|

市場調查報告書

商品編碼

2072642

SPC(石塑複合材料)地板:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)Stone Plastic Composite Flooring - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

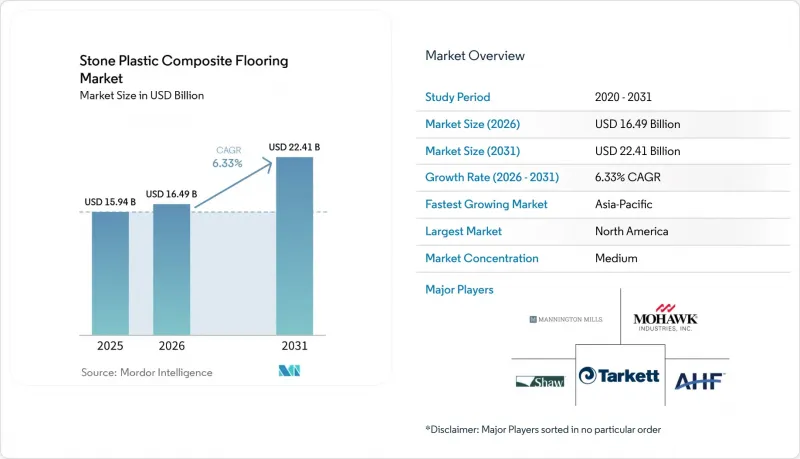

根據 Mordor Intelligence 預測,SPC(石塑複合材料)地板市場將從 2025 年的 159.4 億美元成長到 2026 年的 164.9 億美元,到 2031 年達到 224.1 億美元,複合年成長率為 6.33%。

本報告依產品類型(SPC地磚、SPC板材)、產品厚度(4.0–5.0毫米、5.1–6.0毫米、6.1–6.5毫米、6.5毫米及以上)、安裝方式(自黏等)、最終用戶(住宅、商業)、分銷通路(B2C/零售、B2B/安裝商區和北美地區(北美地區、南美地區)進行細分。市場預測以以金額為準呈現。

全球SPC(石塑複合材料)地板市場趨勢與洞察

防水硬質芯材可取代住宅和小規模商業建築中的層壓板和軟性LVT。

SPC地板市場在廚房、浴室、地下室和小規模商業空間的佔有率持續成長。在這些場所,SPC地板100%防水的剛性芯材和耐用的耐磨層降低了其他材料常見的膨脹和潮氣侵入失效風險。例如,傳統強化複合地板在長時間浸水後厚度會膨脹6-12%,而SPC產品在類似條件下透過標準化浸水和穩定性測試(例如美國材料與試驗協會 (ASTM) 的方法)證明尺寸變化極小。 SPC地板的卡扣式結構無需黏合劑浮動即可快速安裝,方便零售商店分階段入住和夜間整修,最大限度地減少停工時間。卡扣式地板的安裝效率通常為每位安裝人員每天20-40平方米,而需要塗抹和固化黏合劑的黏合地板系統每天的安裝效率僅為10-20平方米。這種「快速安裝」的優勢使SPC地板在醫療和酒店等場所的走廊等區域尤為受歡迎。這些場所對工期要求嚴格,需要即時或當天即可通行。相較之下,黏合劑式彈性地板材料需要24至48小時才能完全投入使用。在商業室內空間,如果使用木地板或磁磚會延長工期或增加維護負擔,則剛性芯材SPC地板可作為彈性地板材料的替代方案。例如,瓷磚鋪設和勾縫通常需要2-3天,而實木地板的鋪設則需要3-7天的適應期,具體取決於現場條件。相較之下,SPC地板尺寸穩定性高,通常無需適應期即可安裝。

卡扣式鎖扣系統非常適合 DIY 項目,而且家庭裝修的需求正在迅速成長。

卡扣式系統所需工具更少,無需黏合劑,即使是經驗豐富的DIY裝修愛好者也能輕鬆安裝,這也是SPC地板市場吸引住宅的原因。此外,由於無需拆除即可直接安裝在現有硬質地板上,施工時間得以縮短,對日常生活的影響也得以減少。因此,在廚房和浴室等需要快速維修的場所,例如只需一個週末即可完成翻新或立即投入使用,硬芯地板產品在翻新週期中備受青睞。供應商提供的資訊也進一步推動了這一趨勢,強調簡化的安裝方法、基材相容性和環境適應性指導,確保即使是非專業人士也能獲得可靠的安裝效果。商業領域也受益於類似的便利,小規模辦公室、診所和精品零售店的室內施工時間得以縮短,並使其能夠在完工後更快地重新開業。

