|

市場調查報告書

商品編碼

2072643

北美SPC(石塑複合材料)地板:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)North America Stone Plastic Composite Flooring - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

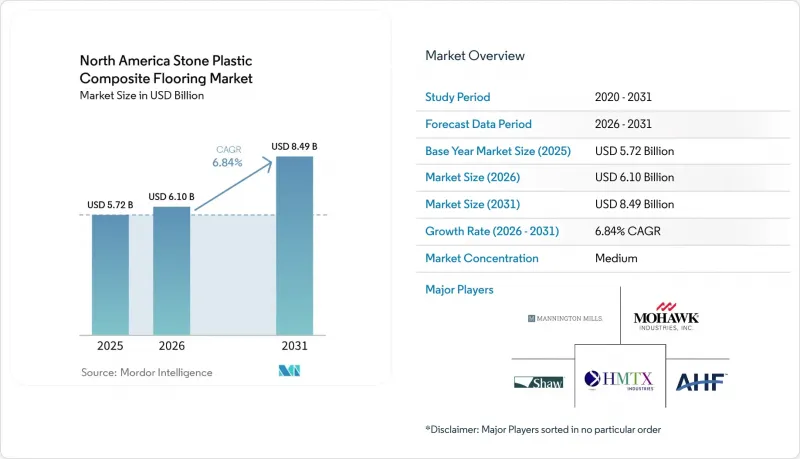

根據 Mordor Intelligence 預測,北美 SPC(石塑複合材料)地板市場將從 2025 年的 57.2 億美元成長到 2026 年的 61 億美元,到 2031 年達到 84.9 億美元,複合年成長率為 6.84%。

本報告依產品類型(SPC地磚、SPC板材)、產品厚度(4.0–5.0毫米、5.1–6.0毫米、6.1–6.5毫米及以上)、安裝方式(自黏式、其他)、最終用戶(住宅、商業)、墨西哥通路(B2C/零售、B2B/承包商/建築商)和地區(美國分類、加拿大建築商)和地區進行分類。預測值以美元計價。

北美SPC(石塑複合材料)地板市場趨勢與洞察

裝潢和DIY對防水硬質芯材的需求

SPC地板解決了室內空間濕度和溫度波動帶來的實際挑戰,因為其石塑複合芯材不會像木質產品那樣在受潮時膨脹。業主青睞其卡扣式浮動安裝方式,這種方式無需使用黏合劑,縮短了安裝時間,並降低了人事費用,因此在北美SPC地板市場中,SPC地板在住宅裝修預算中所佔佔有率越來越大。 SPC地板的普及主要源自於家庭裝修行為和材料性能需求的顯著轉變。根據美國房地產經紀人協會(NAR)統計,二手住宅約佔年度住宅交易量的85%至90%,支撐著大規模的裝修需求。家庭裝修研究所的一項調查發現,超過60%的住宅每年至少進行一項DIY項目,其中地板材料更換是最常見的維修項目之一。此外,SPC地板在-20 度C至60 度C的溫度範圍內保持結構穩定性,最大限度地減少了陽光直射或空調效果不佳的空間中因膨脹而產生的縫隙。這些性能特徵降低了維護頻率和生命週期成本,從而鼓勵出租物業業主和居住者重複購買。

從性能和價格的角度來看,從 LVT/WPC 過渡到 SPC 提供了柔軟性。

鋼芯混凝土(SPC)具有高芯材密度和優異的抗壓強度,與較軟的木塑混凝土(WPC)和軟性層壓地板(LVT)相比,更能抵抗滾動荷載和家具腿的衝擊。這使得SPC能夠以經濟實惠的價格廣泛應用於人流量大的區域。在人流量大的走廊和起居室等區域,業主們已將地毯或軟性LVT更換為SPC,並反饋稱其熱脹冷縮問題有所減少,從而降低了返工和維修的次數。北美SPC地板市場也受益於人們普遍認為,在日常使用中,硬芯結構在耐用性、耐刮擦性和防水性方面具有更高的成本績效。與軟性LVT和WPC相比,SPC在機械性能方面的顯著提升是推動其市場成長的主要因素。根據 ASTM International 的數據,SPC 剛性芯材的密度通常超過 1,900–2,100 kg/m³,而 WPC 的密度為 800–1,200 kg/m³,因此 SPC 具有更高的抗壓痕和抗載荷滾動能力。

