|

市場調查報告書

商品編碼

2072534

印度照明市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)India Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

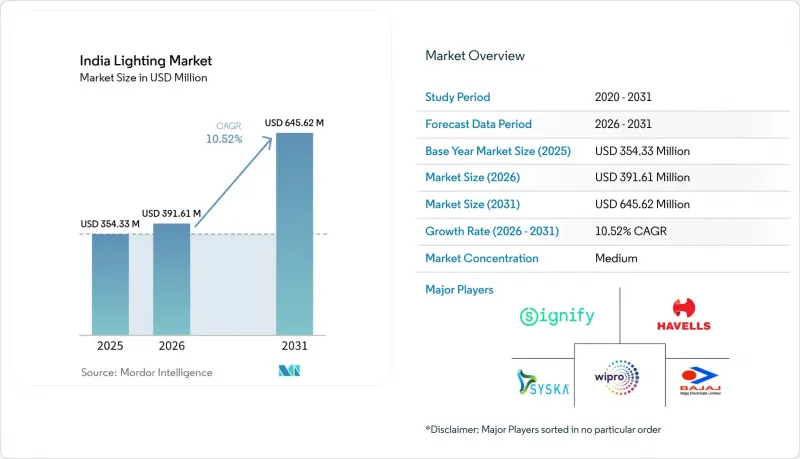

根據 Mordor Intelligence 預測,印度照明市場規模將從 2025 年的 3.5433 億美元成長到 2026 年的 3.9161 億美元,到 2031 年將達到 6.4562 億美元,2026 年至 2031 年的複合年成長率為 10.52%。

本報告按產品類型(照明燈具、燈泡)、光源(LED、傳統光源)、分銷管道(直銷、開發人員、承包商、批發商、電工、照明專家、其他)和應用領域(商業、工業、戶外、住宅)進行分類。市場預測以美元計價。

印度照明市場趨勢與洞察

LED價格下降和能源效率法規

除了新建商業建築必須遵守能源效率標準 (ECBC) 外,印度能源效率局 (BEE) 的星級認證要求也迫使開發商採用高效節能的照明設備,與標準規範相比,節能幅度可達 35% 至 50%。聯合國能源署 (UJALA) 的競標競標將 LED 燈泡的零售價格較 2014 年水準降低了 90%,最終售出 3.687 億個燈泡,使 LED 成為公共部門專案之外的通用標準選擇。隨著電費上漲和企業淨零排放承諾的不斷推進,企業正將照明維修視為脫碳的第一步。因此,商業、工業和豪華住宅建築等各領域對高效能晶片、光學元件和驅動器的需求持續以兩位數的速度成長。儘管競爭激烈,但符合最新超級 ECBC 標準認證產品的供應商仍能維持利潤率。

城市基礎設施快速發展(智慧城市計畫)

在「智慧城市計畫」下,截至2024年7月,已批准價值247億美元的項目,並完成了5,909份工作訂單。每個綜合指揮中心都配備了可即時監控的連網路燈、區域照明和立面照明。市政當局正日益將照明系統整合到交通、安全和環境儀錶板中,將燈具轉變為更廣泛的城市數據平台的邊緣節點。能夠提供互通控制系統、自適應調光演算法和網路安全增強型韌體的韌體正在贏得多年期框架合約。隨著二線城市效仿浦那和瓦拉納西等一線城市的模式設計,中期內合約儲備將穩定成長。此外,專案的集中化縮短了專業安裝商的投資回報期,並為零零件供應商維持了較高的倉儲容量。

中小企業和一般家庭的初始維修成本較高

對於小規模工廠和本地零售商而言,將整個工廠的照明系統改造為LED照明的投資回收期通常長達3-5年。儘管節能潛力高達40-60%,但許多企業仍會推遲該專案。由於缺乏對生命週期經濟的認知,決策者往往只專注於購買價格,而忽略了總擁有成本(TCO)。雖然小額信貸和帳單電費方案已經存在,但由於繁瑣的手續和對技術風險的擔憂,這些方案在大都會圈區以外的利用率仍然很低。這種資本投資障礙正在減緩連網照明設備和感測器的普及,而這些設備的每流明成本高於普通的維修燈泡。

