|

市場調查報告書

商品編碼

2062452

行動電視:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Mobile TV - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

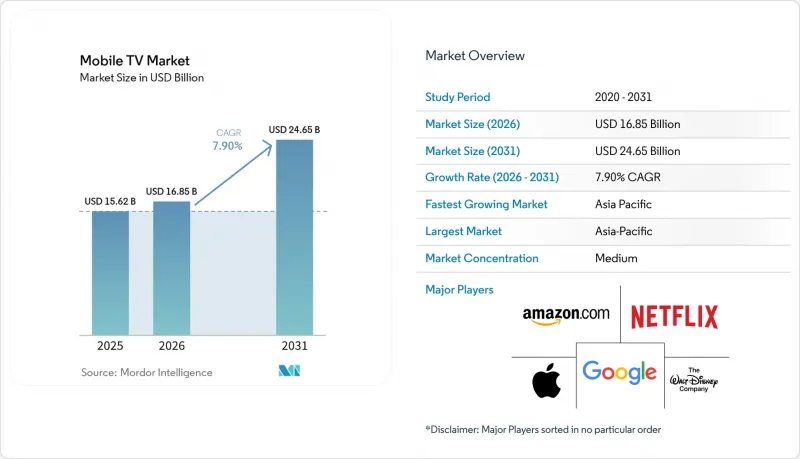

根據 Mordor Intelligence 預測,行動電視市場規模將從 2025 年的 156.2 億美元成長到 2026 年的 168.5 億美元,到 2031 年將達到 246.5 億美元,2026 年至 2031 年的複合年成長率為 7.9%。

本報告按分發平台(OTT單播串流等)、裝置類型(平板電腦等)、收入模式(SVOD等)、內容類型(娛樂、電影等)、網路技術(4G LTE等)、作業系統(iOS等)、觀看習慣(點播播放等)和地區(北美等)進行細分。市場預測以美元計價。

全球行動電視市場趨勢與洞察

5G中頻段網路的擴展

5G在全國範圍內的部署實現了超過500Mbps的持續吞吐量,支援同時進行4K串流媒體播放和互動式疊加。在韓國,預計到2025年,5G用戶數將達到1,749萬,平均下載速度為1064Mbps。這將使200萬人能夠同時在Coupang Play上觀看K聯賽比賽。同年,美國通訊業者完成了C頻段的部署,早期的5G廣播試驗已向數千人提供了FIFA世界盃的比賽影像,而無需支付額外的單次傳輸費用。傳輸成本的降低使營運商能夠將節省的資金重新投資於獨家分發權和零費率套餐,從而進一步促進用戶成長。

混合型AVOD+SVOD獲利模式的興起

目前,各平台都將廣告支援套餐定位在高級套餐之下,以最大限度地擴大用戶涵蓋範圍,同時留住高ARPU(每位用戶平均收入)用戶。 Netflix和Disney+在2025年新增用戶中,大部分都轉向了價格更低的廣告支援套餐,與僅提供SVOD(訂閱隨選視訊)服務的用戶相比,其用戶解約率更低。派拉蒙旗下的Pluto TV擁有超過250個快速頻道,透過將單次播放成本控制在0.1美元以下,實現了盈利。混合模式既能解決已開發地區市場飽和的問題,也能為新興市場提供平價的服務,因為新興市場的用戶付費意願仍有限。

內容授權費飆升

Via LA將2025年H.264專利聯盟的年度支付上限提高至450萬美元,較2022年成長29%。同時,好萊塢製片廠正在延長院線獨家放映期,並推遲行動端SVOD服務的推出。不斷上漲的版權費正在擠壓利潤空間,因為當內容選擇減少時,行動用戶會迅速取消訂閱。儘管多個平台都在轉向原創內容,但CJ ENM儘管投入巨資,卻在2025年第四季累計營運虧損,凸顯了其中存在的風險。

