|

市場調查報告書

商品編碼

2072820

中國礦業物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)China Mining Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

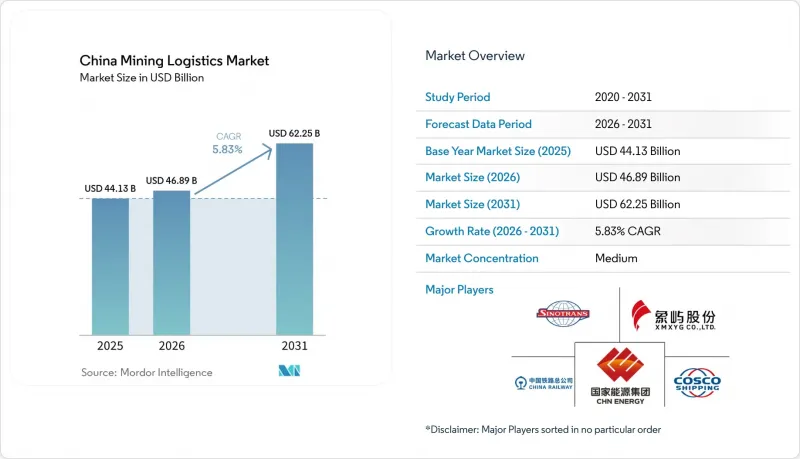

根據 Mordor Intelligence 估計,2025 年中國礦業物流市場規模為 441.3 億美元,預計將從 2026 年的 468.9 億美元成長到 2031 年的 628.5 億美元,2026 年至 2031 年的複合年成長率為 5.83%。

本報告按服務(運輸(公路、鐵路、海運和內河航運、航空)、倉儲和庫存管理、附加價值服務)、商品(鐵礦石、冶金煤和動力煤、基底金屬(銅、鋅、鎳)、黃金等)和地區(華北、東北、華東、華中、華南、西南、西北)進行細分。市場預測以美元計價。

中國礦業物流市場趨勢與洞察

擴建鐵路和水路走廊,用於煤炭和礦石運輸。

由於鐵路和水路走廊的建設重塑了煤炭和礦石運輸路線上的散裝流動模式,中國礦業物流市場正在經歷一場變革。 2025年前五個月,中國鐵路貨運量將達到16億噸,年增3.1%;受標準化多模態產品普及的推動,鐵路和水路聯運的貨櫃運輸量將增加18.4%。這種營運模式的轉變意義重大,因為它強化了綜合運輸的經濟效益,而非單一港口或鐵路交易。西南地區走廊的擴張提高了內陸生產基地與出口門戶之間的連結性,從而增強了內陸省份礦產生產的商業性合理性。隨著越來越多的貨物採用單一合約物流模式運輸,能夠將內陸貨櫃、幹線鐵路運輸、港口裝卸和下游配送整合到單一服務鏈中的營運商將繼續受益於中國礦業物流市場。

對戰略礦產和能源安全的投資

中國的礦業物流市場也受惠於國家主導的能源安全和關鍵礦產加工相關投資。預計到2025年4月,朔黃鐵路累積煤炭運輸量將超過50億噸,這清楚展現了支撐東西向能源流動的專用基礎設施規模。在此背景下,中國的提煉體系仍然至關重要。國際能源總署(IEA)預測,到2025年,中國將在20種戰略性重要礦產中的19種礦產的提煉佔有率中平均佔70%。這種高度集中確保了即使在大宗商品市場短期疲軟的情況下,通往冶煉廠和加工叢集的物流走廊也能保持其戰略重要性。在中國的礦業物流市場中,物流基礎設施不僅有助於保障國家供應安全,也滿足商業性貨運需求,為這些走廊的投資提供了強而有力的支撐。

為遵守散裝設施的環境法規而進行的資本投資

為因應環境法規,中國礦業物流市場,尤其是散貨碼頭和內陸轉運樞紐,資本密集度正在不斷提高。營運商被要求在港口和轉運站擴大除塵系統、封閉式輸送機、廢水處理和電氣設備的使用。 CHN能源的黃騅港五期計畫宣布,到2025年建成將採用16種綠色技術的「近零碳」碼頭,顯示新一代散貨基礎設施所需的投資規模龐大。由於港口發展與更廣泛的公共和能源政策優先事項息息相關,大型國有企業更容易承擔這些成本。同時,在中國礦產分銷市場,中小型民營散貨業者仍面臨風險,因為在貨運量下降時期,合規相關支出會直接與營運資金爭取資源。