對聚氯乙烯(PVC)的永續性以及循環經濟和回收利用的障礙進行審查。

對永續性的高度重視仍然是SPC地板市場面臨的一大阻力。尤其在歐洲,循環經濟目標和公共採購標準正在影響材料的選擇。歐洲塑膠回收商協會(PRE)指出,儘管數十年來各方努力,歐洲經認證的廢舊PVC回收量仍然遠低於產生的廢棄物總量,凸顯了循環經濟願景與實際結果之間的差距。如同VinylPlus進展報告(2024-2025)所述,PVC回收率逐年波動。具體而言,預計回收總量將從2023年的73.7萬噸以上下降到2024年的約72.4萬噸,這凸顯了市場及其結構面臨的挑戰。鑑於這些現實情況,製造商擴大透過環境產品聲明(EPD)記錄產品生命週期的影響,並為特定的彈性地板材料產品線提供回收舉措。這些措施提高了透明度,並有助於參與強調檢驗數據的綠色建築專案。儘管這些措施正在擴大,但與加工的原生材料總量相比,目前再生材料和生物基材料的使用量仍然很低。因此,即使在最永續性的項目中,在確定規格時也必須仔細考慮PVC含量。歐洲產業進度報告和新的環境產品聲明(EPD)為企劃團隊提供了可靠的基準,幫助他們更準確地評估環境績效,並在基礎設施完善的地區規劃廢舊產品的處置。針對剛性芯材地板材料的特定類別EPD的發布,進一步幫助規範制定者比較產品層面的環境影響和文件要求。一些公司為符合條件的項目提供彈性地板材料回收計劃,這代表了一種減少已安裝產品掩埋處置的切實可行的途徑。

細分市場分析

到2025年,SPC板材將佔據84.00%的市場佔有率,並繼續成為住宅木紋地板材料的標準形式。此外,隨著石材、水磨石和混凝土外觀設計在商業空間中日益普及,預計到2031年,SPC地板市場中這一細分市場將以8.03%的複合年成長率成長。板材在SPC地板市場中的佔有率反映了住宅對兼具天然木材美感和防水性能的產品的持續偏好,以及對能夠最大限度減少施工對日常生活影響的浮動安裝方式的青睞。瓷磚因其能夠呈現大尺寸石材的外觀,同時又無需承擔陶瓷和瓷磚所需的重量、固化時間和填縫維護等問題,而越來越受到設計師的歡迎。在商業環境中,硬芯瓷磚能夠支持大廳和走廊的夜間維修,從而實現逼真的外觀效果並實現即時重新開放。

無論項目是商業還是其他用途,外觀和表面處理流程都在不斷提升,減少了與天然材料在美學上的妥協。寬大的長條地板材料產品能夠為整個房間營造出逼真的紋理,這是以往短條地板難以實現的。磁磚擁有豐富的圖案選擇,能夠為飯店和醫療機構等場所打造引人注目的地面裝飾效果,同時保持彈性地板易於維護的特性。 SPC地板市場受益於穩定的安裝方法,這些方法可以分階段安裝,減少黏合劑的使用,並創造更清潔的工作環境。製造商的行業出版物強調,在運作緊張的情況下,剛性芯材產品可以取代勞力密集的地板材料。

