|

市場調查報告書

商品編碼

2072720

溫室氣體會計系統軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)GHG Protocol Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

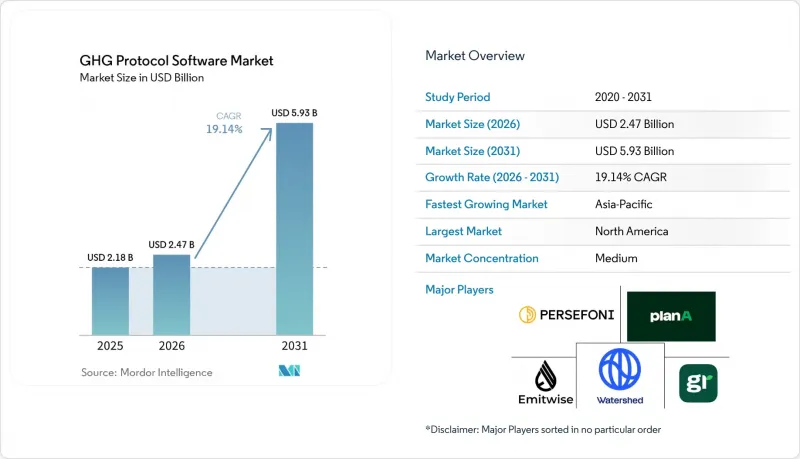

據 Mordor Intelligence 稱,溫室氣體協議軟體市場預計將從 2025 年的 21.8 億美元成長到 2026 年的 24.7 億美元,到 2031 年達到 59.3 億美元,預計 2026 年至 2031 年的複合年成長率為 19.14%。

本報告按部署類型(雲端、本地部署、混合部署)、公司規模(大型企業、中小企業)、解決方案領域(碳計量和庫存管理、ESG報告和揭露管理等)、最終用戶產業(工業製造業等)以及地區進行細分。市場預測以美元計價。

全球溫室氣體會計體系軟體市場趨勢與洞察

監管方面正朝著強制揭露範圍 1、範圍 2 和範圍 3 資料的方向發展。

強制性揭露法規改變了溫室氣體會計系統軟體市場的買方基礎。歐盟的《企業永續性報告指令》(CSRD)於2024年1月1日生效,預計將影響約5萬家公司,其中包括在歐盟境內開展大規模業務的非歐盟企業集團。 ESRS E1要求揭露範圍1、範圍2和重要的範圍3排放,並直接參考溫室氣體會計系統的範圍3標準。加州的SB 253法案是另一個重要的推動因素。加州空氣資源委員會(CARB)於2026年2月26日通過了初步實施指南,將2026年8月10日設定為受影響營業單位提交範圍1和範圍2披露資訊的截止日期。這些法規的影響範圍更廣,因為現在主要買方要求供應商在履行其範圍3類別1義務的過程中提供排放數據,而不僅僅是規模最大的報告公司。這種連鎖反應正推動符合溫室氣體協議的軟體市場以比單純的直接監管所預期的更快的速度擴張,尤其是在那些需要保持參與企業採購計畫資格的供應商中。

與加州合規工作流程中的 CSRD、IFRS S2 和溫室氣體會計系統保持一致。

溫室氣體核算體系軟體市場也受益於同一計算框架被納入多個報告系統。國際標準準則理事會(ISSB)發布的國際財務報告準則S2(IFRS S2)於2024年1月1日生效,明確規定除非相關司法管轄區另有指示,否則必須使用溫室氣體會計系統企業標準。這一核心依賴性在2025年的修訂中保持不變。 2025年1月,溫室氣體核算體係指出,此一依賴已被納入許多國家法規和實施計劃,為供應商的產品設計和客戶維繫提供了堅實的基礎。此外,2025年12月發布的經修訂的ESRS規則進一步與IFRS S1和S2保持一致,並強化了財務控制下整合的必要性,從而提高了互通性。這使得標準化平台優於專有方法。這種整合提升了單一的、可審計的排放清單在溫室氣體會計體系軟體市場中的價值,因為它可以使用單一核心資料集同時滿足多個報告義務。

