|

市場調查報告書

商品編碼

2072683

影片內容行銷服務市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Video Content Marketing Services Market - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

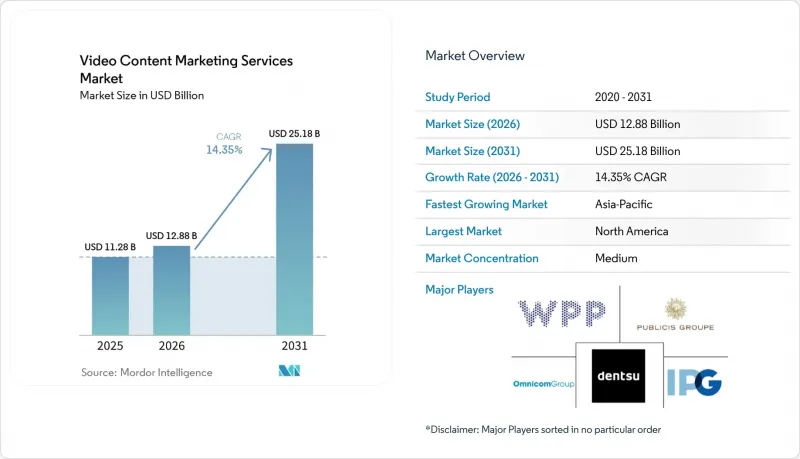

據 Mordor Intelligence 稱,2025 年影片內容行銷服務市值為 112.8 億美元,預計到 2031 年將達到 251.8 億美元,而 2026 年為 128.8 億美元,預測期(2026-2031 年)的複合年成長率為 14.35%。

本報告按服務類型(策略與諮詢、內容創意與劇本創作等)、影片類型(說明影片、教學與操作指南影片等)、影片長度(短影片、長影片)、終端用戶產業(零售與電商、消費品與美妝、銀行、金融服務與保險等)、地區進行細分。市場預測以美元計價。

全球影片內容行銷服務市場趨勢及洞察

增加對短影片的預算撥款

在影片內容行銷服務市場,短影片正從輔助策略轉變為社交和效果行銷規劃的核心組成部分。 Wistia 的一份報告顯示,到 2026 年,全球 57% 的行銷預算將包含專門的短影片預算項目,時長低於 60 秒的影片每次曝光帶來的互動量將是其他內容形式的 2.5 倍。這種轉變推動了外包需求的成長,因為特定平台的短影片節目需要迭代編輯、多種長寬比以及頻繁的更新週期,而許多內部團隊發現難以大規模地維護這些內容。 IAB 預測,到 2026 年,美國社群影片支出將成長 13%,這進一步推動了預算轉移到依賴持續管理執行的內容形式的。由於品牌需要從單一素材創建 4-6 個特定平台的剪輯版本,因此能夠有效率地進行內容版本控制、最佳化和分發的供應商在影片內容行銷服務市場中獲得了更多持續的業務。

企業對人工智慧驅動的生產和版本控制的需求日益成長。

在影片內容行銷服務市場,企業負責人正利用人工智慧驅動的工作流程來擴大影片製作規模,而無需增加員工。 Goldcast 和 Redpoint 的研究表明,到 2025 年,89% 的 B2B 行銷人員和 94% 的高階主管將把影片視為重要的策略要素,近 75% 的企業將增加影片製作預算。採用先進人工智慧影片策略的企業增加影片製作規模的可能性是其他企業的 4.5 倍,77% 的資訊長願意為人工智慧驅動的影片製作解決方案支付溢價。這種需求使那些提供結合人工智慧生成和核准工作流程、品牌管理以及輸出品質檢查等服務的公司受益,而不僅僅是銷售自動化功能。因此,市場環境正在發生變化,速度、版本控制和管治在企業合約中變得越來越重要。

