|

市場調查報告書

商品編碼

2072516

印度倉儲自動化:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)India Warehouse Automation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

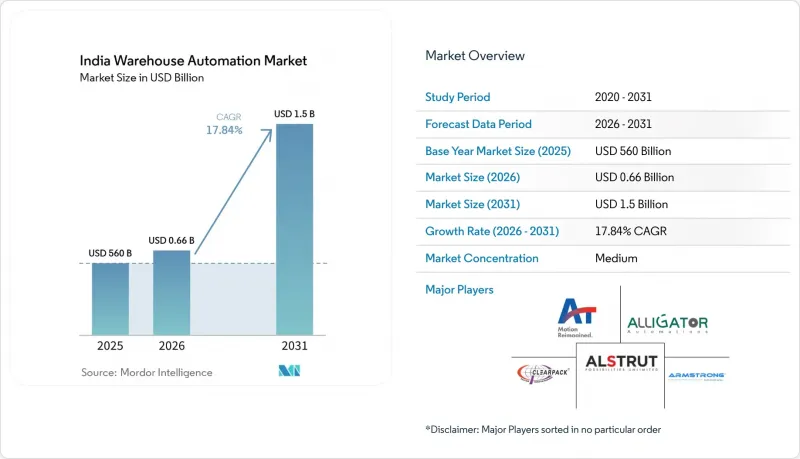

根據 Mordor Intelligence 預測,印度倉庫自動化市場規模將從 2025 年的 5.6 億美元成長到 2026 年的 6.5996 億美元,然後在 2031 年達到 15 億美元,2026 年至 2031 年的複合年成長率為 17.84%。

本報告按組件(硬體、軟體、服務)、自動化程度(基本機械化、半自動化系統、全自動機器人/自動化立體倉庫)、功能(揀选和分揀、碼垛和拆垛、存儲和檢索等)以及最終用戶行業(電子商務/第三方物流、快速消費品/零售等)進行細分。市場預測以美元計價。

印度倉儲自動化市場趨勢與洞察

印度電子商務的爆炸性成長

預計到2030年,印度線上零售業規模將達到3,000億美元,主要得益於食品雜貨訂單的激增,以及2022年二、三線城市銷售額佔總銷售額的41.5%。傳統的堆疊式倉庫已無法滿足顧客對當日達或10分鐘內送達的期望,因此,超過4000家「暗店」(即非實體倉庫)開始採用自動化揀貨艙和機器人分類機。物流成本預計在2024年佔GDP的7.8%至8.9%,但隨著自動化樞紐減少揀貨錯誤並縮短配送距離,物流成本預計將會下降。具有前瞻性的營運商正在自動化立體倉庫(AS/RS)網格上疊加基於人工智慧的庫存管理引擎,以即時調整多通路庫存池。

消費主導加速了倉庫整合進程

商品及服務稅(GST)的引入消除了跨州庫存緩衝,促進了全國物流網路的發展。平均設施面積從2023年的5萬平方英尺飆升至2025年的20萬平方英尺以上,鞏固了高層自動化立體倉庫(AS/RS)和穿梭車系統的經濟可行性。每個倉庫的托盤數量通常超過1萬個,推動了多層包覆式貨架設計的應用,這種設計既能最大限度地利用垂直空間,又能降低建造成本。日常消費品(FMCG)和製藥業受益最大,因為集中化的倉庫位置簡化了批次追溯和低溫運輸合規性。 2024年,浦那和國家首都轄區(NCR)的租金上漲了5%,開發商競相提供A級倉庫,這些倉庫擁有平坦的地面和11-12米的淨空高度,對於高速起重機的運作至關重要。

大量低成本的體力勞動

非正規部門僱用了5億工人,他們的起薪僅為每月1.5萬至2萬盧比,因此機械化投資的回收期較長。三線城市的成本比第一線城市低30%至40%,中小企業往往會延後自動化進程。然而,到了2024年,孟買和德里的薪資漲幅超過15%至20%,因為倉庫競相招攬技術工人。同時,隨著年輕工人轉向技能要求更高的工作崗位,勞動力素質下降,人們對語音揀貨和「貨到人」推車等半自動化輔助工具的興趣日益濃厚。

細分市場分析

預計到2025年,硬體將佔銷售額的60.55%,凸顯了印度倉儲自動化市場對輸送機、穿梭式貨架和機械臂的依賴。位於比萬迪和斯里佩姆布杜爾的大規模棕地園區已部署了高位貨架自動化立體倉庫系統(AS/RS),使現有倉庫的托盤密度提高了四倍。這進一步鞏固了硬體作為營運基礎的地位。然而,隨著部署基礎的成熟,決策者正將預算轉向雲端倉庫管理系統(WMS)、數位雙胞胎和人工智慧引擎,以釋放潛力並將運轉率提升至85%以上。