多層供應鏈中範圍 3 的資料缺口

收集範圍3數據仍是溫室氣體會計體系軟體市場面臨的最大結構性限制。 Sphera於2026年2月進行的一項調查發現,45%的高階主管對範圍3數據的準確性信心有限,而89%的高階主管計劃擴大報告範圍。這表明,報告意願仍然大於對數據品質的擔憂。 2026年4月,EcoVadis宣布將擴展其“碳數據網路”,以提高供應商的透明度,這反映出在分散的供應鏈中收集一致的上游資訊仍然十分困難。 2026年3月31日發布的溫室氣體會計系統第一階段進展報告建議在修訂後的範圍3標準中按數據品質等級進行更清晰的披露,這將需要對許多現有的軟體工作流程進行調整。短期內,這種轉型帶來的負擔可能會延緩溫室氣體會計體系軟體市場在平台擴展方面的決策,但從長遠來看,提案這將增加對更優質供應商資料工具的需求。

細分市場分析

至2025年,基於雲端的部署方案將佔據溫室氣體會計系統軟體市場65.23%的佔有率。這一主導地位反映了無需大量基礎設施投資即可跨營業單位和司法管轄區擴展的軟體的吸引力。雲端系統與跨國公司的營運模式相契合,這些模式要求子公司能夠快速部署、使用標準化的報告模板,以及永續發展、財務和採購團隊之間無縫協作。溫室氣體會計體系軟體市場也受益於多租戶平台,這些平台能夠適應頻繁的監管更新,而無需進行大規模的內部升級。這項優勢對於企業應對CSRD、加州法規以及ISSB相關法規的更廣泛應用至關重要。許多買家更傾向於訂閱式部署,因為這種模式既能快速支援功能擴展,又能降低初始資本負擔。

預計到2031年,混合部署將以20.12%的複合年成長率成長,成為溫室氣體會計系統軟體市場中成長最快的部署模式。這一趨勢體現了控制與柔軟性之間的實際平衡,尤其對於那些希望在金融級環境中管理碳數據註冊,同時在雲端保持供應商協作和分析能力的公司而言。 2026年5月,SAP宣布Green Ledger正在SAP S/4HANA中註冊碳數據,並使用SAP商業技術平台進行報告和協作。這清楚地表明了混合設計為何越來越受歡迎。在能源、公共產業和政府機構等監管嚴格的產業,本地部署系統仍然佔有一席之地,因為這些產業對內部控制和資料主權的要求仍然十分嚴格。然而,溫室氣體會計體系軟體產業的趨勢正在從完全隔離的環境轉向將受保護的核心記錄與靈活的數位介面結合的架構。

2025年,大型企業將佔溫室氣體會計體系軟體銷售額的67.12%,進而在市場中佔據主導地位。由於其規模龐大、面臨法律風險以及跨多個營業單位的報告需求,人工流程已無法處理目前所需的大量排放數據。這些採購企業通常也會實施系統化的供應商選擇程序,強調健全的品質保證管理、稽核文件和ERP整合。實際上,大型企業不僅將該軟體用於資訊揭露,還用於內部控制、合併會計和供應商協作。這些多功能的應用確保了它們在當前溫室氣體會計系統軟體市場支出中繼續保持核心地位。

預計到2031年,中小企業(SME)市場規模將以21.34%的複合年成長率成長,這項變化主要受客戶壓力和直接監管的驅動。 「溫室氣體會計系統企業標準」和「範圍3框架」迫使大型企業向其供應商索取數據,從而有效地將中小企業納入報告鏈,即使在當地法規不直接適用的情況下也是如此。 2026年3月發布的《中小企業溫室氣體清單編制框架》指出,利用數位化工具可以大幅減少創造符合ISO 14064標準的記錄所需的工作量,這推動了低配置平台的普及。為此,供應商將軟體與指導實施支援和諮詢支援相結合,使中小企業無需組建大規模內部團隊即可滿足調查方法的要求。這是溫室氣體會計體系軟體市場正從大型企業的利基市場轉向更廣泛的供應商網路平台類別的最明顯徵兆之一。

區域分析

到2025年,北美將成為最大的區域市場,佔溫室氣體會計系統軟體市場佔有率的36.12%。該地區受益於報告壓力的匯聚:加州建立了一套明確遵循溫室氣體核算體系的州級系統,而上市公司也為更廣泛的氣候變遷資訊揭露義務做好準備。 2026年2月,加州空氣資源委員會(CARB)確認,SB 253法案的實施已進入下一階段,推動了從自願報告向正式合規規劃的過渡。北美也有高度集中的供應商,多家主要軟體供應商的總部都設在美國。這種集中度有助於縮短實施週期,建立更強大的整合生態系統,並促進更具競爭力的企業銷售活動。

