|

市場調查報告書

商品編碼

2072458

歐洲下一代儲存:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Europe Next Generation Storage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

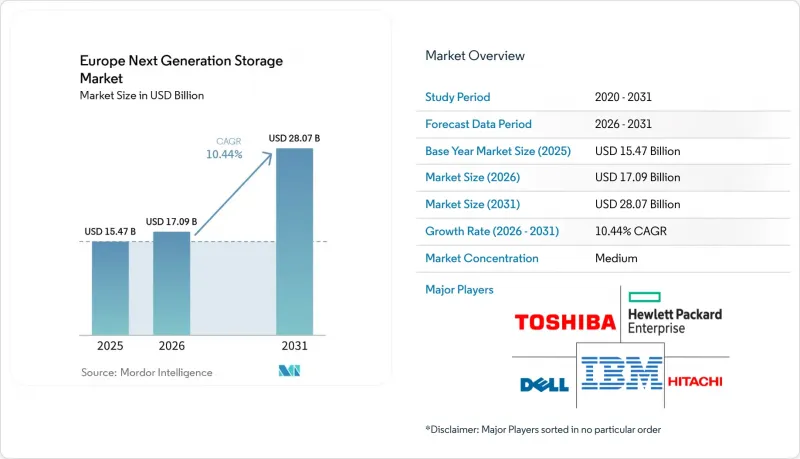

據 Mordor Intelligence 稱,2025 年歐洲下一代儲存市場價值為 154.7 億美元,預計到 2031 年將達到 280.7 億美元,而 2026 年為 170.9 億美元,預測期(2026-2031 年)的複合年成長率為 10.44%。

本報告按儲存系統(直接附加儲存(DAS)、網路附加儲存 (NAS) 等)、儲存架構(檔案儲存、物件式儲存、區塊儲存等)、記憶體和媒體類型(硬碟 (HDD)、 NAND快閃記憶體等)、終端使用者產業(銀行、金融服務和保險 (BFSI)、零售和電子商務等)以及國家/地區進行細分。市場預測以美元 (USD) 為單位。

歐洲下一代儲存市場的趨勢與洞察

數位資料量正呈指數級成長。

預計2023年至2028年間,全球資料產生量將成長三倍,而根據GDPR的本地資料保留要求,新增資料的大部分必須儲存在歐盟境內。因此,計劃部署Petabyte容量的企業正在採用混合拓撲結構,將本地陣列與自主雲端擴展能力結合,以確保合規性並保持低延遲。支出趨勢顯示,企業正大幅轉向可擴展的軟體定義平台,這些平台能夠適應各種文件和物件工作負載,且無需擔心廠商鎖定。因此,隨著企業力求在單一架構中平衡合規性和效能,歐洲下一代儲存市場的擴張速度已超過全球平均水準。

快速過渡到 SSD 和 NVMe 架構

企業採用 PCIe Gen5 NVMe 正在縮小曾經將本地陣列與公共雲端開來的效能差距。德國的製造工廠積極擁抱工業 4.0,將延遲容差控制在 100 微秒以下,閾值。如今,能源效率已成為電路板層面的關鍵指標。固態硬碟 (SSD) 每Terabyte的功耗遠低於機械硬碟 (HDD),這有助於營運商滿足德國 2027 年《能源效率法》中關於資料中心 50% 使用可再生能源的要求。這些趨勢意味著,在歐洲下一代儲存產業中,快閃記憶體媒體正被視為戰術性投資,而非戰術選擇。

全快閃記憶體和NVMe陣列的初始投資成本較高

企業級固態硬碟 (SSD) 的單位容量價格仍比機械硬碟 (HDD) 高出 9.9 倍。對於中小企業 (SME) 而言,即使考慮到快閃記憶體帶來的節能優勢,這種價格差異也會使投資報酬率 (ROI) 的計算變得複雜。雖然超大規模資料中心業者的採用在短期內降低了價格,但許多歐洲中小企業仍將繼續逐步將其工作負載遷移到 QLC 快閃記憶體和高容量硬碟結合的混合配置,直到快閃記憶體的每位元成本降至閾值以下。

細分市場分析

預計到2025年,直接附加儲存(DAS)將佔歐洲下一代儲存市場規模的45.02%,凸顯了企業對關鍵業務工作負載可預測延遲的重視。同時,超融合融合式基礎架構(HCI)預計將以11.18%的複合年成長率成長,反映出市場對將運算、儲存和網路整合到單一策略域中的橫向擴展節點的需求。