在「圍牆花園」中,投資報酬率歸因存在差異。

投資報酬率歸因方面持續存在的差距,短期內會拖累影片內容行銷服務市場的支出。主流平台仍然使用不同的系統來衡量曝光量和轉換率,導致多個管道對同一筆收入聲稱業績達標,從而增加了跨管道評估的難度。這使得代理商和服務供應商難以向財務和採購部門證明影片在銷售漏斗上游的真正價值。實際上,這個問題會削弱人們對基於效果的定價模式的信心,並可能導致合約金額低於僅憑內容量所能支撐的合理水平。隨著客戶對投資報酬率的審查日益嚴格,擁有更強大的分析能力、測試框架和衡量管治的服務提供者將更有能力保持獲利能力。

細分市場分析

到2025年,影片製作將佔影片內容行銷服務市場的34.22%,並繼續保持其最大服務類別的地位。這一地位具有結構性意義,因為策略、搜尋引擎最佳化、分發和推廣都依賴源自製作成果的素材。現場拍攝、剪輯和後製仍然難以與商業影片節目完全分離,因此,大型企業、代理商和品牌自有企業持續在該領域投入資金。同時,人工智慧工具正在降低一些常規製作任務的成本,這正在改變服務提供者對其基礎服務的定價方式以及他們如何將基礎服務與高級服務區分開來。

在影片內容行銷服務市場,動畫和動態圖像預計到2031年將以16.12%的複合年成長率成長,成為成長最快的服務類別。動畫說明影片和產品視覺素材在SaaS、醫療保健和其他受監管產業的需求旺盛,因為它們無需依賴複雜的實景拍攝即可清晰地傳達訊息。此外,隨著買家從一次性專案轉向持續服務契約,策略與諮詢、內容創意與劇本創作、影片SEO以及分發與推廣等領域也在不斷擴展。這種轉變表明,在影片內容行銷服務產業,能夠將製作與搜尋最佳化、內容重用和宣傳活動管理相結合的供應商比僅僅銷售創新產品更受青睞。

到2025年,品牌故事和宣傳影片將佔影片內容行銷服務市場29.56%的佔有率,成為最大的影片類型。這一持續成長得益於企業對聯網電視、YouTube和程式化影片廣告等管道品牌股權的持續投入。這種形式仍然至關重要,因為它在漫長的購買週期中,對於展現品牌形象和建立品牌知名度都發揮關鍵作用。電通在2025年的報告中指出,如果能夠最佳化用戶注意力質量,包括短影片在內的數位影片可以帶來與傳統電視相媲美的多年品牌建設效果。

在影片內容行銷服務市場中,預計到2031年,說明影片的複合年成長率將達到15.89%,成為成長最快的影片類型。其成長的主要驅動力在於企業需要將複雜的產品概念簡化為易於在銷售、行銷和客戶成功等各個環節使用的資源。產品演示影片和教學課程也在不斷擴展,以支援用戶引導、減少對技術支援的依賴並加速產品推廣。這種趨勢表明,影片內容行銷服務市場正在努力平衡長期品牌故事敘述和能夠解答買家實際問題的高實用性內容形式。

區域分析

按地區分類,預計到2025年,北美將佔視訊內容行銷服務市場34.56%的銷售額佔有率,而亞太地區預計將以16.52%的複合年成長率(CAGR)實現最高成長。 2025年,北美仍將是影片內容行銷服務市場最大的區域市場。該地區受益於企業充足的行銷預算、IT和SaaS買家的強勁需求,以及許多經營大規模內容製作業務的大型控股公司網路。宏盟集團(Omnicom)於2025年11月完成了對Interpublic的收購,打造了一家世界領先的行銷和銷售公司,並擴展了其面向企業客戶的大規模託管影片製作能力。美國持續佔據該地區需求的大部分,而加拿大在B2B技術影片服務方面也展現出強勁的成長勢頭。隨著墨西哥近岸製作能力的擴展,其對美國品牌活動的支持度不斷增強,墨西哥的重要性也日益凸顯。

亞太地區是影片內容行銷服務市場成長最快的區域。日本數位影片廣告市場預計到2025年將超過1.0275兆日圓(約67.6億美元),CARTA Holdings、電通、電通數位和Septeni預測,到2026年將達到1.1783兆日圓(約78.6億美元)。根據CyberAgent的報告,日本國內影片廣告市場整體預計到2025年將達到8,855億日圓(約58.3億美元),到2026年將達到1.0437兆日圓(約69.6億美元)。同時,垂直影片廣告成長至2,049億日圓(約13.5億美元),佔智慧型手機影片廣告的29.1%。中國、印度、韓國和澳洲等市場對影片、直播電商和多語言在地化的需求不斷成長,也推動了該市場的發展。

