|

市場調查報告書

商品編碼

2072619

電視廣播服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Television Broadcasting Service - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

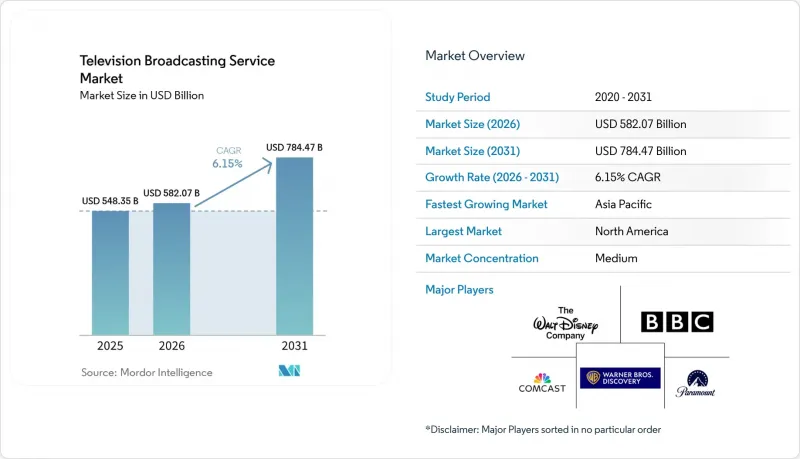

據 Mordor Intelligence 稱,2025 年電視廣播服務市值為 5483.5 億美元,預計到 2031 年將達到 7844.7 億美元,而 2026 年為 5820.7 億美元,預測期(2026-2031 年)的複合成長率為 6.15%。

本報告依分送平台(地面電波電視、有線電視、IPTV、OTT/網路電視及其他)、服務類型(訂閱制、廣告支援制及其他)、廣播公司類型(公共廣播、私人廣播及其他)、內容類型(娛樂和戲劇、體育、新聞和時事及其他)以及地區進行分類。市場預測以美元計價。

全球電視廣播服務市場的趨勢與洞察

「停掉有線電視服務」正在推動OTT和串流電視的普及。

到2026年1月,串流媒體將佔電視總使用量的47%,較上月增加5.4個百分點。家庭用戶在保持高速寬頻的同時,取消了多頻道捆綁訂閱,並將支出轉向提供點播內容庫和直播頻道的點播應用程式。康卡斯特(Comcast)2025年第四季的國內付費電視用戶數量較上年同期下降了10%,而Peacock同期付費用戶數量則增加了12%。由於免費服務依靠廣告收入維持運營,且無需訂閱費,因此用戶轉換門檻顯著降低,加速了有線電視用戶的流失。到了2026年1月,Tubi和Roku Channel的觀眾佔有率均實現中等個位數的成長。因此,廣播公司正將資金轉向D2C(直接面對消費者)技術,優先考慮流暢的應用體驗和豐富的節目庫,而非談判分銷合約。

廣告主對體育賽事直播中廣告位的需求日益成長

2014年至2024年間,體育賽事轉播權的價值成長了113%,遠超過廣告市場的整體成長速度,這主要得益於品牌方對即時觸達和高互動性的重視。 Netflix在日本轉播的世界棒球經典賽吸引了3,140萬觀眾,這表明即使是訂閱制平台也願意為獨家實況活動支付高價。在快節奏的串流服務中,體育頻道的廣告收入成長了105%,廣告留存率也比影片高出71%。由於資金雄厚的串流媒體服務和國家級廣播公司壟斷了高關注度內容,當地電視台被迫將重心轉向小眾體育賽事和補充節目。

SVOD平台正在搶走傳統線性電視的觀眾。

儘管串流媒體用戶增加至1.316億,華納兄弟探索頻道2025年第四季的線性電視網路收入仍較去年同期下降12%。隨著觀眾群體的轉移,線性廣告位正在萎縮,而SVOD(訂閱視訊點播)的每位觀眾收入低於傳統電視廣播。康卡斯特在2025年第四季流失了10%的美國國內付費電視用戶,進一步加劇了長達十年的「停掉有線電視服務」趨勢。因此,廣播公司必須投資建設冗餘基礎設施,以運營面向消費者的直接應用程式,同時還要維持其傳統電視網路,這在轉型期給利潤率帶來了壓力。

細分市場分析

到2025年,OTT和網路電視將佔電視廣播服務市場收入的36.45%,預計到2031年將以6.57%的複合年成長率成長。這一成長反映了智慧電視作業系統的普及,這些作業系統推動了串流媒體應用的發展,以及行動網路對影片流量的零費率。有線和衛星廣播仍然是農村和沿海地區的主要傳輸方式,但隨著低地球軌道寬頻預計將在三年內成為可行的替代方案,用戶持續下降。地面電波電視受益於ATSC 3.0的互動性,但其擴張受到頻率重新分配的限制。 IPTV的市佔率仍僅限於通訊業者在光纖覆蓋區域提供的配套服務。

