|

市場調查報告書

商品編碼

2072474

密碼管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Password Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

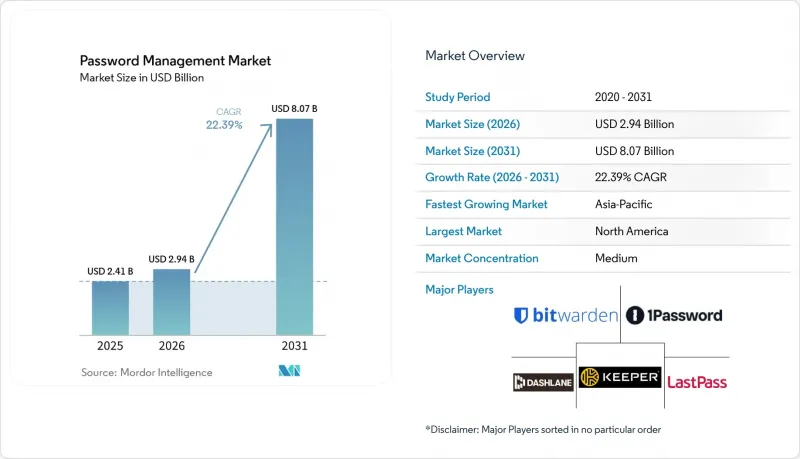

根據 Mordor Intelligence 預測,密碼管理市場規模將從 2025 年的 24.1 億美元和 2026 年的 29.4 億美元成長到 2031 年的 80.7 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 22.39%。

本報告按解決方案類型(自助服務、特權使用者)、存取/技術類型(桌上型電腦和筆記型電腦、其他)、部署類型(雲端託管、本地部署、混合式部署)、企業規模(大型企業、中小企業)、最終用戶產業(銀行、金融服務和保險、醫療保健、其他)以及地區(北美、南美、其他)進行細分。市場預測以美元計價。

全球密碼管理市場趨勢及洞察

零信任計畫加速北美銀行、金融服務和保險 (BFSI) 產業特權密碼庫的部署

2024年和2025年,監管機構指出憑證濫用問題及其與非法貿易和貸款詐騙案件的關聯。為此,美國和加拿大的銀行開始在其零信任架構中引入特權密碼庫。美國貨幣監理署(OCC)強制要求資產超過100億美元的金融機構為其所有管理員帳戶提供即時存取和會話日誌記錄。據CyberArk稱,2025年上半年68%的訂單是金融服務業升級到動態特權存取密碼庫的,該密碼庫每90分鐘輪換一次。預算不足以部署設備的中型銀行正在轉向基於雲端的特權存取解決方案,Delinea在2025年迅速擴展了這項功能。類似的監管要求也開始在歐洲和亞太地區出現,顯示全球正在產生連鎖反應。

歐盟 GDPR 和 NIS-2 監管要求正在推動企業範圍內的密碼審計和升級。

第二版《網路與資訊安全指令》(NIS-2)於2024年10月全面生效,並與《一般資料保護規範》(GDPR)共同強制要求歐洲公司清點其子公司和供應鏈合作夥伴的所有憑證。 2024年至2025年間,因密碼管理不善而產生的罰款總合高達12億歐元(13億美元),這使得密碼庫的實施成為比其他安全項目更為優先的事項。德國、法國和荷蘭在混合架構方面主導,這些架構將特權密碼保留在本地,同時將員工憑證路由到託管的雲端密碼庫。為歐洲客戶提供服務的非歐盟公司也需要遵守指令,而且全球需求不斷成長。

尤其是德語區(德國、奧地利和瑞士)的資料外洩事件引起了廣泛關注,並損害了用戶信任。

2022 年 LastPass 資料外洩事件揭露了加密的保險庫資料和未加密的元資料,導致德國、奧地利和瑞士的信任度長期下降。許多組織遷移到本地部署解決方案或 Bitwarden 等開放原始碼解決方案,理由是這些方案比專有加密方案更透明。 2024 年,德國聯邦資訊安全辦公室呼籲對供應商進行獨立評估。在供應商採用標準化加密和持續的第三方審計之前,德語區(德國、奧地利和瑞士)的謹慎態度可能會阻礙雲端技術的普及。