細分市場分析

預計到2025年,單播OTT將佔總營收的72.1%,而5G廣播預計將以9.4%的複合年成長率成長。通訊業者更傾向於eMBMS,因為它允許他們透過單一傳輸覆蓋無限數量的用戶,並降低尖峰時段成本。美國在中頻段分配的60MHz頻譜正在推動商業測試。通訊業者收費的「電視無所不在」服務維持對直播新聞和體育賽事套餐的特定需求,而衛星混合服務則覆蓋了光纖尚未普及的農村地區。

在2025年世界盃的測試中,eMBMS展現出了與單播相當的表現(1080p60解析度下延遲低於200毫秒)。歐洲廣播聯盟(EBU)內部推動跨國標準化的監管措施可能會加速其普及。傳統廣播公司,例如環球電視台(Globo)旗下的“GloboPop”,直接轉向應用程式,凸顯了從批發分發模式向消費者主導的所有權模式的轉變。

預計到2025年,智慧型手機將佔行動電視市場收入的82.8%,繼續保持其在行動電視市場的領先地位。穿戴式設備,包括VR和AR眼鏡,預計將以9.1%的複合年成長率成長,例如Meta公司售價799美元的Ray-Ban Display和蘋果公司即將上市的售價低於1000美元的N50等產品,將提升移動性。平板電腦則迎合了合作社和教育等細分市場的需求,而具備影片播放功能的功能手機則填補了價格空白。智慧型手機和穿戴式裝置的廣泛普及得益於技術進步、價格下降以及人們對行動娛樂解決方案日益成長的需求。

穿戴式裝置對長寬比和空間音訊提出了新的要求,迫使內容創作者重新思考他們的製作方式。 Netflix 於 2026 年 4 月推出了垂直視訊串流,以迎合用戶對垂直螢幕觀看的偏好。同時,蘋果的 Vision Pro 雖然普及率有限,但卻激發了早期開發者對 3D 敘事的興趣。向穿戴式裝置和身臨其境型技術的轉變預計將重新定義內容創作策略,各公司正在投資創新格式以滿足不斷變化的消費者偏好。

預計到2025年,SVOD(訂閱視訊點播)將佔總收入的49.3%,而混合型免費增值模式和FAST(免費廣告支援型串流電視)正以9.7%的複合年成長率成長。訂閱視訊點播(SVOD)憑藉其提供加值內容和獨家發行管道的優勢,繼續主導市場。然而,混合型免費增值模式和FAST平台的成長正在重塑競爭格局。 Pluto TV體現了FAST平台的低成本優勢,儘管其平均用戶收入(ARPU)較低,但仍保持盈利。 Netflix和Disney+等主要平台已推出廣告支援型套餐,事實證明,這些套餐能夠有效降低用戶解約率並擴大用戶群。按次付費觀看(PPV)對於UFC格鬥等高規格賽事仍然十分重要,每場比賽的售價在70至80美元之間,但其市場佔有率正在逐漸下降。

儘管現行法規允許混合模式,但隱私規則限制了行為定向廣告,迫使平台轉向情境廣告。尤其是在已開發市場,隱私法規限制了行為導向廣告的使用,迫使平台轉而採用情境廣告投放。在新興市場,平台透過將免費套餐與可購買的電商連結結合,從過去依賴非法內容下載的用戶身上獲取收入。在這些地區,平台正在利用創新的商業化戰略,例如將電商連結整合到免費套餐內容中,從過去依賴非法內容的用戶身上獲取收益。

區域分析

預計到2025年,亞太地區將佔全球營收的35.8%,成為領先地區,並將在2031年之前維持8.8%的最高複合年成長率。中國擁有12億月活躍行動影片用戶,騰訊視訊、愛奇藝和抖音三大平台加起來,是全球最大的單一市場。在印度,包含板球賽事轉播權的預付套餐正在推動用戶成長,而韓國AVOD(廣告支援的視訊點播)的快速成長表明混合模式已日趨成熟。日本非常重視動畫,因此全球串流媒體業者需要獲得當地的IP授權。

