|

市場調查報告書

商品編碼

2038420

先進陶瓷市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測Advanced Ceramics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

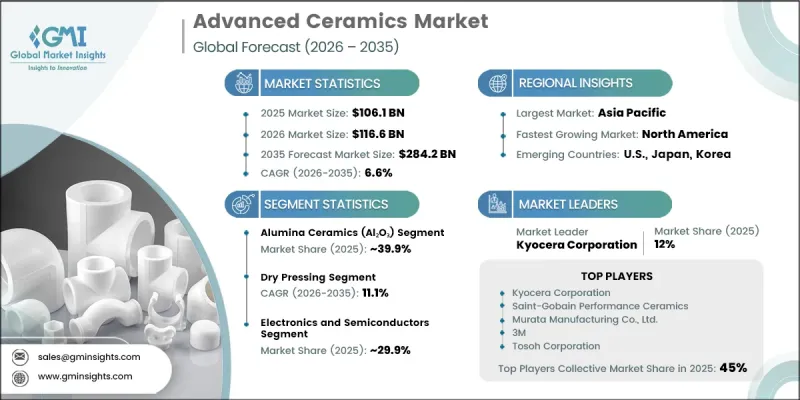

預計到 2025 年,全球先進陶瓷市場規模將達到 1,061 億美元,年複合成長率為 6.6%,到 2035 年將達到 2,842 億美元。

過去幾年,在電氣化、工業自動化和醫療技術創新的推動下,該市場經歷了穩定成長。高性能陶瓷在對耐久性、永續性和小型化要求極高的領域日益重要。清潔能源、高效能運算和電動車領域的原始設備製造商 (OEM) 正在採用陶瓷,以利用其耐熱性、耐磨性和化學穩定性。生物相容性氧化鋯和氧化鋁廣泛應用於醫療設備,而陶瓷塗層則因其熱穩定性和輕量化優勢而被航太和國防工業所採用。地緣政治格局的變化正在推動美國和歐盟本地陶瓷供應鏈的發展,增強了該行業的韌性。監管壓力和企業努力正在促成永續製造流程和可回收陶瓷產品的出現,例如 CoorsTek 和 Saint-Gobain 等公司正在投資低碳燒結和閉合迴路生產系統。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 1061億美元 |

| 預測金額 | 2842億美元 |

| 複合年成長率 | % |

到2025年,氧化鋁陶瓷產業將佔據39.9%的市場。氧化鋁、氧化鋯、碳化矽和氮化矽等先進原料的應用正在推動電子、汽車和醫療等領域的發展。這些材料對全球工業供應鏈至關重要,因為它們具有優異的硬度、熱穩定性、耐腐蝕性和高性能,特別適用於小型化應用。

預計到2025年,乾壓成型法將佔據27.1%的最大市場佔有率,並預計在2026年至2035年間以11.1%的複合年成長率成長。該製程與燒結技術相結合,被廣泛用於製造具有均勻可靠材料性能的高密度零件。等靜壓成型也常用於實現均勻壓縮,尤其適用於對結構完整性要求較高的應用。此外,射出成型和擠出成型則用於製造複雜形狀的零件和連續型材,以滿足各種設計需求。

預計到2025年,北美先進陶瓷市場佔有率將達到22.4%,反映出該地區在全球市場的強勁成長動能。該市場主要受航太、國防、電子、醫療保健和清潔能源等行業的強勁需求驅動,並正經歷顯著的技術進步。北美擁有成熟的研發能力、先進的製造基礎設施以及嚴格的性能和安全標準,這些優勢共同促進了高性能陶瓷解決方案的開發和應用,鞏固了北美作為高階先進陶瓷生產和創新領先中心的地位。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 電子和半導體封裝應用領域的需求不斷成長

- 電動車的普及和高級駕駛輔助系統(ADAS)的日益普及

- 因其耐熱性和耐磨性,在航太零件中的應用範圍擴大。

- 產業潛在風險與挑戰

- 加工成本高,原料採購成本也高。

- 市場機遇

- 陶瓷在固態電池技術的應用

- 擴展 5G 和射頻技術的基礎設施

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 依材料類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利趨勢