關稅、UFLPA的審查以及PVC原料價格的波動

由於執法措施要求提供更可靠的證據和端到端的可追溯性,進口商正在最佳化採購和文件編制,以證明其供應鏈的清潔。據美國海關與邊防安全(CBP) 稱,僅在《維吾爾強迫勞動預防法》(UFLPA) 實施的第一年,執法部門就查獲了超過 3500 批貨物,價值超過 9 億美元。這增加了合規成本和清關時間。買家正在考慮包括關稅風險在內的總到貨成本。對中國產乙烯基複合地板材料產品徵收的 301 條款關稅仍維持在最高 25%,查獲貨物可能會使港口滯留時間延長 2-4 週,並可能增加每個貨櫃每天 100-300 美元的倉儲和停泊費。 PVC 樹脂仍然佔 SPC 成本的很大一部分,由於零售價格受到嚴格控制,樹脂價格的波動會對利潤率造成壓力。一些品牌正將其生產設施多元化佈局至東南亞和北美,以平衡關稅系統並簡化審計流程,這改變了對美國和加拿大的出貨分佈。這些相互衝突的因素使規劃變得複雜,並抑制了北美SPC地板市場的短期成長。

細分市場分析

預計到2025年,SPC板材將佔據72.10%的市場。隨著北美SPC地板市場中以設計為導向的項目不斷增加,SPC地磚預計到2031年將維持7.10%的複合年成長率。板材具有許多優勢,例如逼真的木紋外觀、壓花質感以及符合住宅偏好和DIY安裝趨勢的經典佈局。由於其幾何圖案和大尺寸模組,地磚在酒店業和綜合用途空間中的應用日益廣泛,這些優勢減少了勾縫,並加快了維護速度。安裝人員指出,「卡扣機制的穩定性」和「平整度」對於大尺寸地磚至關重要,因此在高人流量區域,認證系統是首選。這種兼具美觀性和實用性的選擇,使得兩種產品形式都能為北美SPC地板市場的穩定成長做出貢獻。

SPC地磚與強化複合地板和軟性乙烯基地板的區別在於,它能夠呈現僅以木條地板為主的產品系列難以實現的視覺效果。產品開發團隊為公共空間的地磚產品增加了防滑處理和更厚的耐磨層,使其即使在日常清潔和車輛碾壓下也能輕鬆保持美觀。隨著家居裝飾商店和專賣店調整陳列方案並引入更多裝飾地磚選擇,預計地磚將在北美SPC地板市場逐步擴大市場佔有率,而不會對主流木條地板的銷售量造成負面影響。此外,視覺化工具可以幫助消費者評估地磚在家中的實際效果,從而降低在擁有多種圖案的空間中做出購買決策的門檻。

到2025年,厚度在5.1-6.0毫米之間的產品將佔據北美SPC地板市場34.80%的佔有率,而厚度超過6.5毫米的地板預計到2031年將以7.45%的複合年成長率成長。中等厚度的結構兼顧了剛性芯材的穩定性和具有競爭力的成本,使其適用於大多數住宅房間和許多輕型商業空間。較厚的產品內建墊片以降低衝擊噪音,與合適的基層結合使用,有助於滿足多種安裝配置的建築規範要求。安裝人員強調邊緣強度和輪廓精度是維持所有厚度產品長期性能的關鍵,ASSURE標準採用的抗斷裂測試也支持這一觀點。這些特性指南北美SPC地板市場中不同項目選擇合適的產品。

輕薄的入門級產品適用於快速的表面翻新,但更容易受到基材平整度和重物集中荷載的影響,因此在高人流量區域風險較高。厚度超過 6.5 毫米的高級產品適用於飯店走廊和底層多用戶住宅等對隔音和抗凹陷性能要求更高的場所。標準化特定厚度範圍可以降低訓練難度,並最大限度地減少門口過渡區域出現的問題,從而提升北美 SPC 地板行業的安裝效果。中等價位的產品在北美 SPC 地板市場仍佔據核心地位,因為買家會綜合考慮總安裝成本和是否符合建築規範。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 裝潢和DIY對防水硬質芯材的需求

