|

市場調查報告書

商品編碼

2072638

美國精密陶瓷:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)United States Advanced Ceramics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

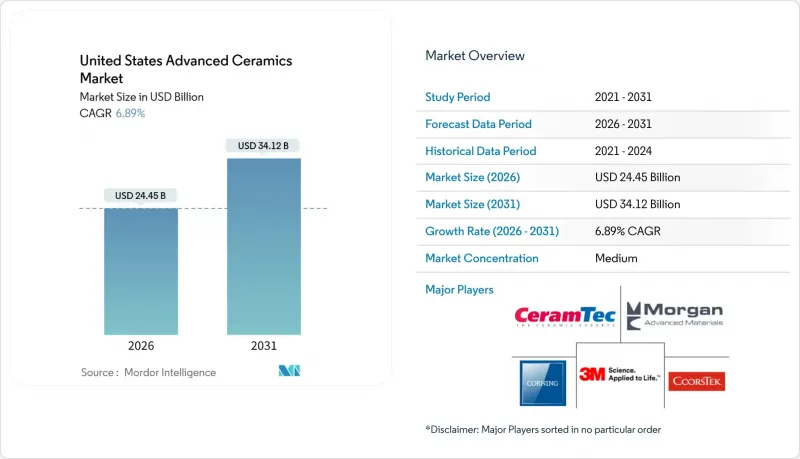

據 Mordor Intelligence 稱,美國精密陶瓷市場在 2026 年的估值為 244.5 億美元,預計在預測期(2026-2031 年)內將以 6.89% 的複合年成長率成長,到 2031 年達到 341.2 億美元。

本報告按材料類型(氧化鋁、鈦酸鹽、氧化鋯、碳化矽及其他)、類別(單片陶瓷、陶瓷基質複合材料、陶瓷塗層)和終端用戶產業(電氣電子、汽車及交通運輸、工業、化學、醫療及其他終端用戶產業)進行細分。市場預測以美元計價。

美國精密陶瓷市場趨勢與洞察

來自航太和國防領域的強勁需求

2024年,美國國防部簽署了MACH契約,擴大了陶瓷基質複合材料(CMC)的應用範圍。這些合約預計CMC將在遠超鎳基高溫合金極限的極端溫度下運作。陸軍的遠程火砲項目引領了這一趨勢,該項目指定使用碳化矽(SiC)內襯來延長砲管壽命。此舉正在加速反應黏結SiC零件的普及應用。同時,在民用航太領域,通用電氣航空航太公司的RISE驗證機採用了CMC外罩,顯著減輕了單架飛機的重量並降低了油耗。為了進一步支持軍方的努力,2025年3月宣布了根據《國防生產法》第3章提供的津貼。這項計畫旨在將部分軍用陶瓷供應帶回國內市場,減少對海外供應的依賴。這些措施不僅推動了先進陶瓷的量產需求,也為供應商提供了更清晰的多年預測。

電子元件和半導體的微型化進程正在迅速加快。

隨著邏輯晶片微型化至2奈米節點和高頻寬記憶體堆疊,每個晶片封裝所需的陶瓷用量也不斷增加。英特爾位於俄亥俄州的巨型工廠計劃於2026年底開始量產,預計每年將消耗大量的氧化鋁基板。國家先進封裝製造計畫正共同資助玻璃陶瓷中介層技術,可降低100GHz以上頻率的訊號損耗。這項進步為人工智慧加速器中的晶片級架構鋪平了道路。目前,單一高階加速器整合了多個多層陶瓷電容器,每個電容器都需處理高瞬態電流。與2020年的數據相比,這一數字顯著成長。鑑於亞微米級的分層可能導致潛在的現場故障,人們越來越依賴採用自動化光學檢測系統和電腦斷層掃描(CT)系統的檢測系統。電子產品需求的激增不僅在短期內提高了產量,也推高了高純度粉末和基板坯料的平均售價。