在歐洲,影片內容行銷服務市場呈現穩定成長態勢,其中德國、英國和法國表現尤為突出。在這些國家,汽車、消費品和金融服務業的廣告商持續增加對優質品牌影片的投資。英國仍然是品牌故事和動畫製作的重要中心,但隨著歐盟《人工智慧法案》第50條將於2026年生效,歐洲行銷人員在揭露人工智慧產生的影片方面將面臨更嚴格的審查。以巴西和阿根廷為首的南美洲市場仍然是一個新興的機會市場,其需求主要集中在消費品、零售和社交電宣傳活動。中東和非洲地區仍處於發展初期,但隨著行動優先的影片觀看和內容投資的成長,阿拉伯聯合大公國、沙烏地阿拉伯、南非、奈及利亞和埃及的廣告商對該地區的興趣持續成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 增加對短影片的預算撥款

- 企業對人工智慧驅動的生產和版本控制的需求日益成長。

- 擴大創作者主導和員工主導的影片宣傳活動

- 擴大影片在 B2B 教育、產品展示和網路研討會重用的應用。

- 購物影片和零售媒體影片工作流程的成長

- 加速人工智慧配音和多語言在地化,以拓展中階市場。

- 市場限制因素

- 在封閉式生態系中,投資報酬率歸因方面持續存在差異。

- 大量的創新更新需求增加了分發的複雜性。

- 針對人工智慧資訊揭露和合成媒體制定更嚴格的合規規則。

- 平台演算法的差異導致自然觸達率的可預測性降低

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按服務類型

- 策略與諮詢

- 內容創意構思與劇本創作

- 影像製作

- 動畫和動態圖像

- 影片SEO和元資料最佳化

- 分銷和促銷

- 其他服務類型

- 按影片類型

- 說明影片

- 產品示範影片

- 教程和操作影片

- 品牌故事和宣傳影片

- 其他影片類型(教育影片、網路研討會等)

- 按影片尺寸

- 影片

- 長影片

- 按最終用戶行業分類

- 零售與電子商務

- 消費品/美容

- 媒體與娛樂

- 資訊科技/通訊

- BFSI

- 醫療保健和生命科學

- 其他終端使用者產業(教育、旅遊旅館、工業、汽車)

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他亞太國家

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 卡達

- 其他中東國家

- 非洲

- 南非

- 埃及

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- WPP plc

- Publicis Groupe SA

- Omnicom Group Inc.

- Dentsu Group Inc.

- Interpublic Group of Companies, Inc.

- Accenture plc

- S4 Capital plc

- Adobe Inc.

- Brightcove Inc.

- Kaltura, Inc.

- Vimeo.com, Inc.

- Vidyard Inc.

- Wistia, Inc.

- Lemonlight Media, Inc.

- Wyzowl Limited

- Demo Duck, LLC

- Epipheo, Inc.

- Yum Yum Videos LLC

- VeracityColab, LLC

- webdew, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the video content marketing services market size was valued at USD 11.28 billion in 2025 and estimated to grow from USD 12.88 billion in 2026 to reach USD 25.18 billion by 2031, at a CAGR of 14.35% during the forecast period (2026-2031).

This report is Segmented by Service Type (Strategy and Consulting, Content Ideation and Scripting, and More), Video Type (Explainer Videos, Tutorial and How-To Videos, and More), Video Size (Short-Form Videos, and Long-Form Videos), End-User Industry (Retail and E-Commerce, Consumer Goods and Beauty, BFSI, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Video Content Marketing Services Market Trends and Insights

Rising Short-Form Video Budget Reallocation

Short-form video has moved from a supporting tactic to the center of social and performance planning in the video content marketing services market. Wistia reported that 57% of marketing budgets globally included a dedicated short-form video line item in 2026, and videos under 60 seconds generated 2.5x more engagement per impression than other content formats.This shift is raising outsourced demand because platform-native short-form programs need repeated edits, multiple aspect ratios, and frequent refresh cycles that many internal teams cannot sustain at scale. The IAB stated that social video spending in the United States rose 13% in 2026, which confirms the pace of budget movement toward formats that rely on continuous managed execution. As brands create 4 to 6 platform-specific cuts from one source asset, providers that can version, optimize, and distribute content efficiently are capturing more recurring work in the video content marketing services market.