到2031年,軟體市場27.40%的複合年成長率反映了這一轉型。 Addverb的「Mobinity」等SaaS平台能夠整合和管理多供應商設備,並利用機器學習技術進行工位分配、人員配備和能源管理。在2026-2028年的支出週期中,改裝將成為主導,因為營運商意識到,與傳統硬體佈局相比,數據豐富的控制層能夠帶來顯著的投資回報。服務業也呈現類似的趨勢,因為需要整合商將分散的機械設備整合到統一的、符合API規範的生態系統中。

到2025年,半自動化解決方案將佔印度倉庫自動化市場48.60%的佔有率,這反映了市場對逐步變革的合理需求。配備即時位置感測器的揀貨指示燈站、旋轉貨架模組和堆高機通常可將生產效率提高40-60%,而成本卻比全機器人系統低30-50%。企業正在將這些工具與靈活的資金籌措結合,檢驗其工作流程,然後逐步升級到「貨到人」機器人系統。

全自動化機器人系統正以27.10%的複合年成長率快速發展,並日益應用於製藥和低溫運輸設施中,因為在這些領域,違規罰款遠高於設備成本。供應商正在將環境監測、可追溯性記錄和人工智慧視覺功能整合到承包單元中,將錯誤率降低到0.1%以下。隨著國內零件生產線在「零件製造方案」下不斷擴張,價格競爭力也不斷提升。預計到2031年,全自動化系統將佔新建設案的60%,其他方式將佔40%。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 印度電子商務的爆炸性成長

- 商品及服務稅 (GST) 引發了倉庫整合加速。

- 商品及服務稅 (GST)電子帳單開立 API 簡介

- 政府的產品授權計劃 (PLI) 正在促進 SKU 數量的成長。

- 10分鐘內「快速交易」的需求

- 主要物流樞紐人手不足激增

- 市場限制因素

- 大量低成本的體力勞動

- 自動化立體倉庫和機器人技術的初始資本投資成本高昂

- 中小企業擁有的倉庫位置分散。

- 電力品質和地面平整度方面的標準不一致。

- 價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素對市場的影響

第5章 市場規模與成長預測

- 按組件

- 硬體

- 軟體

- 服務

- 按自動化級別

- 基本機械化

- 半自動系統

- 全自動(機器人/自動化立體倉庫)

- 按功能

- 揀貨和分類

- 碼垛和卸垛

- 儲存和檢索

- 包裝和標籤

- 影像檢查和品管

- 運輸和AGV/AMR

- 按最終用戶行業分類

- 電子商務與第三方物流

- 快速消費品和零售

- 藥品和醫療保健

- 車

- 電子設備

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Addverb Technologies Private Limited

- Alligator Automations Private Limited

- Alstrut India Private Limited

- Armstrong Machine Builders Private Limited

- Clearpack India Private Limited

- Delta Electronics, Inc.

- Falcon Autotech Private Limited

- Signode India Limited

- Titan Engineering and Automation Limited

- Win Automation(Wipro Limited)

- Worldpack Automation Systems Private Limited

- SICK AG

- Keyence Corporation

- OMRON Corporation

- GreyOrange Private Limited

- Godrej Consoveyo Logistics Automation Limited

- SSI SCHAEFER Systems International Private Limited

- Daifuku Co., Ltd.

- Swisslog Holding AG

- Honeywell Intelligrated(Honeywell International Inc.)

- Toyota Material Handling India Private Limited

- Vanderlande Industries BV

第7章 市場機會與未來展望

According to Mordor Intelligence, the india warehouse automation market size is expected to grow from USD 560 million in 2025 to USD 659.96 million in 2026 and is forecast to reach USD 1.5 billion by 2031 at 17.84% CAGR over 2026-2031.

This report is Segmented by Component (Hardware, Software, and Services), Automation Level (Basic Mechanization, Semi-Automated Systems, and Fully Automated Robotics/AS-RS), Function (Picking and Sorting, Palletizing and Depalletizing, Storage and Retrieval, and More), and End-User Industry (E-Commerce and 3PL, FMCG and Retail, and More). The Market Forecasts are Provided in Terms of Value (USD).

India Warehouse Automation Market Trends and Insights

Explosive Growth of Indian E-commerce

India's online retail sector is on track to reach USD 300 billion by 2030, propelled by a surge in grocery orders and a 41.5% sales contribution from Tier-2 and Tier-3 cities in 2022. Traditional block-stack warehouses can no longer support same-day or 10-minute expectations, prompting 4,000+ dark stores to install automated picking pods and robotic sorters. Logistics costs, which consumed 7.8-8.9% of GDP in 2024, are forecast to fall as automated hubs cut mis-picks and shrink delivery kilometers. Forward-looking operators are layering AI-based inventory engines over AS/RS grids to orchestrate multi-channel stock pools in real time.