廣播公司目前正採用整合技術棧,將單一內容流以FAST訊號的形式傳輸,並提供線性頻道、點播劇集和動態廣告插入功能。派拉蒙影業於2025年第四季整合了其Paramount+和Pluto TV的工作流程,使其單流成本降低了15%。這種模式既能確保規模經濟效益,又能適應不斷變化的觀眾偏好,從而確保OTT平台電視廣播服務市場的成長,同時又不會完全取代傳統電視模式。

預計到2025年,廣告支援服務將佔總收入的55.78%,並以6.88%的複合年成長率成長,超過訂閱服務的成長速度,這反映了人們對家庭預算負擔日益加重的擔憂。 Netflix的廣告支援計畫在2026年第一季達到1.9億月有效用戶,大幅提升了季度收入,達到122.5億美元。 Roku在2025年第四季的平台收入達到12.2億美元,凸顯了其FAST模式的經濟可行性,該模式得益於更高的廣告完成率和更精準的定向投放,從而提高了每千次展示成本(CPM)。

訂閱服務仍然是熱門原創內容的基石,但內容庫更新的停滯不前導致解約率急劇上升。混合模式如今十分普遍,以廣告支援的免費計劃作為切入點,引導用戶升級到高級計劃,從而滿足不同收入群體的「付費意願」。因此,電視廣播服務的市場佔有率正在向廣告主導模式轉變,但由於程序化系統實現了廣告位銷售的自動化,利潤率正在提高。

區域分析

亞太地區預計在2025年貢獻32.87%的收入,這主要得益於印度OTT服務的爆炸式成長以及中國政府資助的5G廣播基礎設施建設。 Zee5實現5.64億印度盧比(約680萬美元)的正EBITDA,凸顯了區域語言平台單位經濟效益的可行性。在韓國,TVING與Waveve的合併使其廣告收入成長了74.7%,而富士電視台收購F1獨家轉播權則是一項旨在增強觀眾對高階體育賽事忠誠度的豪賭。

北美和歐洲的傳統電視平台正經歷可控的衰退,而串流媒體服務的成長正在抵消這種影響。預計到2026年第一季,Peacock的付費用戶將成長12%,達到4,600萬,而Comcast的傳統電視用戶預計將下降10%。美國聯邦通訊委員會(FCC)提案逐步淘汰ATSC 1.0標準,這正在加速向以IP為中心的傳輸模式轉變。同時,歐洲對廣播配額和所有者數量上限的限制,也增加了該地區產業結構重組的複雜性。

預計中東地區將以7.98%的複合年成長率實現最高成長,這得益於政府對當地工作室的資助以及光纖到戶(FTTH)的建設,從而支持4K HDR線性頻道的播放。在南美洲,巴西的「Globoplay」扮演核心角色,下載量超過1億次,並透過利用其在葡語地區的足球轉播權,抵禦來自全球新參與企業的衝擊。由於高昂的價格導致寬頻普及率有限,非洲仍處於發展階段,但預計行動優先的經營模式將使其在預測期後半段迎頭趕上。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 「停掉有線電視服務」正在推動OTT和串流電視的普及。

- 廣告主對體育賽事直播廣告版位的需求日益成長

- 新興市場的寬頻和智慧電視普及率

- 引入ATSC 3.0以實現互動式廣播

- OEM支援的快速通路生態系統正在蓬勃發展。

- 基於雲端的播出降低了小眾網路的准入門檻。

- 市場限制因素

- SVOD平台競相爭取傳統電視觀眾

- 在地採購率和外資所有權上限限制

- 取得優質版權的成本正在飆升。

- 5G頻率的重新分配將降低地面電波的傳輸容量。

- 宏觀經濟因素對市場的影響

- 產業價值/價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 透過分銷平台

- 地面電波電視

- 衛星電視

- 有線電視

- IPTV

- OTT/網路電視

- 按服務類型

- 訂閱制

- 廣告支援類型

- 按次付費/交易型

- 廣播公司類型

- 公共廣播

- 私人廣播

- 區域和教育廣播

- 按內容類型

- 娛樂與戲劇

- 運動的

- 新聞和時事

- 兒童與家庭

- 其他內容類型

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他亞太國家

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲地區

- 中東

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- British Broadcasting Corporation(BBC)

- Comcast Corporation

- Paramount Global

- The Walt Disney Company

- Warner Bros. Discovery, Inc.

