|

市場調查報告書

商品編碼

2071326

燈具照明市場機會、成長要素、產業趨勢分析及2026-2035年預測。Lamps and Lighting Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

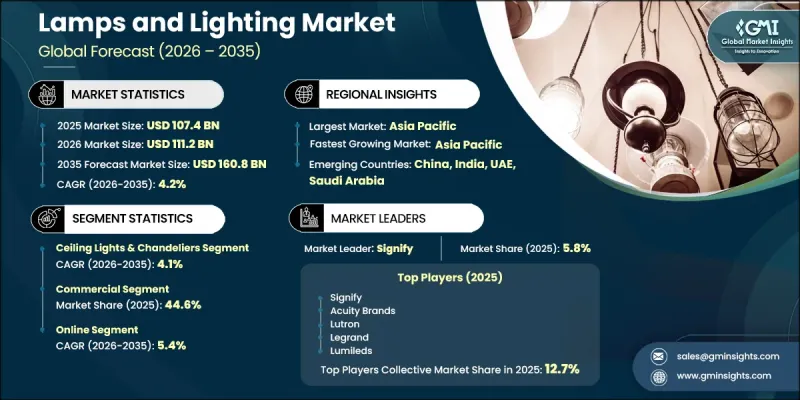

預計到 2025 年,全球燈具和照明市場價值將達到 1,074 億美元,並將以 4.2% 的複合年成長率成長,到 2035 年達到 1,608 億美元。

由於城市快速發展、可支配收入水準提高以及照明技術的不斷進步,照明產業正穩步擴張。節能照明系統(尤其是LED照明解決方案)的日益普及是市場擴張的主要成長要素之一。政府限制使用高能耗白熾燈產品的法規進一步加速了向高效替代品的轉變。此外,永續性增強的永續發展措施和環保意識也推動了住宅、商業和工業領域對環保照明解決方案的需求。具備遙控、亮度調節和色彩自訂等功能的智慧照明系統的日益普及也對市場產生了積極影響。建設活動和基礎設施建設項目的活性化,尤其是在新興國家,進一步推動了對最新照明解決方案的需求。辦公大樓、零售商店和酒店等商業空間的擴張也促進了市場的穩定成長。總而言之,燈具和照明市場正朝著智慧化、節能化和注重設計的解決方案發展,以適應現代生活方式和基礎設施需求。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 1074億美元 |

| 預計金額 | 1608億美元 |

| 複合年成長率 | 4.2% |

預計2025年,吸頂燈和水晶燈市場規模將達599億美元,預測期內複合年成長率(CAGR)為4.1%。消費者對美觀節能的照明解決方案的偏好不斷成長,是推動該細分市場持續成長的主要因素。現代室內設計趨勢對市場需求產生了顯著影響,照明在營造氛圍和提升視覺吸引力方面發揮核心作用。 LED技術的引入進一步提高了能源效率和產品壽命,使這些照明解決方案在住宅和商業環境中都更具吸引力。隨著人們對現代室內空間的日益關注,預計該細分市場的需求成長將持續下去。

預計到2025年,商業照明市場將佔據44.6%的市場。商業照明市場的成長主要得益於辦公空間、零售商店、飯店設施和其他公共空間的擴張。節能智慧照明系統的日益普及,幫助企業在遵守能源法規的同時降低營運成本。此外,智慧互聯照明技術在商業建築的應用,也有助於提升能源管理和自動化水準。住宅照明市場同樣呈現強勁成長勢頭,消費者在住宅維修和改造中加強對節能美觀照明解決方案的投資。

預計到2025年,美國燈具照明市場將佔據全球81%的佔有率,市場規模將達到174億美元。美國市場成長的主要驅動力是快速的都市化、技術進步以及對節能照明解決方案日益成長的需求。強力的監管支持,例如推廣LED照明和提高能源效率,也進一步推動了市場擴張。此外,永續建築實踐和綠建築標準的廣泛應用,也帶動了住宅、商業和工業領域對先進照明系統的需求。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 供應鏈分析

- 全球採購模式

- 供應鏈脆弱性

- 近岸外包和回岸外包的趨勢

- 3.7.4 供應商多角化策略

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 機會

- 成長潛力分析

- 未來市場趨勢

- 技術與創新展望

- 最新科技趨勢

- 新興技術

- 波特五力分析

- PESTLE分析

- 價格趨勢

- 對過去價格趨勢的分析

- 定價策略:按業務類型分類

- 監理框架

- 美國聯邦法規

- 美國能源局(DOE) 照明標準

- 《能源政策法案》(EPAct)的要求

- 照明生態設計指令(2009/125/EC)