德國的國家數位化津貼正在推動超融合技術的發展,該計畫要求製造商在不違反主權法規的前提下,進行現場處理以分析感測器數據。戴爾科技和CoreWeave的機架級人工智慧平台已證明,整合資源與Petabyte級快閃記憶體結合,可提供1.4 exaFLOPS的運算能力,使其成為介於單晶片陣列和純公共雲端之間的理想選擇。

到2025年,物件式的儲存將佔據歐洲下一代儲存市場65.05%的佔有率,為從分析日誌到8K媒體檔案等各種非結構化資料集提供RESTful、可橫向擴展的儲存庫。軟體定義儲存(SDS)正以11.74%的複合年成長率快速成長,因為它透過將服務與硬體解耦,滿足了「資料法」的可攜性原則。

歐洲的銀行和保險公司正在試行一種資料遷移協調器,該協調器能夠在主權雲端合作夥伴之間即時遷移Petabyte級資料集,而不會中斷交易。與Hitachi Vantara和Hammerspace等公司的夥伴關係,實現了自動化分類和遷移,同時保持元資料的完整性,最大限度地減少了重構舊有應用程式所帶來的負擔。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 數位資料的爆炸性成長

- 快速過渡到 SSD 和 NVMe 架構

- 需要超低延遲的 AI/ML 工作負載

- 歐盟企業採用混合多重雲端

- 邊緣運算和5G微型資料中心的普及

- 透過歐盟的 Gaia-X 和資料法實現主權雲端儲存。

- 市場限制因素

- 全快閃記憶體和NVMe陣列的初始部署成本較高

- 歐盟資料主權合規方面的碎片化

- 傳統工作負載遷移和供應商鎖定風險

- NAND/SSD中稀土元素和關鍵金屬的供應限制

- 價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 評估宏觀經濟趨勢對市場的影響

第5章 市場規模與成長預測

- 儲存系統

- 直接附加儲存(DAS)

- 網路附加儲存 (NAS)

- 儲存區域網路(SAN)

- 融合式基礎架構(HCI)

- 其他

- 儲存架構

- 文件類型和物件類型存儲

- 區塊儲存

- 軟體定義儲存 (SDS)

- 按記憶體和媒體類型分類

- 硬碟機(HDD)

- NAND快閃記憶體

- NVMe

- 3D XPoint/Optane

- 新興的非揮發性記憶

- 按最終用戶行業分類

- BFSI

- 零售與電子商務

- 資訊科技/通訊

- 醫療保健和生命科學

- 媒體與娛樂

- 政府/國防

- 其他終端用戶產業

- 國家

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Dell Technologies

- Hewlett Packard Enterprise(HPE)

- NetApp

- Hitachi Vantara

- IBM

- Toshiba

- Pure Storage

- DataDirect Networks(DDN)

- Scality

- Fujitsu

- Netgear

- Huawei Technologies

- Samsung Electronics

- Western Digital

- Seagate Technology

- Micron Technology

- Lenovo

- Cisco Systems

- Oracle

- VAST Data

第7章 市場機會與未來展望

According to Mordor Intelligence, the europe next generation storage market size was valued at USD 15.47 billion in 2025 and estimated to grow from USD 17.09 billion in 2026 to reach USD 28.07 billion by 2031, at a CAGR of 10.44% during the forecast period (2026-2031).

This report is Segmented by Storage System (Direct-Attached Storage (DAS), Network-Attached Storage (NAS), and More), Storage Architecture (File and Object-Based Storage, Block Storage, and More), Memory and Media Type (Hard Disk Drive (HDD), NAND Flash, and More), End-User Industry (BFSI, Retail and E-Commerce, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

Europe Next Generation Storage Market Trends and Insights

Exploding Volume of Digital Data

Global data creation is set to triple between 2023 and 2028, and local retention obligations under GDPR mean most of that growth must be stored inside EU borders. Enterprises planning for petabyte-scale capacity are therefore deploying hybrid topologies that couple on-premises arrays with sovereign-cloud extensions, ensuring compliance while keeping latency in check. Spending patterns show a marked tilt toward scalable, software-defined platforms that can ingest diverse file and object workloads without vendor lock-in. The result is a Europe next generation storage market whose expansion rate outpaces global averages as organizations attempt to blend compliance and performance within a single architecture.