Fast-track GST-Led Consolidation of Warehouses

GST removed state-border inventory buffers, allowing national distribution networks to flourish. Average facility size jumped from 50,000 sq ft in 2023 to over 200,000 sq ft by 2025, cementing the economic case for high-bay AS/RS and shuttle systems. Pallet counts per site often top 10,000, encouraging multilevel clad-rack designs that maximize vertical space while trimming civil costs. FMCG and pharmaceuticals benefit most because consolidated nodes simplify batch traceability and cold-chain compliance. Rental rates climbed 5% in Pune and NCR during 2024 as developers raced to deliver Grade-A boxes with flat floors and 11-12 m clear heights, prerequisites for fast-moving cranes.

Abundant Low-cost Manual Labor Pool

With 500 million workers in the informal sector, entry-level wages of Rs 15,000-20,000 per month extend the payback window for mechanization. In Tier-3 centers, costs are 30-40% lower, tempting SMEs to delay automation. Yet wage inflation topped 15-20% in Mumbai and Delhi during 2024 as warehouses competed for skilled handlers. Simultaneously, younger workers are pivoting to higher-skill jobs, eroding labor quality and fueling interest in semi-automated aids such as voice picking and goods-to-person carts.

Other drivers and restraints analyzed in the detailed report include:

- Adoption of Goods and Services Tax E-invoicing APIs

- Government PLI Schemes Boosting SKU Proliferation

- High Upfront CAPEX of AS/RS and Robotics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware commanded 60.55% of 2025 revenue, underscoring India warehouse automation market reliance on conveyors, shuttle racks, and robotic arms. Large brownfield campuses in Bhiwandi and Sriperumbudur tapped high-bay AS/RS to quadruple pallet density within existing footprints, reinforcing hardware's role as the operational backbone. Yet as installed bases mature, decision-makers are shifting budget toward cloud WMS, digital twins, and AI engines that unlock latent capacity and lift utilization above 85%.

Software's 27.40% CAGR through 2031 mirrors this pivot. SaaS platforms such as Addverb's Mobinity orchestrate multi-vendor fleets and inject machine learning into slotting, labor assignment, and energy management. Retro-fits dominate 2026-2028 spending cycles as operators realize that data-rich control layers deliver step-change returns on earlier hardware layouts. Services follow suit because integrators are needed to weave siloed machines into unified, API-compliant ecosystems.

Semi-automated solutions held 48.60% of India warehouse automation market share in 2025, reflecting a pragmatic appetite for incremental change. Put-to-light stations, carousel modules, and lift trucks fitted with real-time location sensors typically raise productivity 40-60% but cost 30-50% less than full robotics. Enterprises pair these tools with flexible financing, testing workflows before upgrading to goods-to-person bots.

Fully automated robotics, advancing at 27.10% CAGR, are surfacing in pharmaceutical and cold-chain facilities where compliance fines dwarf equipment costs. Vendors bundle environmental monitoring, traceability logs, and AI vision into turnkey cells that slash error rates to under 0.1%. Price parity is also improving as domestic component lines scale under the Component Manufacturing Scheme. By 2031, industry consensus expects a 60-40 split favoring fully automated formats in greenfield builds.

Complete Report Scope:

- By Component

- Hardware

- Software

- Services

- By Automation Level

- Basic Mechanization

- Semi-Automated Systems

- Fully Automated (Robotics/AS-RS)

- By Function

- Picking and Sorting

- Palletizing and Depalletizing

- Storage and Retrieval

- Packaging and Labelling

- Vision Inspection and QC

- Transportation and AGV/AMR

- By End-user Industry

- E-commerce and 3PL

- FMCG and Retail

- Pharmaceuticals and Healthcare

- Automotive

- Electronics

- Other End-user Industries

List of Companies Covered in this Report:

- Addverb Technologies Private Limited

- Alligator Automations Private Limited

- Alstrut India Private Limited

- Armstrong Machine Builders Private Limited

- Clearpack India Private Limited

- Delta Electronics, Inc.

- Falcon Autotech Private Limited

- Signode India Limited

- Titan Engineering and Automation Limited

- Win Automation (Wipro Limited)

- Worldpack Automation Systems Private Limited

- SICK AG

- Keyence Corporation

- OMRON Corporation

- GreyOrange Private Limited

- Godrej Consoveyo Logistics Automation Limited

- SSI SCHAEFER Systems International Private Limited

- Daifuku Co., Ltd.

- Swisslog Holding AG

- Honeywell Intelligrated (Honeywell International Inc.)

