|

市場調查報告書

商品編碼

2066773

歐洲混合動力電動車電池:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Europe Hybrid Electric Vehicle Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

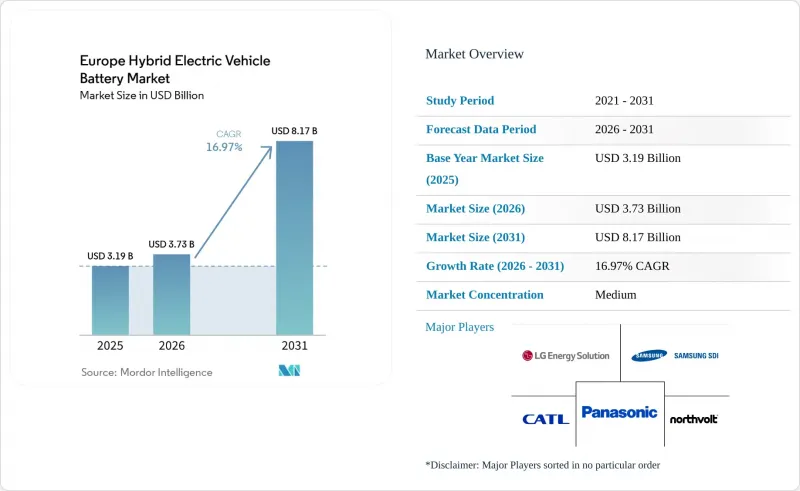

根據 Mordor Intelligence 預測,歐洲混合動力電動車電池市場規模將從 2025 年的 31.9 億美元成長到 2026 年的 37.3 億美元,到 2031 年將達到 81.7 億美元,2026 年至 2031 年的複合年成長率為 16.97%。

[1] 歐盟委員會,“二氧化碳排放性能標準提案”,ec.europa.eu。輕度混合動力汽車的普及率正在上升,超過了全混合動力汽車和插電式混合動力汽車。這是因為該技術能夠在燃油效率提高10-15%的情況下,以全混合動力汽車約三分之一的系統成本實現這一目標,同時保持盈利能力並避免開發昂貴的充電基礎設施。 [2] Stellantis,“2024年電氣化策略”,stellantis.com。隨著電池製造商追求降低材料成本和增強供應鏈韌性,鋰離子電池將在2025年主導市場,佔銷售額的78.2%。本報告按電池化學成分(鋰離子電池、鎳氫電池、鉛酸電池等)、混合程度(輕度混合電池、完全混合電池等)、電壓等級(60V 或以下、60-200V、200-400V、400V 或以上)、車輛類別(乘用車、英國、摩托車和三輪分類車等地區(德國分類車等)。

歐洲混合動力電動汽車電池市場的趨勢與洞察

提高混合動力車產量,以符合歐盟二氧化碳排放目標

汽車製造商必須達到2025年車隊平均排放量93.6克/公里的上限,該上限較2021年的115.1克/公里有所下調。超過此上限將導致每售出一輛車,每超標1克排放量需繳納95歐元的罰款。這促使各品牌在其銷量較大的B級和C級車型中推廣混合動力傳動系統。 Stellantis、雷諾和大眾汽車在2024年擴大了其48伏特車型陣容。每家公司都採用了皮帶驅動的啟動發電機系統,在成本增加不到1000歐元的情況下,將經認證的排放減少了約12克/公里。零排放和低排放氣體車輛的超級積分政策將持續到2025年,這使得製造商可以透過生產混合動力汽車來維持合規性,直到純電動車基礎設施建成。因此,這項法律規範將確保鋰離子電池的基本需求至少持續到 2027 年,之後更嚴格的 2030 年目標將進一步增加電氣化的壓力。

在中歐和東歐投資建造超級工廠和推進供應鏈本地化

2024年,匈牙利、波蘭和斯洛伐克新建電池工廠的投資總額超過150億歐元。其中,寧德時代(CATL)位於德布勒森的工廠(產能100吉瓦時)和LG能源解決方案公司位於弗羅茨瓦夫的工廠(產能擴建至70吉瓦時)是這項投資的核心。與西歐相比,這些地區的人事費用低15-20%,而且由於接近性德國組裝廠,電池組的前置作業時間縮短至24小時以內。歐洲電池聯盟的共同資助正在加速上游工程正極前驅體和隔膜計畫的開發,以取代亞洲原料,同時降低每千瓦時電池的隱含二氧化碳排放。隨著碳足跡揭露成為強制性要求,本地供應鏈正在獲得策略優勢。

