|

市場調查報告書

商品編碼

2072878

微藻類水產飼料:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Microalgae-Based Aquafeed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

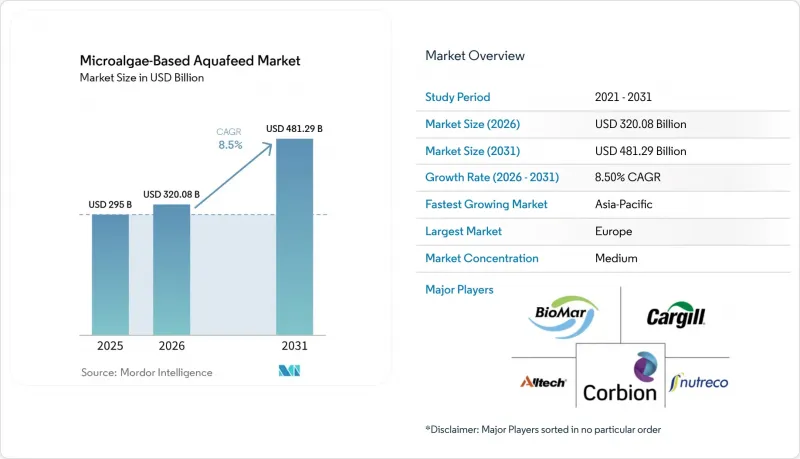

根據 Mordor Intelligence 預測,微藻類衍生水產飼料的市場規模預計將從 2025 年的 2.95 億美元和 2026 年的 3.2008 億美元成長到 2031 年的 4.8129 億美元,2026 年至 2031 年的複合成長率為 8.5%。

本報告按產品類型(全微藻類、藻粉或藻粉、富含DHA的藻油、藻蛋白分離物及其他)、藻種(螺旋藻、小球藻、微擬球藻、裂殖藻及其他)和地區(北美、南美、歐洲、亞太、中東和非洲)進行細分。市場預測以美元計價。

全球微藻類衍生水產飼料市場趨勢及洞察

閉迴路光生物反應器水產養殖成本快速下降

封閉式光生物反應器已將營運成本降低至每公斤乾生質能3美元以下,消除了藻類與魚粉之間長期存在的價格差距,並促進了藻類在高階鮭魚和蝦飼料中的更廣泛應用。 Algiecel公司於2024年籌集了5000萬丹麥克朗(約670萬美元),用於在工業排放源部署模組化裝置,證明了該移動系統在源頭捕獲二氧化碳廢料的擴充性。生命週期分析表明,螺旋藻在全面投產後,生產資金籌措可降至每公斤1.30美元,只要現貨價格保持在每噸1700美元以上,藻類的價格預計將與魚粉大致持平。此外,封閉式系統設計消除了黴菌毒素和重金屬污染,這對於微藻類水產飼料市場中的高階複合飼料至關重要。出於可追溯性的考慮,美國食品藥物管理局(FDA) 和歐洲食品安全局 (EFSA) 等監管機構更傾向於在光生物反應器中培養的菌株,與在開放式池塘中培養的替代菌株相比,這可以縮短獲得批准的時間。

無抗生素水產品的溢價機會

歐洲和北美零售商為不含抗生素的鮭魚和蝦支付兩位數的溢價,這直接獎勵了水產養殖戶採用增強免疫力的藻類飼料。 Veramaris Big Data Chile 2026 研究調查了 1.43 億條智利鮭魚,結果表明,飼料中二十碳五烯酸 (EPA) 和二十二碳六烯酸 (DHA) 的總量達到或超過 7.2%,可提高飼料轉化率,並將品質下降率降低高達 100%,這證明了添加藻類飼料的成本效益。一項使用微綠藻 (Microchloropsis gaditana) 的研究表明,魚片中的 omega-3 含量增加了 23%,細菌感染率降低了 85.68%,抗生素的使用量也顯著減少。在蝦類養殖中也觀察到了類似的效果,添加 10% 的螺旋藻可使蝦的最終體重增加 10.82 克,並將弧菌感染的死亡率降低了一半。這表明,採用微藻類衍生水產養殖飼料的市場解決方案在健康和經濟方面均具有優勢。隨著消費者意識的不斷提高,「無抗生素」標籤正從高階市場的差異化因素轉變為一項必要條件,從而鞏固了藻類在高價值水產養殖中的作用。