細分市場分析

到2025年,運輸業將佔中國礦業物流市場的68.18%,這反映了煤炭、鐵礦石和礦石精礦在全國範圍內巨大的運輸量。公共政策、貨運走廊建設資金和港口投資都在推動大規模散裝運輸,因此鐵路、海運和內河航運仍然是主要的運輸方式。在鐵路網不發達的山區和內陸礦區,道路運輸在「第一公里」運輸中仍然發揮著至關重要的作用。空運在運輸服務組合中佔比很小,因為礦產品通常單價較低且重量較大,但對於精煉金屬和關鍵零件,在交貨時間至關重要的情況下,仍然會採用更快捷的運輸方式。

成長最快的細分市場是附加價值服務,預計到2031年將以6.49%的複合年成長率成長,這主要得益於鋼廠將礦石混煉、品位最佳化和水分管理等業務外包給港口物流營運商。倉儲和庫存管理仍然至關重要,因為鋼廠和電廠需要緩衝庫存來平衡採購週期,並在運輸中斷期間維持營運。位於日照港寶武的1000萬噸級智慧礦石混煉中心表明,中國礦業物流業正在從單純的貨運轉向服務型產業,以提高送入高爐的礦石品質並減少現場處理需求。隨著這種模式的普及,除了運輸和裝卸費用外,客製化加工合約的收入佔比預計將在中國礦業物流市場進一步提高。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 戰略物流走廊分析

- 基礎設施和交通配置分析

- 市場促進因素

- 擴建鐵路和水路走廊,用於煤炭和礦石運輸。

- 戰略性礦產和能源安全投資

- 擴大深海礦石碼頭的處理能力

- 降低物流成本並推廣模式轉換政策

- 港口側的礦石混合和加工

- 引入自動駕駛運輸和智慧調度

- 市場限制因素

- 與散裝節點環境合規相關的資本投資

- 鋼鐵週期和鐵礦石價格波動

- 從礦井到主線的「第一英里」存在瓶頸

- 對沿海樞紐失效的敏感性

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 地緣政治事件對市場的影響

第5章 市場規模與成長預測

- 按服務

- 運輸

- 路

- 鐵路

- 海路和內河航道

- 航空

- 倉儲和庫存管理

- 附加價值服務

- 運輸

- 依產品

- 鐵礦石

- 冶金用煤及一般用途煤

- 普通金屬(銅、鋅、鎳)

- 金子

- 其他礦物和金屬

- 按地區

- 中國北方

- 中國東北

- 華東

- 華中地區

- 華南

- 中國西南地區

- 中國西北地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- China Energy Investment Corporation(CHN Energy)

- Sinotrans Limited

- COSCO SHIPPING Logistics and Supply Chain Management Co., Ltd.

- China Logistics Group Co., Ltd.

- China State Railway Group(CR)

- Ningbo Zhoushan Port Company Limited

- Shandong Port Group Co., Ltd.

- Tianjin Port(Group)Co., Ltd.

- Hebei Port Group Co., Ltd.

- China Minmetals Corporation

- Shandong Energy Group Co., Ltd.

- Jizhong Energy Group Co., Ltd.

- Jiayou International Logistics Co., Ltd.

- Xiamen Xiangyu Co., Ltd.

- Lianyungang Port Group Co., Ltd.

- Beibu Gulf Port Co., Ltd.

- EACON Mining

- CiDi Inc.

- Chongqing Logistics Group

- WAYTOUS(Zhongke Huituo(Beijing)Technology Co., Ltd.)

第7章 市場機會與未來展望

According to Mordor Intelligence, the china mining logistics market size was estimated at USD 44.13 billion in 2025 and is expected to increase from USD 46.89 billion in 2026 to USD 62.85 billion by 2031, growing at a CAGR of 5.83% from 2026 to 2031.

This report is Segmented by Service (Transportation (Road, Rail, Sea and Inland Waterways, Air), Warehousing and Inventory Management, Value-Added Services), by Commodity (Iron Ore, Metallurgical and Thermal Coal, Base Metals (Cu, Zn, Ni), Gold, and More) and by Geography (North, Northeast, East, Central, South, Southwest, Northwest China). The Market Forecasts are Provided in Terms of Value (USD).

China Mining Logistics Market Trends and Insights

Rail-Water Corridor Expansion for Coal and Ore

The China mining logistics market is being reshaped by rail-water corridor development that is redirecting bulk flows across coal and ore routes. China's railways carried 1.6 billion tons of freight in the first 5 months of 2025, up 3.1% year on year, while rail-water intermodal container volumes rose 18.4% as standardized multimodal products gained traction. That operating shift matters because it strengthens the economics of integrated movement instead of isolated port or rail transactions. Corridor expansion in Southwest China is also widening access between inland production centers and export gateways, thereby improving the commercial case for mining output from interior provinces. As more cargo moves under single-contract logistics structures, the China mining logistics market should continue to reward operators that can combine inland pickup, mainline rail, port handling, and downstream delivery into one service chain.