Growing Enterprise Demand for AI-Assisted Production and Versioning

Enterprise buyers are using AI-assisted workflows in the video content marketing services market to expand output without matching headcount growth. Goldcast and Redpoint found that 89% of B2B marketers and 94% of C-suite executives viewed video as important to strategy in 2025, and nearly 75% were increasing video production budgets. Organizations using advanced AI video strategies were 4.5 times more likely to increase video creation output, and 77% of CIOs said they were willing to pay a premium for AI-enhanced video production solutions. This demand is rewarding service providers that pair AI generation with approval workflows, brand controls, and output quality checks rather than selling automation alone. The result is a market environment where enterprise contracts increasingly value speed, versioning, and governance together.

Persistent ROI Attribution Gaps Across Walled Gardens

Persistent ROI attribution gaps remain a near-term brake on spending in the video content marketing services market. Large platforms still measure exposure and conversion through separate systems, which lets multiple channels claim credit for the same sale and complicates cross-channel evaluation. That makes it harder for agencies and service providers to prove the full value of upper-funnel video to finance and procurement teams. In practice, the problem reduces confidence in outcome-based pricing and can keep contract sizes below what content volume alone would justify. Providers with stronger analytics, testing frameworks, and measurement governance are better positioned to defend margins as clients scrutinize ROI more closely.

Other drivers and restraints analyzed in the detailed report include:

- Expansion Of Creator-Led And Employee-Led Video Campaigns

- Rising Adoption of Video for B2B Education, Product Demos, and Webinar Repurposing

- High-Volume Creative Refresh Requirements Raising Delivery Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Video production accounted for 34.22% of the video content marketing services market size in 2025, which kept it as the largest service category. That position is structural because strategy, SEO, distribution, and promotional work all depend on production output as their starting asset. The segment continued to attract enterprise, agency, and direct-brand spending because live capture, editing, and post-production remain difficult to remove from commercial video programs. At the same time, AI-assisted tools are reducing the cost of some routine production tasks, which is changing how providers price base execution and differentiate premium work.

Animation and motion graphics is projected to grow at 16.12% CAGR through 2031 in the video content marketing services market, making it the fastest-growing service type. Demand is rising because animated explainers and product visuals help SaaS, healthcare, and other regulated categories communicate clearly without relying on complex live-action shoots. Strategy and consulting, content ideation and scripting, video SEO, and distribution and promotion are also expanding as buyers move toward always-on service contracts instead of isolated projects. This shift shows that the video content marketing services industry is rewarding providers that combine production with discoverability, repurposing, and campaign management rather than selling creative output alone.

Branded storytelling and promotional videos represented 29.56% share in the video content marketing services market in 2025, which made them the largest video type. Their staying power comes from continued enterprise spending on brand equity across connected TV, YouTube, and programmatic video placements. This format remains important because it carries the main burden of expressing brand identity and building recall across long buying cycles. Dentsu reported in 2025 that digital video, including short-form, could deliver multi-year brand-building effects comparable to linear TV when attention quality was optimized.

Explainer videos are projected to grow at 15.89% CAGR through 2031 in the video content marketing services market, making them the fastest-growing video type. Growth is strongest where companies need to reduce complex product ideas into simple assets that can work across sales, marketing, and customer success. Product demonstration videos and tutorial formats are also expanding because they support onboarding, support deflection, and product adoption. This mix shows that the video content marketing services market is balancing long-term brand storytelling with high-utility formats that answer practical buyer questions.

Complete Report Scope:

- By Service Type

- Strategy and Consulting

- Content Ideation and Scripting

- Video Production

- Animation and Motion Graphics

- Video SEO and Metadata Optimization

- Distribution and Promotion

- Other Service Types

- By Video Type

- Explainer Videos

- Product Demonstration Videos

- Tutorial and How-To Videos

- Branded Storytelling and Promotional Videos

- Other Video Types (Educational and Webinar, etc.)