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲(MEA)

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依材料類型分類,2022-2035年

- 氧化鋁陶瓷(Al2O3)

- 高純度氧化鋁(Al2O3 99.5% 或更高)

- 標準氧化鋁(95-99% Al2O3)

- 碳化矽陶瓷(SiC)

- 反應燒結碳化矽(RBSC)

- 燒結碳化矽(SSiC)

- 熱壓碳化矽(HPSiC)

- 其他

- 氧化鋯陶瓷(ZrO2)

- 釔安定氧化鋯(YSZ)

- 鎂穩定氧化鋯(MSZ)

- 二氧化鈰穩定氧化鋯 (CSZ)

- 其他

- 氮化矽陶瓷(Si2N3)

- 反應鍵結氮化矽(RBSN)

- 熱壓縮氮化矽(HPSN)

- 其他

- 碳化鈦

- 碳化硼

- 其他

第6章 市場估價與預測:依製造流程分類,2022-2035年

- 乾壓

- 燒結

- 等靜壓成型(CIP/HIP)

- 射出成型

- 擠出成型和模壓

- 積層製造/3D列印

- 磁帶鑄造

- 其他

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 電子和半導體

- 半導體製造設備

- 電子基板和封裝

- 電容器和電阻器

- 5G 和射頻應用

- 其他

- 汽車應用

- 引擎部件和溫度控管

- 電動車的電力電子設備

- 感測器和排放氣體控制

- 煞車系統和易損零件

- 其他

- 航太/國防

- 隔熱塗層

- 陶瓷基質複合材料(CMCs)

- 裝甲和彈道防護

- 其他

- 醫學和生物醫學

- 整形外科植入

- 牙科用途

- 手術器械

- 其他

- 能源和發電

- 燃料電池和電池

- 太陽能應用

- 核能應用

- 其他

- 工業和製造業

- 切削刀具和磨損部件

- 化學處理設備

- 耐火材料應用

- 其他

- 其他

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第9章:公司簡介

- Kyocera Corporation

- CoorsTek Inc.

- 3M

- CeramTec GmbH

- Morgan Advanced Materials

- Saint-Gobain Performance Ceramics

- Rauschert GmbH

- McDanel Advanced Ceramic Technologies

- Elan Technology

- Ferrotec(USA)Corporation

- Advanced Ceramic Materials(ACM)Corporation

- Blasch Precision Ceramics, Inc.

- Momentive Technologies

- MARUWA Co., Ltd

- Superior Technical Ceramics

- Schunk Group

- NTK CERATEC CO., LTD.

- Tosoh Corporation

- Murata Manufacturing Co., Ltd.

- Carborundum Universal Limited(CUMI)

The Global Advanced Ceramics Market was valued at USD 106.1 billion in 2025 and is estimated to grow at a CAGR of 6.6% to reach USD 284.2 billion by 2035.

The market has seen consistent growth over the past few years, driven by innovations in electrification, industrial automation, and medical technologies. Advanced ceramics are gaining importance in sectors emphasizing durability, sustainability, and miniaturization. Original equipment manufacturers in clean energy, high-performance computing, and e-mobility rely on ceramics for their heat resistance, wear resistance, and chemical inertness. Biocompatible grades of zirconia and alumina are widely used in medical devices, while aerospace and defense industries utilize ceramic coatings for thermal stability and weight reduction. Geopolitical shifts have prompted the development of local ceramic supply chains in the U.S. and EU, enhancing industrial resilience. Sustainable manufacturing processes and recyclable ceramic products are emerging due to regulatory pressures and corporate initiatives, with companies like CoorsTek and Saint-Gobain investing in low-carbon sintering and closed-loop production systems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $106.1 Billion |

| Forecast Value | $284.2 Billion |

| CAGR | % |

The alumina ceramics segment held 39.9% share in 2025 The use of advanced raw materials such as alumina, zirconia, silicon carbide, and silicon nitride is driving applications across electronics, automotive, and medical sectors. These materials offer superior hardness, thermal stability, corrosion resistance, and high-performance miniaturized applications, making them essential for global industrial supply chains.