Strategic Mineral and Energy Security Investment

The China mining logistics market is also supported by state-backed investment tied to energy security and critical mineral processing. The Shuohuang Railway has passed 5 billion cumulative tons of coal moved by April 2025, which shows the scale of dedicated infrastructure already supporting west-to-east energy flows. China's refining position remains central to this logic, with the IEA stating in 2025 that China held an average 70% refining share across 19 of 20 strategically important minerals IEA. That level of concentration keeps inbound logistics corridors to smelter and processing clusters strategically important even when short-term commodity markets soften. In the China mining logistics market, this creates a durable floor for corridor investment because logistics infrastructure is serving national supply security as much as commercial freight demand.

Environmental Compliance Capex for Bulk Nodes

Environmental compliance is raising capital intensity for the China mining logistics market, especially at bulk terminals and inland handling nodes. Operators are being pushed toward dust suppression systems, sealed conveyors, wastewater controls, and higher use of electrified equipment at ports and transfer stations. CHN Energy's Huanghua Port Phase V project was presented in 2025 as a near-zero carbon terminal with 16 categories of green technology, showing the scale of investment now needed in new-generation bulk infrastructure. Large state-backed operators can more easily absorb these costs because port development is tied to broader public and energy priorities. In the China mining logistics market, smaller private bulk operators remain more exposed because compliance spending directly competes with working capital during weaker throughput periods.

Other drivers and restraints analyzed in the detailed report include:

- Deepwater Ore-Terminal Capacity Expansion

- Lower Logistics Cost and Modal-Shift Policy Push

- Steel-Cycle and Ore-Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation held 68.18% of the China mining logistics market share in 2025, which reflects the sheer weight of coal, iron ore, and mineral concentrate movement across the country. Rail and sea and inland waterways remain the dominant transport sub-modes because public policy, freight corridor funding, and port investment all favor bulk movement at scale. Road transport still plays an essential first-mile role in mountain and interior mining areas where rail connectivity is incomplete. Air logistics remains a very small part of the service mix because mining cargo is usually heavy and low value per unit of weight, though refined metals and critical spare parts still use faster modes when timing matters.

The fastest growth is in value-added services, which are projected to expand at a 6.49% CAGR through 2031 as mills outsource blending, grade optimization, and moisture management to logistics operators at ports. Warehousing and inventory management remain important because steel mills and power plants need buffer stocks to smooth procurement cycles and protect operations during transport disruptions. Baowu's 10-million-ton intelligent ore blending center at Rizhao Port shows how the China mining logistics industry is shifting from pure cargo movement toward service layers that improve furnace input quality and lower on-site handling needs. As that model spreads, the China mining logistics market should see a larger share of revenue come from customized processing contracts rather than only transport and handling fees.

Complete Report Scope:

- By Service

- Transportation

- Road

- Rail

- Sea and Inland Waterways

- Air

- Warehousing and Inventory Management

- Value-Added Services

- Transportation

- By Commodity

- Iron Ore

- Metallurgical and Thermal Coal

- Base Metals (Cu, Zn, Ni)

- Gold

- Other Minerals/Metals

- By Geography

- North China

- Northeast China

- East China

- Central China

- South China

- Southwest China

- Northwest China

List of Companies Covered in this Report:

- China Energy Investment Corporation (CHN Energy)

- Sinotrans Limited

- COSCO SHIPPING Logistics and Supply Chain Management Co., Ltd.

- China Logistics Group Co., Ltd.

- China State Railway Group (CR)

- Ningbo Zhoushan Port Company Limited

- Shandong Port Group Co., Ltd.

- Tianjin Port (Group) Co., Ltd.

- Hebei Port Group Co., Ltd.

- China Minmetals Corporation

- Shandong Energy Group Co., Ltd.

- Jizhong Energy Group Co., Ltd.

- Jiayou International Logistics Co., Ltd.

- Xiamen Xiangyu Co., Ltd.

- Lianyungang Port Group Co., Ltd.

- Beibu Gulf Port Co., Ltd.

- EACON Mining

- CiDi Inc.