細分市場分析

預計到2025年,照明燈具細分市場將佔印度照明市場銷售額的58.72%,並將在2031年之前以11.78%的複合年成長率成長。這表明該細分市場在印度照明市場的銷售和銷售成長中都發揮著主導作用。推動這一細分市場成長的因素包括「智慧城市計畫」的競標(該計畫指定使用配備感測器的整合式照明燈具)以及私人開發商將照明納入建築自動化合約以縮短試運行時間的趨勢。照明燈具通常是建築立面照明方案的核心,由於其整合了符合印度能源效率局規範的光學元件、驅動器和機載診斷,因此比通用燈具具有更高的利潤率。此外,面向城市軌道交通、機場航站大樓和資料中心項目的承包商傾向於選擇承包照明燈具,以最大限度地減少現場佈線錯誤並加快驗收測試,這進一步鞏固了該細分市場在印度照明市場的主導地位。

另一個利好因素是二、三線城市的可程式設計RGB建築照明專案。在這些地區,地方政府希望在不承擔大城市高昂成本的情況下促進旅遊業發展。符合印度標準局(BIS)安全標準的中型製造商,透過將能夠承受高濕度沿海氣候的DMX控制功能與鋁擠壓散熱器相結合,在該領域獲得了優勢。相較之下,由於價格下跌和政府大規模採購競標標準的修訂,燈具利潤率受到擠壓,導致燈具市場佔有率持續下降。儘管如此,住宅市場仍在繼續將節能燈(CFL)改裝為LED燈,這在一定程度上緩解了燈具銷量的下滑,但不足以扭轉市場向高價值照明燈具轉變的趨勢。

預計到2025年,印度LED照明解決方案將佔據印度照明市場81.35%的佔有率,到2031年將以12.05%的最高複合年成長率成長。印度照明市場規模的成長主要得益於LED在商業吸頂燈、路燈和工業高棚燈領域的應用,這反映出LED產品在價格敏感的農村地區安裝市場的進一步滲透。 「UJALA」和「全國街道照明計畫」的競標使LED的經濟性趨於正常化。同時,ECBC的「超級」評級推動了對光效超過150 lm/W的照明燈具的高階需求,這些燈具的價格仍然較高。傳統的螢光和HID技術目前主要在老舊的高溫工廠中使用,面臨驅動器額定功率下降的風險,但隨著堅固耐用的LED光源平台通過加速壽命測試,即使是這些小眾市場也在萎縮。

此外,一項名為Li-Fi的先導計畫也正在推動LED的普及。該專案將照明設備轉變為資料節點,使設施能夠在不造成射頻擁塞的情況下疊加寬頻容量。 Wipro Lighting與pureLiFi的合作,正是供應商在快速商品化的二極體市場中,透過將照明與連接相結合來維持獲利能力的典型案例。同時,一項針對白色家電的「生產連結獎勵計畫計畫」正在補貼板載晶片(COB)後端生產線,進一步實現LED物料清單(BOM)的本地化,並提高抵禦進口衝擊的成本抵禦能力。這對整個印度照明行業來說都是一個積極因素。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- LED價格下降和能源效率法規

- 城市基礎設施快速發展(智慧城市計畫)

- 政府採購(UJALA 和 SLNP)

- 二、三線城市外牆照明專案的成長

- 直流微電網和離網太陽能照明的需求日益成長

- 在企業園區引進Li-Fi試點項目

- 市場限制因素

- 對於中小企業和一般家庭來說,維修的初始成本相對較高。

- 分銷管道碎片化和仿冒品

- 進口相關的LED驅動IC價格波動。

- 政府EPC合約付款週期延長

- 產業供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素的影響

第5章 市場規模與成長預測

- 依產品類型

- 照明燈具/裝置

- 燈

- 透過光源

- LED

- 傳統的

- 透過分銷管道

- 直銷/開發人員/承包商

- 批發商/電工

- 燈具專賣店

- 其他

- 透過使用

- 商業

- 辦公室

- 零售和酒店

- 醫療機構

- 其他

- 產業

- 流程工業

- 各行業

- 倉庫和其他工業設施

- 戶外的

- 住宅

- 商業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Signify NV

- Havells India Limited

- Wipro Lighting(Wipro Ltd.)