高昂的製造和加工成本

使用鑽石刀具進行精密研磨會產生大量的材料去除成本。對於複雜形狀的工件,尤其是在使用金屬合金時,這些成本會進一步增加。陶瓷渦輪增壓器轉子雖然效率更高,但比鎳基產品更昂貴。這種價格差異限制了陶瓷轉子的應用範圍,使其僅限於高階車型。製造商面臨著因收縮率變化而導致的良率下降。為了解決這個問題,他們採用先將生坯成型至更大尺寸,然後再進行機械加工以達到指定公差的工藝,但這會增加生產時間。黏著劑噴塗顯著減少了這種二次加工的需求,但氧化鋁和碳化矽粉末的高成本阻礙了它們在工業零件中的廣泛應用。粉末合成技術的進步和混合製造流程的改進有望緩解這些成本挑戰。

細分市場分析

由於氧化鋁具有極高的成本績效,預計到2025年,其在精密陶瓷市場將佔據41.46%的佔有率,使其成為半導體腔室、防彈裝甲和耐磨工廠組件的理想材料。隨著電動車逆變器需求的成長,對具有高散熱能力的基板的需求也隨之激增,這將使Wolfspeed在2025會計年度的基板規模預計到2031年將以7.82%的複合年成長率成長。

隨著 ISO 6474-2:2024 標準日益嚴格,醫用級氧化鋁新增了顆粒級可追溯性要求。這導致合規成本急劇上升,尤其給小規模磨粉廠帶來了沉重負擔。同時,與黏著劑噴塗製程相容的氮化矽粉末的出現正在革新整個產業。這些創新顯著縮短了渦輪機零件的前置作業時間,並大幅減少了材料浪費。生命週期評估 (LCA) 凸顯了碳化矽泵密封件在腐蝕性環境下延長平均故障間隔時間 (MTBF) 的優勢。這種顯著的性能提升足以抵消更高的材料成本。隨著設計人員越來越重視運作和小型化,氧化鋁仍將保持其作為通用基板的地位,但預計其市場佔有率將在 2028 年後下降,為鈦酸鹽和碳化矽產量的成長讓路。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 來自航太和國防領域的強勁需求

- 電子和半導體領域小型化的快速發展

- 快速部署5G和電力電子基礎設施

- 聯邦政府為高超音速和太空計畫提供的資金

- 引入積層製造技術,縮短前置作業時間。

- 市場限制因素

- 高昂的生產和加工成本

- 與脆性和設計柔軟性相關的限制

- 關鍵礦產供應鏈中的脆弱性

- 價值鏈分析

- 監理情勢

- 波特五力模型

第5章 市場規模與成長預測

- 材料類型

- 氧化鋁

- 鈦酸鹽

- 氧化鋯

- 碳化矽

- 其他材料類型

- 按類別類型

- 單片陶瓷

- 陶瓷基質複合材料

- 陶瓷塗層

- 按最終用戶行業分類

- 電氣和電子設備

- 汽車和運輸業

- 產業

- 化學品

- 醫學領域

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- 3M

- Blasch Precision Ceramics, Inc.

- CeramTec GmbH

- CoorsTek Inc.

- Corning Incorporated

- Elan Technology

- Ferrotec Corporation

- KYOCERA Corporation

- Materion Corporation

- Morgan Advanced Materials

- Saint-Gobain

第7章 市場機會與未來展望

According to Mordor Intelligence, the united states advanced ceramics market size is estimated at USD 24.45 billion in 2026, and is expected to reach USD 34.12 billion by 2031, at a CAGR of 6.89% during the forecast period (2026-2031).

This report is Segmented by Material Type (Alumina, Titanate, Zirconia, Silicon Carbide, and Other Types), Class Type (Monolithic Ceramics, Ceramic Matrix Composites, and Ceramic Coatings), and End-User Industry (Electrical and Electronics, Automotive and Transportation, Industrial, Chemicals, Medical, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

United States Advanced Ceramics Market Trends and Insights

Strong Demand from Aerospace and Defense

In 2024, the Pentagon inked MACH contracts, pushing the boundaries of ceramic matrix composite (CMC) procurement. These contracts target operations at extreme temperatures, surpassing the limits of nickel superalloys. The Army's Extended Range Cannon Artillery project is leading the charge, specifying silicon-carbide liners that extend barrel life. This move is accelerating the adoption of reaction-bonded SiC components. Meanwhile, in the commercial aerospace arena, GE Aerospace's RISE demonstrator is leveraging CMC shrouds, achieving significant weight reduction per aircraft and translating to fuel savings. Further underscoring the military's commitment, a grant under the Defense Production Act Title III was announced in March 2025. This initiative aims to repatriate a portion of the military's ceramic supply, reducing dependence on foreign sources. Together, these initiatives are not only driving demand for advanced ceramics into mainstream production but also providing suppliers with a clearer, multiyear outlook.

