|

市場調查報告書

商品編碼

1982291

全像資料儲存市場機會、成長要素、產業趨勢分析及2026-2035年預測Holographic Data Storage Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

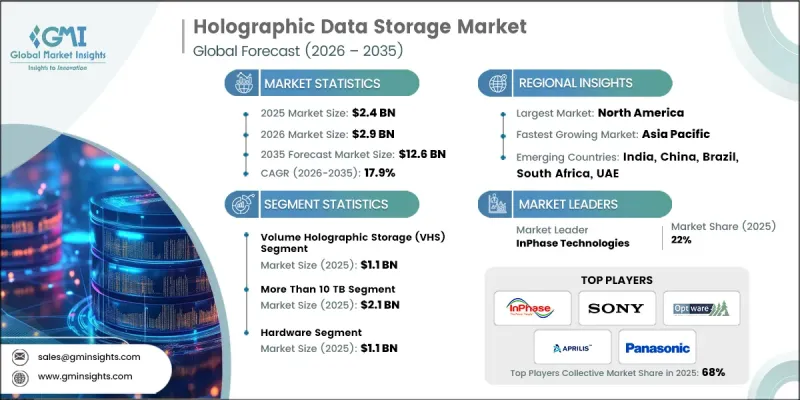

全球全像資料儲存市場預計到 2025 年將達到 24 億美元,並有望以 17.9% 的複合年成長率成長,到 2035 年將達到 126 億美元。

隨著各組織機構對密度和擴充性遠超傳統系統的儲存技術的需求日益成長,全像資料儲存產業正蓬勃發展。雲端運算和資料密集型應用的普及推動了數位資訊的成長,進而加速了對下一代儲存平台的需求。企業和機構越來越重視安全、長期的歸檔解決方案,以確保資料的長期持久性和完整性。對快速數據存取和高速處理能力的日益成長的需求進一步推動了市場對全像儲存技術的應用。需要安全、高容量環境的產業正在轉向全像系統來管理複雜的數位工作負載。全像儲存能夠處理指數級成長的數據,同時支援高效的搜尋,這使其在現代數位基礎設施中確立了變革性解決方案的地位。隨著傳統儲存技術逐漸接近其物理和效能極限,全像資料儲存正成為建構高密度、面向未來的儲存生態系統的理想替代方案。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 24億美元 |

| 預測金額 | 126億美元 |

| 複合年成長率 | 17.9% |

全像資料儲存的關鍵優勢在於其能夠將資訊記錄在整個儲存媒體的體積內,而不僅限於表面層。這種體積式儲存方法顯著提高了儲存密度,並提升了平行資料搜尋效能。公共和私營研究機構正在探索超越傳統磁碟系統的先進儲存框架,以滿足未來資料環境的需求。這種對持續創新的投入凸顯了該技術在應對快速擴展的數位生態系統所帶來的擴展性挑戰方面的潛力。隨著資料基礎設施日益複雜,各機構正在投資於能夠提供持久性、高效性和長期可擴展性的先進儲存方案。

預計2025年,體積全像儲存(VHS)市場規模將達到11億美元。 VHS技術的優點在於能夠將資料嵌入到記錄媒體的整個深度,從而實現超高密度儲存和高效的平行資料處理。企業和機構對安全、耐用且節省空間的歸檔系統的需求日益成長,正在加速VHS技術的普及應用。 VHS能夠在保持資料完整性的同時減少實體儲存空間,這是其主要吸引力之一。製造商正被敦促透過提高光敏聚合物材料的耐久性並最佳化讀寫精度,來鞏固VHS作為傳統歸檔技術競爭性替代方案的地位。

到2025年,容量超過10TB的市場規模將達到21億美元。這項市場需求主要由大規模數位基礎設施驅動,這些基礎設施需要超高容量解決方案,以安全地長期儲存資料。隨著人們對節能型歸檔系統的日益關注,對能夠降低營運成本並最大限度減少基礎設施面積的高容量全像平台的投資正在加速成長。建議產業相關人員專注於可擴展的系統結構,並與大規模相關人員建立策略合作夥伴關係,以加速關鍵任務型超高容量全像儲存解決方案的商業化進程。

預計到2025年,北美全像資料儲存市場佔有率將達到34.3%。該地區的主導地位得益於其強大的研發環境、先進的數位基礎設施以及對新興儲存技術的早期應用。持續推動的數位轉型措施以及對節能型歸檔框架日益成長的重視,將持續刺激市場需求。隨著大規模資料操作的擴展,全像儲存正日益被視為建構彈性可擴展數位生態系統的戰略要素。我們鼓勵企業深化研究合作,並根據機構需求客製化產品開發,以最大限度地掌握該地區的成長機會。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 與傳統儲存解決方案相比,資料儲存密度和容量更高