- 能源標籤條例(歐盟)2019/2015

- 貿易數據分析

- 進出口量及進口額趨勢

- 主要貿易路線及關稅的影響

- 人工智慧和生成式人工智慧對市場的影響

- 人工智慧正在改變傳統的經營模式。

- 按客戶群分類的生成式人工智慧用例和部署藍圖

- 風險、限制和監管考量

- 人工智慧驅動的生態系統整合

- 消費行為分析

- 購買模式

- 偏好分析

- 不同地區的消費行為差異

- 電子商務對購買決策的影響

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 吸頂燈和水晶燈

- 間接照明

- 嵌入式照明

- 工作照明

- 其他(例如重點照明)

- 燈泡和照明燈具

- 白熾燈泡

- 鹵素

- 發光二極體

- 其他(例如,節能螢光)

- 可攜式燈

- 檯燈

- 落地燈

- 檯燈

- 其他(閱讀燈等)

第6章 市場估計與預測:依技術分類,2022-2035年

- Smart

- 傳統的

第7章 市場估計與預測:依安裝類型分類,2022-2035年

- 室內的

- 戶外的

第8章 市場估計與預測:依價格分類,2022-2035年

- 低價位(500以下)

- 中價位(500-999 美元)

- 高價位(1000美元或以上)

第9章 市場估價與預測:依最終用戶分類,2022-2035年

- 住宅

- 商業

- 辦公室

- 零售空間

- 飯店和餐廳

- 醫院和醫療設施

- 其他(教育機構等)

- 產業

第10章 市場估價與預測:依通路分類,2022-2035年

- 線上

- 電子商務

- 公司網站

- 離線

- 超級市場和大賣場

- 專賣店

- 其他(家居建材商店等)

第11章 市場估價與預測:按地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- UAE

第12章:公司簡介

- 全球主要公司

- Acuity Brands

- Fagerhult

- Legrand

- Lutron

- Panasonic

- Signify(Philips)

- Zumtobel Group

- 當地公司

- Bajaj Electricals

- Crompton Greaves Consumer

- Foshan Lighting(FSL)

- Havells India

- NVC Lighting

- Opple Lighting

- Trilux

- 新興企業和專業公司

- Amerlux

- BIOS Lighting

- California LightWorks

- Heliospectra

- Lumileds

- Seoul Semiconductor

- Visa Lighting

The Global Lamps and Lighting Market was valued at USD 107.4 billion in 2025 and is estimated to grow at a CAGR of 4.2% to reach USD 160.8 billion by 2035.

The industry is expanding steadily due to rapid urban development, rising disposable income levels, and continuous advancements in lighting technologies. Increasing adoption of energy-efficient lighting systems, particularly LED-based solutions, is one of the primary growth catalysts shaping market expansion. Government regulations restricting the use of high-energy-consuming incandescent lighting products have further accelerated the shift toward efficient alternatives. In addition, sustainability initiatives and environmental awareness are driving demand for eco-friendly lighting solutions across residential, commercial, and industrial sectors. The market is also benefiting from the growing penetration of smart lighting systems that offer features such as remote operation, adjustable brightness, and customizable color settings. Rising construction activities and infrastructure development projects, particularly in emerging economies, are further supporting demand for modern lighting solutions. Expanding commercial spaces, including offices, retail environments, and hospitality infrastructure, are also contributing to consistent market growth. Overall, the lamps and lighting market is evolving toward intelligent, energy-efficient, and design-oriented solutions aligned with modern lifestyle and infrastructure requirements.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $107.4 Billion |

| Forecast Value | $160.8 Billion |

| CAGR | 4.2% |

The ceiling lights and chandeliers segment generated USD 59.9 billion in 2025 and is projected to grow at a CAGR of 4.1% through the forecast period. This segment continues to dominate due to increasing consumer preference for aesthetically appealing and energy-efficient lighting solutions. Demand is strongly influenced by modern interior design trends, where lighting plays a central role in enhancing ambiance and visual appeal. The integration of LED technology has further improved energy efficiency and product lifespan, making these lighting solutions more attractive for both residential and commercial applications. Growing emphasis on contemporary interior spaces is expected to sustain demand growth in this segment.