2025年,厚度為4.0-5.0毫米的SPC地板佔了43.67%的市佔率。然而,隨著豪華住宅和多用戶住宅企劃團隊對更高隔音性能和腳感舒適度的需求日益成長,預計到2031年,厚度為5.1-6.0毫米的產品將以9.23%的複合年成長率成長。更厚的整合式底層結構有助於滿足建築規範中IIC和STC的最低要求,無需組裝多層結構,從而減少了不確定性並簡化了文件編制。對於尋求更強衝擊隔音效果的開發商而言,更厚的單SKU組裝產品降低了現場條件與實驗室測試產品之間差異的風險。這些產品還能減輕因底層輕微不平整造成的“透聲效應”,從而減少因硬質底層空隙和不平整而導致的返工需求。環境產品聲明 (EPD) 現在提供量化的生命週期指標,例如全球暖化潛勢值 (kg CO2-eq/m2)、能源消耗 (MJ/m2) 以及各種 SPC 結構的處置方案,使規範制定者能夠比較厚度或基材的變化如何影響所有項目選項的環境性能。

厚度有實際的上限;超過此上限會增加材料成本,並使相鄰房間的邊界處理更加困難。然而,在典型範圍內,由於其在隔音性能、舒適性和易於安裝方面的平衡性,高檔規格的地板仍然被多用戶住宅和豪華住宅廣泛採用。高檔配置的SPC地板市場規模龐大,這得益於那些將簡化建築規範合規性和居住者舒適度作為採購考慮的項目的出現。隨著供應商對聲學定義和現場指南的標準化,人們對底層地板材料的了解也得到了提升。在美國,住宅單元之間隔音的最小間隔要求決定了多用戶住宅的許多選擇。底層地板供應商持續進行宣傳活動,協助團隊選擇合適的配置以達到預期的IIC、STC和Delta IIC效能。

區域分析

2025年,北美將佔全球SPC市場價值的35.88%。由於維修週期短,且建築規範對隔音標準有嚴格要求,北美專案擴大採用剛性芯材結構,這種結構結合了快速浮動安裝和透過底層地板實現的聲學控制。國內彈性地板材料產能的擴張預計將改善產品可得性,並緩解交貨週期長和附加費用波動的影響。在以規範為導向的商業項目中,美國建築規範對住宅單元隔間牆的樓板和天花板的IIC和STC性能設定了最低標準。通常,較厚的SPC結構結合合適的底層地板可以超越此標準。這些因素意味著,SPC地板市場在租賃物業的翻新和旨在為所有住宅單元提供一致居住體驗的新多戶住宅項目中將繼續發揮至關重要的作用。各公司發布的關於彈性地板材料產能擴張的公告強調,隨著新的國內生產線達到運作,前置作業時間和產品範圍都將得到改善。

預計亞太地區將實現最快成長,2026年至2031年的複合年成長率將達到9.77%。這反映了SPC地板市場生產商規模的擴大,以及都市區住宅存量在維修過程中擴大採用防水彈性地板材料。在歐洲,市場成長持續穩步推進,這主要得益於成熟市場公共採購標準優先考慮聲學舒適度、環境資訊揭露和詳細文件。 2025年歐洲的貿易措施重塑了下游加工商的樹脂經濟格局,從而刺激了原料多元化以及對更接近終端需求的工藝和生產線的投資。這拓寬了歐洲SPC地板市場可靠資訊來源的範圍,並促進了企劃團隊專注於檢驗數據和符合標準的安裝。

在英國和歐盟,2025年實施的反傾銷措施改變了部分樹脂的定價關係,影響了加工商的採購計畫。同時,彈性地板材料對透明的環境產品數據和室內空氣品質文件的重視程度也在不斷提高。產業協會發布的針對SPC(合成塑膠地板)的EPD(環境產品聲明)可作為團隊比較不同產品類型生命週期報告的直接參考資料,從而支持建立一致的選擇框架。隨著公共和私人綠色建築標準的日益普及,文件記錄和回收/再利用方案在採購中變得越來越重要,能夠提供檢驗數據和回收計劃的公司將獲得競爭優勢。這些因素正在推動歐洲SPC地板市場的發展,引導其走向符合政策和文件記錄趨勢的產品形式和供應商。這些綜合因素正在穩步提升市場對兼具性能和資訊揭露標準的產品的需求。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 用於住宅和小規模商業建築的防水硬芯地板材料,可取代超耐磨地板和軟性LVT地板。