儘管歐洲在所提供數據的區域佔有率方面並非排名第一,但其在溫室氣體核算體系軟體市場仍擁有最完善的法規環境。預計從2024年到2028年,CSRD(碳排放交易準則)的分階段實施將導致需求曲線呈現逐步上升的趨勢,這表明新買家正在逐步進入市場,而不是一次性湧入。德國的情況尤其突出,因為其工業出口企業不僅面臨營業單位層面的報告義務,還需對跨境貿易相關產品進行碳排放報告。 Carbmee於2026年6月發布的溫室排放管理軟體定位報告反映了德語區(德國、奧地利和瑞士)市場的供應商正在開發利用合規報告和營運報告重疊部分的產品這一現實。此外,制度和監管壓力持續推動英國、法國、義大利、西班牙和荷蘭等國的軟體採用,顯示整個歐洲的商業機會仍然強勁。

預計到2031年,亞太地區將以26.41%的複合年成長率成長,成為溫室氣體會計系統軟體市場成長最快的區域市場。這項加速成長主要得益於新加坡、日本、澳洲、香港和馬來西亞逐步採用ISSB相關報告,從而形成了一個在2024年之前基本上不存在的強制性需求基礎。中國是另一個需求來源,因為企業報告通常依賴與工業活動相關的工廠層級排放監測。隨著上市公司被要求遵守不斷擴展的資訊揭露要求和溫室氣體報告方法,韓國和印度的重要性也日益凸顯。中東和非洲市場仍處於起步階段,但SINAI於2026年2月與沙烏地阿拉伯區域自願碳市場公司建立的合作關係表明,政府支持的企業脫碳平台正在開始促進當地需求。南美洲在所提供的細分市場數據中並不特別突出,但其對全球框架和跨境供應鏈報告的採用表明,它很可能繼續與未來的平台擴張息息相關。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 監管機構正努力強制揭露範圍 1、範圍 2 和範圍 3 的數據。

- 從基於支出的估算過渡到主要供應商數據

- 與加州合規工作流程中的 CSRD、IFRS S2 和溫室氣體會計系統保持一致。

- 財務和永續發展部門對可審計的碳數據有需求。

- 將碳休閒與ERP和財務管理系統整合

- 利用人工智慧進行排放因子映射和數據匹配

- 市場限制因素

- 不同司法管轄區報告規則的差異

- 多層供應鏈中範圍 3 資料的資料缺口

- 對於中型企業的採購負責人來說,實施和變革管理的負擔很重。

- 與品質保證、可追溯性和調查方法。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 部署模式

- 基於雲端的

- 現場

- 混合

- 按公司規模

- 大公司

- 小型企業

- 解決方案類別

- 碳核算和庫存管理

- ESG報告與資訊揭露管理

- 範圍 3 和供應鏈排放管理

- 脫碳計畫和氣候分析

- 保證、審計、管治

- 按最終用戶行業分類

- 工業製造

- 能源、公共產業、資源

- BFSI

- 零售和消費品

- 資訊科技/通訊

- 醫療保健和生命科學

- 政府/公共部門

- 運輸/物流

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 荷蘭

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Persefoni AI, Inc.

- Watershed Technology, Inc.

- Plan A ESG GmbH

- Greenly SAS

- Green Project Technologies

- Sweep SAS

- Normative AB

- CarbonChain Ltd.

- SINAI Technologies, Inc.

- Sphera Solutions, Inc.

- Cority Software Inc.

- Benchmark Gensuite, LLC

- FigBytes Inc.

- Carbmee GmbH

- Terrascope Pte. Ltd.

- Greenstone+Ltd

- ClimatePartner GmbH

- Novisto Inc.

- EcoRealities GmbH

- Workiva Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the GHG protocol software market size is expected to increase from USD 2.18 billion in 2025 to USD 2.47 billion in 2026 and reach USD 5.93 billion by 2031, growing at a CAGR of 19.14% over 2026-2031.

This report is Segmented by Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Solution Area (Carbon Accounting and Inventory Management, ESG Reporting and Disclosure Management, and More), End-User Industry (Industrial Manufacturing, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global GHG Protocol Software Market Trends and Insights

Regulatory Push for Mandatory Scope 1, Scope 2, and Scope 3 Disclosures

Mandatory disclosure rules have changed the buyer base for the GHG Protocol Software Market. The EU CSRD took effect from January 1, 2024, and it covers an estimated 50,000 companies, including non-EU groups with substantial EU operations, with ESRS E1 requiring Scope 1, Scope 2, and significant Scope 3 disclosures that directly reference the GHG Protocol Scope 3 Standard. California SB 253 added another major trigger: the California Air Resources Board adopted initial implementation language on February 26, 2026, and confirmed filing deadlines for Scope 1 and Scope 2 disclosures for covered entities on August 10, 2026. These rules matter beyond the largest reporters, as large buyers now push emissions data requests down to their suppliers as they work through Scope 3 Category 1 obligations. That spillover is widening adoption in the GHG Protocol Software Market faster than direct regulation alone would suggest, especially for suppliers that need to remain eligible for enterprise procurement programs.