重要礦產價格波動

碳酸鋰價格從2022年底的每噸8萬美元暴跌至2024年12月的近1萬美元。同時,硫酸鎳價格在短短一年內波動幅度高達每噸7,000美元。這種價格波動給固定價格供應合約的利潤率帶來了壓力,尤其是對於缺乏垂直整合的參與企業。投資者在為產能擴張提供資金時,現在要求加入價格調整條款和上游礦山的股權,導致多家超級工廠的運作計畫延期。

細分市場分析

預計到2025年,鋰離子電池將佔總需求的77.60%,其中高鎳NMC電池動力來源混合動力汽車,其能量密度要求為250-280 Wh/kg。磷酸鐵鋰電池(LFP)憑藉其3000次循環壽命和無鈷供應鏈,在輕度混合動力車市場佔據了更大的佔有率。比亞迪的「Blade Pack」電池組就是一個很好的例子,它在Stellantis車型中將系統成本降低了30%。新興的鈉離子電池和固態固態電池預計將以每年30.90%的速度成長,但預計在瑞典Northvolt試驗生產線於2026年後開始為入門級混合動力汽車量產之前,其規模仍將受到限制。由於豐田在面向歐洲市場的新車型中轉向使用鋰離子電池,鎳氫電池的市佔率已下降至7.60%。歐洲混合動力汽車電池市場正呈現化學成分兩極化的趨勢。注重成本的輕度混合動力車傾向於採用磷酸鐵鋰電池和鈉離子電池,注重性能的插電式混合動力汽車則繼續採用高鎳基鎳基碳化物電池,而全固態電池正在超豪華汽車中進行測試。

先進電池技術的引入增加了回收的複雜性。採用硫化物電解液的全固態電池組需要新的拆解和回收工藝,但歐洲很少有回收商願意大規模實施這些工藝。同時,無鈷電池形式降低了2023/1542號法規的監管負擔,使原始設備製造商(OEM)能夠節省因高鈷含量電池而產生的50-80歐元/千瓦時的合規成本。為了應對這些變化,超級工廠需要設計靈活的生產線,以便在不長時間運作下切換化學成分。亞洲的成熟企業已經展現了這種能力,歐洲的新興參與企業必須迅速跟進。

在歐洲混合動力汽車電池市場,預計到2025年,輕度混合動力汽車將佔總銷量的46.70%,並且預計到2031年,該細分市場將以18.64%的年均成長率成長。由於48伏特系統成本低廉(僅需800歐元),因此它是大眾高爾夫和雷諾Clio等車型的主要合規方式。以豐田e-CVT系統為代表的全混合動力車佔了28.40%的市場佔有率,但由於歐洲汽車品牌正在重新評估其研發預算分配,其複合年成長率相對較低,僅為10.60%。插電式混合動力車佔總銷售量的22.00%,但德國和英國取消購車獎勵削弱了其在總擁有成本(TCO)方面的競爭力,使其相對於純電動車(BEV)處於不利地位。

實際駕駛數據進一步加劇了這種壓力。 2024 年《交通與環境》雜誌的一項調查發現,面向車隊的插電式混合動力車 (PHEV) 純電模式的續航里程不足其總續航里程的一半,這促使政策制定者考慮引入基於更嚴格利用率係數的測試方法。在缺乏稅收優惠的情況下,隨著充電網路的建設,消費者傾向於選擇低成本的輕度混合動力汽車或純電動車 (BEV)。由於增程器器封裝複雜,其市佔率低於 2.90%,預計要到 2031 年才能普及。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 增加混合動力汽車(HEV)產量,以符合歐盟二氧化碳排放目標。