- RTL Group SA

- Nippon Television Holdings, Inc.

- Fuji Media Holdings, Inc.

- Sky Group Limited

- Mediaset SpA

- Eutelsat Communications SA

- Sinclair Broadcast Group, Inc.

- Nexstar Media Group, Inc.

- Seven West Media Limited

- ITV plc

- ProSiebenSat.1 Media SE

- Grupo Globo Comunicacao e Participacoes SA

- China Central Television(CCTV)

- Zee Entertainment Enterprises Limited

- CJ ENM Co., Ltd.

- Television Broadcasts Limited(TVB)

- Roku, Inc.

- Amazon.com, Inc.(Freevee)

- Pluto TV LLC

- DAZN Group Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the television broadcasting service market size was valued at USD 548.35 billion in 2025 and estimated to grow from USD 582.07 billion in 2026 to reach USD 784.47 billion by 2031, at a CAGR of 6.15% during the forecast period (2026-2031).

This report is Segmented by Delivery Platform (Terrestrial Broadcast TV, Cable TV, IPTV, OTT/Internet TV, and More), Service Type (Subscription-Based, Advertising-Supported, and More), Broadcaster Type (Public Service, Commercial, and More), Content Genre (Entertainment and Drama, Sports, News and Current Affairs, and More), and Geography. Market Forecasts are Provided in Terms of Value (USD).

Global Television Broadcasting Service Market Trends and Insights

Cord-Cutting Pushes Adoption of OTT and Streaming TV

Streaming's share of total television usage reached 47% in January 2026, a 5.4-point jump in 12 months. Households keep high-speed broadband but cancel multichannel bundles, funneling spending toward a-la-carte apps that bundle on-demand libraries with live linear channels. Comcast lost 10% of domestic linear pay-TV subscribers year-over-year in Q4 2025, yet Peacock added 12% more paid subscribers over the same period. Free ad-supported services accelerate churn from cable because zero subscription cost slashes switching friction; Tubi and The Roku Channel each posted mid-single-digit viewing-share gains by January 2026. Broadcasters therefore prioritize seamless app experiences and robust libraries over carriage negotiations, shifting capital toward direct-to-consumer technology.

Growing Advertiser Demand for Live-Sports Inventory

Sports rights appreciated 113% in value between 2014 and 2024, dwarfing overall advertising growth because brands prize real-time reach and high engagement. Netflix's World Baseball Classic stream in Japan drew 31.4 million viewers, illustrating that even subscription-first platforms will pay premiums for exclusive live events. On FAST services, sports channels enjoyed 105% advertising-revenue growth and 71% higher ad recall than short-form video. Deep-pocketed streamers and national broadcasters thus lock up marquee properties, forcing regional networks to pivot toward niche sports or shoulder programming.

SVOD Platforms Cannibalizing Linear Viewership

Warner Bros Discovery's linear-networks revenue fell 12% year-over-year in Q4 2025 even as streaming subscribers rose to 131.6 million. Linear advertising inventory shrinks alongside audience migration, and per-viewer revenue on SVOD is lower than on scheduled broadcasts. Comcast lost 10% of domestic pay-TV households in Q4 2025, reinforcing a decade-long cord-cutting trend. Broadcasters must therefore fund duplicative infrastructure to run direct-to-consumer apps while still maintaining legacy networks, compressing margins during transition.

Other drivers and restraints analyzed in the detailed report include:

- Broadband and Smart-TV Penetration in Emerging Markets

- Roll-Out of ATSC 3.0 Enabling Interactive Broadcasts

- Escalating Premium-Rights Acquisition Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

OTT and internet TV captured 36.45% of 2025 revenue in the television broadcasting service market and will rise at a 6.57% CAGR to 2031. The surge reflects smart-TV operating systems that foreground streaming apps and mobile networks that zero-rate video traffic. Cable and satellite still anchor rural and maritime distribution, yet subscriber erosion continues as low-earth-orbit broadband promises viable alternatives within three years. Terrestrial broadcast TV benefits from ATSC 3.0 interactivity, but spectrum refarming limits expansion. IPTV's share remains confined to carrier bundles in fiber-rich geographies.

Broadcasters now deploy converged technology stacks so that one asset manifests as a linear channel, an on-demand episode, and a FAST feed with dynamic ad insertion. Paramount unified its Paramount+ and Pluto TV workflows in Q4 2025, cutting per-stream cost by 15%. This model safeguards scale economics while surfing audience preference shifts, ensuring that the television broadcasting service market size for OTT platforms grows without wholly cannibalizing legacy formats.