GHG Protocol Alignment in CSRD, IFRS S2, and California Compliance Workflows

The GHG Protocol Software Market is also benefiting from the fact that the same accounting framework is embedded across multiple reporting systems. IFRS S2, issued by the ISSB and effective from January 1, 2024, explicitly requires the use of the GHG Protocol Corporate Standard unless a jurisdiction directs otherwise, and the 2025 amendments did not change that core dependency. The GHG Protocol stated in January 2025 that this dependency is already embedded in rules or adoption plans across a wide range of countries, providing vendors with a durable foundation for product design and customer retention. Interoperability is also tightening, as amended ESRS rules issued in December 2025 moved further toward alignment with IFRS S1 and S2 and reinforced the need for financial-control-style consolidation, which favors standardized platforms over custom methods. That convergence increases the value of a single audit-ready emissions inventory in the GHG Protocol Software Market because a single core dataset can support multiple reporting obligations simultaneously.

Scope 3 Data Gaps Across Multi-Tier Supply Chains

Scope 3 data collection remains the biggest structural constraint on the GHG Protocol Software Market. Sphera found in February 2026 that 45% of business leaders had only limited confidence in the accuracy of Scope 3 data, even though 89% planned broader reporting, indicating that reporting ambition is still ahead of data quality. EcoVadis stated in April 2026 that it was expanding its Carbon Data Network to improve supplier transparency, reflecting the ongoing difficulty of collecting consistent upstream information across fragmented supply chains. The GHG Protocol Phase 1 Progress Update from March 31, 2026, proposed more explicit disclosure by data quality tier in the revised Scope 3 Standard, and that would require many existing software workflows to be recalibrated. In the near term, that transition burden can slow platform expansion decisions in the GHG Protocol Software Market even though it should increase long-run demand for better supplier data tools.

Other drivers and restraints analyzed in the detailed report include:

- Audit-Ready Carbon Data Demand Across Finance and Sustainability Teams

- AI-Assisted Emissions Factor Mapping and Data Reconciliation

- Fragmented Reporting Rules Across Jurisdictions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud-based deployment held 65.23% of the GHG Protocol Software Market share in 2025, and that lead reflected the appeal of software that can scale across entities and jurisdictions without heavy infrastructure investment. Cloud systems align with the operating model of multinational companies that need faster onboarding for subsidiaries, standardized reporting templates, and easier collaboration among sustainability, finance, and procurement teams. The GHG Protocol Software Market also benefited from multi-tenant platforms' ability to support frequent regulatory updates without requiring lengthy in-house upgrades. That advantage mattered as companies adjusted to the CSRD, California rules, and broader adoption linked to the ISSB. Many buyers also preferred subscription-based deployments because they reduced upfront capital commitments while supporting faster feature expansion.

Hybrid deployment is projected to grow at a 20.12% CAGR through 2031, which makes it the fastest-growing deployment model in the GHG Protocol Software Market. This pattern reflects a practical balance between control and flexibility, especially for companies that want carbon entries governed within finance-grade environments while keeping supplier collaboration and analytics in the cloud. SAP stated in May 2026 that Green Ledger posts carbon data in SAP S/4HANA, using SAP Business Technology Platform for reporting and collaboration, which illustrates why hybrid design is gaining traction. On-premises systems still retain a place in regulated sectors such as energy, utilities, and government, where internal control and data sovereignty requirements remain strict. Even so, the direction of the GHG Protocol Software industry now points toward architectures that combine protected core records with flexible digital interfaces rather than fully isolated environments.

Large enterprises accounted for 67.12% of revenue in 2025, giving them the leading position in the GHG Protocol Software Market. Their scale, legal exposure, and multi-entity reporting needs made manual processes too limited for the volume of emissions data now required. These buyers also tended to run structured vendor selection programs that favored strong assurance controls, audit documentation, and ERP integration. In practice, large companies use the software not just for disclosure, but also for internal control, consolidation, and supplier engagement. That combination kept them at the center of current spending across the GHG Protocol Software Market.