- 卡扣式壓鉚機制非常適合 DIY 項目,由於家庭裝修需求不斷成長,其需求量也隨之激增。

- 成本績效效益對比木材/磁磚:拓展目標市場

- 延長多用戶住宅和出租物業的翻新週期

- 由於關稅導致供應轉移(中國→越南/韓國/土耳其),使得本地供應量增加,規格也得到認可。

- 商業設施內部施工,重點在於最大限度地減少安裝過程中的停機時間,並縮短工期。

- 市場限制因素

- PVC永續性檢驗及循環利用/回收障礙

- 原料價格波動(PVC樹脂、添加劑)

- 與WPC/層壓板相比,隔音性和耐刮擦性之間存在權衡。

- 關稅、貿易措施和非關稅壁壘增加了接收貨物的成本和複雜性。

- 產業價值鏈分析

- 波特五力分析

- 洞察最新市場趨勢與創新

- 洞察近期產業趨勢(新產品發布、策略性舉措、投資、合作、合資、業務擴張、併購等)

第5章 市場規模與成長預測

- 依產品類型

- SPC磁磚

- SPC板材

- 產品厚度(依類別)

- 4.0~5.0 mm

- 5.1~6.0 mm

- 6.1~6.5 mm

- 6.5毫米或以上

- 透過安裝方法

- 自黏式

- 黏牢

- 互鎖/卡扣

- 其他

- 最終用戶

- 住宅

- 商業

- 透過分銷管道

- B2C/零售

- 家居建材商店

- 地板材料專賣店

- 線上

- 其他分銷管道

- B2B/承包商

- B2C/零售

- 按地區

- 北美洲

- 加拿大

- 美國

- 墨西哥

- 南美洲

- 巴西

- 秘魯

- 智利

- 阿根廷

- 其他南美國家

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 比荷盧經濟聯盟(比利時、荷蘭、盧森堡)

- 北歐國家(丹麥、芬蘭、冰島、挪威、瑞典)

- 其他歐洲國家

- 亞太地區

- 印度

- 中國

- 日本

- 澳洲

- 韓國

- 東南亞

- 其他亞太國家

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 奈及利亞

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Mohawk Industries

- Shaw Industries(incl. COREtec)

- Tarkett

- Mannington Mills

- CFL Flooring

- Novalis Innovative Flooring

- Beaulieu International Group(BerryAlloc)

- LX Hausys

- Huali Industrial Group

- DECNO Group

- NOX Corporation

- Forbo Flooring Systems

- Gerflor

- AHF Product

- HMTX Industries

第7章 市場機會與未來展望

According to Mordor Intelligence, the stone plastic composite flooring market size stood at USD 16.49 billion in 2026, up from USD 15.94 billion in 2025, and is projected to reach USD 22.41 billion by 2031 at a 6.33% CAGR.

This report is Segmented by Product Type (SPC Tiles, SPC Planks), Product Thickness (4. 0-5. 0 Mm, 5. 1-6. 0 Mm, 6. 1-6. 5 Mm, Above 6. 5 Mm), Installation Method (Self-Adhesive, and More), End User (Residential, Commercial), Distribution Channel (B2C/Retail, B2B/Contractors), and Geography (North America, South America, Europe, and More). Market Forecasts are Provided in Terms of Value.

Global Stone Plastic Composite Flooring Market Trends and Insights

Waterproof Rigid-Core Replacing Laminate and Flexible LVT in Home and Light Commercial

The SPC flooring market continues to gain share in kitchens, bathrooms, basements, and light-commercial areas where 100% waterproof rigid cores and durable wear layers reduce failure risk associated with swelling or moisture ingress in other materials. Traditional laminate flooring, for example, can swell by 6-12% in thickness after prolonged water exposure, whereas SPC products typically show negligible dimensional change under similar conditions, as determined by standardized water-immersion and stability tests (e.g., American Society for Testing and Materials methods). Click-lock construction enables fast floating installations that require no adhesive cure, supporting phased occupancies and overnight retail refits that minimize lost trading hours. Installation productivity for click systems typically ranges from 20-40 m2 per installer per day, compared with 10-20 m2 for glued flooring systems due to adhesive application and curing requirements. This speed-to-service benefit makes SPC flooring compelling in healthcare and hospitality corridors where installations must proceed under tight schedules and enable immediate or same-day walk-on use, unlike adhesive-based resilient flooring, which may require 24-48 hours before full service. In commercial interiors, rigid-core options serve as resilient alternatives where wood or tile would extend timelines or increase maintenance demand. Ceramic tile installations, for instance, often require 2-3 days for setting and grout curing, while hardwood installations involve acclimation periods of 3-7 days depending on site conditions. By contrast, SPC flooring can be installed without acclimation in many cases due to its dimensional stability.