- Toyota Material Handling India Private Limited

- Vanderlande Industries B.V.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosive growth of Indian e-commerce

- 4.2.2 Fast-track GST-led consolidation of warehouses

- 4.2.3 Adoption of Goods and Services Tax e-invoicing APIs

- 4.2.4 Government PLI schemes boosting SKU proliferation

- 4.2.5 Demand for 10-minute "quick-commerce" fulfilment

- 4.2.6 Labor-shortage spikes in Tier-1 logistics hubs

- 4.3 Market Restraints

- 4.3.1 Abundant low-cost manual labor pool

- 4.3.2 High upfront capex of AS/RS and robotics

- 4.3.3 Fragmented SME-owned warehouse footprint

- 4.3.4 Inconsistent power-quality and floor-flatness norms

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Degree of Competition

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Automation Level

- 5.2.1 Basic Mechanization

- 5.2.2 Semi-Automated Systems

- 5.2.3 Fully Automated (Robotics/AS-RS)

- 5.3 By Function

- 5.3.1 Picking and Sorting

- 5.3.2 Palletizing and Depalletizing

- 5.3.3 Storage and Retrieval

- 5.3.4 Packaging and Labelling

- 5.3.5 Vision Inspection and QC

- 5.3.6 Transportation and AGV/AMR

- 5.4 By End-user Industry

- 5.4.1 E-commerce and 3PL

- 5.4.2 FMCG and Retail

- 5.4.3 Pharmaceuticals and Healthcare

- 5.4.4 Automotive

- 5.4.5 Electronics

- 5.4.6 Other End-user Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Addverb Technologies Private Limited

- 6.4.2 Alligator Automations Private Limited

- 6.4.3 Alstrut India Private Limited

- 6.4.4 Armstrong Machine Builders Private Limited

- 6.4.5 Clearpack India Private Limited

- 6.4.6 Delta Electronics, Inc.

- 6.4.7 Falcon Autotech Private Limited

- 6.4.8 Signode India Limited

- 6.4.9 Titan Engineering and Automation Limited

- 6.4.10 Win Automation (Wipro Limited)

- 6.4.11 Worldpack Automation Systems Private Limited

- 6.4.12 SICK AG

- 6.4.13 Keyence Corporation

- 6.4.14 OMRON Corporation

- 6.4.15 GreyOrange Private Limited

- 6.4.16 Godrej Consoveyo Logistics Automation Limited

- 6.4.17 SSI SCHAEFER Systems International Private Limited

- 6.4.18 Daifuku Co., Ltd.

- 6.4.19 Swisslog Holding AG

- 6.4.20 Honeywell Intelligrated (Honeywell International Inc.)

- 6.4.21 Toyota Material Handling India Private Limited

- 6.4.22 Vanderlande Industries B.V.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

倉儲自動化市場:按組件、自動化等級、倉庫規模、所有權模式、應用、最終用戶、國家和地區分類-全球產業分析、市場規模、市場佔有率和預測(2026-2033 年)

倉儲自動化市場:按組件、自動化等級、倉庫規模、所有權模式、應用、最終用戶、國家和地區分類-全球產業分析、市場規模、市場佔有率和預測(2026-2033 年) 倉儲自動化市場:按自動化類型、類別、組件、應用和最終用戶分類-2026-2032年全球市場預測自動化倉庫揀貨市場:2026年至2032年全球市場預測(依技術、系統類型、揀選方式、最終使用者產業、部署模式和組織規模分類)

倉儲自動化市場:按自動化類型、類別、組件、應用和最終用戶分類-2026-2032年全球市場預測自動化倉庫揀貨市場:2026年至2032年全球市場預測(依技術、系統類型、揀選方式、最終使用者產業、部署模式和組織規模分類) 2026年全球語音辨識語言模型市場報告2026年全球倉庫機器人車隊編配市場報告2026年全球倉儲自動化系統市場報告2026年全球倉儲自動化市場報告

2026年全球語音辨識語言模型市場報告2026年全球倉庫機器人車隊編配市場報告2026年全球倉儲自動化系統市場報告2026年全球倉儲自動化市場報告 日本倉儲自動化市場規模、佔有率、趨勢和預測:按組件、最終用戶和地區分類,2026-2034年

日本倉儲自動化市場規模、佔有率、趨勢和預測:按組件、最終用戶和地區分類,2026-2034年 倉儲自動化市場-全球產業規模、佔有率、趨勢、機會及預測(依產品、自動化程度、技術、應用、垂直產業、地區及競爭格局分類),2021-2031年語音揀選市場:收入模式、公司規模、部署類型、類型和最終用戶、全球預測(2026-2032 年)

倉儲自動化市場-全球產業規模、佔有率、趨勢、機會及預測(依產品、自動化程度、技術、應用、垂直產業、地區及競爭格局分類),2021-2031年語音揀選市場:收入模式、公司規模、部署類型、類型和最終用戶、全球預測(2026-2032 年)