SMEs are projected to expand at a 21.34% CAGR through 2031, and this shift is being driven as much by customer pressure as by direct regulation. The GHG Protocol Corporate Standard and Scope 3 framework push large enterprises to request supplier data, which effectively brings smaller firms into the reporting chain even when local rules do not directly cover them. A March 2026 framework on SME GHG inventory development noted that digital tools can sharply reduce the effort required to build ISO 14064-aligned records, which supports the case for lower-configuration platforms. Vendors are responding by pairing software with guided onboarding and advisory support, so smaller firms can meet methodology requirements without enterprise-scale internal teams. This is one of the clearest signs that the GHG Protocol Software Market is moving from a large-enterprise niche into a broader supplier-network platform category.

Complete Report Scope:

- By Deployment Mode

- Cloud-Based

- On-Premises

- Hybrid

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

- By Solution Area

- Carbon Accounting and Inventory Management

- ESG Reporting and Disclosure Management

- Scope 3 and Supply Chain Emissions Management

- Decarbonization Planning and Climate Analytics

- Assurance, Audit and Governance

- By End-user Industry

- Industrial Manufacturing

- Energy, Utilities and Resources

- BFSI

- Retail and Consumer Goods

- IT and Telecom

- Healthcare and Life Sciences

- Government and Public Sector

- Transportation and Logistics

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Netherlands

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America held 36.12% of the GHG Protocol Software Market share in 2025, making it the largest regional market. The region benefited from overlapping reporting pressures, as California established a state-level regime explicitly aligned with the GHG Protocol while public companies prepared for broader climate disclosure obligations. The California Air Resources Board confirmed in February 2026 that SB 253 implementation had entered its next phase, reinforcing the shift from voluntary reporting to formal compliance planning. North America also had strong vendor density, with several major software providers headquartered in the United States. That concentration supported faster implementation cycles, stronger integration ecosystems, and more competitive enterprise sales activity.

Europe remained the most developed regulatory environment for the GHG Protocol Software Market, even though it did not lead in regional share in the data provided. The CSRD phase-in created a rolling demand curve from 2024 through 2028, meaning new buyer cohorts continue to enter the market in sequence rather than all at once. Germany stood out because industrial exporters there face both entity-level reporting duties and product carbon reporting needs tied to cross-border trade. Carbmee's June 2026 positioning on GHG emissions management software reflects how vendors in the DACH market are building products that leverage this overlap between compliance and operational reporting. The broader European opportunity also remains strong in the United Kingdom, France, Italy, Spain, and the Netherlands, where institutional and regulatory pressure continues to reinforce software adoption.

Asia-Pacific is projected to grow at a 26.41% CAGR through 2031, which makes it the fastest-growing regional segment in the GHG Protocol Software Market. This acceleration is being driven by phased adoption of ISSB-linked reporting across Singapore, Japan, Australia, Hong Kong, and Malaysia, which has created a mandatory demand base that was far less established before 2024. China adds another source of demand because enterprise reporting often depends on plant-level emissions monitoring tied to industrial operations. South Korea and India are also becoming more important as listed companies face widening disclosure expectations and alignment with GHG reporting methods. The Middle East and Africa remained earlier-stage markets, but SINAI's February 2026 partnership with Saudi Arabia's Regional Voluntary Carbon Market Company showed that government-backed enterprise decarbonization platforms are beginning to build local demand. South America was less prominent in the provided segment data, but global framework adoption and cross-border supply chain reporting are likely to keep it connected to future platform expansion.

- Persefoni AI, Inc.

- Watershed Technology, Inc.

- Plan A ESG GmbH

- Greenly SAS

- Green Project Technologies

- Sweep SAS

- Normative AB

- CarbonChain Ltd.

- SINAI Technologies, Inc.

- Sphera Solutions, Inc.

- Cority Software Inc.

- Benchmark Gensuite, LLC

- FigBytes Inc.

- Carbmee GmbH

- Terrascope Pte. Ltd.

- Greenstone+ Ltd

- ClimatePartner GmbH

- Novisto Inc.