DIY-Friendly Click-Lock and Renovation-Led Demand Spike

Homeowners are drawn to the SPC flooring market because click-lock systems reduce tool requirements and eliminate the need for adhesives, bringing installation within reach for proficient DIY renovators. The ability to install over many existing hard surfaces without demolition also shortens project duration and reduces overall project disruption. Renovation cycles have therefore favored rigid-core products for single-weekend room refreshes and fast kitchen or bath upgrades that must be ready for immediate use. This pattern is reinforced by supplier content that emphasizes simplified installs, subfloor tolerances, and acclimation guidance that help non-professionals achieve reliable outcomes. The commercial side benefits from the same friction reduction, which compresses fit-out schedules for small offices, clinics, and boutique retail while keeping spaces open for business sooner after install.

Polyvinyl Chloride (PVC) Sustainability Scrutiny and Circularity/Recycling Barriers

Sustainability scrutiny remains a persistent headwind for the SPC flooring market, especially in Europe, where circular-economy targets and public procurement standards shape material selection. Plastics Recyclers Europe (PRE) has concluded that, despite decades of initiatives, certified post-consumer PVC recycling volumes in Europe remain well below overall waste generation, which underscores the gap between circular ambition and realized outcomes. As highlighted in the VinylPlus Progress Report (2024-2025), PVC recycling volumes have fluctuated year on year. Specifically, the total recycled volumes dipped from exceeding 737,000 tons in 2023 to approximately 724,000 tons in 2024, underscoring the challenges faced in the market and its structure. These realities have pushed manufacturers to document lifecycle impacts through EPDs and to offer reclamation initiatives for certain resilient lines. These steps improve transparency and ease participation in green building programs that value verifiable data. While such measures are expanding, current volumes of reclaimed or bio-attributed materials are small compared to total virgin throughput, which means specification decisions in the most sustainability-sensitive projects still weigh PVC content carefully. European industry progress reports and new EPDs provide credible baselines for project teams that want to evaluate environmental performance more precisely and to plan end-of-life handling where infrastructure exists. Published category EPDs for rigid-core floors further help specifiers benchmark product-level impacts and documentation requirements. Company programs that offer resilient reclamation for qualifying projects demonstrate one practical route to reduce landfill disposal of installed products.

Other drivers and restraints analyzed in the detailed report include:

- Price-to-Performance vs Wood/Tile Expands Addressable Market

- Growth of Multi-Family and Rental Refresh Cycles

- Feedstock Price Volatility (PVC Resin, Additives)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

SPC planks held 84.00% of the 2025 market size and remain the default format for wood-look residential installations, and the segment is projected to expand at an 8.03% CAGR through 2031 as stone, terrazzo, and concrete visuals gain reach in commercial spaces within the SPC flooring market. The SPC flooring market share of plank formats reflects sustained homeowner preference for natural wood aesthetics paired with waterproof performance, and for floating installations that reduce disruption. Tiles are gaining popularity among designers who want large-format stone looks without the weight, cure time, or grout maintenance of ceramic or porcelain. In commercial settings, rigid-core tiles support overnight lobby and corridor upgrades with realistic visuals and immediate return to service.

Across residential and commercial projects, visuals and surface finishes continue to improve, reducing aesthetic trade-offs with natural materials. Wider and longer plank assortments deliver room-scale realism that was previously difficult to achieve with shorter lengths. For tiles, patterning options allow statement floors in hospitality and healthcare while maintaining the maintenance profile that resilient platforms are known for. The SPC flooring market benefits from a stable installation method that supports phased work, reduces adhesive use, and results in cleaner job sites. Commercial publications from manufacturers reinforce how rigid-core products can replace more labor-intensive surfaces where uptime is a scheduling constraint.