儘管北美和歐洲的成長速度放緩,但它們仍然佔這些地區總銷售額的約55%。派拉蒙影業和華納兄弟探索頻道宣布將於2026年完成價值1,110億美元的合併,顯示產業整合面臨壓力。隨著歐盟強制執行網路中立原則,零費率模式已被逐步取消,迫使平台將投資重點放在提升用戶體驗品質(QoE)上,而不是依靠免費數據來求得差異化。

在南美洲、中東和非洲,儘管基礎建設和收入不平等問題依然存在,但年複合成長率仍達7-8%。環球電視台(Globo)於2026年4月在巴西推出「GloboPop」服務,顯示區域廣播公司正將重心轉向精選垂直影片。海灣國家正在投資衛星回程傳輸,以確保國際賽事的轉播;而在奈及利亞、肯亞和坦尚尼亞,售價40美元的補貼智慧型手機正在推動人們首次體驗串流服務。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 5G中等頻寬網路的擴展

- 透過混合型AVOD+SVOD實現獲利的興起

- 新興市場中的經濟型智慧型手機

- 將通訊業者和衛星通訊整合到實況活動中

- 邊緣原生AI預測預快取

- 引入具有購物功能的影片將提升每位用戶平均收入 (ARPU)。

- 市場限制因素

- 內容授權費飆升

- eMBMS廣播中頻寬不足

- 監管機構對零利率數據的強烈反對

- 6 GHz 頻段串流傳輸中的電池和熱限制

- 產業價值鏈分析

- 宏觀經濟因素對市場的影響

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 透過分銷平台

- OTT/單播串流媒體

- Everywhere-收費通訊業者電視服務。

- 5G廣播(eMBMS)

- 衛星/地面電波混合

- 依設備類型

- 智慧型手機

- 藥片

- 功能手機

- 連網型穿戴式裝置(VR/AR眼鏡)

- 按收入模式

- 訂閱式視訊點播 (SVOD)

- 廣告支援的視訊點播(AVOD)

- 交易型(TVOD/PPV)

- 混合模式(免費增值和快速模式)

- 按內容類型

- 娛樂和電影

- 體育直播

- 新聞資訊

- 教育/兒童

- 網路科技

- 4G/LTE

- 5G NR

- Wi-Fi 6/6E

- 傳統 3G/2G

- 透過作業系統

- Android

- IOS

- HarmonyOS 和其他作業系統

- 透過查看狀態

- 點播播放

- 即時線性串流媒體

- 下載到您的手機

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他亞太國家

- 南美洲

- 中東和非洲

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Netflix, Inc.

- Amazon.com, Inc.

- Google LLC

- The Walt Disney Company

- Apple Inc.

- Tencent Holdings Ltd.

- Baidu, Inc.

- Alibaba Group Holding Ltd.

- Hulu, LLC

- Warner Bros. Discovery, Inc.

- Paramount Global

- Rakuten Group, Inc.

- Reliance Industries Limited

- Kuaishou Technology

- SEA Ltd.

- PCCW Ltd.

- Globo Comunicacao e Participacoes SA

- CJ ENM Co., Ltd.

- Eros International Plc

- TelevisaUnivision Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the mobile TV market size is expected to increase from USD 15.62 billion in 2025 to USD 16.85 billion in 2026 and reach USD 24.65 billion by 2031, growing at a CAGR of 7.9% over 2026-2031.

This report is Segmented by Delivery Platform (OTT Unicast Streaming, and More), Device Type (Tablets, and More), Revenue Model (SVOD, and More), Content Type (Entertainment and Movies, and More), Network Technology (4G LTE, and More), Operating System (iOS, and More), Viewing Context (On-Demand Playback, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Mobile TV Market Trends and Insights

Expansion of 5G Mid-Band Networks

Nationwide 5G rollouts are enabling sustained throughput above 500 Mbps, which supports simultaneous 4K streams and interactive overlays. South Korea reported 17.49 million 5G subscribers in 2025 with average download speeds of 1,064 Mbps, allowing 2 million concurrent viewers of K-League matches on Coupang Play. U.S. carriers completed C-band deployments the same year, and early 5G Broadcast trials delivered FIFA World Cup feeds to thousands without per-stream cost penalties. Lower delivery costs let operators reinvest savings in exclusive rights or zero-rated bundles, spurring subscriber growth.