- Bajaj Electricals Ltd.

- Syska LED Lights Pvt Ltd.

- Crompton Greaves Consumer Electricals Ltd.

- Surya Roshini Ltd.

- Halonix Technologies Pvt Ltd.

- MIC Electronics Ltd.

- Orient Electric Ltd.

- Panasonic Life Solutions India Pvt Ltd.

- Osram GmbH

- Zumtobel Group AG

- Acuity Brands Inc.

- Eaton Corporation plc(Cooper Lighting)

- Hubbell Inc.

- Fagerhult AB

- Dialight plc

- Nichia Corporation

- Eveready Industries India Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the india lighting market size is expected to grow from USD 354.33 million in 2025 to USD 391.61 million in 2026 and is forecast to reach USD 645.62 million by 2031 at 10.52% CAGR over 2026-2031.

This report is Segmented by Product Type (Luminaires / Fixtures, and Lamps), Light Source (LED, and Conventional), Distribution Channel (Direct Sales / Developers / Contract, Wholesalers / Electricians, Lighting Specialists, and Others), Application (Commercial, Industrial, Outdoor, and Residential). The Market Forecasts are Provided in Terms of Value (USD).

India Lighting Market Trends and Insights

LED price erosion and energy-efficiency mandates

Mandatory ECBC compliance for new commercial buildings plus BEE star-label requirements have pushed developers toward high-efficacy fixtures that deliver 35%-50% energy savings relative to baseline codes. UJALA's competitive tenders cut retail LED bulb prices by 90% from 2014 figures and distributed 36.87 crore units, making LEDs the universal default even beyond public-sector programs. As electricity tariffs climb and corporate net-zero pledges gain momentum, enterprises now treat lighting retrofits as first-wave decarbonization measures. The result is sustained double-digit volume demand for premium-efficiency chips, optics, and drivers across commercial, industrial, and high-end residential builds. Vendors that certify products under the latest Super ECBC thresholds are defending margins despite broader price competition.

Rapid urban infrastructure build-out (Smart Cities Mission)

The Smart Cities Mission has approved USD 24.7 billion in projects and completed 5,909 work orders by July 2024; each integrated command center specifies connected street, area, and facade lighting that can be monitored in real time. Municipalities increasingly bundle lighting into traffic, safety, and environmental dashboards, turning luminaires into edge nodes for broader city-data platforms. Vendors able to supply interoperable controls, adaptive-dimming algorithms, and cyber-secure firmware are winning multiyear framework contracts. Because second-tier cities replicate flagship designs from metros such as Pune and Varanasi, contract pipelines extend well into the medium term. The clustering of projects also shortens payback cycles for specialized installers and keeps warehouse throughput high for component suppliers.

High upfront retrofit cost for SMEs and households

Small factories and neighborhood retailers often face payback periods of 3-5 years on full-facility LED conversions, making many defer projects despite 40%-60% potential energy savings. Limited awareness of lifecycle economics keeps decision-makers focused on sticker price rather than total cost of ownership. Although micro-finance and utility-on-bill schemes exist, uptake remains low in non-metro clusters because of cumbersome documentation and perceived technology risk. This capex hurdle slows penetration of connected fixtures and sensors that carry higher dollar-per-lumen pricing compared with basic retrofit bulbs.

Other drivers and restraints analyzed in the detailed report include:

- Government procurement (UJALA and SLNP)

- Growth of Tier-II/III city facade-lighting projects

- Fragmented distribution and counterfeit products

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The luminaires and fixtures segment commanded a 58.72% revenue slice of the India lighting market in 2025 and is projected to grow at a 11.78% CAGR through 2031, underlining its dual role as both volume and value driver of the India lighting market. This category's rise stems from Smart Cities Mission tenders that specify integrated, sensor-ready fixtures and from private developers bundling lighting with building-automation contracts to cut commissioning time. Luminaires frequently anchor facade-lighting packages, earning higher margins than commodity lamps because they embed optics, drivers, and on-board diagnostics that meet Bureau of Energy Efficiency specifications. Contractors targeting metro rail, airport-terminal, and data-center projects also prefer turnkey luminaires to minimize field wiring errors and accelerate sign-off, extending the segment's edge in the India lighting market.