The 4.0-5.0 mm tier accounted for 43.67% of the SPC flooring market in 2025, yet 5.1-6.0 mm products are forecast to grow at a 9.23% CAGR through 2031, as project teams pursue higher acoustic ratings and a more cushioned feel underfoot in premium residential and multi-family settings. Thicker constructions with integrated underlayment help projects meet minimum code thresholds for IIC and STC without assembling multiple layers, reducing variables and simplifying documentation. For developers seeking stronger impact sound control, thicker single-SKU assemblies reduce the risk of mismatches between field conditions and lab-tested packages. These choices also reduce telegraphing from minor subfloor unevenness, which limits callbacks for hollow spots or lippage on harder substrates. EPDs now provide quantified lifecycle metrics, such as global warming potential (kg CO2-eq/m2), energy use (MJ/m2), and end-of-life scenarios for different SPC constructions, enabling specifiers to compare how changes in thickness and underlayment affect environmental performance across project options.

There is a practical upper bound on thickness beyond which material cost and transitions to adjacent rooms become less forgiving. Within common ranges, however, the balance of acoustics, comfort, and ease of install continues to push premium formats into multi-family and higher-end residential specifications. The SPC flooring market size for premium assemblies is supported by projects where simplified code compliance and occupant comfort are procurement drivers. Underlayment knowledge has also improved as suppliers standardize acoustic definitions and field guidance. In the United States, minimum dwelling separation requirements for sound control anchor many of these choices in multi-family contexts. Education from underlayment providers continues to help teams select assemblies to reach target IIC, STC, and Delta IIC outcomes.

Complete Report Scope:

- By Product Type

- SPC Tiles

- SPC Planks

- By Product Thickness

- 4.0-5.0 mm

- 5.1-6.0 mm

- 6.1-6.5 mm

- Above 6.5 mm

- By Installation Method

- Self-Adhesive

- Glue-Down

- Interlocking/Click-lock

- Others

- By End User

- Residential

- Commercial

- By Distribution Channel

- B2C/Retail

- Home Centers

- Specialty Flooring Stores

- Online

- Other Distribution Channels

- B2B/Contractors

- B2C/Retail

- By Geography

- North America

- Canada

- United States

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- Rest of Europe

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South-East Asia

- Rest of Asia-Pacific

- Middle East & Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East & Africa

- North America

Geography Analysis

North America accounted for 35.88% of the global SPC market value in 2025. North American projects increasingly cite rapid renovation cycles and code-bound soundproofing thresholds as reasons to specify rigid-core assemblies that combine fast floating installation with underlayment-based acoustic control. Expanded domestic resilient capacity is expected to improve availability and reduce exposure to long shipping windows and variable surcharges. For spec-driven commercial projects, U.S. codes set floor-ceiling performance minimums for IIC and STC in dwelling separations. This baseline is often exceeded by thicker SPC assemblies with matched underlays. Those considerations keep the SPC flooring market relevant in rental refreshes and in new multi-family developments aiming for consistent resident experiences across stacked units. Company disclosures on resilient manufacturing expansion underline that lead times and product breadth will improve as new domestic lines reach full production.

Asia-Pacific is projected to record the fastest growth at a 9.77% CAGR from 2026 to 2031, reflecting both producer scale and urban housing stock adopting waterproof, resilient surfaces during renovation cycles in the SPC flooring market. European growth continues at a measured pace as mature markets weigh acoustic comfort, environmental disclosures, and public procurement criteria that prioritize detailed documentation. Trade actions in Europe have reshaped resin economics for downstream converters in 2025, which encouraged material diversification and investment in processes and lines closer to end demand. These conditions have expanded the SPC flooring market's range of reliable sources in Europe and supported project teams focused on validated data and compliant assemblies.