Dry pressing accounted for the largest share of 27.1% in 2025 and is projected to expand at a CAGR of 11.1% from 2026 to 2035. This process, along with sintering techniques, is widely used to manufacture high-density components with uniform and reliable material properties. Isostatic pressing is also commonly adopted to achieve consistent compaction, particularly for applications requiring high structural integrity. In addition, injection molding and extrusion methods are used to produce complex-shaped parts and continuous profiles tailored to diverse design requirements.

North America Advanced Ceramics Market held a 22.4% share in 2025, reflecting strong regional growth on a global scale. The market demonstrates a high level of technological advancement, driven by robust demand from aerospace, defense, electronics, healthcare, and clean energy industries. The region benefits from well-established research and development capabilities, advanced manufacturing infrastructure, and stringent performance and safety standards. These factors collectively support the development and adoption of high-performance ceramic solutions, strengthening North America's position as a key hub for premium advanced ceramics production and innovation.

Key players in the Global Advanced Ceramics Market include Morgan Advanced Materials, Saint-Gobain Performance Ceramics, Kyocera Corporation, Murata Manufacturing Co., Ltd., CoorsTek Inc., NGK Spark Plug Co., Ltd., McDanel Advanced Ceramic Technologies, CeramTec GmbH, 3M, Rauschert GmbH, Ferrotec Holdings Corporation, and Elan Technology. Companies in the Advanced Ceramics Market strengthen their position through multiple strategic initiatives. They are investing heavily in research and development to create high-performance, sustainable, and cost-efficient ceramics. Mergers, acquisitions, and strategic partnerships expand technological capabilities, production capacity, and geographic reach. Firms are also adopting low-carbon manufacturing processes and closed-loop production systems to meet sustainability targets. Diversifying product portfolios, entering new end-use sectors, and optimizing supply chains enhance operational efficiency and resilience..

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material Type

- 2.2.3 Manufacturing Process

- 2.2.4 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand in electronics and semiconductor packaging applications

- 3.2.1.2 Expansion of EVs and advanced driver-assistance systems (ADAS) adoption

- 3.2.1.3 Increased use in aerospace components for thermal and wear resistance

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High processing costs and expensive raw material sourcing

- 3.2.3 Market opportunities

- 3.2.3.1 Ceramic use in solid-state battery technologies

- 3.2.3.2 Growing infrastructure for 5G and RF technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By Material type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Material Type, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Alumina ceramics (Al2O3)

- 5.2.1 High-purity alumina (>99.5% Al2O3)

- 5.2.2 Standard alumina (95-99% Al2O3)

- 5.3 Silicon carbide ceramics (SiC)

- 5.3.1 Reaction bonded silicon carbide (RBSC)

- 5.3.2 Sintered silicon carbide (SSiC)

- 5.3.3 Hot pressed silicon carbide (HPSiC)

- 5.3.4 Others

- 5.4 Zirconia ceramics (ZrO2)

- 5.4.1 Yttria-stabilized zirconia (YSZ)

- 5.4.2 Magnesia-stabilized zirconia (MSZ)

- 5.4.3 Ceria-stabilized zirconia (CSZ)

- 5.4.4 Others

- 5.5 Silicon nitride ceramics (Si2N3)

- 5.5.1 Reaction bonded silicon nitride (RBSN)

- 5.5.2 Hot pressed silicon nitride (HPSN)

- 5.5.3 Others

- 5.6 Titanium carbide

- 5.7 Boron carbide

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Manufacturing Process, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Dry pressing

- 6.3 Sintering

- 6.4 Isostatic pressing (CIP/HIP)

- 6.5 Injection molding

- 6.6 Extrusion and forming

- 6.7 Additive manufacturing / 3D printing

- 6.8 Tape casting

- 6.9 Others

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Electronics and semiconductors

- 7.2.1 Semiconductor manufacturing equipment

- 7.2.2 Electronic substrates and packages

- 7.2.3 Capacitors and resistors

- 7.2.4 5G and RF applications

- 7.2.5 Others

- 7.3 Automotive applications

- 7.3.1 Engine components and thermal management

- 7.3.2 Electric vehicle power electronics

- 7.3.3 Sensors and emission control

- 7.3.4 Brake systems and wear parts

- 7.3.5 Others

- 7.4 Aerospace and defense

- 7.4.1 Thermal barrier coatings

- 7.4.2 Ceramic matrix composites (CMCs)