- 雲端運算和巨量資料應用的快速成長

- 安全、長期檔案儲存的需求日益成長

- 高速資料搜尋和處理的需求日益成長。

- 在國防、醫療和多媒體產業的應用日益廣泛。

- 陷阱與挑戰

- 實施和維護高成本

- 將技術與現有IT基礎設施整合的複雜性

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 新興經營模式

- 合規要求

- 供應鏈韌性

- 地緣政治分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 市場集中度分析

- 按地區

- 主要企業的競爭標竿分析

- 產品系列比較

- 產品線

- 科技

- 創新

- 區域部署對比

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 產品系列比較

- 2022-2025 年重大發展

- 併購

- 夥伴關係和聯盟

- 技術進步

- 業務拓展與投資策略

- 永續發展計劃

- 數位轉型計劃

- 新興/Start-Ups競爭對手的發展趨勢

第5章 市場估計與預測:依技術分類,2022-2035年

- 體積全像儲存(VHS)

- 表面全像儲存(SHS)

- 混合全像存儲

第6章 市場估算與預測:依儲存容量分類,2022-2035年

- 小於1TB

- 1 TB~10 TB

- 超過10TB

第7章 市場估計與預測:依組件分類,2022-2035年

- 硬體

- 軟體

- 服務

第8章 市場估算與預測:依材料分類,2022-2035年

- 主要趨勢

- 光聚合物

- 屈光晶體

- 矽基存儲

- 聚合物薄膜

第9章 市場估計與預測:依應用領域分類,2022-2035年

- 企業資料儲存與資料中心

- 歸檔儲存和備份

- 即時高容量數據訪問

- 重要且安全的存儲

- 其他

第10章 市場估價與預測:依最終用戶產業分類,2022-2035年

- 主要趨勢

- 資訊科技/通訊

- 銀行、金融和保險(BFSI)

- 衛生保健

- 媒體與娛樂

- 政府

- 國防/航太

- 其他(教育機構、研究機構等)

第11章 市場估價與預測:按地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第12章:公司簡介

- 主要企業

- Sony Corporation

- Panasonic Holdings Corporation

- Samsung Electronics

- Hitachi, Ltd.

- IBM Corporation

- Microsoft Corporation

- Intel Corporation

- Toshiba Corporation

- 按地區分類的主要企業

- 北美洲

- Western Digital Corporation

- Seagate Technology

- InPhase Technologies

- Optware Corporation

- Aprilis Inc.

- 歐洲

- Holographic Versatile Disc(HVD)Alliance

- 亞太地區

- Fujifilm Holdings Corporation

- 北美洲

- 小眾/顛覆者

- Akonia Holographics

- Zebra Imaging

The Global Holographic Data Storage Market was valued at USD 2.4 billion in 2025 and is estimated to grow at a CAGR of 17.9% to reach USD 12.6 billion by 2035.

The holographic data storage industry is gaining strong momentum as organizations seek storage technologies capable of delivering exceptional density and scalability beyond conventional systems. Growing volumes of digital information, fueled by cloud computing expansion and data-intensive applications, are accelerating the need for next-generation storage platforms. Enterprises and institutions are increasingly prioritizing secure, long-term archival solutions that ensure durability and data integrity over extended periods. Rising demand for rapid data access and high-speed processing capabilities is further strengthening market adoption. Industries requiring secure, high-capacity environments are turning to holographic systems to manage complex digital workloads. The ability of holographic storage to handle exponential data growth while supporting efficient retrieval positions as a transformative solution in modern digital infrastructure. As traditional storage technologies approach physical and performance limitations, holographic data storage is emerging as a compelling alternative for high-density, future-ready storage ecosystems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.4 Billion |

| Forecast Value | $12.6 Billion |

| CAGR | 17.9% |

A defining strength of holographic data storage lies in its capacity to record information throughout the full volume of the storage medium rather than restricting it to surface-level layers. This volumetric approach enables dramatically higher storage densities and enhances parallel data retrieval performance. Public and private research bodies are exploring advanced storage frameworks that move beyond conventional disk-based systems to support future data environments. Continuous innovation efforts highlight the technology's potential to address the scaling challenges associated with rapidly expanding digital ecosystems. As data infrastructure grows in complexity, institutions are investing in advanced storage paradigms capable of delivering endurance, efficiency, and long-term scalability.