- 從軟性LVT/WPC過渡到SPC的性能價格比

- 零售業措施:家居裝潢商店及專賣店擴大SPC處理範圍

- 酒店業的採用以及多用戶住宅翻新中的商業用途。

- 鎖具系統(5G/Unilin)的進步可減少安裝時間和召回次數。

- 近岸外包/透過提高國內SPC產能縮短前置作業時間/合規風險

- 市場限制因素

- 關稅/根據UFLPA進行的扣押以及PVC原料價格的波動

- 由於超薄SPC的品質問題,該品類的信心下降。

- 由於智慧財產權執法力度加大(美國國際貿易委員會關於 LVT/SPC 交叉管轄的 GEO),成本不斷增加。

- 標準收緊(ASSURE v2.0 斷裂測試)增加了設備重新調整的負擔。

- 產業價值鏈分析

- 波特五力分析

- 洞察最新產業趨勢與創新

- 近期產業趨勢分析(新產品發布、策略性舉措、投資、合作、合資、業務擴張、併購等)

第5章 市場規模與成長預測

- 依產品類型

- SPC磁磚

- SPC板材

- 產品厚度(依類別)

- 4.0~5.0 mm

- 5.1~6.0 mm

- 6.1~6.5 mm

- 6.5毫米或以上

- 透過安裝方法

- 自黏式

- 黏牢

- 互鎖/卡扣

- 其他

- 最終用戶

- 住宅

- 商業

- 透過分銷管道

- B2C/零售

- 家居建材商店

- 地板材料專賣店

- 線上

- 當地金屬製品(非正規市場)

- 其他分銷管道

- B2B/承包商

- B2C/零售

- 按地區

- 美國

- 加拿大

- 墨西哥

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Shaw Industries

- Mohawk Industries

- Mannington Mills

- AHF Products

- Tarkett North America

- CFL Flooring

- Novalis Innovative Flooring(NovaFloor)

- Wellmade Performance Floors

- Nox Corporation

- Huali Floors

- Gerflor

- Beaulieu International Group(Beauflor)

- LX Hausys(formerly LG Hausys)

- United Surface Solutions

- Republic Floor(manufacturing)

- Zhejiang Kingdom Flooring Plastic Co., Ltd.

- Zhejiang Walrus New Material Co., Ltd.

- Zhangjiagang Yihua Plastics Co., Ltd.

- Jiangsu Lejia Plastic Co., Ltd.

- Changzhou Runchang Wood Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the north america stone plastic composite flooring market size stood at USD 6.10 billion in 2026, up from USD 5.72 billion in 2025, and is projected to reach USD 8.49 billion by 2031 at a 6.84% CAGR.

This report is Segmented by Product Type (SPC Tiles, SPC Planks), Product Thickness (4. 0-5. 0 Mm, 5. 1-6. 0 Mm, 6. 1-6. 5 Mm, and More), Installation Method (Self-Adhesive, and More), End User (Residential, Commercial), Distribution Channel (B2C/Retail, and B2B/Contractors/Builders), and Geography (United States, Canada, Mexico). Forecasts are Provided in Terms of Value (USD).

North America Stone Plastic Composite Flooring Market Trends and Insights

Renovation and DIY Preference for Waterproof Rigid Core

SPC addresses a practical problem in wet or variable-temperature interior spaces because its stone-plastic core does not swell like wood-based products under moisture exposure. Homeowners value click-lock floating installation that avoids adhesives, shortens project duration, and lowers labor costs compared with glue-down jobs, helping the North American SPC flooring market capture a larger share of renovation budgets. SPC adoption is supported by measurable shifts in renovation behavior and material performance needs. According to the National Association of Realtors, existing homes account for roughly 85-90% of annual housing transactions, sustaining a large renovation base. The Home Improvement Research Institute notes that over 60% of homeowners undertake at least one DIY project annually, with flooring among the most common upgrades. SPC also maintains structural stability over a temperature range of approximately -20°C to 60°C, minimizing expansion gaps in sunlit or semi-conditioned spaces. These performance characteristics translate into lower maintenance frequency and reduced lifecycle costs, reinforcing repeat purchases among landlords and owner-occupiers.

Shift from Flexible LVT/WPC to SPC on Performance to Price

SPC's higher core density and compression tolerance improve resistance to rolling loads and furniture legs compared to softer WPC or flexible LVT, supporting wider use in high-traffic zones at accessible price points. Property owners who switch from carpet or flexible LVT to SPC in busy corridors and living areas report fewer expansion and contraction issues, which cuts callbacks for replacements and repairs. The North American SPC flooring market also benefits from the perception that rigid core formats deliver greater value per dollar due to their durability, scratch resistance, and water tolerance in daily use. The transition toward SPC is driven by quantifiable improvements in mechanical performance relative to flexible LVT and WPC. According to ASTM International, SPC's rigid core density typically exceeds 1,900-2,100 kg/m3, compared with 800-1,200 kg/m3 for WPC, resulting in significantly higher resistance to indentation and rolling loads.