Electronics and Semiconductor Miniaturization Surge

As logic scales down to 2-nanometer nodes and high-bandwidth memory stacks, ceramic consumption per chip package rises. Intel's Ohio megasite, set to commence volume production in late 2026, is projected to consume significant amounts of alumina substrates annually. The National Advanced Packaging Manufacturing Program is co-funding glass-ceramic interposers, which reduce signal loss at frequencies above 100 GHz. This advancement paves the way for chiplet architectures in AI accelerators. Presently, a single high-end accelerator boasts numerous multilayer ceramic capacitors, each handling transient currents at high levels, a significant increase from 2020 figures. Given that sub-micron delaminations can lead to latent field failures, there's a growing reliance on inspection regimes utilizing automated optical and computed-tomography systems. This surge in electronics not only fuels immediate volume growth but also drives up average selling prices for high-purity powders and substrate blanks.

High Production and Machining Costs

Precision grinding with diamond tools incurs significant costs for material removal. This cost escalates for intricate geometries, especially when metal alloys are used. While ceramic turbocharger rotors offer efficiency benefits, they come with a premium over their nickel-based counterparts. This price difference confines their use to high-end vehicle trims. Producers face yield losses due to shrinkage variability. To counter this, they oversize green bodies and then machine them back to the desired tolerance, a process that extends production time. Although binder-jetting can significantly reduce the need for this secondary machining, the high cost of alumina and silicon-carbide powders hinders their widespread adoption for industrial parts. The cost challenges are expected to diminish as powder synthesis techniques advance and hybrid manufacturing processes become more refined.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Deployment of 5G and Power-Electronics Infrastructure

- Federal Funding for Hypersonic and Space Programs

- Brittleness and Design-Flexibility Constraints

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Alumina accounted for 41.46% of the advanced ceramics market share in 2025, thanks to its cost-performance ratio, making it ideal for semiconductor chambers, ballistic armor, and wear-resistant plant components. As demand for EV inverters grows, the need for substrates with high heat dissipation capabilities has surged, propelling Wolfspeed to achieve substantial substrate revenue in fiscal 2025. Titanate-based dielectrics, though smaller in tonnage, are advancing at a 7.82% CAGR through 2031, powered by the densification of 5G base stations and automotive radar modules that need high-permittivity capacitors.

Under the tightening regulations of ISO 6474-2:2024, there's a new mandate for granular traceability in medical-grade alumina. This has led to a spike in compliance costs, particularly burdening smaller mills. Meanwhile, the emergence of binder-jettable silicon-nitride powders is revolutionizing the industry. These innovations are significantly reducing turbine-component lead times and achieving a notable reduction in material waste. Life-cycle assessments highlight the advantages of silicon-carbide pump seals, which are extending the mean time between failures in corrosive environments. This significant enhancement justifies the premium on material costs. As designers increasingly prioritize uptime and miniaturization, it's anticipated that while alumina will maintain its foothold in commodity substrates, its market share will wane post-2028, giving way to the rising volumes of titanate and silicon-carbide.

Complete Report Scope:

- By Material Type

- Alumina

- Titanate

- Zirconia

- Silicon Carbide

- Other Material Types

- By Class Type

- Monolithic Ceramics

- Ceramic Matrix Composites

- Ceramic Coatings

- By End-user Industry

- Electrical and Electronics

- Automotive and Transportation

- Industrial

- Chemicals

- Medical

- Other End-user Industries

List of Companies Covered in this Report:

- 3M

- Blasch Precision Ceramics, Inc.

- CeramTec GmbH

- CoorsTek Inc.