Rise Of Hybrid AVOD + SVOD Monetization

Platforms now layer ad-supported plans beneath premium tiers to maximize reach while preserving high-ARPU subscribers. Netflix and Disney+ shifted large portions of 2025 sign-ups to lower-priced ad tiers, noting lower churn compared with SVOD-only cohorts. Paramount's Pluto TV achieved profitability with over 250 FAST channels by keeping per-stream costs below USD 0.10. Hybrid models combat saturation in developed regions and improve affordability in emerging markets where willingness to pay remains limited.

Escalating Content-Licensing Inflation

Via LA raised annual H.264 patent-pool caps to USD 4.5 million in 2025, up 29% since 2022. Hollywood studios simultaneously lengthened exclusive theatrical windows, delaying availability on mobile SVOD services. Rising rights costs squeeze margins because mobile users churn quickly when catalogs shrink. Several platforms have pivoted toward originals, yet CJ ENM's heavy investment still produced an operating loss in Q4 2025, underscoring execution risk.

Other drivers and restraints analyzed in the detailed report include:

- Smartphone Affordability In Emerging Markets

- Telco-Satellite Aggregation For Live Events

- Regulatory Backlash On Data Zero-Rating

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Unicast OTT accounted for 72.1% of revenue in 2025, yet 5G Broadcast is projected to expand at a 9.4% CAGR. Operators favor eMBMS because one transmission serves unlimited viewers, cutting peak costs. U.S. spectrum allocations of 60 MHz in mid-band spectrum support commercial trials. Carrier-billed TV-everywhere retains niche relevance for live news and sports bundles, while satellite-hybrid paths cover rural zones where fiber is scarce.

eMBMS performance parity with unicast, sub-200 ms latency for 1080p60, was proven during the 2025 World Cup trials. Regulatory momentum in the European Broadcasting Union for cross-border standards may accelerate adoption. Traditional broadcasters transitioning to direct apps, such as Globo-owned GloboPop, highlight a shift from wholesale carriage to consumer ownership.

Smartphones captured 82.8% of 2025 revenue and remain the core viewing device of the mobile TV market. Wearables, including VR and AR glasses, are forecast to rise 9.1% CAGR as products like Meta's USD 799 Ray-Ban Display and Apple's forthcoming N50 under USD 1,000 improve mobility. Tablets serve communal and educational niches, while video-capable feature phones bridge affordability gaps. The increasing adoption of smartphones and wearables is driven by advancements in technology, affordability, and the growing demand for on-the-go entertainment solutions.

Wearables require new video ratios and spatial audio, prompting content teams to rethink production. Netflix introduced a vertical-clip feed in April 2026, meeting portrait-first habits, while Apple's Vision Pro triggered early developer interest in 3D storytelling despite limited adoption. The shift towards wearables and immersive technologies is expected to redefine content creation strategies, with companies investing in innovative formats to cater to evolving consumer preferences.

SVOD represented 49.3% of 2025 revenue, but hybrid freemium and FAST are advancing at a 9.7% CAGR. The Subscription Video on Demand (SVOD) segment continues to dominate the market, driven by its ability to offer premium content and exclusive releases. However, the growth of hybrid freemium models and Free Ad-Supported Streaming Television (FAST) platforms is reshaping the competitive landscape. Pluto TV exemplifies the lean-cost economics of FAST platforms, which sustain profitability even at low Average Revenue Per User (ARPU). Major players like Netflix and Disney+ have introduced ad-supported tiers, which have proven effective in reducing subscriber churn and expanding their audience reach. Pay-per-view remains relevant for high-profile events, such as UFC fights priced at USD 70-80 per event, although its market share is gradually declining.