新藻類菌株法規核准延遲

美國食品藥物管理局(FDA) 的「公認安全」(GRAS) 認證流程以及歐盟 (EU) 的新食品法規可能會使新菌株的商業化進程延長兩到三年,並增加大量的文件成本。對於使用 CRISPR 技術編輯的高 EPA 含量藻類而言,這種延遲尤其嚴重,因為這類藻類具有更優的脂質特性。這些藻類面臨更嚴格的審查,尤其是在歐洲和日本,這些地區對基因編輯普遍持懷疑態度。儘管像 KnipBio 這樣的公司已於 2025 年獲得美國和加拿大的細菌生質能批准,但其在歐洲的批准仍在進行中,這限制了微藻類衍生水產飼料市場的整體生產擴張。監管的碎片化迫使生產商維持獨立的生產線,導致成本重複,並減緩了全球擴張。由於缺乏國際食品法典委員會 (轉碼器 Alimentarius) 的統一標準,核准延遲在中期內仍將是結構性限制。

細分市場分析

2025年,藻油在微藻類衍生水產飼料市場中佔最大佔有率,達38.0%。這是因為鮭魚養殖戶依賴藻油中穩定的二十二碳六烯酸(DHA)含量來確保魚片的高價。相較之下,分離蛋白是成長最快的細分市場,預計2026年至2031年間將以13.5%的複合年成長率成長。這主要歸功於泰國、厄瓜多和印度的蝦苗孵化場以高蛋白濃縮飼料取代魚粉,以提高幼蝦的存活率。由於市場對標準化成分的需求,以及美國食品飼料食品藥物管理局(FDA)「公認安全」(微藻類 )法規和歐盟新食品審查流程下簡化安全檢查的必要性,微藻衍生水產飼料市場中分離蛋白的市場佔有率正在進一步擴大。閉迴路光生物反應器的成本不斷下降,以及排碳權貨幣化的能力,縮小了其與魚粉的價格差距,從而促進了這一成長最快領域的普及。

微藻類和藻粉在飼料配方中佔5-15%,儘管細胞壁的存在降低了其消化率,但它們仍能為吳郭魚和觀賞魚提供色素和增強免疫力的益處。由於多年供應合約保障了高階鮭魚和海水魚飼料的穩定需求,預計藻油市場將維持強勁的複合年成長率,直至2031年。 Fermentalg公司於2026年推出的多功能藻油Omega Origins含有40%的二十碳五烯酸(EPA)和20%的二十二碳六烯酸(DHA)。這些藻油可以減少下游加工步驟,並降低成品飼料的成本。能夠在模組化系統中共培養多種藻株的生產商,可以柔軟性為其他細分市場提供滿足不同營養需求的混合成分。

區域分析

2025年,歐洲佔了最大的市場佔有率,達到35.5%。這主要歸功於挪威和丹麥的鮭魚養殖戶採用藻油來滿足海洋管理委員會(MSC)的可追溯性和無抗生素標準。亞太地區是成長最快的地區,預計2026年至2031年將以10.7%的複合年成長率成長,這主要得益於印度對藻油的零關稅政策以及中國對替代蛋白的優惠待遇。在歐洲,用於淨化水產養殖廢水的微藻類生物精煉的公共資金持續投入,而在亞太地區,進口關稅的降低正在縮小藻油與魚粉的成本差距。這些既對比鮮明又相輔相成的政策因素,使得這個規模最大、成長最快的區域市場呈現不同的成長軌跡。

在北美,得益於食品藥物管理局批准的新菌株的引入以及鮭魚養殖戶將藻類添加到飼料中以減少範圍3排放,該領域正實現穩步成長。在南美,智利的數據顯示,當藻類油中長鏈ω-3脂肪酸的總合含量超過7.2%時,飼料轉換率會提高,品質下降的情況會減少,這為該領域帶來了推動作用。在中東,適應海水環境的螺旋藻和綠藻生產設施的擴張,將碳捕獲與內陸水產養殖的擴張聯繫起來。非洲仍處於起步階段,埃及和南非的先導計畫尚需進一步降低成本,以實現全面商業化部署。

區域投資趨勢表明,產能擴張正在加速。位於蘇格蘭和法國的歐洲光生物治療反應器基地計劃到2027年將其產能提高數倍,而在日本和韓國,該技術的有效性正在通過先導計畫進行檢驗,之後才會進行全面商業化應用。挪威和加州推出的新排碳權計畫透過抵消高達15%的生產成本,提高了藻類的競爭力,並刺激了跨洲際的興趣。隨著魚粉價格持續波動和永續性標準日益嚴格,預計藻類的使用將在所有主要水產養殖區擴大,從而推動全球微藻類衍生水產飼料市場的整體擴張。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 閉迴路光生物反應器水產養殖成本快速下降