The commercial segment accounted for 44.6% share in 2025. Growth in the commercial segment is driven by the expansion of office spaces, retail establishments, hospitality venues, and other institutional facilities. Increasing adoption of energy-efficient and smart lighting systems is helping organizations reduce operational costs while complying with energy regulations. Additionally, the integration of smart and connected lighting technologies in commercial buildings is supporting improved energy management and automation. The residential segment is also witnessing strong momentum as consumers increasingly invest in energy-saving and visually appealing lighting solutions for home improvement and modernization.

United States Lamps and Lighting Market held an 81% share in 2025 generating USD 17.4 billion. Market growth in the country is supported by rapid urbanization, technological advancements, and rising demand for energy-efficient lighting solutions. Strong regulatory support promoting LED adoption and energy conservation has further strengthened market expansion. The widespread implementation of sustainable building practices and green construction standards is also driving demand for advanced lighting systems across residential, commercial, and industrial applications.

Key companies operating in the Global Lamps and Lighting Market include Signify (Philips), Panasonic, Lutron, Legrand, Zumtobel Group, Fagerhult, Acuity Brands, Opple Lighting, Bajaj Electricals, Havells India, Crompton Greaves Consumer, FSL (Foshan Lighting), NVC Lighting, Trilux, Amerlux, BIOS Lighting, California LightWorks, Heliospectra, Lumileds, Seoul Semiconductor, and Visa Lighting. Companies in the Global Lamps and Lighting Market are focusing on multiple strategic initiatives to strengthen their market presence and enhance competitiveness. Product innovation remains a key priority, with manufacturers developing advanced LED systems, smart lighting solutions, and energy-efficient designs tailored to evolving consumer demands. Investment in research and development is enabling improvements in product performance, durability, and customization capabilities. Many companies are expanding their smart lighting portfolios by integrating IoT-based controls, automation features, and connectivity solutions. Strategic partnerships with construction firms, real estate developers, and infrastructure projects are supporting wider market penetration. Expansion into emerging markets and strengthening of distribution networks are also improving accessibility.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Technology

- 2.2.4 Installation

- 2.2.5 Price

- 2.2.6 End Users

- 2.2.7 Distribution Channel

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Supply Chain Analysis

- 3.2.1 Global sourcing patterns

- 3.2.2 Supply chain vulnerabilities

- 3.2.3 Nearshoring & reshoring trends

- 3.3 3.7.4. Supplier Diversification Strategies

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.4.3 Opportunities

- 3.5 Growth potential analysis

- 3.6 Future market trends

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Porter's five forces analysis

- 3.9 PESTEL analysis

- 3.10 Price trends

- 3.10.1 Historical price trend analysis

- 3.10.2 Pricing strategy by player type

- 3.11 Regulatory framework

- 3.11.1 United States Federal Regulations

- 3.11.2 Department of Energy (DOE) Lighting Standards

- 3.11.3 Energy Policy Act (EPAct) Requirements

- 3.11.4 Ecodesign Directive (2009/125/EC) for Lighting

- 3.11.5 Energy Labeling Regulation (EU) 2019/2015

- 3.12 Trade Data Analysis (Driven by Paid Database)

- 3.12.1 Import & export volume & value trends

- 3.12.2 Key trade corridors & tariff impact

- 3.13 Impact of AI & generative AI on the market

- 3.13.1 AI-driven disruption of traditional business models

- 3.13.2 GenAI use cases & adoption roadmap by customer segment

- 3.13.3 Risks, limitations & regulatory considerations

- 3.13.4 AI-enabled ecosystem integration

- 3.14 Consumer behavior analysis

- 3.14.1 Purchasing patterns

- 3.14.2 Preference analysis

- 3.14.3 Regional variations in consumer behavior

- 3.14.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035 ($Billion, Million Units)

- 5.1 Key trends

- 5.2 Ceiling lights & chandeliers

- 5.2.1 Ambient lighting

- 5.2.2 Recessed lighting

- 5.2.3 Task lighting

- 5.2.4 Others (accent lighting etc.)

- 5.3 Light bulbs & fittings

- 5.3.1 Incandescent

- 5.3.2 Halogen

- 5.3.3 Light-emitting diode

- 5.3.4 Others (compact fluorescent etc.)

- 5.4 Portable lamps

- 5.4.1 Table lamps

- 5.4.2 Floor lamps

- 5.4.3 Desk lamps

- 5.4.4 Others (reading lights etc.)