Second-order momentum comes from programmable RGB architectural jobs in Tier-II/III cities, where local authorities seek tourism branding without paying metro-grade premiums. Mid-range manufacturers that certify to BIS safety rules are winning here by pairing aluminum extrusion heat sinks with DMX controls that survive high-humidity coastal climates. Lamps, by contrast, continue to cede ground as price erosion compresses margins and government procurement resets bulk tender benchmarks. Even so, retrofit CFL-to-LED bulb swaps persist in the residential channel, cushioning lamps' volume decline but not reversing the structural tilt toward higher-value luminaires.

India LED lighting solutions held an 81.35% India lighting market share in 2025 and are projected to post the fastest 12.05% CAGR to 2031. The India lighting market size is tied to LEDs for commercial ceilings, roadway poles, and industrial high-bays, reflecting deeper penetration into price-sensitive rural installations. UJALA and Street Lighting National Program tenders normalized LED economics, while ECBC "Super" ratings funnel premium demand toward >=150-lm/W luminaires that still command price premiums. Conventional fluorescent and HID technologies now survive mainly in legacy high-temperature factories where drivers face derating risks, but even those niches are shrinking as ruggedized LED engine platforms pass accelerated lifecycle tests.

LED adoption also benefits from emerging Li-Fi pilots that turn luminaires into data nodes, allowing facilities to overlay broadband capacity without radio-frequency congestion. Wipro Lighting's alliance with pureLiFi exemplifies how vendors link illumination with connectivity to protect margins in a rapidly commoditizing diode market. At the same time, the Production-Linked Incentive Scheme for white goods subsidizes chip-on-board back-end lines, further localizing the LED bill of materials and improving cost resilience against import shocks, an upside for the India lighting industry as a whole.

Complete Report Scope:

- By Product Type

- Luminaires / Fixtures

- Lamps

- By Light Source

- LED

- Conventional

- By Distribution Channel

- Direct Sales / Developers / Contract

- Wholesalers / Electricians

- Lighting Specialists

- Others

- By Application

- Commercial

- Offices

- Retail and Hospitality

- Healthcare Facilities

- Others

- Industrial

- Process Industries

- Discrete Industries

- Warehouses and Other Industrial Set-ups

- Outdoor

- Residential

- Commercial

List of Companies Covered in this Report:

- Signify N.V.

- Havells India Limited

- Wipro Lighting (Wipro Ltd.)

- Bajaj Electricals Ltd.

- Syska LED Lights Pvt Ltd.

- Crompton Greaves Consumer Electricals Ltd.

- Surya Roshini Ltd.

- Halonix Technologies Pvt Ltd.

- MIC Electronics Ltd.

- Orient Electric Ltd.

- Panasonic Life Solutions India Pvt Ltd.

- Osram GmbH

- Zumtobel Group AG

- Acuity Brands Inc.

- Eaton Corporation plc (Cooper Lighting)

- Hubbell Inc.

- Fagerhult AB

- Dialight plc

- Nichia Corporation

- Eveready Industries India Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 LED price erosion and energy-efficiency mandates

- 4.2.2 Rapid urban infrastructure build-out (Smart Cities Mission)

- 4.2.3 Government procurement (UJALA and SLNP)

- 4.2.4 Growth of Tier-II/III city facade-lighting projects

- 4.2.5 Emerging DC-micro-grid and off-grid solar lighting demand

- 4.2.6 Integration of Li-Fi pilots in enterprise campuses

- 4.3 Market Restraints

- 4.3.1 High upfront retrofit cost for SMEs and households

- 4.3.2 Fragmented distribution and counterfeit products

- 4.3.3 Import-linked volatility in LED driver IC pricing

- 4.3.4 Slow pay-out cycles in government EPC contracts

- 4.4 Industry Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Luminaires / Fixtures