Tariffs, UFLPA Scrutiny, and PVC Input Price Volatility

Importers adjust sourcing and documentation to show clean supply chains because enforcement tools now require higher confidence evidence and end-to-end traceability. According to U.S. Customs and Border Protection, enforcement under the Uyghur Forced Labor Prevention Act led to over 3,500 shipment detentions valued at over USD 900 million in its first year, increasing compliance costs and clearance times. Buyers weigh landed cost scenarios that include tariff exposure, Section 301 tariffs on Chinese vinyl flooring products remain at up to 25%, and potential detentions, which can extend port dwell times by 2-4 weeks and add storage and demurrage costs of USD 100-USD 300 per container per day. PVC resin remains a significant share of SPC cost, and swings in resin pricing create margin pressure when retail price points are tightly managed. Some brands diversify production footprints to Southeast Asia or North America to balance tariff grids and streamline audits, which shifts how volumes are allocated to the United States and Canada . These cross-currents make planning more complex and temper near-term growth for the North American SPC flooring market.

Other drivers and restraints analyzed in the detailed report include:

- Retail Push: Home Centers and Specialty Expanding SPC Access

- Commercial Uptake in Hospitality and Multifamily Retrofits

- Quality Issues from Ultra Thin SPC Eroding Category Trust

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

SPC planks held 72.10% in 2025, and SPC tiles are projected to post a 7.10% CAGR through 2031 as design-driven projects gain scale in the North America SPC flooring market. Planks benefit from realistic wood visuals, embossed textures, and familiar room layouts that align with residential preferences and DIY installation flows. Tile formats expand use cases in hospitality and mixed-use spaces where geometric layouts or larger modules reduce grout lines and speed maintenance routines. Installers cite consistent click lock performance and flatness as critical for large format tiles, which supports the selection of certified systems in higher traffic locations. This balance of aesthetics and practicality positions both formats to contribute to steady growth in the North America SPC flooring market.

SPC tiles improve differentiation against laminate and flexible vinyl because tiles enable visual narratives not easily created with plank-only assortments. Product teams add slip-resistant finishes and thicker wear layers to tile SKUs aimed at public spaces, which helps preserve appearance under daily cleaning and rolling traffic. As home centers and specialty stores adjust planograms to include more statement tile options, tiles can capture incremental share without displacing core plank volume in the North America SPC flooring market. Visualizer tools also help household buyers evaluate tile looks at home, which lowers decision friction for pattern rich spaces.

The 5.1-6.0 mm class accounted for 34.80% of the North America SPC flooring market share in 2025, while planks thicker than 6.5 mm are projected to post a 7.45% CAGR through 2031. Mid-range constructions balance rigid core stability with competitive cost, making them a good fit for most residential rooms and many light commercial spaces. Thicker builds integrate attached pads that support impact sound reduction, helping satisfy building code targets in many assemblies when paired with appropriate subfloors. Contractors highlight edge strength and profile precision as keys to long-term performance across all thicknesses, a claim reinforced by the fracture resistance test adopted in the ASSURE standard. These attributes inform fit-for-purpose selections across projects in the North America SPC flooring market.

Thin, entry-level products can work for quick cosmetic refreshes, yet they are more sensitive to subfloor flatness and heavy point loads, which increases the risk in high-traffic spaces. Premium >6.5 mm products suit hospitality corridors and multifamily units above grade because acoustics and indentation resistance carry more weight in those applications. Installers who standardize on a thickness band reduce training complexity and minimize profile transition issues at doorways, which improves job outcomes in the North America SPC flooring industry . Buyers weigh total installed cost and code alignment, which keeps mid range SKUs central to the North America SPC flooring market.