細分市場分析

特權密碼管理工具是成長最快的解決方案,預計到 2031 年將以 23.8% 的複合年成長率成長。另一方面,自助服務應用程式目前市場規模龐大,但成長速度較慢。銀行、醫療保健和公共部門的監管規定現在強制要求憑證輪調、存取日誌記錄和職責分離,但這些功能僅內建在特權管理平台中。網路保險合約條款也推動了這一轉變,因為依賴靜態電子表格的公司無法獲得優惠保費。

預計到2025年,自助服務工具將佔據46.5%的市場。儘管自助服務供應商不斷增強其企業級功能,但它們仍然容易受到消費者密碼金鑰趨勢的影響。混合辦公模式的普及正在引入新的終端並擴大密碼管理市場,但由於管理員帳戶的安全性至關重要,特權管理平台預計仍將繼續推動市場成長。

行動解決方案正經歷最強勁的成長勢頭,預計到 2031 年將成長 24.1%。同時,桌面用戶端在 2025 年仍將佔總支出的 38.1%。北歐模式表明,智慧型手機上的生物識別保險庫可以同時提升使用者體驗和合規性。隨著密碼儲存整合到 iCloud 鑰匙圈和 Windows Hello 中,獨立供應商面臨的競爭壓力日益增大,因此差異化的跨平台相容性至關重要。

密碼管理市場的成長主要得益於遠距辦公和5G連線的普及,這兩項技術能夠實現零延遲的即時憑證同步。桌上型電腦和筆記型電腦對於開發人員和分析師而言仍然至關重要,這也確保了多樣化的存取策略將成為主流。

區域分析

受零信任政策、網路保險合約要求以及成熟的雲端環境的推動,北美地區預計到2025年將佔全球收入的38.9%。美國銀行業迅速回應了美國貨幣監理署(OCC)的新指導意見,加拿大金融機構也採取了類似的整合模式。隨著企業採用率達到峰值,成長速度將逐漸放緩,市場關注將轉向中小企業。

預計到2031年,亞太地區將以24.13%的複合年成長率(CAGR)成為所有地區中成長最快的。政府推行的「雲端優先」策略、蓬勃發展的創業生態系統以及行動網際網路的廣泛應用,都在推動對跨平台資料儲存解決方案的需求。印度和東南亞的採用率成長最為迅猛,而日本和韓國則更著重於監管合規和員工流動性。

在歐洲,受GDPR和NIS-2等監管法規的壓力,穩健的混合部署正在穩步推進。 DACH地區(德國、奧地利、瑞士)市場依然保持謹慎,在LastPass事件後,更傾向於開放原始碼和自託管解決方案。在其他地區,俄羅斯以及中東和非洲部分地區的資料本地化法規正在促進本地供應商生態系統的發展,預計密碼管理市場將繼續保持其區域特色。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 零信任計畫正在加速北美銀行、金融服務和保險 (BFSI) 行業採用特權密碼庫。

- 歐盟 GDPR 和 NIS-2 監管要求正在促使企業進行全公司範圍的密碼審計和升級。

- SaaS 帶來的身份資訊激增,正在亞太地區的中型企業市場創造對跨平台資料儲存解決方案的需求。

- 員工流動性和自帶設備辦公室 (BYOD) 正在推動北歐國家採用行動優先的密碼管理器。

- 美國網路保險核保需要自動身分驗證憑證完整性認證

- RPA 和 DevOps 管道中對「API 優先」整合的需求正在推動金鑰管理的普及。

- 市場限制因素

- 尤其是在德語區(DACH),曾發生過一些備受矚目的資料外洩事件,損害了用戶信任(例如 LastPass 2022)。

- Paskey 和 FIDO2 的日益普及可望降低未來消費者領域的市場規模。

- 監管資料居住要求使 CloudVault 在中東的部署變得複雜。

- 長期存在為影子 IT 儲存密碼的做法,導致大型企業遷移成本不斷上升。

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監管和技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按解決方案類型

- 自助式密碼管理

- 特權使用者的密碼管理

- 訪問/技術類型

- 桌上型電腦和筆記型電腦

- 行動裝置

- 語音啟動密碼重置

- 瀏覽器擴充功能和網路保險庫

- 部署模式

- 雲端託管

- 現場

- 混合

- 按公司規模

- 大公司

- 中小企業

- 按最終用戶行業分類

- 銀行、金融服務和保險(BFSI)

- 醫療保健和生命科學

- 資訊科技/通訊

- 政府/公共部門

- 零售與電子商務

- 製造業

- 教育

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 澳洲

- 紐西蘭

- 其他亞太國家

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 肯亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- LastPass(GoTo)

- 1Password(AgileBits)

- Dashlane Inc.