In the United Kingdom and the EU, anti-dumping measures implemented in 2025 altered some resin price relationships and affected converters' sourcing plans. These changes arrived alongside continued emphasis on transparent environmental product data and indoor-air quality documentation for resilient floors. Association-issued EPDs tailored to SPC provide a direct reference for teams comparing lifecycle reporting across product types, which supports consistent selection frameworks. As public and private green-building criteria spread, documentation and reclamation options become more relevant to procurement, and companies that can offer validated data and take-back programs are well-positioned. These factors sustain the SPC flooring market in Europe while steering it toward formats and suppliers that align with policy and documentation trends. The combined effect is steady demand with a tilt toward offerings that meet both performance and disclosure thresholds.

- Mohawk Industries

- Shaw Industries (incl. COREtec)

- Tarkett

- Mannington Mills

- CFL Flooring

- Novalis Innovative Flooring

- Beaulieu International Group (BerryAlloc)

- LX Hausys

- Huali Industrial Group

- DECNO Group

- NOX Corporation

- Forbo Flooring Systems

- Gerflor

- AHF Product

- HMTX Industries

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Waterproof rigid-core replacing laminate and flexible LVT in home and light commercial

- 4.2.2 DIY-friendly click-lock and renovation-led demand spike

- 4.2.3 Price-to-performance vs wood/tile expands addressable market

- 4.2.4 Growth of multi-family and rental refresh cycles

- 4.2.5 Tariff-driven supply shifts (China->Vietnam/Korea/Turkey) expand localized availability/spec acceptance

- 4.2.6 Fast-turn commercial fit-outs valuing minimal downtime installation

- 4.3 Market Restraints

- 4.3.1 PVC sustainability scrutiny and circularity/recycling barriers

- 4.3.2 Feedstock price volatility (PVC resin, additives)

- 4.3.3 Acoustics and scratch resistance trade-offs vs WPC/laminate

- 4.3.4 Tariff/trade actions and non-tariff barriers raise landed costs and complexity

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Industry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 SPC Tiles

- 5.1.2 SPC Planks

- 5.2 By Product Thickness

- 5.2.1 4.0-5.0 mm

- 5.2.2 5.1-6.0 mm

- 5.2.3 6.1-6.5 mm

- 5.2.4 Above 6.5 mm

- 5.3 By Installation Method

- 5.3.1 Self-Adhesive

- 5.3.2 Glue-Down

- 5.3.3 Interlocking/Click-lock

- 5.3.4 Others

- 5.4 By End User

- 5.4.1 Residential

- 5.4.2 Commercial

- 5.5 By Distribution Channel

- 5.5.1 B2C/Retail

- 5.5.1.1 Home Centers

- 5.5.1.2 Specialty Flooring Stores

- 5.5.1.3 Online

- 5.5.1.4 Other Distribution Channels

- 5.5.2 B2B/Contractors

- 5.5.1 B2C/Retail

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 Canada

- 5.6.1.2 United States

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Peru

- 5.6.2.3 Chile

- 5.6.2.4 Argentina

- 5.6.2.5 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Spain

- 5.6.3.5 Italy

- 5.6.3.6 BENELUX (Belgium, Netherlands, Luxembourg)

- 5.6.3.7 NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- 5.6.3.8 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 India

- 5.6.4.2 China

- 5.6.4.3 Japan

- 5.6.4.4 Australia

- 5.6.4.5 South Korea

- 5.6.4.6 South-East Asia

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East & Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Nigeria

- 5.6.5.5 Rest of Middle East & Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Mohawk Industries

- 6.4.2 Shaw Industries (incl. COREtec)

- 6.4.3 Tarkett

- 6.4.4 Mannington Mills

- 6.4.5 CFL Flooring

- 6.4.6 Novalis Innovative Flooring

- 6.4.7 Beaulieu International Group (BerryAlloc)

- 6.4.8 LX Hausys

- 6.4.9 Huali Industrial Group

- 6.4.10 DECNO Group

- 6.4.11 NOX Corporation

- 6.4.12 Forbo Flooring Systems

- 6.4.13 Gerflor

- 6.4.14 AHF Product

- 6.4.15 HMTX Industries

7 Market Opportunities & Future Outlook

- 7.1 Healthcare & clinic retrofits: hygienic, quick-install SPC with enhanced stain/chemical resistance

- 7.2 Acoustic code-compliant SPC with pre-attached underlayment for multi-family/high-rise specifications