Rapid Shift to SSD and NVMe Architectures

Enterprise adoption of PCIe Gen5 NVMe is eliminating the performance gap that once separated on-premises arrays from public-cloud tiers. German manufacturing plants embracing Industry 4.0 have pushed latency budgets below 100 µs, a threshold unattainable for spinning disks. Energy efficiency is now a board-level metric; SSDs consume markedly fewer kilowatt-hours per terabyte than HDDs, helping operators meet the German Energy Efficiency Act's 50% renewable-energy threshold for data centres set for 2027. These dynamics position flash media as a strategic rather than tactical investment across the Europe next generation storage industry.

High Capital Cost of All-Flash and NVMe Arrays

Enterprise SSDs still carry a unit-cost premium as high as 9.9X over HDD capacity. For small and midsize firms, this delta complicates ROI calculations even when flash energy savings are factored in. Hyperscaler uptake is driving near-term price easing, but many European SMEs will continue staging workloads on hybrid tiers that mix QLC flash with high-capacity disk until flash crosses the cost-per-bit threshold.

Other drivers and restraints analyzed in the detailed report include:

- AI / ML Workloads Demanding Ultra-Low Latency

- Hybrid Multi-Cloud Adoption Across EU Enterprises

- Data-Sovereignty Compliance Fragmentation Across EU

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Direct-Attached Storage contributed 45.02% share to Europe next generation storage market size in 2025, underscoring enterprises' preference for predictable latency in mission-critical workloads. Hyper-Converged Infrastructure, however, is forecast to log an 11.18% CAGR, reflecting appetite for scale-out nodes that blend compute, storage and networking into a single policy domain.

Momentum toward hyperconvergence is reinforced by national digitalisation grants in Germany, where manufacturers need on-site processing to analyse sensor data without violating sovereignty rules. Dell Technologies and CoreWeave's rack-level AI platform demonstrates how converged resources can supply 1.4 exaFLOPS alongside petabyte-scale flash, making them an attractive middle ground between monolithic arrays and purely public-cloud tiers.

File and Object-Based Storage captured 65.05% of Europe next generation storage market share in 2025 by delivering RESTful, scale-out repositories for unstructured datasets, from analytics logs to 8K media files. Software-Defined Storage is scaling faster at 11.74% CAGR because it uncouples services from hardware, thereby fulfilling the Data Act's portability ethos.

European banks and insurers are piloting data-mobility orchestrators capable of live-migrating petabyte datasets between sovereign-cloud partners without disrupting transaction latency. Partnerships such as Hitachi Vantara and Hammerspace provide automated classification and movement that preserve metadata integrity, minimizing refactoring pain for legacy apps.

Complete Report Scope:

- By Storage System

- Direct-Attached Storage (DAS)

- Network-Attached Storage (NAS)

- Storage Area Network (SAN)

- Hyper-Converged Infrastructure (HCI)

- Others

- By Storage Architecture

- File and Object-Based Storage

- Block Storage

- Software-Defined Storage (SDS)

- By Memory and Media Type

- Hard Disk Drive (HDD)

- NAND Flash

- NVMe

- 3D XPoint / Optane

- Emerging NVM

- By End-User Industry

- BFSI

- Retail and e-Commerce

- IT and Telecom

- Healthcare and Life Sciences

- Media and Entertainment

- Government and Defence

- Other End-User Industries

- By Country

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

List of Companies Covered in this Report:

- Dell Technologies

- Hewlett Packard Enterprise (HPE)

- NetApp

- Hitachi Vantara

- IBM

- Toshiba

- Pure Storage

- DataDirect Networks (DDN)

- Scality

- Fujitsu

- Netgear

- Huawei Technologies

- Samsung Electronics

- Western Digital

- Seagate Technology

- Micron Technology

- Lenovo

- Cisco Systems

- Oracle

- VAST Data

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Exploding volume of digital data

- 4.2.2 Rapid shift to SSD and NVMe architectures

- 4.2.3 AI / ML workloads demanding ultra-low latency

- 4.2.4 Hybrid multi-cloud adoption across EU enterprises

- 4.2.5 Edge-computing and 5G micro-data-centre proliferation

- 4.2.6 EU Gaia-X and Data Act enabling sovereign-cloud storage

- 4.3 Market Restraints

- 4.3.1 High capital cost of all-flash and NVMe arrays

- 4.3.2 Data-sovereignty compliance fragmentation across EU

- 4.3.3 Legacy workload migration and vendor lock-in risks

- 4.3.4 Rare-earth and critical-metal supply constraints for NAND/SSD

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of the Impact of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Storage System

- 5.1.1 Direct-Attached Storage (DAS)