- Keeper Security, Inc.

- Bitwarden, Inc.

- CyberArk Software Ltd.

- Delinea

- Microsoft Corporation

- IBM Corporation

- Apple Inc.

- Broadcom(CA Technologies)

- Okta Inc.

- SailPoint Technologies, Inc.

- Quest Software Inc.

- Hitachi ID Systems

- FastPassCorp A/S

- Avatier

- Trend Micro Incorporated

- Ivanti

- HashiCorp

- Thycotic

- BeyondTrust Corporation

- EmpowerID, Inc.

- Intuitive Security Systems Pty. Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the password management market size is projected to expand from USD 2.41 billion in 2025 and USD 2.94 billion in 2026 to USD 8.07 billion by 2031, registering a CAGR of 22.39% between 2026 to 2031.

This report is Segmented by Solution Type (Self-Service, and Privileged User), Access / Technology Type (Desktop and Laptop, and More), Deployment Mode (Cloud-Hosted, On-Premises, and Hybrid), Enterprise Size (Large, and SMEs), End-User Vertical (BFSI, Healthcare, and More), and Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Password Management Market Trends and Insights

Zero-Trust Programs Accelerating Privileged Password Vault Deployments in North American BFSI

Regulators linked credential misuse to unauthorized trading and loan-fraud incidents in 2024 and 2025, prompting United States and Canadian banks to embed privileged vaults into zero-trust architectures. The Office of the Comptroller of the Currency required institutions with assets above USD 10 billion to provide just-in-time access and session recording for every administrative account. CyberArk noted that 68% of its first-half 2025 bookings came from financial-services upgrades to dynamic privileged access management vaults that rotate passwords every 90 minutes. Mid-tier banks lacking appliance budgets turned to cloud-delivered privileged access, a capability rapidly expanded by Delinea in 2025. Similar mandates are emerging in Europe and the Asia Pacific, indicating global spillover.

EU GDPR and NIS-2 Mandates Triggering Enterprise-Wide Password Audits and Upgrades

The Network and Information Security Directive 2 entered full force in October 2024 and, together with GDPR, compelled European firms to inventory every credential across subsidiaries and supply-chain partners. Fines linked to weak password hygiene totaled EUR 1.2 billion (USD 1.3 billion) over 2024-2025 and elevated password vault roll-outs above other security projects. Germany, France and the Netherlands spearheaded hybrid architectures that keep privileged passwords on-premises while routing employee credentials to managed cloud vaults. Non-EU corporations serving European customers must also comply, broadening global demand.

High-Profile Breaches Undermining User Trust, Especially in DACH Region

The 2022 LastPass breach revealed encrypted vault data and unencrypted metadata, triggering a lingering trust deficit across Germany, Austria and Switzerland. Many organizations pivoted to on-premises or open-source options such as Bitwarden, citing transparency advantages over proprietary encryption. Germany's Federal Office for Information Security urged independent vendor assessments in 2024. Until vendors embrace standardized encryption and continuous third-party audits, caution in the DACH region will restrain cloud adoption.

Other drivers and restraints analyzed in the detailed report include:

- Surge in SaaS Identity Sprawl Creating Demand for Cross-Platform Vaults in Asia Pacific Mid-Market

- API-First Integration Needs for RPA and DevOps Pipelines Fueling Secrets-Management Adoption

- Rising Adoption of Passkeys and FIDO2 Reducing Future TAM in Consumer Segment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Privileged password tools represented the fastest-growing solution, advancing at a 23.8% CAGR through 2031, while self-service applications, although larger today, face growth deceleration. Banking, healthcare, and public-sector mandates now require credential rotation, access logging, and separation of duties, capabilities embedded only in privileged platforms. Cyber-insurance clauses reinforce the shift by denying favorable premiums to firms that rely on static spreadsheets.