Regulations currently allow hybrid models, yet privacy rules cap behaviorally targeted ads, nudging platforms toward contextual placement. Privacy regulations, particularly in developed markets, limit the use of behaviorally targeted advertisements, compelling platforms to adopt contextual ad placements instead. For emerging markets, free tiers paired with shoppable commerce links monetize audiences that previously pirated content. In these regions, platforms are leveraging innovative monetization strategies, such as integrating e-commerce links into free-tier content, to capture revenue from audiences that historically relied on pirated material.

Geography Analysis

Asia-Pacific led with 35.8% of 2025 revenue and will keep the highest 8.8% CAGR to 2031. China's 1.2 billion monthly mobile video users across Tencent Video, iQIYI, and Douyin form the largest single-country opportunity. India's prepaid bundles that feature cricket rights maintain subscriber momentum, and South Korea's rapid AVOD growth points to the maturation of hybrid models. Japan emphasizes anime, forcing global streamers to license local IP.

North America and Europe grow more slowly but still account for roughly 55% of revenue combined. A USD 111 billion merger between Paramount and Warner Bros. Discovery, announced in 2026, illustrates consolidation pressure. EU net-neutrality enforcement eliminates zero-rating, requiring platforms to invest in quality of experience rather than free data to stand out.

South America, the Middle East, and Africa present 7-8% CAGR prospects, though infrastructure and income gaps remain. Globo's April 2026 launch of GloboPop in Brazil displays regional broadcasters' pivot to curated vertical video. Gulf states invest in satellite backhaul to guarantee coverage of global tournaments, while subsidized USD 40 smartphones in Nigeria, Kenya, and Tanzania catalyze first-time streaming.

- Netflix, Inc.

- Amazon.com, Inc.

- Google LLC

- The Walt Disney Company

- Apple Inc.

- Tencent Holdings Ltd.

- Baidu, Inc.

- Alibaba Group Holding Ltd.

- Hulu, LLC

- Warner Bros. Discovery, Inc.

- Paramount Global

- Rakuten Group, Inc.

- Reliance Industries Limited

- Kuaishou Technology

- SEA Ltd.

- PCCW Ltd.

- Globo Comunicacao e Participacoes S.A.

- CJ ENM Co., Ltd.

- Eros International Plc

- TelevisaUnivision Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of 5G Mid-Band Networks

- 4.2.2 Rise of Hybrid AVOD + SVOD Monetisation

- 4.2.3 Smartphone Affordability in Emerging Markets

- 4.2.4 Telco-Satellite Aggregation for Live Events

- 4.2.5 Edge-Native AI Predictive Pre-Caching

- 4.2.6 Shoppable Video Integration Boosting ARPU

- 4.3 Market Restraints

- 4.3.1 Escalating Content-Licensing Inflation

- 4.3.2 Spectrum Scarcity for eMBMS Broadcast

- 4.3.3 Regulatory Backlash on Data Zero-Rating

- 4.3.4 Battery-Thermal Limits on 6 GHz Streaming

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Delivery Platform

- 5.1.1 OTT/Unicast Streaming

- 5.1.2 Carrier-Billed TV-Everywhere

- 5.1.3 5G Broadcast (eMBMS)

- 5.1.4 Satellite-Terrestrial Hybrid

- 5.2 By Device Type

- 5.2.1 Smartphones

- 5.2.2 Tablets

- 5.2.3 Feature Phones

- 5.2.4 Connected Wearables (VR/AR Glasses)

- 5.3 By Revenue Model

- 5.3.1 Subscription Video-on-Demand (SVOD)

- 5.3.2 Advertising Video-on-Demand (AVOD)

- 5.3.3 Transactional (TVOD/PPV)

- 5.3.4 Hybrid (Freemium and FAST)