- Chongqing Logistics Group

- WAYTOUS (Zhongke Huituo (Beijing) Technology Co., Ltd.)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Strategic Logistics Corridor Analysis

- 4.3 Infrastructure and Modal Mix Analysis

- 4.4 Market Drivers

- 4.4.1 Rail-Water Corridor Expansion for Coal And Ore

- 4.4.2 Strategic Mineral and Energy Security Investment

- 4.4.3 Deepwater Ore-Terminal Capacity Expansion

- 4.4.4 Lower-Logistics-Cost and Modal-Shift Policy Push

- 4.4.5 Port-Side Ore Blending and Processing

- 4.4.6 Autonomous Haulage and Smart Dispatch Deployment

- 4.5 Market Restraints

- 4.5.1 Environmental Compliance Capex for Bulk Nodes

- 4.5.2 Steel-Cycle and Ore-Price Volatility

- 4.5.3 First-Mile Mine-to-Mainline Bottlenecks

- 4.5.4 Coastal Hub Disruption Sensitivity

- 4.6 Value / Supply-Chain Analysis

- 4.7 Regulatory Landscape

- 4.8 Technological Outlook

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Threat of New Entrants

- 4.9.2 Bargaining Power of Suppliers

- 4.9.3 Bargaining Power of Buyers

- 4.9.4 Threat of Substitutes

- 4.9.5 Intensity of Rivalry

- 4.10 Impact of Geopolitical Events on the Market

5 Market Size and Growth Forecasts

- 5.1 By Service

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Rail

- 5.1.1.3 Sea and Inland Waterways

- 5.1.1.4 Air

- 5.1.2 Warehousing and Inventory Management

- 5.1.3 Value-Added Services

- 5.1.1 Transportation

- 5.2 By Commodity

- 5.2.1 Iron Ore

- 5.2.2 Metallurgical and Thermal Coal

- 5.2.3 Base Metals (Cu, Zn, Ni)

- 5.2.4 Gold

- 5.2.5 Other Minerals/Metals

- 5.3 By Geography

- 5.3.1 North China

- 5.3.2 Northeast China

- 5.3.3 East China

- 5.3.4 Central China

- 5.3.5 South China

- 5.3.6 Southwest China

- 5.3.7 Northwest China

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 China Energy Investment Corporation (CHN Energy)

- 6.4.2 Sinotrans Limited

- 6.4.3 COSCO SHIPPING Logistics and Supply Chain Management Co., Ltd.

- 6.4.4 China Logistics Group Co., Ltd.

- 6.4.5 China State Railway Group (CR)

- 6.4.6 Ningbo Zhoushan Port Company Limited

- 6.4.7 Shandong Port Group Co., Ltd.

- 6.4.8 Tianjin Port (Group) Co., Ltd.

- 6.4.9 Hebei Port Group Co., Ltd.

- 6.4.10 China Minmetals Corporation

- 6.4.11 Shandong Energy Group Co., Ltd.

- 6.4.12 Jizhong Energy Group Co., Ltd.

- 6.4.13 Jiayou International Logistics Co., Ltd.

- 6.4.14 Xiamen Xiangyu Co., Ltd.

- 6.4.15 Lianyungang Port Group Co., Ltd.

- 6.4.16 Beibu Gulf Port Co., Ltd.

- 6.4.17 EACON Mining

- 6.4.18 CiDi Inc.

- 6.4.19 Chongqing Logistics Group

- 6.4.20 WAYTOUS (Zhongke Huituo (Beijing) Technology Co., Ltd.)

7 Market Opportunities and Future Outlook

- 7.1 White-space and unmet-need assessment

2026年全球鑽井服務市場報告

2026年全球鑽井服務市場報告 美國礦業物流:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)

美國礦業物流:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年) 線索挖掘軟體市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、組織規模、地區和競爭格局分類,2021-2031年

線索挖掘軟體市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、組織規模、地區和競爭格局分類,2021-2031年 阿根廷市場:依最終用途產業、萃取方法、銀含量、產品形式、應用和地區分類

阿根廷市場:依最終用途產業、萃取方法、銀含量、產品形式、應用和地區分類 材料產業現況—2026年第一第一季回顧2026年全球太空金屬採礦市場報告

材料產業現況—2026年第一第一季回顧2026年全球太空金屬採礦市場報告 都市掩埋場採礦市場預測至2034年-按廢棄物類型、採礦方法、計劃類型、應用、最終用戶和地區分類的全球分析

都市掩埋場採礦市場預測至2034年-按廢棄物類型、採礦方法、計劃類型、應用、最終用戶和地區分類的全球分析 豎井鑽機市場:按設備類型、技術、移動類型、動力來源和最終用戶分類 - 全球預測(2026-2032 年)探勘鑽機市場:熱塑性塑膠、熱固性樹脂、應用、終端用戶、全球預測(2026-2032)

豎井鑽機市場:按設備類型、技術、移動類型、動力來源和最終用戶分類 - 全球預測(2026-2032 年)探勘鑽機市場:熱塑性塑膠、熱固性樹脂、應用、終端用戶、全球預測(2026-2032) 2035年線索探勘軟體市場分析與預測:類型、產品、服務、技術、組件、應用、部署、最終用戶與功能

2035年線索探勘軟體市場分析與預測:類型、產品、服務、技術、組件、應用、部署、最終用戶與功能