- 5.1.2 Lamps

- 5.2 By Light Source

- 5.2.1 LED

- 5.2.2 Conventional

- 5.3 By Distribution Channel

- 5.3.1 Direct Sales / Developers / Contract

- 5.3.2 Wholesalers / Electricians

- 5.3.3 Lighting Specialists

- 5.3.4 Others

- 5.4 By Application

- 5.4.1 Commercial

- 5.4.1.1 Offices

- 5.4.1.2 Retail and Hospitality

- 5.4.1.3 Healthcare Facilities

- 5.4.1.4 Others

- 5.4.2 Industrial

- 5.4.2.1 Process Industries

- 5.4.2.2 Discrete Industries

- 5.4.2.3 Warehouses and Other Industrial Set-ups

- 5.4.3 Outdoor

- 5.4.4 Residential

- 5.4.1 Commercial

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Signify N.V.

- 6.4.2 Havells India Limited

- 6.4.3 Wipro Lighting (Wipro Ltd.)

- 6.4.4 Bajaj Electricals Ltd.

- 6.4.5 Syska LED Lights Pvt Ltd.

- 6.4.6 Crompton Greaves Consumer Electricals Ltd.

- 6.4.7 Surya Roshini Ltd.

- 6.4.8 Halonix Technologies Pvt Ltd.

- 6.4.9 MIC Electronics Ltd.

- 6.4.10 Orient Electric Ltd.

- 6.4.11 Panasonic Life Solutions India Pvt Ltd.

- 6.4.12 Osram GmbH

- 6.4.13 Zumtobel Group AG

- 6.4.14 Acuity Brands Inc.

- 6.4.15 Eaton Corporation plc (Cooper Lighting)

- 6.4.16 Hubbell Inc.

- 6.4.17 Fagerhult AB

- 6.4.18 Dialight plc

- 6.4.19 Nichia Corporation

- 6.4.20 Eveready Industries India Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

全球通用照明市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球通用照明市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 燈具照明市場機會、成長要素、產業趨勢分析及2026-2035年預測。

燈具照明市場機會、成長要素、產業趨勢分析及2026-2035年預測。 垂直農業照明市場規模、佔有率和趨勢分析報告:按組件、照明類型、農場類型、安裝類型、作物類型、最終用途、地區和細分市場預測(2026-2033 年)

垂直農業照明市場規模、佔有率和趨勢分析報告:按組件、照明類型、農場類型、安裝類型、作物類型、最終用途、地區和細分市場預測(2026-2033 年) 基礎設施照明市場-全球產業規模、佔有率、趨勢、機會和預測:按技術、產品、應用、地區和競爭格局分類,2021-2031年

基礎設施照明市場-全球產業規模、佔有率、趨勢、機會和預測:按技術、產品、應用、地區和競爭格局分類,2021-2031年 住宅Wi-Fi基礎設施

住宅Wi-Fi基礎設施 2026年全球機場排水系統市場報告

2026年全球機場排水系統市場報告 室內農業LED系統市場預測至2034年—全球系統類型、LED系統、組件、技術、應用、最終用戶和區域分析

室內農業LED系統市場預測至2034年—全球系統類型、LED系統、組件、技術、應用、最終用戶和區域分析 全球氣體放電管市場(至 2030 年):按產品類型(通孔、表面黏著技術、混合型)、電極數量(2 位、3 位)、電壓(高壓、低壓和中壓)和應用(配電、通訊、消費性電子產品、工業)分類

全球氣體放電管市場(至 2030 年):按產品類型(通孔、表面黏著技術、混合型)、電極數量(2 位、3 位)、電壓(高壓、低壓和中壓)和應用(配電、通訊、消費性電子產品、工業)分類 障礙指示燈市場:2026-2032年全球市場預測(依技術、亮度、安裝方式、應用及最終用戶分類)

障礙指示燈市場:2026-2032年全球市場預測(依技術、亮度、安裝方式、應用及最終用戶分類) 照明市場報告:按類型、應用程式、最終用戶和地區分類(2025-2033 年)

照明市場報告:按類型、應用程式、最終用戶和地區分類(2025-2033 年)