- 無抗生素水產品的溢價機會

- 透過企業的淨零排放政策促進藻類的使用。

- 再生水產養殖認證體系

- 藻類飼料廠碳權貨幣化

- 從 2025 年起,受厄爾尼諾現象影響,海洋衍生原料的供應將出現波動。

- 市場限制因素

- 開發中國家魚粉的價格差異

- 新藻類菌株法規核准延遲

- 黴菌毒素與重金屬污染風險

- 大眾對基因編輯藻類飼料的看法

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 依產品類型

- 整個微藻類

- 藻粉或藻粉

- 藻油(富含DHA)

- 藻蛋白分離物

- 其他

- 類型

- 螺旋藻

- 小球藻

- 微擬球藻

- 裂體細胞

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 其他北美國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲和紐西蘭

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析(2025 年)

- 公司簡介

- Cargill, Incorporated

- Corbion NV

- BioMar Group A/S

- Nutreco NV(Skretting)

- Alltech, Inc.

- DSM-Firmenich AG

- Archer-Daniels-Midland Company

- AlgaEnergy, SA

- Innovafeed SAS

- KnipBio, Inc.

- Cyanotech Corporation

- Algatech Ltd.

- Mowi ASA(Mowi Feed)

- Aller Aqua A/S

- Qualitas Health Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the microalgae-based aquafeed market size is anticipated to expand from USD 295 million in 2025 and USD 320.08 million in 2026 to USD 481.29 million by 2031, registering a 8.5% CAGR between 2026 to 2031.

This report is Segmented by Product Type (Whole Microalgae, Algae Meal or Flour, Algal Oil DHA-Rich, Algae Protein Isolate, and Others), by Species (Spirulina, Chlorella, Nannochloropsis, Schizochytrium, and Others), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Microalgae-Based Aquafeed Market Trends and Insights

Rapid Cost Decline in Closed-Photobioreactor Farming

Closed photobioreactors are cutting operating expenses below USD 3 per kilogram of dry biomass, closing the historical gap with fishmeal and spurring wider use of algae in premium salmon and shrimp feeds. Algiecel secured DKK 50 million (USD 6.7 million) in 2024 to deploy modular units at industrial emission points, demonstrating the scalability of mobile systems that capture waste carbon dioxide at source. Lifecycle analyses indicate Spirulina production costs could fall to USD 1.30 per kilogram at full scale, positioning algae near price parity with fishmeal as long as spot prices stay above USD 1,700 per metric ton. The closed-system design also eliminates contamination from mycotoxins and heavy metals, a key requirement for premium formulations in the microalgae-based aquafeed market. Regulators such as the United States Food and Drug Administration and the European Food Safety Authority favor photobioreactor-grown strains for their traceability, shortening approval times versus open-pond alternatives.

Premium Pricing Opportunity for Antibiotic-Free Seafood

Retailers in Europe and North America pay double-digit premiums for antibiotic-free salmon and shrimp, giving farmers a direct economic incentive to adopt immune-boosting algal ingredients. The Veramaris Big Data Chile study 2026 study covering 143 million Chilean salmon showed diets containing at least 7.2% combined eicosapentaenoic acid and docosahexaenoic acid improved feed conversion ratios and cut quality downgrades by up to 100%, reinforcing the cost-benefit case for algae inclusion. Trials with Microchloropsis gaditana increased fillet omega-3 content by 23% and reduced bacterial infections by 85.68%, demonstrably lowering antibiotic use. Similar effects were observed in shrimp, where Spirulina at 10% inclusion increased final weight to 10.82 grams and halved Vibrio mortality, demonstrating that microalgae-based aquafeed market solutions can drive both health and financial gains. As consumer awareness continues to rise, antibiotic-free labeling is moving from a differentiator to a prerequisite in premium channels, cementing algae's role in high-value aquaculture.

Regulatory Approval Lag for Novel Algae Strains

The United States Food and Drug Administration's Generally Recognized as Safe pathway and the European Union's Novel Food regulation can add 2-3 years and significant documentation costs before the commercial launch of new strains. This delay is acute for CRISPR-edited high-EPA algae that offer superior lipid profiles yet face stricter scrutiny, especially in Europe and Japan, where public skepticism toward gene editing persists. Companies such as KnipBio secured United States and Canadian approvals for bacterial biomass in 2025 but still await European clearance, limiting scale-up across the microalgae-based aquafeed market. Regulatory fragmentation forces producers to maintain separate production lines, duplicating costs and slowing global rollouts. Lack of harmonization under Codex Alimentarius keeps the approval lag a structural restraint in the medium term.