- By Video Size

- Short-Form Videos

- Long-Form Videos

- By End-User Industry

- Retail and E-commerce

- Consumer Goods and Beauty

- Media and Entertainment

- IT and Telecom

- BFSI

- Healthcare and Life Sciences

- Other End-User Industries (Education, Travel and Hospitality, Industrial, Automotive)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- United Arab Emirates

- Saudi Arabia

- Qatar

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- North America

Geography Analysis

By geography, North America held 34.56% revenue share in 2025, yet Asia-Pacific is on track for the highest regional CAGR of 16.52%. North America remained the largest regional segment in the video content marketing services market in 2025. The region benefits from dense enterprise marketing budgets, strong demand from IT and SaaS buyers, and the presence of major holding company networks with large content production operations. Omnicom completed its acquisition of Interpublic in November 2025, creating the world's leading marketing and sales company and expanding large-scale managed video capacity for enterprise clients. The United States continued to account for most regional demand, while Canada showed solid momentum in B2B technology video services. Mexico also gained relevance as nearshore production capacity expanded in support of U.S. brand work.

Asia-Pacific is the fastest-growing regional segment in the video content marketing services market. Japan's digital video advertising market exceeded JPY 1.0275 trillion (USD 6.76 billion) in 2025, and CARTA Holdings, Dentsu, Dentsu Digital, and Septeni forecast it would reach JPY 1.1783 trillion (USD 7.86 billion) in 2026. CyberAgent reported that Japan's broader domestic video advertising market stood at JPY 885.5 billion (USD 5.83 billion) in 2025 and would rise to JPY 1.0437 trillion (USD 6.96 billion) in 2026, while vertical video advertising grew to JPY 204.9 billion (USD 1.35 billion) and represented 29.1% of smartphone video advertising. China, India, South Korea, and Australia are also supporting growth as short video, live commerce, and multilingual localization demand expand across the region.

Europe showed steady growth in the video content marketing services market, led by Germany, the United Kingdom, and France, where automotive, consumer goods, and financial services buyers continue to invest in premium brand video. The United Kingdom remained an important center for branded storytelling and animation work, while European marketers also faced tighter scrutiny around AI-generated video disclosure as Article 50 of the EU AI Act moved toward enforcement in 2026. South America remained an emerging opportunity led by Brazil and Argentina, with demand tied mainly to consumer goods, retail, and social commerce campaigns. The Middle East and Africa stayed earlier in development, but the UAE, Saudi Arabia, South Africa, Nigeria, and Egypt continued to attract more advertiser interest as mobile-first video consumption and content investment increased.

- WPP plc

- Publicis Groupe S.A.

- Omnicom Group Inc.

- Dentsu Group Inc.

- Interpublic Group of Companies, Inc.

- Accenture plc

- S4 Capital plc

- Adobe Inc.

- Brightcove Inc.

- Kaltura, Inc.

- Vimeo.com, Inc.

- Vidyard Inc.

- Wistia, Inc.

- Lemonlight Media, Inc.

- Wyzowl Limited

- Demo Duck, LLC

- Epipheo, Inc.

- Yum Yum Videos LLC

- VeracityColab, LLC

- webdew, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Short-Form Video Budget Reallocation

- 4.2.2 Growing Enterprise Demand for AI-Assisted Production and Versioning

- 4.2.3 Expansion of Creator-Led and Employee-Led Video Campaigns

- 4.2.4 Rising Adoption of Video for B2B Education, Product Demos, and Webinar Repurposing

- 4.2.5 Growth of Shoppable Video and Retail Media Video Workflows

- 4.2.6 Acceleration of AI Dubbing and Multilingual Localization for Mid-Market Expansion