The volume holographic storage (VHS) segment generated USD 1.1 billion in 2025. VHS technology stands out due to its capability to embed data across the entire depth of the recording material, enabling ultra-high storage density and efficient parallel data processing. Growing requirements for secure, durable, and space-efficient archival systems are accelerating VHS adoption across enterprise and institutional environments. Its ability to maintain data integrity while reducing physical storage space enhances its appeal. Manufacturers are encouraged to improve photopolymer material durability and optimize read/write precision to strengthen VHS positioning as a competitive alternative to legacy archival technologies.

The more than 10 TB capacity segment accounted for USD 2.1 billion in 2025. Demand within this segment is driven by large-scale digital infrastructures that require ultra-high-capacity solutions capable of preserving data securely over extended durations. Increasing emphasis on energy-efficient archival systems is accelerating investment in high-capacity holographic platforms that lower operational costs and minimize infrastructure footprints. Industry participants are advised to focus on scalable system architectures and strategic collaborations with large institutional stakeholders to accelerate the commercialization of mission-critical, ultra-high-capacity holographic storage solutions.

North America Holographic Data Storage Market held a 34.3% share in 2025. Regional leadership is supported by a strong research and innovation environment, advanced digital infrastructure, and early adoption of emerging storage technologies. Ongoing digital transformation initiatives and emphasis on energy-efficient archival frameworks continue to stimulate demand. As large-scale data operations expand, holographic storage is increasingly viewed as a strategic enabler for resilient and scalable digital ecosystems. Companies are encouraged to deepen research collaborations and align product development with institutional requirements to capitalize on growth opportunities within the region.

Key participants in the Global Holographic Data Storage Market include InPhase Technologies, Optware Corporation, Aprilis Inc., Akonia Holographics, Zebra Imaging, Holographic Versatile Disc (HVD) Alliance, Sony Corporation, Panasonic Holdings Corporation, Samsung Electronics, Fujifilm Holdings Corporation, Hitachi, Ltd., General Electric (GE Research), IBM Corporation, Microsoft Corporation, Toshiba Corporation, Intel Corporation, Western Digital Corporation, and Seagate Technology. Companies competing in the Holographic Data Storage Market are reinforcing their market presence through continuous innovation and strategic alliances. Industry leaders are prioritizing research investments to enhance media stability, improve data transfer speeds, and increase storage density. Partnerships with enterprise data infrastructure providers and institutional organizations are accelerating commercialization efforts. Firms are also focusing on scalable product architectures to address large-capacity storage requirements. Strengthening intellectual property portfolios and advancing material science capabilities remain central strategies for differentiation.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Technology trends

- 2.2.2 Storage capacity trends

- 2.2.3 Component trends

- 2.2.4 Application trends

- 2.2.5 End-user industry trends

- 2.2.6 Material trends

- 2.2.7 Regional trends

- 2.3 TAM Analysis, 2026 - 2035 (USD Billion)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 High data storage density and capacity compared to traditional storage solutions

- 3.2.1.2 Rapid growth in cloud computing and big data applications

- 3.2.1.3 Increasing demand for secure and long-term archival storage

- 3.2.1.4 Rising need for high-speed data retrieval and processing

- 3.2.1.5 Growing adoption in defense, healthcare, and multimedia industries

- 3.2.2 Pitfalls and challenges

- 3.2.2.1 High cost of implementation and maintenance

- 3.2.2.2 Complexity of technology integration with existing IT infrastructure

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging Business Models

- 3.9 Compliance Requirements

- 3.10 Supply Chain Resilience

- 3.11 Geopolitical Analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Product portfolio comparison

- 4.3.1.1 Product range breadth

- 4.3.1.2 Technology

- 4.3.1.3 Innovation

- 4.3.2 Geographic presence comparison

- 4.3.2.1 Global footprint analysis

- 4.3.2.2 Service network coverage

- 4.3.2.3 Market penetration by region

- 4.3.3 Competitive positioning matrix

- 4.3.3.1 Leaders

- 4.3.3.2 Challengers

- 4.3.3.3 Followers

- 4.3.3.4 Niche players

- 4.3.4 Strategic outlook matrix

- 4.3.1 Product portfolio comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Technology, 2022 - 2035 (USD Billion)

- 5.1 Key trends

- 5.2 Volume Holographic Storage (VHS)

- 5.3 Surface Holographic Storage (SHS)

- 5.4 Hybrid Holographic Storage

Chapter 6 Market Estimates and Forecast, By Storage Capacity, 2022 - 2035 (USD Billion)