Other drivers and restraints analyzed in the detailed report include:

- Corporate Net-Zero Pledges are Accelerating Algae Inclusion

- Regenerative Aquaculture Certifications are Emerging

- Public Perception of Genetically Edited Algal Feeds

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Algal oil held the largest 38.0% share of the microalgae-based aquafeed market in 2025, as salmon producers rely on its stable docosahexaenoic acid profile to secure premium fillet pricing. In contrast, protein isolates are the fastest segment and are projected to grow at a 13.5% CAGR during 2026-2031 as shrimp hatcheries in Thailand, Ecuador, and India replace fishmeal with high-protein concentrates that lift larval survival. The microalgae-based aquafeed market size for isolates is expanding further as the United States Food and Drug Administration's Generally Recognized as Safe rules and the European Union's Novel Food reviews favor standardized compositions that streamline safety checks. Cost declines in closed photobioreactors and the ability to monetize carbon credits narrow the price gap with fishmeal, reinforcing the adoption of the fastest segment.

Whole microalgae and algal meal occupy niche positions that deliver pigmentation and immune benefits to tilapia and ornamental fish at 5-15% inclusion, even when cell wall barriers reduce digestibility. Algal oil is still forecast to grow at a solid CAGR through 2031 as multi-year supply contracts ensure steady demand in premium salmon and marine finfish feeds. Multi-functional oils, such as the Omega Origins launched by Fermentalg in 2026, contain 40% eicosapentaenoic acid and 20% docosahexaenoic acid. These oils reduce post-processing steps and lower finished-feed costs. Producers that can co-cultivate multiple strains inside modular systems gain flexibility to supply blended ingredients that meet diverse nutrient targets across the remaining segments.

Complete Report Scope:

- By Product Type

- Whole Microalgae

- Algae Meal/Flour

- Algal Oil (DHA-rich)

- Algae Protein Isolate

- Others

- By Species

- Spirulina

- Chlorella

- Nannochloropsis

- Schizochytrium

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- North America

Geography Analysis

Europe delivered the largest 35.5% share of the microalgae-based aquafeed market in 2025, as Norwegian and Danish salmon farmers adopted algal oils to meet Marine Stewardship Council traceability and antibiotic-free standards. Asia-Pacific is the fastest region, forecast to expand at a 10.7% CAGR from 2026-2031 on the back of India's zero-tariff algal oil policy and China's alternative-protein incentives. Europe continues to channel public funding into microalgae biorefineries that clean aquaculture effluent, while Asia-Pacific leverages import duty cuts to narrow the cost gap with fishmeal. These contrasting yet complementary policy drivers underpin divergent growth paths in the largest and fastest regional markets.

North America is growing steadily as Food and Drug Administration approvals open the door for novel strains and as salmon producers integrate algae to curb Scope 3 emissions. South America benefits from Chilean data showing improved feed conversion ratios and fewer downgrades when algal oils exceed 7.2% combined long-chain omega-3 content. The Middle East scales seawater-adapted Spirulina and Chlorella facilities that link carbon capture with inland aquaculture expansion. Africa remains early-stage, with pilot projects in Egypt and South Africa awaiting further cost declines before commercial rollouts.

Regional investment patterns signal accelerating capacity additions. European photobioreactor hubs in Scotland and France target multi-fold capacity jumps by 2027, while Japanese and South Korean pilots validate technology ahead of full commercialization. New carbon-credit programs in Norway and California offset up to 15% of production cost, making algae more competitive and fuelling cross-continental interest. As fishmeal volatility persists and sustainability labels harden, every major aquaculture zone is projected to widen algae usage, collectively expanding the global microalgae-based aquafeed market.

- Cargill, Incorporated

- Corbion N.V.

- BioMar Group A/S

- Nutreco N.V. (Skretting)

- Alltech, Inc.

- DSM-Firmenich AG

- Archer-Daniels-Midland Company

- AlgaEnergy, S.A.

- Innovafeed SAS

- KnipBio, Inc.

- Cyanotech Corporation

- Algatech Ltd.

- Mowi ASA (Mowi Feed)

- Aller Aqua A/S

- Qualitas Health Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid cost decline in closed-photobioreactor farming

- 4.2.2 Premium pricing opportunity for antibiotic-free seafood

- 4.2.3 Corporate net-zero pledges are accelerating algae inclusion

- 4.2.4 Regenerative aquaculture certifications are emerging

- 4.2.5 Carbon-credit monetization for algae feed plants

- 4.2.6 Marine ingredient supply volatility post-2025 El Nino events

- 4.3 Market Restraints

- 4.3.1 Price gap versus fishmeal persists in developing nations

- 4.3.2 Regulatory approval lag for novel algae strains

- 4.3.3 Mycotoxin and heavy-metal contamination risk

- 4.3.4 Public perception of "genetically edited" algal feeds

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Whole Microalgae

- 5.1.2 Algae Meal/Flour

- 5.1.3 Algal Oil (DHA-rich)