- 7.4.3 Armor and ballistic protection

- 7.4.4 Others

- 7.5 Medical and biomedical

- 7.5.1 Orthopedic implants

- 7.5.2 Dental applications

- 7.5.3 Surgical instruments

- 7.5.4 Others

- 7.6 Energy and power generation

- 7.6.1 Fuel cells and batteries

- 7.6.2 Solar energy applications

- 7.6.3 Nuclear applications

- 7.6.4 Others

- 7.7 Industrial and manufacturing

- 7.7.1 Cutting tools and wear parts

- 7.7.2 Chemical processing equipment

- 7.7.3 Refractory applications

- 7.7.4 Others

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Kyocera Corporation

- 9.2 CoorsTek Inc.

- 9.3 3M

- 9.4 CeramTec GmbH

- 9.5 Morgan Advanced Materials

- 9.6 Saint-Gobain Performance Ceramics

- 9.7 Rauschert GmbH

- 9.8 McDanel Advanced Ceramic Technologies

- 9.9 Elan Technology

- 9.10 Ferrotec (USA) Corporation

- 9.11 Advanced Ceramic Materials (ACM) Corporation

- 9.12 Blasch Precision Ceramics, Inc.

- 9.13 Momentive Technologies

- 9.14 MARUWA Co., Ltd

- 9.15 Superior Technical Ceramics

- 9.16 Schunk Group

- 9.17 NTK CERATEC CO., LTD.

- 9.18 Tosoh Corporation

- 9.19 Murata Manufacturing Co., Ltd.

- 9.20 Carborundum Universal Limited (CUMI)

先進功能陶瓷市場預測至2034年:按材料類型、性能、製造流程、應用、產業和地區分類的全球分析氧化物陶瓷市場預測(2034 年)-按材料類型、形狀、性能、應用、產業和地區分類的全球分析結構陶瓷市場預測至2034年-按材料類型、形狀、性能、應用、產業和地區分類的全球分析能源陶瓷市場預測至2034年-按產品類型、材料類型、性能、應用、產業和地區分類的全球分析陶瓷粉末市場預測至2034年—按材料類型、純度、製造方法、應用、產業和地區分類的全球分析非氧化物陶瓷市場預測至2034年-按材料類型、形狀、性能、應用、產業和地區分類的全球分析

先進功能陶瓷市場預測至2034年:按材料類型、性能、製造流程、應用、產業和地區分類的全球分析氧化物陶瓷市場預測(2034 年)-按材料類型、形狀、性能、應用、產業和地區分類的全球分析結構陶瓷市場預測至2034年-按材料類型、形狀、性能、應用、產業和地區分類的全球分析能源陶瓷市場預測至2034年-按產品類型、材料類型、性能、應用、產業和地區分類的全球分析陶瓷粉末市場預測至2034年—按材料類型、純度、製造方法、應用、產業和地區分類的全球分析非氧化物陶瓷市場預測至2034年-按材料類型、形狀、性能、應用、產業和地區分類的全球分析 特種高性能陶瓷市場:依材料、產品類型、製造流程、純度等級、耐熱等級及最終用戶分類-2026-2032年全球市場預測

特種高性能陶瓷市場:依材料、產品類型、製造流程、純度等級、耐熱等級及最終用戶分類-2026-2032年全球市場預測 美國精密陶瓷:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)先進陶瓷材料市場預測至2034年—按材料類型、產品類型、分類、應用、最終用戶和地區分類的全球分析

美國精密陶瓷:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)先進陶瓷材料市場預測至2034年—按材料類型、產品類型、分類、應用、最終用戶和地區分類的全球分析 陶瓷丙烷市場 - 全球產業規模、佔有率、趨勢、機會、預測:按應用、類型、地區和競爭格局分類,2021-2031年

陶瓷丙烷市場 - 全球產業規模、佔有率、趨勢、機會、預測:按應用、類型、地區和競爭格局分類,2021-2031年