- 5.1.2 Network-Attached Storage (NAS)

- 5.1.3 Storage Area Network (SAN)

- 5.1.4 Hyper-Converged Infrastructure (HCI)

- 5.1.5 Others

- 5.2 By Storage Architecture

- 5.2.1 File and Object-Based Storage

- 5.2.2 Block Storage

- 5.2.3 Software-Defined Storage (SDS)

- 5.3 By Memory and Media Type

- 5.3.1 Hard Disk Drive (HDD)

- 5.3.2 NAND Flash

- 5.3.3 NVMe

- 5.3.4 3D XPoint / Optane

- 5.3.5 Emerging NVM

- 5.4 By End-User Industry

- 5.4.1 BFSI

- 5.4.2 Retail and e-Commerce

- 5.4.3 IT and Telecom

- 5.4.4 Healthcare and Life Sciences

- 5.4.5 Media and Entertainment

- 5.4.6 Government and Defence

- 5.4.7 Other End-User Industries

- 5.5 By Country

- 5.5.1 Germany

- 5.5.2 United Kingdom

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Dell Technologies

- 6.4.2 Hewlett Packard Enterprise (HPE)

- 6.4.3 NetApp

- 6.4.4 Hitachi Vantara

- 6.4.5 IBM

- 6.4.6 Toshiba

- 6.4.7 Pure Storage

- 6.4.8 DataDirect Networks (DDN)

- 6.4.9 Scality

- 6.4.10 Fujitsu

- 6.4.11 Netgear

- 6.4.12 Huawei Technologies

- 6.4.13 Samsung Electronics

- 6.4.14 Western Digital

- 6.4.15 Seagate Technology

- 6.4.16 Micron Technology

- 6.4.17 Lenovo

- 6.4.18 Cisco Systems

- 6.4.19 Oracle

- 6.4.20 VAST Data

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

全球新一代資料儲存市場(至 2032 年):按儲存系統(直接附加儲存、網路附加儲存)、儲存媒體(硬碟、固態磁碟機)和儲存架構(基於檔案的儲存、基於物件的儲存)分類

全球新一代資料儲存市場(至 2032 年):按儲存系統(直接附加儲存、網路附加儲存)、儲存媒體(硬碟、固態磁碟機)和儲存架構(基於檔案的儲存、基於物件的儲存)分類 下一代資料儲存市場:按類型、架構、儲存媒體、部署模式、產業和地區分類

下一代資料儲存市場:按類型、架構、儲存媒體、部署模式、產業和地區分類 2026-2030年全球人工智慧最佳化儲存市場

2026-2030年全球人工智慧最佳化儲存市場 新一代資料儲存市場:2026-2032年全球市場預測(按儲存媒體、儲存架構、服務類型、部署模式、應用程式和最終用戶產業分類)

新一代資料儲存市場:2026-2032年全球市場預測(按儲存媒體、儲存架構、服務類型、部署模式、應用程式和最終用戶產業分類) 2026年全球天基資料記錄市場報告2026年全球下一代資料儲存市場報告

2026年全球天基資料記錄市場報告2026年全球下一代資料儲存市場報告 全像資料儲存市場機會、成長要素、產業趨勢分析及2026-2035年預測

全像資料儲存市場機會、成長要素、產業趨勢分析及2026-2035年預測 新一代資料儲存市場:依儲存類型(DAS、NAS、SAN)、儲存媒體、架構、最終用戶(銀行、金融服務和保險(BFSI)、零售、醫療保健、製造業、政府、IT 和電信、其他最終用戶)和地區劃分 - 至2027年的全球預測

新一代資料儲存市場:依儲存類型(DAS、NAS、SAN)、儲存媒體、架構、最終用戶(銀行、金融服務和保險(BFSI)、零售、醫療保健、製造業、政府、IT 和電信、其他最終用戶)和地區劃分 - 至2027年的全球預測 新一代資料儲存技術市場-全球產業規模、佔有率、趨勢、機會與預測:按類型、解決方案、記憶體、地區和競爭格局分類,2021-2031年

新一代資料儲存技術市場-全球產業規模、佔有率、趨勢、機會與預測:按類型、解決方案、記憶體、地區和競爭格局分類,2021-2031年 下一代資料儲存市場規模、佔有率和成長分析(按儲存系統、儲存媒體和地區分類)—產業預測(2026-2033 年)

下一代資料儲存市場規模、佔有率和成長分析(按儲存系統、儲存媒體和地區分類)—產業預測(2026-2033 年)