- 在中歐和東歐投資建造超級工廠和推進供應鏈本地化

- 歐洲鋰離子電池組價格下降

- 歐盟關於永續電池的法規中的獎勵

- 48V輕混架構中的突波

- 鈉離子電池的出現及其在低成本混合動力汽車。

- 市場限制因素

- 重要礦產價格波動

- OEM廠商的資本投資正轉向純電動車平台。

- 電池跨境運輸相關法規的複雜性

- 氫燃料電池內燃機混合動力汽車的興起正在推動投資方向的轉變。

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

- 投資分析

第5章 市場規模與成長預測

- 電池化學成分

- 鋰離子電池(NMC、NCA、LFP、LTO)

- 鎳氫電池(NiMH)

- 鉛酸

- 新興的固態電池/鈉離子電池

- 按雜交程度

- 輕度混合動力(48V MHEV)

- 全混合動力(HEV)

- 插電式混合動力車(PHEV)

- 有效距離式混合動力汽車

- 電壓等級

- 60伏特或以下

- 60~200 V

- 200~400 V

- 400伏特或以上

- 按車輛類型

- 搭乘用車

- 商用車輛

- 兩輪/三輪車

- 非公路及特殊用途

- 按地區

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 挪威

- 俄羅斯

- 其他歐洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- BYD Company Ltd

- LG Energy Solution

- Panasonic Holdings Corporation

- Samsung SDI Co., Ltd.

- SK On Co., Ltd.

- EnerSys

- Clarios

- Gotion High-Tech Co Ltd

- Northvolt AB

- Automotive Cells Company(ACC)

- VARTA AG

- CATL Europe

- AESC Envision

- InoBat Auto

- Verkor

- FREYR Battery

- SVOLT Energy Technology

- Saft Groupe SA

- Leclanche SA

- E4V

第7章 市場機會與未來展望

According to Mordor Intelligence, the europe hybrid electric vehicle battery market size is expected to grow from USD 3.19 billion in 2025 to USD 3.73 billion in 2026 and is forecast to reach USD 8.17 billion by 2031 at 16.97% CAGR over 2026-2031.

[1] European Commission, "Proposal for CO2 Emission Performance Standards," ec.europa.eu Mild-hybrid penetration is climbing ahead of full and plug-in variants because the technology delivers 10-15% fuel-economy gains at roughly one-third the system cost of a full hybrid, preserving margin while avoiding expensive charging infrastructure build-outs. [2] Stellantis, "2024 Electrification Strategy," stellantis.com Li-ion chemistries dominated in 2025 with 78.2% volume, as cell makers chase lower material cost and supply-chain resilience. This report is Segmented by Battery Chemistry (Lithium-Ion, Nickel-Metal Hydride, Lead-Acid, and More), Degree of Hybridization (Mild Hybrid, Full Hybrid, and More), Voltage Class (Up To 60V, 60 To 200V, 200 To 400V, and Above 400V), Vehicle Class (Passenger Cars, Commercial Vehicles, Two-/Three-Wheelers, and More), and Geography (Germany, United Kingdom, Spain, Netherlands, and More).

Europe Hybrid Electric Vehicle Battery Market Trends and Insights

Rising HEV Production Volumes Aligned With EU CO2 Fleet Targets

Automakers must meet the 2025 fleet-average ceiling of 93.6 g/km, reduced from 115.1 g/km in 2021, or pay EUR 95 for every excess gram per vehicle sold, pushing brands to standardize hybrid powertrains across high-volume B- and C-segment models. Stellantis, Renault, and Volkswagen expanded 48-volt offerings in 2024, each leveraging belt-starter-generator systems that shave roughly 12 g/km from type-approval emissions for less than a EUR 1,000 cost premium. Because super-credits for zero and low-emission vehicles can still be applied through 2025, building hybrids today generates compliance headroom while BEV infrastructure scales. This rule architecture therefore locks in baseline demand for lithium-ion cells through at least 2027, after which the stricter 2030 targets will intensify electrification pressure.