Advertising-supported offerings controlled 55.78% of 2025 revenue and are projected to expand at a 6.88% CAGR, exceeding subscription growth as households manage budget fatigue. Netflix's ad tier achieved 190 million monthly active users in Q1 2026, materially boosting quarterly revenue of USD 12.25 billion. Roku's USD 1.22 billion Q4 2025 platform revenue validates FAST economics, where higher completion rates and granular targeting lift CPMs.

Subscription services still underpin blockbuster originals but face churn spikes when catalogs stagnate. Hybrid models now dominate: a free, ad-supported on-ramp funnels users toward premium tiers, capturing willingness-to-pay across the income curve. The television broadcasting service market share mix therefore tilts back toward advertising, yet margins improve because programmatic systems automate inventory sales.

Complete Report Scope:

- By Delivery Platform

- Terrestrial Broadcast TV

- Satellite Broadcast TV

- Cable TV

- IPTV

- OTT / Internet TV

- By Service Type

- Subscription-Based Services

- Advertising-Supported Services

- Pay-Per-View / Transactional

- By Broadcaster Type

- Public Service Broadcasters

- Commercial Broadcasters

- Community / Educational Broadcasters

- By Content Genre

- Entertainment and Drama

- Sports

- News and Current Affairs

- Kids and Family

- Other Content Genre

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

Asia-Pacific generated 32.87% of 2025 revenue, buoyed by India's OTT leapfrog and China's state-funded 5G broadcast infrastructure. Zee5's EBITDA-positive milestone at INR 564 million (USD 6.8 million) confirms unit-economics viability for regional-language platforms. South Korea's TVING integration with Wavve boosted advertising 74.7%, and Fuji Television's exclusive Formula 1 rights bet on premium sports loyalty.

Linear platforms in North America and Europe are witnessing a managed decline, which is being offset by the growth of streaming services. By Q1 2026, Peacock achieved a 12% increase in paid subscribers, reaching 46 million, while Comcast's linear base saw a 10% contraction. The FCC's proposed ATSC 1.0 sunset is expediting the transition to IP-centric distribution models. Meanwhile, European quotas and ownership caps are adding complexity to consolidation efforts in the region.

The Middle East is forecast to post the highest 7.98% CAGR, underwritten by sovereign wealth-fund backing of local studios and fiber-to-the-home builds that enable 4K HDR linear channels. South America pivots around Brazil's Globoplay, exceeding 100 million downloads, leveraging Portuguese-language football rights to fend off global entrants. Africa remains nascent because broadband affordability limits mass adoption, but mobile-first models promise catch-up growth in the outer forecast years.

- British Broadcasting Corporation (BBC)

- Comcast Corporation

- Paramount Global

- The Walt Disney Company

- Warner Bros. Discovery, Inc.

- RTL Group S.A.

- Nippon Television Holdings, Inc.

- Fuji Media Holdings, Inc.

- Sky Group Limited

- Mediaset S.p.A.

- Eutelsat Communications S.A.

- Sinclair Broadcast Group, Inc.

- Nexstar Media Group, Inc.

- Seven West Media Limited

- ITV plc

- ProSiebenSat.1 Media SE

- Grupo Globo Comunicacao e Participacoes S.A.

- China Central Television (CCTV)

- Zee Entertainment Enterprises Limited

- CJ ENM Co., Ltd.

- Television Broadcasts Limited (TVB)

- Roku, Inc.

- Amazon.com, Inc. (Freevee)

- Pluto TV LLC

- DAZN Group Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cord-Cutting Pushes Adoption of OTT and Streaming TV