- 5.4 By Content Type

- 5.4.1 Entertainment and Movies

- 5.4.2 Live Sports

- 5.4.3 News and Information

- 5.4.4 Education and Kids

- 5.5 By Network Technology

- 5.5.1 4G/LTE

- 5.5.2 5G NR

- 5.5.3 Wi-Fi 6/6E

- 5.5.4 Legacy 3G/2G

- 5.6 By Operating System

- 5.6.1 Android

- 5.6.2 iOS

- 5.6.3 HarmonyOS and Other Operating Systems

- 5.7 By Viewing Context

- 5.7.1 On-Demand Playback

- 5.7.2 Live Linear Streaming

- 5.7.3 Download-to-Go

- 5.8 By Geography

- 5.8.1 North America

- 5.8.1.1 United States

- 5.8.1.2 Canada

- 5.8.1.3 Mexico

- 5.8.2 Europe

- 5.8.2.1 Germany

- 5.8.2.2 United Kingdom

- 5.8.2.3 France

- 5.8.2.4 Russia

- 5.8.2.5 Rest of Europe

- 5.8.3 Asia-Pacific

- 5.8.3.1 China

- 5.8.3.2 Japan

- 5.8.3.3 India

- 5.8.3.4 South Korea

- 5.8.3.5 Australia

- 5.8.3.6 Rest of Asia-Pacific

- 5.8.4 South America

- 5.8.5 Middle East and Africa

- 5.8.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Netflix, Inc.

- 6.4.2 Amazon.com, Inc.

- 6.4.3 Google LLC

- 6.4.4 The Walt Disney Company

- 6.4.5 Apple Inc.

- 6.4.6 Tencent Holdings Ltd.

- 6.4.7 Baidu, Inc.

- 6.4.8 Alibaba Group Holding Ltd.

- 6.4.9 Hulu, LLC

- 6.4.10 Warner Bros. Discovery, Inc.

- 6.4.11 Paramount Global

- 6.4.12 Rakuten Group, Inc.

- 6.4.13 Reliance Industries Limited

- 6.4.14 Kuaishou Technology

- 6.4.15 SEA Ltd.

- 6.4.16 PCCW Ltd.

- 6.4.17 Globo Comunicacao e Participacoes S.A.

- 6.4.18 CJ ENM Co., Ltd.

- 6.4.19 Eros International Plc

- 6.4.20 TelevisaUnivision Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

電視廣播服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

電視廣播服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 4K衛星廣播市場規模、佔有率和成長分析:按廣播平台、組件、內容類型、服務供應商、最終用戶和地區分類-2026-2033年產業預測

4K衛星廣播市場規模、佔有率和成長分析:按廣播平台、組件、內容類型、服務供應商、最終用戶和地區分類-2026-2033年產業預測 行動電視市場報告:按內容類型、技術、服務類型、應用程式和地區分類(2026-2034 年)

行動電視市場報告:按內容類型、技術、服務類型、應用程式和地區分類(2026-2034 年) 有線電視網路市場:依服務類型、內容類型、技術、傳輸方式、訊號品質、最終用戶和發行管道分類-2026-2032年全球市場預測

有線電視網路市場:依服務類型、內容類型、技術、傳輸方式、訊號品質、最終用戶和發行管道分類-2026-2032年全球市場預測 2026年全球數位地面電視市場報告2026年全球數位有線電視機上盒市場報告免費電視服務市場:按內容類型、傳輸技術、終端類型、收入模式、頻段和應用分類-2026-2032年全球市場預測行動電視市場:2026-2032年全球市場預測(依裝置類型、平台、網路類型、內容類型、訂閱模式和最終用戶分類)

2026年全球數位地面電視市場報告2026年全球數位有線電視機上盒市場報告免費電視服務市場:按內容類型、傳輸技術、終端類型、收入模式、頻段和應用分類-2026-2032年全球市場預測行動電視市場:2026-2032年全球市場預測(依裝置類型、平台、網路類型、內容類型、訂閱模式和最終用戶分類) 4K衛星廣播市場到2035年的分析和預測:按類型、產品、服務、技術、組件、應用、設備、部署、最終用戶和解決方案數位地面電視市場:按組件、服務類型、解析度、技術和最終用戶分類 - 2026-2032年全球市場預測

4K衛星廣播市場到2035年的分析和預測:按類型、產品、服務、技術、組件、應用、設備、部署、最終用戶和解決方案數位地面電視市場:按組件、服務類型、解析度、技術和最終用戶分類 - 2026-2032年全球市場預測