- 6.1 Key trends

- 6.2 Less than 1 TB

- 6.3 1 TB to 10 TB

- 6.4 More than 10 TB

Chapter 7 Market Estimates and Forecast, By Component, 2022 - 2035 (USD Billion)

- 7.1 Key trends

- 7.2 Hardware

- 7.3 Software

- 7.4 Services

Chapter 8 Market Estimates and Forecast, By Material, 2022 - 2035 (USD Billion)

- 8.1 Key Trends

- 8.2 Photopolymers

- 8.3 Photorefractive Crystals

- 8.4 Silicon-based Storage

- 8.5 Polymer Thin Films

Chapter 9 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion)

- 9.1 Key trends

- 9.2 Enterprise Data Storage & Data Centers

- 9.3 Archival Storage & Backup

- 9.4 Real-Time High-Volume Data Access

- 9.5 Critical Secure Storage

- 9.6 Others

Chapter 10 Market Estimates and Forecast, By End-User Industry, 2022 - 2035 (USD Billion)

- 10.1 Key Trends

- 10.2 IT & Telecommunications

- 10.3 Banking, Financial Services & Insurance (BFSI)

- 10.4 Healthcare

- 10.5 Media & Entertainment

- 10.6 Government

- 10.7 Defense & Aerospace

- 10.8 Others (Education, Research Institutions, etc.)

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Key Players

- 12.1.1 Sony Corporation

- 12.1.2 Panasonic Holdings Corporation

- 12.1.3 Samsung Electronics

- 12.1.4 Hitachi, Ltd.

- 12.1.5 IBM Corporation

- 12.1.6 Microsoft Corporation

- 12.1.7 Intel Corporation

- 12.1.8 Toshiba Corporation

- 12.2 Regional Key Players

- 12.2.1 North America

- 12.2.1.1 Western Digital Corporation

- 12.2.1.2 Seagate Technology

- 12.2.1.3 InPhase Technologies

- 12.2.1.4 Optware Corporation

- 12.2.1.5 Aprilis Inc.

- 12.2.2 Europe

- 12.2.2.1 Holographic Versatile Disc (HVD) Alliance

- 12.2.3 Asia Pacific

- 12.2.3.1 Fujifilm Holdings Corporation

- 12.2.1 North America

- 12.3 Niche / Disruptors

- 12.3.1 Akonia Holographics

- 12.3.2 Zebra Imaging

下一代資料儲存市場:按類型、架構、儲存媒體、部署模式、產業和地區分類

下一代資料儲存市場:按類型、架構、儲存媒體、部署模式、產業和地區分類 2026-2030年全球人工智慧最佳化儲存市場

2026-2030年全球人工智慧最佳化儲存市場 新一代資料儲存市場:2026-2032年全球市場預測(按儲存媒體、儲存架構、服務類型、部署模式、應用程式和最終用戶產業分類)

新一代資料儲存市場:2026-2032年全球市場預測(按儲存媒體、儲存架構、服務類型、部署模式、應用程式和最終用戶產業分類) 2026年全球天基資料記錄市場報告2026年全球下一代資料儲存市場報告

2026年全球天基資料記錄市場報告2026年全球下一代資料儲存市場報告 新一代資料儲存市場:依儲存類型(DAS、NAS、SAN)、儲存媒體、架構、最終用戶(銀行、金融服務和保險(BFSI)、零售、醫療保健、製造業、政府、IT 和電信、其他最終用戶)和地區劃分 - 至2027年的全球預測

新一代資料儲存市場:依儲存類型(DAS、NAS、SAN)、儲存媒體、架構、最終用戶(銀行、金融服務和保險(BFSI)、零售、醫療保健、製造業、政府、IT 和電信、其他最終用戶)和地區劃分 - 至2027年的全球預測 新一代資料儲存技術市場-全球產業規模、佔有率、趨勢、機會與預測:按類型、解決方案、記憶體、地區和競爭格局分類,2021-2031年

新一代資料儲存技術市場-全球產業規模、佔有率、趨勢、機會與預測:按類型、解決方案、記憶體、地區和競爭格局分類,2021-2031年 下一代資料儲存市場規模、佔有率和成長分析(按儲存系統、儲存媒體和地區分類)—產業預測(2026-2033 年)

下一代資料儲存市場規模、佔有率和成長分析(按儲存系統、儲存媒體和地區分類)—產業預測(2026-2033 年) 下一代資料儲存市場:2025 年至 2030 年的未來預測

下一代資料儲存市場:2025 年至 2030 年的未來預測 下一代儲存:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

下一代儲存:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)