- EcoRealities GmbH

- Workiva Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory Push for Mandatory Scope 1, Scope 2, and Scope 3 Disclosures

- 4.2.2 Shift From Spend-Based Estimates to Primary Supplier Data

- 4.2.3 GHG Protocol Alignment in CSRD, IFRS S2, and California Compliance Workflows

- 4.2.4 Audit-Ready Carbon Data Demand Across Finance and Sustainability Teams

- 4.2.5 Carbon Ledger Integration With ERP and Financial Controls

- 4.2.6 AI-Assisted Emissions Factor Mapping and Data Reconciliation

- 4.3 Market Restraints

- 4.3.1 Fragmented Reporting Rules Across Jurisdictions

- 4.3.2 Scope 3 Data Gaps Across Multi-Tier Supply Chains

- 4.3.3 High Implementation and Change-Management Burden for Mid-Market Buyers

- 4.3.4 Assurance, Traceability, and Methodology Switching Complexity

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 Cloud-Based

- 5.1.2 On-Premises

- 5.1.3 Hybrid

- 5.2 By Enterprise Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium Enterprises

- 5.3 By Solution Area

- 5.3.1 Carbon Accounting and Inventory Management

- 5.3.2 ESG Reporting and Disclosure Management

- 5.3.3 Scope 3 and Supply Chain Emissions Management

- 5.3.4 Decarbonization Planning and Climate Analytics

- 5.3.5 Assurance, Audit and Governance

- 5.4 By End-user Industry

- 5.4.1 Industrial Manufacturing

- 5.4.2 Energy, Utilities and Resources

- 5.4.3 BFSI

- 5.4.4 Retail and Consumer Goods

- 5.4.5 IT and Telecom

- 5.4.6 Healthcare and Life Sciences

- 5.4.7 Government and Public Sector

- 5.4.8 Transportation and Logistics

- 5.4.9 Other End-user Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Netherlands

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Persefoni AI, Inc.

- 6.4.2 Watershed Technology, Inc.

- 6.4.3 Plan A ESG GmbH

- 6.4.4 Greenly SAS

- 6.4.5 Green Project Technologies

- 6.4.6 Sweep SAS

- 6.4.7 Normative AB

- 6.4.8 CarbonChain Ltd.

- 6.4.9 SINAI Technologies, Inc.

- 6.4.10 Sphera Solutions, Inc.

- 6.4.11 Cority Software Inc.

- 6.4.12 Benchmark Gensuite, LLC

- 6.4.13 FigBytes Inc.

- 6.4.14 Carbmee GmbH

- 6.4.15 Terrascope Pte. Ltd.

- 6.4.16 Greenstone+ Ltd

- 6.4.17 ClimatePartner GmbH

- 6.4.18 Novisto Inc.

- 6.4.19 EcoRealities GmbH

- 6.4.20 Workiva Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

V2G(車輛到電網)軟體平台及聚合服務市場:市場機會、成長要素、產業趨勢分析及2026-2035年預測

V2G(車輛到電網)軟體平台及聚合服務市場:市場機會、成長要素、產業趨勢分析及2026-2035年預測 車網互動(V2G)和雙向充電解決方案市場預測至2034年-按充電器類型、車輛類型、通訊與控制、技術、應用、最終用戶和地區分類的全球分析

車網互動(V2G)和雙向充電解決方案市場預測至2034年-按充電器類型、車輛類型、通訊與控制、技術、應用、最終用戶和地區分類的全球分析 V2G(車輛到電網):市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)

V2G(車輛到電網):市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年) V2G(車輛到電網)技術市場分析與預測(至2035年):按類型、產品、服務、技術、組件、應用、部署方式、最終用戶、功能和安裝方式分類V2G通訊協定及聚合軟體市場機會、成長要素、產業趨勢分析及2026-2035年預測

V2G(車輛到電網)技術市場分析與預測(至2035年):按類型、產品、服務、技術、組件、應用、部署方式、最終用戶、功能和安裝方式分類V2G通訊協定及聚合軟體市場機會、成長要素、產業趨勢分析及2026-2035年預測 V2G市場規模、佔有率、趨勢和預測:按解決方案類型、車輛類型、充電方式、應用和地區分類,2026-2034年

V2G市場規模、佔有率、趨勢和預測:按解決方案類型、車輛類型、充電方式、應用和地區分類,2026-2034年 V2G充電器市場:按充電器類型、輸出功率、連接方式、車輛類型和最終用戶分類-2026-2032年全球市場預測

V2G充電器市場:按充電器類型、輸出功率、連接方式、車輛類型和最終用戶分類-2026-2032年全球市場預測 V2G(車輛到電網)技術市場:按應用、電源和地區分類

V2G(車輛到電網)技術市場:按應用、電源和地區分類 2026年全球V2G(車輛到電網)技術市場報告

2026年全球V2G(車輛到電網)技術市場報告 V2G市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年的預測

V2G市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年的預測