- 4.3 Market Restraints

- 4.3.1 Persistent ROI Attribution Gaps Across Walled Gardens

- 4.3.2 High-Volume Creative Refresh Requirements Raising Delivery Complexity

- 4.3.3 Tightening AI Disclosure and Synthetic Media Compliance Rules

- 4.3.4 Platform Algorithm Volatility Reducing Predictability of Organic Reach

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Strategy and Consulting

- 5.1.2 Content Ideation and Scripting

- 5.1.3 Video Production

- 5.1.4 Animation and Motion Graphics

- 5.1.5 Video SEO and Metadata Optimization

- 5.1.6 Distribution and Promotion

- 5.1.7 Other Service Types

- 5.2 By Video Type

- 5.2.1 Explainer Videos

- 5.2.2 Product Demonstration Videos

- 5.2.3 Tutorial and How-To Videos

- 5.2.4 Branded Storytelling and Promotional Videos

- 5.2.5 Other Video Types (Educational and Webinar, etc.)

- 5.3 By Video Size

- 5.3.1 Short-Form Videos

- 5.3.2 Long-Form Videos

- 5.4 By End-User Industry

- 5.4.1 Retail and E-commerce

- 5.4.2 Consumer Goods and Beauty

- 5.4.3 Media and Entertainment

- 5.4.4 IT and Telecom

- 5.4.5 BFSI

- 5.4.6 Healthcare and Life Sciences

- 5.4.7 Other End-User Industries (Education, Travel and Hospitality, Industrial, Automotive)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Qatar

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Nigeria

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 WPP plc

- 6.4.2 Publicis Groupe S.A.

- 6.4.3 Omnicom Group Inc.

- 6.4.4 Dentsu Group Inc.

- 6.4.5 Interpublic Group of Companies, Inc.

- 6.4.6 Accenture plc

- 6.4.7 S4 Capital plc

- 6.4.8 Adobe Inc.

- 6.4.9 Brightcove Inc.

- 6.4.10 Kaltura, Inc.

- 6.4.11 Vimeo.com, Inc.

- 6.4.12 Vidyard Inc.

- 6.4.13 Wistia, Inc.

- 6.4.14 Lemonlight Media, Inc.

- 6.4.15 Wyzowl Limited

- 6.4.16 Demo Duck, LLC

- 6.4.17 Epipheo, Inc.

- 6.4.18 Yum Yum Videos LLC

- 6.4.19 VeracityColab, LLC

- 6.4.20 webdew, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

視訊內容管理系統市場:按組件、部署模式、內容類型、組織規模和最終用戶產業分類-2026-2032年全球市場預測數位視訊內容解決方案市場:按組件、部署類型、組織規模、最終用戶產業和應用程式分類-2026-2032年全球市場預測

視訊內容管理系統市場:按組件、部署模式、內容類型、組織規模和最終用戶產業分類-2026-2032年全球市場預測數位視訊內容解決方案市場:按組件、部署類型、組織規模、最終用戶產業和應用程式分類-2026-2032年全球市場預測 2026年全球教育影片授權市場報告

2026年全球教育影片授權市場報告 全球企業影片內容管理市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球企業影片內容管理市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026-2030年全球數位影片內容市場

2026-2030年全球數位影片內容市場 視訊內容管理系統市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、功能和解決方案分類

視訊內容管理系統市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、功能和解決方案分類 數位影片內容市場報告:按經營模式、設備、類型和地區分類(2026-2034 年)

數位影片內容市場報告:按經營模式、設備、類型和地區分類(2026-2034 年) 數位視訊內容市場-全球產業規模、佔有率、趨勢、機會和預測:按經營模式、設備、地區和競爭對手分類,2021-2031年影片內容行銷服務市場按服務類型、影片類型、平台、服務層級、分發管道和最終用戶產業分類-2026年至2032年全球預測日本數位影片內容市場規模、佔有率、趨勢及預測(依經營模式、類型、設備及地區分類,2026-2034年)

數位視訊內容市場-全球產業規模、佔有率、趨勢、機會和預測:按經營模式、設備、地區和競爭對手分類,2021-2031年影片內容行銷服務市場按服務類型、影片類型、平台、服務層級、分發管道和最終用戶產業分類-2026年至2032年全球預測日本數位影片內容市場規模、佔有率、趨勢及預測(依經營模式、類型、設備及地區分類,2026-2034年)