- Corning Incorporated

- Elan Technology

- Ferrotec Corporation

- KYOCERA Corporation

- Materion Corporation

- Morgan Advanced Materials

- Saint-Gobain

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Strong Demand from Aerospace and Defense

- 4.2.2 Electronics and Semiconductor Miniaturization Surge

- 4.2.3 Rapid Deployment of 5G and Power-Electronics Infrastructure

- 4.2.4 Federal Funding for Hypersonic and Space Programs

- 4.2.5 Additive Manufacturing Adoption Reducing Lead-Times

- 4.3 Market Restraints

- 4.3.1 High Production and Machining Costs

- 4.3.2 Brittleness and Design-Flexibility Constraints

- 4.3.3 Critical Mineral Supply-Chain Vulnerability

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products and Services

- 4.6.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material Type

- 5.1.1 Alumina

- 5.1.2 Titanate

- 5.1.3 Zirconia

- 5.1.4 Silicon Carbide

- 5.1.5 Other Material Types

- 5.2 By Class Type

- 5.2.1 Monolithic Ceramics

- 5.2.2 Ceramic Matrix Composites

- 5.2.3 Ceramic Coatings

- 5.3 By End-user Industry

- 5.3.1 Electrical and Electronics

- 5.3.2 Automotive and Transportation

- 5.3.3 Industrial

- 5.3.4 Chemicals

- 5.3.5 Medical

- 5.3.6 Other End-user Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)}

- 6.4.1 3M

- 6.4.2 Blasch Precision Ceramics, Inc.

- 6.4.3 CeramTec GmbH

- 6.4.4 CoorsTek Inc.

- 6.4.5 Corning Incorporated

- 6.4.6 Elan Technology

- 6.4.7 Ferrotec Corporation

- 6.4.8 KYOCERA Corporation

- 6.4.9 Materion Corporation

- 6.4.10 Morgan Advanced Materials

- 6.4.11 Saint-Gobain

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

先進陶瓷材料市場預測至2034年—按材料類型、產品類型、分類、應用、最終用戶和地區分類的全球分析

先進陶瓷材料市場預測至2034年—按材料類型、產品類型、分類、應用、最終用戶和地區分類的全球分析 陶瓷丙烷市場 - 全球產業規模、佔有率、趨勢、機會、預測:按應用、類型、地區和競爭格局分類,2021-2031年超高溫材料市場預測至2034年-按材料、成分、製程、應用、最終用戶和地區分類的全球分析

陶瓷丙烷市場 - 全球產業規模、佔有率、趨勢、機會、預測:按應用、類型、地區和競爭格局分類,2021-2031年超高溫材料市場預測至2034年-按材料、成分、製程、應用、最終用戶和地區分類的全球分析 先進陶瓷市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測

先進陶瓷市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測 特種高性能陶瓷市場:依材料、最終用戶、製造流程和產品形式分類-2026-2032年全球市場預測

特種高性能陶瓷市場:依材料、最終用戶、製造流程和產品形式分類-2026-2032年全球市場預測 先進陶瓷市場報告:按材料、類型、終端應用產業和地區分類(2026-2034 年)

先進陶瓷市場報告:按材料、類型、終端應用產業和地區分類(2026-2034 年) 2026-2034年全球先進陶瓷市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球先進陶瓷市場規模、佔有率、趨勢和成長分析報告 陶瓷嵌件芯市場規模、佔有率和成長分析:依材質等級、製造流程、形狀/複雜程度、應用領域和地區分類-產業預測,2026-2033年先進陶瓷市場:依材料、產品類型、終端用戶產業及通路分類-2026-2032年全球市場預測

陶瓷嵌件芯市場規模、佔有率和成長分析:依材質等級、製造流程、形狀/複雜程度、應用領域和地區分類-產業預測,2026-2033年先進陶瓷市場:依材料、產品類型、終端用戶產業及通路分類-2026-2032年全球市場預測 全球先進陶瓷市場(至 2035 年):依材料類型、產品類別、應用類型、終端用戶產業、地區、產業趨勢及預測

全球先進陶瓷市場(至 2035 年):依材料類型、產品類別、應用類型、終端用戶產業、地區、產業趨勢及預測