Self-service tools held a 46.5% market share in 2025. Self-service vendors continue to enhance enterprise features, yet remain susceptible to the consumer shift toward passkeys. Hybrid work introduces new endpoints and expands the password management market, but the security premium associated with administrative accounts ensures that privileged vaults continue to drive growth.

Mobile solutions hold the strongest tailwind, forecast to rise at 24.1% to 2031, whereas desk-based clients maintain 38.1% of 2025 spending. The Nordic model has demonstrated that biometric-enabled vaults on smartphones can improve both user experience and compliance simultaneously. iCloud Keychain and Windows Hello now incorporate passkey storage, intensifying competitive pressure on independent vendors and making differentiated cross-platform support mandatory.

Growth in the password management market stems from remote work and 5G connectivity that allow real-time credential sync without latency. Desktops and laptops remain indispensable for developers and analysts, ensuring multipronged access strategies prevail.

Complete Report Scope:

- By Solution Type

- Self-Service Password Management

- Privileged User Password Management

- By Access/Technology Type

- Desktop and Laptop

- Mobile Devices

- Voice-Enabled Password Reset

- Browser Extensions and Web Vaults

- By Deployment Mode

- Cloud-Hosted

- On-Premises

- Hybrid

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By End-User Vertical

- Banking, Financial Services and Insurance (BFSI)

- Healthcare and Life Sciences

- IT and Telecommunications

- Government and Public Sector

- Retail and E-Commerce

- Manufacturing

- Education

- Other End-User Verticals

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Rest of Asia Pacific

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- North America

Geography Analysis

North America contributed 38.9% of 2025 revenue, propelled by zero-trust mandates, cyber-insurance terms, and a mature cloud landscape. United States banks responded swiftly to the new OCC guidance, while Canadian institutions followed a similar pattern of integration. Growth will gradually moderate as enterprise penetration peaks, and attention shifts to small and medium-sized organizations.

The Asia Pacific is projected to post the fastest regional CAGR of 24.13% through 2031. Cloud-first government projects, a vibrant startup ecosystem, and widespread mobile internet drive demand for cross-platform vaults. India and Southeast Asia exhibit the sharpest adoption curves, while Japan and South Korea focus on regulatory compliance and workforce mobility.

Europe demonstrates robust hybrid deployments under the pressures of GDPR and NIS-2. DACH markets remain cautious, favoring open-source or self-hosted solutions in the wake of the LastPass incident. Elsewhere, regulations on data localization in Russia and parts of the Middle East and Africa are fostering local vendor ecosystems, ensuring the password management market retains regional nuances.

- LastPass (GoTo)

- 1Password (AgileBits)

- Dashlane Inc.

- Keeper Security, Inc.

- Bitwarden, Inc.

- CyberArk Software Ltd.

- Delinea

- Microsoft Corporation

- IBM Corporation

- Apple Inc.

- Broadcom (CA Technologies)

- Okta Inc.

- SailPoint Technologies, Inc.

- Quest Software Inc.

- Hitachi ID Systems

- FastPassCorp A/S

- Avatier

- Trend Micro Incorporated

- Ivanti

- HashiCorp

- Thycotic

- BeyondTrust Corporation

- EmpowerID, Inc.

- Intuitive Security Systems Pty. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Zero-Trust Programs Accelerating Privileged Password Vault Deployments in North American BFSI

- 4.2.2 EU GDPR and NIS-2 Mandates Triggering Enterprise-wide Password Audits and Upgrades

- 4.2.3 Surge in SaaS Identity Sprawl Creating Demand for Cross-Platform Vaults in Asia Pacific Mid-Market

- 4.2.4 Workforce Mobility and BYOD Driving Mobile-First Password Managers in Nordics

- 4.2.5 Cyber-Insurance Underwriting Requiring Automated Credential Hygiene Proof in United States

- 4.2.6 API-First Integration Needs for RPA and DevOps Pipelines Fueling Secrets Management Adoption

- 4.3 Market Restraints

- 4.3.1 High-Profile Breaches (e.g., LastPass 2022) Undermining User Trust, Especially in DACH Region

- 4.3.2 Rising Adoption of Passkeys/FIDO2 Reducing Future TAM in Consumer Segment

- 4.3.3 Regulatory Data-Residency Rules Complicating Cloud Vault Roll-Outs in Middle East

- 4.3.4 Persistent Shadow-IT Password Stores Inflating Migration Costs for Large Enterprises