Chapter 6 Market Estimates & Forecast, By Technology, 2022 - 2035 ($Billion, Million Units)

- 6.1 Key trends

- 6.2 Smart

- 6.3 Conventional

Chapter 7 Market Estimates & Forecast, By Installation, 2022 - 2035 ($Billion, Million Units)

- 7.1 Key trends

- 7.2 Indoor

- 7.3 Outdoor

Chapter 8 Market Estimates & Forecast, By Price, 2022 - 2035 ($Billion, Million Units)

- 8.1 Key trends

- 8.2 Low (below 500)

- 8.3 Medium (USD 500 - USD 999)

- 8.4 High (USD 1,000 and above)

Chapter 9 Market Estimates & Forecast, By End Users, 2022 - 2035 ($Billion, Million Units)

- 9.1 Key trends

- 9.2 Residential

- 9.3 Commercial

- 9.3.1 Office

- 9.3.2 Retail spaces

- 9.3.3 Hotels and restaurants

- 9.3.4 Hospital and healthcare facilities

- 9.3.5 Others (educational institutes etc.)

- 9.4 Industrial

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Billion, Million Units)

- 10.1 Key trends

- 10.2 Online

- 10.2.1 E-commerce

- 10.2.2 Company websites

- 10.3 Offline

- 10.3.1 Supermarkets and hypermarkets

- 10.3.2 Specialty stores

- 10.3.3 Others (home improvement stores etc.)

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Billion, Million Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Key Players

- 12.1.1 Acuity Brands

- 12.1.2 Fagerhult

- 12.1.3 Legrand

- 12.1.4 Lutron

- 12.1.5 Panasonic

- 12.1.6 Signify (Philips)

- 12.1.7 Zumtobel Group

- 12.2 Regional Players

- 12.2.1 Bajaj Electricals

- 12.2.2 Crompton Greaves Consumer

- 12.2.3 Foshan Lighting (FSL)

- 12.2.4 Havells India

- 12.2.5 NVC Lighting

- 12.2.6 Opple Lighting

- 12.2.7 Trilux

- 12.3 Emerging/Niche Specialists

- 12.3.1 Amerlux

- 12.3.2 BIOS Lighting

- 12.3.3 California LightWorks

- 12.3.4 Heliospectra

- 12.3.5 Lumileds

- 12.3.6 Seoul Semiconductor

- 12.3.7 Visa Lighting

全球通用照明市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球通用照明市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 垂直農業照明市場規模、佔有率和趨勢分析報告:按組件、照明類型、農場類型、安裝類型、作物類型、最終用途、地區和細分市場預測(2026-2033 年)

垂直農業照明市場規模、佔有率和趨勢分析報告:按組件、照明類型、農場類型、安裝類型、作物類型、最終用途、地區和細分市場預測(2026-2033 年) 基礎設施照明市場-全球產業規模、佔有率、趨勢、機會和預測:按技術、產品、應用、地區和競爭格局分類,2021-2031年

基礎設施照明市場-全球產業規模、佔有率、趨勢、機會和預測:按技術、產品、應用、地區和競爭格局分類,2021-2031年 住宅Wi-Fi基礎設施

住宅Wi-Fi基礎設施 2026年全球機場排水系統市場報告

2026年全球機場排水系統市場報告 室內農業LED系統市場預測至2034年—全球系統類型、LED系統、組件、技術、應用、最終用戶和區域分析

室內農業LED系統市場預測至2034年—全球系統類型、LED系統、組件、技術、應用、最終用戶和區域分析 全球氣體放電管市場(至 2030 年):按產品類型(通孔、表面黏著技術、混合型)、電極數量(2 位、3 位)、電壓(高壓、低壓和中壓)和應用(配電、通訊、消費性電子產品、工業)分類

全球氣體放電管市場(至 2030 年):按產品類型(通孔、表面黏著技術、混合型)、電極數量(2 位、3 位)、電壓(高壓、低壓和中壓)和應用(配電、通訊、消費性電子產品、工業)分類 障礙指示燈市場:2026-2032年全球市場預測(依技術、亮度、安裝方式、應用及最終用戶分類)

障礙指示燈市場:2026-2032年全球市場預測(依技術、亮度、安裝方式、應用及最終用戶分類) 照明市場報告:按類型、應用程式、最終用戶和地區分類(2025-2033 年)背光模組導光板市場報告:趨勢、預測及競爭分析(至2035年)

照明市場報告:按類型、應用程式、最終用戶和地區分類(2025-2033 年)背光模組導光板市場報告:趨勢、預測及競爭分析(至2035年)