Gigafactory Investments in CEE Region Localizing Supply Chains

Over EUR 15 billion was committed to new cell plants in Hungary, Poland, and Slovakia during 2024, led by CATL's 100 GWh Debrecen facility and LG Energy Solution's Wroclaw expansion to 70 GWh. The labor arbitrage of 15-20% versus Western Europe, plus just-in-time proximity to German assembly hubs, trims pack lead times to under 24 hours. European Battery Alliance co-financing is accelerating upstream cathode precursor and separator projects that substitute Asia-origin inputs, simultaneously lowering embedded CO2 per kWh. As carbon-footprint declarations become mandatory, local supply chains gain a strategic advantage.

Critical Mineral Cost Volatility

Lithium carbonate prices collapsed from USD 80,000/t in late 2022 to near USD 10,000/t by December 2024, while nickel sulfate swung USD 7,000/t inside a single year. Such turbulence compresses margins on fixed-price supply deals, particularly for smaller European entrants lacking vertical integration. Investors now demand price-adjustment clauses or equity stakes in upstream mines before funding capacity expansions, delaying several gigafactory timelines.

Other drivers and restraints analyzed in the detailed report include:

- Surge in 48-V Mild-Hybrid Architectures

- EU Sustainable-Battery Regulation Incentives

- OEM Cap-ex Shift Toward Full-BEV Platforms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lithium-ion held 77.60% of 2025 demand, with high-nickel NMC variants powering plug-in hybrids that require 250-280 Wh/kg energy density. LFP gained share in mild-hybrids owing to 3,000-cycle durability and cobalt-free supply chains, a feat demonstrated by BYD's Blade pack that cut system cost 30% for Stellantis models. Emerging sodium-ion and solid-state formats should grow 30.90% annually yet remain sub-scale until after 2026, when Northvolt's pilot line in Sweden starts series output for entry-level hybrids. Nickel-metal-hydride slipped to 7.60% share as Toyota transitioned to new European releases to lithium-ion. The European hybrid electric vehicle battery market sees chemistry bifurcation: cost-sensitive mild hybrids gravitate to LFP and sodium-ion, performance-oriented PHEVs keep high-nickel NMC, and ultra-premium variants pilot solid-state cells.

Advanced chemistries introduce recycling complexity. Solid-state packs using sulfide electrolytes demand novel dismantling and recovery steps that few European recyclers are ready to scale. Simultaneously, cobalt-free formats lighten obligations under Regulation 2023/1542, saving OEMs the EUR 50-80/kWh compliance premium attached to high cobalt content cells. These shifts require gigafactories to design flexible lines capable of chemistry switching without extended downtime, a capability that entrenched Asian incumbents already demonstrate, and new European players must replicate quickly.

The European hybrid electric vehicle battery market recorded 46.70% revenue from mild hybrids in 2025, and this cohort will compound 18.64% annually to 2031. System costs as low as EUR 800 make 48-volt the dominant compliance lever for models such as the Volkswagen Golf and Renault Clio. Full hybrids, typified by Toyota's e-CVT system, held a 28.40% share yet face a slower 10.60% CAGR as European brands redirect engineering budgets. Plug-in hybrids claimed 22.00% revenue but are vulnerable after Germany and the UK scrapped purchase incentives, eroding total-cost-of-ownership parity with BEVs.

Real-world usage data compounds the pressure. A 2024 Transport & Environment study found fleet PHEVs drive less than half their kilometers in electric mode, prompting policymakers to consider tougher utility-factor testing. Absent tax breaks, buyers gravitate either to lower-cost mild hybrids or to BEVs as charging networks improve. Range-extender designs remain below 2.90% share due to packaging complexity and are unlikely to scale before 2031.

List of Companies Covered in this Report:

- BYD Company Ltd

- LG Energy Solution

- Panasonic Holdings Corporation

- Samsung SDI Co., Ltd.

- SK On Co., Ltd.

- EnerSys

- Clarios

- Gotion High-Tech Co Ltd

- Northvolt AB

- Automotive Cells Company (ACC)

- VARTA AG

- CATL Europe

- AESC Envision

- InoBat Auto

- Verkor

- FREYR Battery

- SVOLT Energy Technology

- Saft Groupe S.A.