Complete Report Scope:

- By Product Type

- SPC Tiles

- SPC Planks

- By Product Thickness

- 4.0-5.0 mm

- 5.1-6.0 mm

- 6.1-6.5 mm

- Above 6.5 mm

- By Installation Method

- Self-Adhesive

- Glue-Down

- Interlocking/Click-lock

- Others

- By End User

- Residential

- Commercial

- By Distribution Channel

- B2C / Retail

- Home Centers

- Specialty Flooring Stores

- Online

- Local Hardware Shops (unorganized market)

- Other Distribution Channels

- B2B / Contractors

- B2C / Retail

- By Geography

- United States

- Canada

- Mexico

List of Companies Covered in this Report:

- Shaw Industries

- Mohawk Industries

- Mannington Mills

- AHF Products

- Tarkett North America

- CFL Flooring

- Novalis Innovative Flooring (NovaFloor)

- Wellmade Performance Floors

- Nox Corporation

- Huali Floors

- Gerflor

- Beaulieu International Group (Beauflor)

- LX Hausys (formerly LG Hausys)

- United Surface Solutions

- Republic Floor (manufacturing)

- Zhejiang Kingdom Flooring Plastic Co., Ltd.

- Zhejiang Walrus New Material Co., Ltd.

- Zhangjiagang Yihua Plastics Co., Ltd.

- Jiangsu Lejia Plastic Co., Ltd.

- Changzhou Runchang Wood Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Renovation and DIY preference for waterproof rigid core

- 4.2.2 Shift from flexible LVT/WPC to SPC on performance-to-price

- 4.2.3 Retail push: home centers and specialty expanding SPC access

- 4.2.4 Commercial uptake in hospitality and multifamily retrofits

- 4.2.5 Locking-system advances (5G/Unilin) cut install time/recalls

- 4.2.6 Nearshoring/domestic SPC capacity reduces lead-times/compliance risk

- 4.3 Market Restraints

- 4.3.1 Tariffs/UFLPA detentions and PVC input volatility

- 4.3.2 Quality issues from ultra-thin SPC eroding category trust

- 4.3.3 IP enforcement (USITC GEO on interlocking LVT/SPC) raises costs

- 4.3.4 Tightening standards (ASSURE v2.0 fracture test) add retooling burden

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Industry

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Industry

5 Market Size & Growth Forecasts (Value in USD Billion)

- 5.1 By Product Type

- 5.1.1 SPC Tiles

- 5.1.2 SPC Planks

- 5.2 By Product Thickness

- 5.2.1 4.0-5.0 mm

- 5.2.2 5.1-6.0 mm

- 5.2.3 6.1-6.5 mm

- 5.2.4 Above 6.5 mm

- 5.3 By Installation Method

- 5.3.1 Self-Adhesive

- 5.3.2 Glue-Down

- 5.3.3 Interlocking/Click-lock

- 5.3.4 Others

- 5.4 By End User

- 5.4.1 Residential

- 5.4.2 Commercial

- 5.5 By Distribution Channel

- 5.5.1 B2C / Retail

- 5.5.1.1 Home Centers

- 5.5.1.2 Specialty Flooring Stores

- 5.5.1.3 Online

- 5.5.1.4 Local Hardware Shops (unorganized market)

- 5.5.1.5 Other Distribution Channels

- 5.5.2 B2B / Contractors

- 5.5.1 B2C / Retail

- 5.6 By Geography

- 5.6.1 United States

- 5.6.2 Canada

- 5.6.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Shaw Industries

- 6.4.2 Mohawk Industries

- 6.4.3 Mannington Mills

- 6.4.4 AHF Products

- 6.4.5 Tarkett North America

- 6.4.6 CFL Flooring

- 6.4.7 Novalis Innovative Flooring (NovaFloor)

- 6.4.8 Wellmade Performance Floors

- 6.4.9 Nox Corporation

- 6.4.10 Huali Floors

- 6.4.11 Gerflor

- 6.4.12 Beaulieu International Group (Beauflor)

- 6.4.13 LX Hausys (formerly LG Hausys)

- 6.4.14 United Surface Solutions

- 6.4.15 Republic Floor (manufacturing)

- 6.4.16 Zhejiang Kingdom Flooring Plastic Co., Ltd.

- 6.4.17 Zhejiang Walrus New Material Co., Ltd.

- 6.4.18 Zhangjiagang Yihua Plastics Co., Ltd.

- 6.4.19 Jiangsu Lejia Plastic Co., Ltd.

- 6.4.20 Changzhou Runchang Wood Co., Ltd.

7 Market Opportunities & Future Outlook

- 7.1 Performance-led premiumization: thicker SPC (> 6.5 mm) for IIC/STC code compliance in multifamily/hospitality

- 7.2 Domestic/nearshore SPC programs for tariff/UFLPA-sensitive RFPs with faster lead-times