- 4.2.2 Growing Advertiser Demand for Live-Sports Inventory

- 4.2.3 Broadband and Smart-TV Penetration in Emerging Markets

- 4.2.4 Roll-Out of ATSC 3.0 Enabling Interactive Broadcasts

- 4.2.5 OEM-Backed FAST Channel Ecosystems Gain Traction

- 4.2.6 Cloud-Based Playout Lowers Entry Barriers for Niche Nets

- 4.3 Market Restraints

- 4.3.1 SVOD Platforms Cannibalizing Linear Viewership

- 4.3.2 Local Content and Foreign-Ownership Regulation Caps

- 4.3.3 Escalating Premium-Rights Acquisition Costs

- 4.3.4 Spectrum Refarming for 5G Reduces Terrestrial Capacity

- 4.3.5 Impact of Macroeconomic Factors on the Market

- 4.3.6 Industry Value / Supply-Chain Analysis

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.7 Threat of New Entrants

- 4.8 Bargaining Power of Suppliers

- 4.9 Bargaining Power of Buyers

- 4.10 Threat of Substitutes

- 4.11 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Delivery Platform

- 5.1.1 Terrestrial Broadcast TV

- 5.1.2 Satellite Broadcast TV

- 5.1.3 Cable TV

- 5.1.4 IPTV

- 5.1.5 OTT / Internet TV

- 5.2 By Service Type

- 5.2.1 Subscription-Based Services

- 5.2.2 Advertising-Supported Services

- 5.2.3 Pay-Per-View / Transactional

- 5.3 By Broadcaster Type

- 5.3.1 Public Service Broadcasters

- 5.3.2 Commercial Broadcasters

- 5.3.3 Community / Educational Broadcasters

- 5.4 By Content Genre

- 5.4.1 Entertainment and Drama

- 5.4.2 Sports

- 5.4.3 News and Current Affairs

- 5.4.4 Kids and Family

- 5.4.5 Other Content Genre

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 Saudi Arabia

- 5.5.4.1.2 United Arab Emirates

- 5.5.4.1.3 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Egypt

- 5.5.4.2.3 Rest of Africa

- 5.5.4.1 Middle East

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 British Broadcasting Corporation (BBC)

- 6.4.2 Comcast Corporation

- 6.4.3 Paramount Global

- 6.4.4 The Walt Disney Company

- 6.4.5 Warner Bros. Discovery, Inc.

- 6.4.6 RTL Group S.A.

- 6.4.7 Nippon Television Holdings, Inc.

- 6.4.8 Fuji Media Holdings, Inc.

- 6.4.9 Sky Group Limited

- 6.4.10 Mediaset S.p.A.

- 6.4.11 Eutelsat Communications S.A.

- 6.4.12 Sinclair Broadcast Group, Inc.

- 6.4.13 Nexstar Media Group, Inc.

- 6.4.14 Seven West Media Limited

- 6.4.15 ITV plc

- 6.4.16 ProSiebenSat.1 Media SE

- 6.4.17 Grupo Globo Comunicacao e Participacoes S.A.

- 6.4.18 China Central Television (CCTV)

- 6.4.19 Zee Entertainment Enterprises Limited

- 6.4.20 CJ ENM Co., Ltd.

- 6.4.21 Television Broadcasts Limited (TVB)

- 6.4.22 Roku, Inc.

- 6.4.23 Amazon.com, Inc. (Freevee)

- 6.4.24 Pluto TV LLC

- 6.4.25 DAZN Group Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

4K衛星廣播市場規模、佔有率和成長分析:按廣播平台、組件、內容類型、服務供應商、最終用戶和地區分類-2026-2033年產業預測

4K衛星廣播市場規模、佔有率和成長分析:按廣播平台、組件、內容類型、服務供應商、最終用戶和地區分類-2026-2033年產業預測 行動電視市場報告:按內容類型、技術、服務類型、應用程式和地區分類(2026-2034 年)

行動電視市場報告:按內容類型、技術、服務類型、應用程式和地區分類(2026-2034 年) 行動電視:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

行動電視:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 有線電視網路市場:依服務類型、內容類型、技術、傳輸方式、訊號品質、最終用戶和發行管道分類-2026-2032年全球市場預測

有線電視網路市場:依服務類型、內容類型、技術、傳輸方式、訊號品質、最終用戶和發行管道分類-2026-2032年全球市場預測 2026年全球數位地面電視市場報告2026年全球數位有線電視機上盒市場報告免費電視服務市場:按內容類型、傳輸技術、終端類型、收入模式、頻段和應用分類-2026-2032年全球市場預測行動電視市場:2026-2032年全球市場預測(依裝置類型、平台、網路類型、內容類型、訂閱模式和最終用戶分類)

2026年全球數位地面電視市場報告2026年全球數位有線電視機上盒市場報告免費電視服務市場:按內容類型、傳輸技術、終端類型、收入模式、頻段和應用分類-2026-2032年全球市場預測行動電視市場:2026-2032年全球市場預測(依裝置類型、平台、網路類型、內容類型、訂閱模式和最終用戶分類) 4K衛星廣播市場到2035年的分析和預測:按類型、產品、服務、技術、組件、應用、設備、部署、最終用戶和解決方案數位地面電視市場:按組件、服務類型、解析度、技術和最終用戶分類 - 2026-2032年全球市場預測

4K衛星廣播市場到2035年的分析和預測:按類型、產品、服務、技術、組件、應用、設備、部署、最終用戶和解決方案數位地面電視市場:按組件、服務類型、解析度、技術和最終用戶分類 - 2026-2032年全球市場預測