技術、組件、應用、部署方式、最終用戶、解決方案和模式分類 支付安全市場規模、佔有率、趨勢和預測:按組件、平台、企業規模、最終用戶和地區分類,2026-2034 年

支付安全市場規模、佔有率、趨勢和預測:按組件、平台、企業規模、最終用戶和地區分類,2026-2034 年 支付安全市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測

支付安全市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測 2026年全球支付安全市場報告

2026年全球支付安全市場報告 支付安全市場 - 全球產業規模、佔有率、趨勢、機會、預測(按類型、組件、解決方案、地區和競爭格局分類),2021-2031年

支付安全市場 - 全球產業規模、佔有率、趨勢、機會、預測(按類型、組件、解決方案、地區和競爭格局分類),2021-2031年 支付安全市場規模、佔有率和成長分析(按組件、組織規模、垂直產業和地區分類)-2026-2033年產業預測

支付安全市場規模、佔有率和成長分析(按組件、組織規模、垂直產業和地區分類)-2026-2033年產業預測