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory and Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Solution Type

- 5.1.1 Self-Service Password Management

- 5.1.2 Privileged User Password Management

- 5.2 By Access/Technology Type

- 5.2.1 Desktop and Laptop

- 5.2.2 Mobile Devices

- 5.2.3 Voice-Enabled Password Reset

- 5.2.4 Browser Extensions and Web Vaults

- 5.3 By Deployment Mode

- 5.3.1 Cloud-Hosted

- 5.3.2 On-Premises

- 5.3.3 Hybrid

- 5.4 By Enterprise Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises (SMEs)

- 5.5 By End-User Vertical

- 5.5.1 Banking, Financial Services and Insurance (BFSI)

- 5.5.2 Healthcare and Life Sciences

- 5.5.3 IT and Telecommunications

- 5.5.4 Government and Public Sector

- 5.5.5 Retail and E-Commerce

- 5.5.6 Manufacturing

- 5.5.7 Education

- 5.5.8 Other End-User Verticals

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.4.5 Australia

- 5.6.4.6 New Zealand

- 5.6.4.7 Rest of Asia Pacific

- 5.6.5 Middle East

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Kenya

- 5.6.6.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 LastPass (GoTo)

- 6.4.2 1Password (AgileBits)

- 6.4.3 Dashlane Inc.

- 6.4.4 Keeper Security, Inc.

- 6.4.5 Bitwarden, Inc.

- 6.4.6 CyberArk Software Ltd.

- 6.4.7 Delinea

- 6.4.8 Microsoft Corporation

- 6.4.9 IBM Corporation

- 6.4.10 Apple Inc.

- 6.4.11 Broadcom (CA Technologies)

- 6.4.12 Okta Inc.

- 6.4.13 SailPoint Technologies, Inc.

- 6.4.14 Quest Software Inc.

- 6.4.15 Hitachi ID Systems

- 6.4.16 FastPassCorp A/S

- 6.4.17 Avatier

- 6.4.18 Trend Micro Incorporated

- 6.4.19 Ivanti

- 6.4.20 HashiCorp

- 6.4.21 Thycotic

- 6.4.22 BeyondTrust Corporation

- 6.4.23 EmpowerID, Inc.

- 6.4.24 Intuitive Security Systems Pty. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

全球密碼管理軟體市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球密碼管理軟體市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 密碼管理器市場 - 全球產業規模、佔有率、趨勢、機會、預測:按解決方案類型、技術類型、最終用戶供應商、地區和競爭對手分類,2021-2031 年

密碼管理器市場 - 全球產業規模、佔有率、趨勢、機會、預測:按解決方案類型、技術類型、最終用戶供應商、地區和競爭對手分類,2021-2031 年 密碼管理市場報告:按類型、存取權限、部署模式、最終用戶、行業和地區分類(2026-2034 年)

密碼管理市場報告:按類型、存取權限、部署模式、最終用戶、行業和地區分類(2026-2034 年) 2026年全球密碼管理器市場報告

2026年全球密碼管理器市場報告 密碼管理軟體市場規模、佔有率和成長分析:按部署類型、使用者類型、功能、定價模式和地區分類 - 2026-2033 年產業預測

密碼管理軟體市場規模、佔有率和成長分析:按部署類型、使用者類型、功能、定價模式和地區分類 - 2026-2033 年產業預測 密碼管理市場分析及預測(至2035年):依類型、產品類型、服務、技術、元件、應用、部署類型、最終使用者及功能分類全球密碼管理市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析以及未來預測(2026-2034 年)

密碼管理市場分析及預測(至2035年):依類型、產品類型、服務、技術、元件、應用、部署類型、最終使用者及功能分類全球密碼管理市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析以及未來預測(2026-2034 年) 密碼管理市場規模、佔有率和成長分析(按類型、存取類型、部署類型、企業規模、應用程式、最終用戶和地區分類)-2026-2033年產業預測

密碼管理市場規模、佔有率和成長分析(按類型、存取類型、部署類型、企業規模、應用程式、最終用戶和地區分類)-2026-2033年產業預測 密碼管理:全球市場佔有率和排名、總收入和需求預測(2025-2031 年)

密碼管理:全球市場佔有率和排名、總收入和需求預測(2025-2031 年) 全球密碼管理器市場

全球密碼管理器市場