- 5.1.4 Algae Protein Isolate

- 5.1.5 Others

- 5.2 By Species

- 5.2.1 Spirulina

- 5.2.2 Chlorella

- 5.2.3 Nannochloropsis

- 5.2.4 Schizochytrium

- 5.2.5 Others

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 South America

- 5.3.2.1 Brazil

- 5.3.2.2 Argentina

- 5.3.2.3 Rest of South America

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Rest of Europe

- 5.3.4 Asia-Pacific

- 5.3.4.1 China

- 5.3.4.2 India

- 5.3.4.3 Japan

- 5.3.4.4 South Korea

- 5.3.4.5 Australia and New Zealand

- 5.3.4.6 Rest of Asia-Pacific

- 5.3.5 Middle East

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Rest of Middle East

- 5.3.6 Africa

- 5.3.6.1 South Africa

- 5.3.6.2 Egypt

- 5.3.6.3 Rest of Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis (2025)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Cargill, Incorporated

- 6.4.2 Corbion N.V.

- 6.4.3 BioMar Group A/S

- 6.4.4 Nutreco N.V. (Skretting)

- 6.4.5 Alltech, Inc.

- 6.4.6 DSM-Firmenich AG

- 6.4.7 Archer-Daniels-Midland Company

- 6.4.8 AlgaEnergy, S.A.

- 6.4.9 Innovafeed SAS

- 6.4.10 KnipBio, Inc.

- 6.4.11 Cyanotech Corporation

- 6.4.12 Algatech Ltd.

- 6.4.13 Mowi ASA (Mowi Feed)

- 6.4.14 Aller Aqua A/S

- 6.4.15 Qualitas Health Inc.

7 Market Opportunities and Future Outlook

水產養殖飼料市場:2026-2032年全球市場預測(依飼料種類、食材種類、原料來源種類、目標魚類、水產養殖系統、水產養殖環境、飼料配方、最終使用者和分銷管道分類)

水產養殖飼料市場:2026-2032年全球市場預測(依飼料種類、食材種類、原料來源種類、目標魚類、水產養殖系統、水產養殖環境、飼料配方、最終使用者和分銷管道分類) 水產飼料市場報告:按魚類品種、原料、添加劑、產品形式和地區分類(2026-2034 年)

水產飼料市場報告:按魚類品種、原料、添加劑、產品形式和地區分類(2026-2034 年) 水生幼蟲飼料市場規模、佔有率和成長分析:按類型、應用、配方/形式、配銷通路、物種、地區和行業預測,2026-2033年

水生幼蟲飼料市場規模、佔有率和成長分析:按類型、應用、配方/形式、配銷通路、物種、地區和行業預測,2026-2033年 水產養殖飼料酵素市場規模、佔有率和成長分析:按酵素類型、酵素形態、水生動物和地區分類-2026-2033年產業預測

水產養殖飼料酵素市場規模、佔有率和成長分析:按酵素類型、酵素形態、水生動物和地區分類-2026-2033年產業預測 水產飼料市場規模、佔有率、成長和全球產業分析:按類型、應用和地區分類,並對 2026-2034 年進行洞察和預測。全球飼料市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

水產飼料市場規模、佔有率、成長和全球產業分析:按類型、應用和地區分類,並對 2026-2034 年進行洞察和預測。全球飼料市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 飼料市場-全球產業規模、佔有率、趨勢、機會及預測(依成分、添加劑、種類、形態、生命週期、區域及競爭格局分類,2021-2031年)

飼料市場-全球產業規模、佔有率、趨勢、機會及預測(依成分、添加劑、種類、形態、生命週期、區域及競爭格局分類,2021-2031年) 中國水產飼料市場評估:依品種、生命階段、形態、通路和地區劃分,機會與預測(2018-2032)

中國水產飼料市場評估:依品種、生命階段、形態、通路和地區劃分,機會與預測(2018-2032) 飼料市場規模、佔有率和成長分析(按成分、類型、形態、生命週期、功能、通路和地區分類)-2026-2033年產業預測

飼料市場規模、佔有率和成長分析(按成分、類型、形態、生命週期、功能、通路和地區分類)-2026-2033年產業預測 飼料市場規模、佔有率和成長分析(按類型、成分、形態、生命週期、分銷管道和地區分類)—產業預測(2026-2033 年)

飼料市場規模、佔有率和成長分析(按類型、成分、形態、生命週期、分銷管道和地區分類)—產業預測(2026-2033 年)