- Leclanche SA

- E4V

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising HEV production volumes aligned with EU CO? fleet targets

- 4.2.2 Gigafactory investments in CEE region localizing supply chains

- 4.2.3 Declining lithium-ion pack prices in Europe

- 4.2.4 EU sustainable-battery regulation incentives

- 4.2.5 Surge in 48-V mild-hybrid architectures

- 4.2.6 Emergence of sodium-ion batteries for low-cost hybrids

- 4.3 Market Restraints

- 4.3.1 Critical mineral cost volatility

- 4.3.2 OEM cap-ex shift toward full-BEV platforms

- 4.3.3 Cross-border battery-transport regulatory complexity

- 4.3.4 Rise of hydrogen ICE hybrids diverting investment

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 Market Size & Growth Forecasts

- 5.1 By Battery Chemistry

- 5.1.1 Lithium-ion (NMC, NCA, LFP, LTO)

- 5.1.2 Nickel-Metal Hydride (NiMH)

- 5.1.3 Lead-acid

- 5.1.4 Emerging Solid-State/Sodium-ion

- 5.2 By Degree of Hybridization

- 5.2.1 Mild Hybrid (48 V MHEV)

- 5.2.2 Full Hybrid (HEV)

- 5.2.3 Plug-in Hybrid (PHEV)

- 5.2.4 Range-Extender Hybrid

- 5.3 By Voltage Class

- 5.3.1 Up to 60 V

- 5.3.2 60 to 200 V

- 5.3.3 200 to 400 V

- 5.3.4 Above 400 V

- 5.4 By Vehicle Class

- 5.4.1 Passenger Cars

- 5.4.2 Commercial Vehicles

- 5.4.3 Two-/Three-Wheelers

- 5.4.4 Off-Highway and Specialty

- 5.5 By Geography

- 5.5.1 Germany

- 5.5.2 United Kingdom

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Netherlands

- 5.5.7 Norway

- 5.5.8 Russia

- 5.5.9 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 BYD Company Ltd

- 6.4.2 LG Energy Solution

- 6.4.3 Panasonic Holdings Corporation

- 6.4.4 Samsung SDI Co., Ltd.

- 6.4.5 SK On Co., Ltd.

- 6.4.6 EnerSys

- 6.4.7 Clarios

- 6.4.8 Gotion High-Tech Co Ltd

- 6.4.9 Northvolt AB

- 6.4.10 Automotive Cells Company (ACC)

- 6.4.11 VARTA AG

- 6.4.12 CATL Europe

- 6.4.13 AESC Envision

- 6.4.14 InoBat Auto

- 6.4.15 Verkor

- 6.4.16 FREYR Battery

- 6.4.17 SVOLT Energy Technology

- 6.4.18 Saft Groupe S.A.

- 6.4.19 Leclanche SA

- 6.4.20 E4V

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

混合動力汽車電池:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

混合動力汽車電池:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 混合動力電動車電池市場規模、佔有率和成長分析(按電池類型、車輛類型、推進方式、製造方式和地區分類)—產業預測(2026-2033 年)中國混合動力汽車電池市場:佔有率分析、產業趨勢/統計、成長預測(2025-2030)中東和非洲混合動力電動車電池市場佔有率分析、產業趨勢、統計和成長預測(2025-2030)亞太地區混合電動汽車電池 -市場佔有率分析、產業趨勢、成長預測(2025-2030)北美混合電動汽車電池:市場佔有率分析、行業趨勢和成長預測(2025-2030)南美混合電動汽車電池:市場佔有率分析、行業趨勢和成長預測(2025-2030)印度混合電動汽車電池 -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030)德國混合動力電動車電池:市場佔有率分析、產業趨勢、成長預測(2025-2030)東南亞國協混合動力汽車電池:市場佔有率分析、產業趨勢與成長預測(2025-2030)

混合動力電動車電池市場規模、佔有率和成長分析(按電池類型、車輛類型、推進方式、製造方式和地區分類)—產業預測(2026-2033 年)中國混合動力汽車電池市場:佔有率分析、產業趨勢/統計、成長預測(2025-2030)中東和非洲混合動力電動車電池市場佔有率分析、產業趨勢、統計和成長預測(2025-2030)亞太地區混合電動汽車電池 -市場佔有率分析、產業趨勢、成長預測(2025-2030)北美混合電動汽車電池:市場佔有率分析、行業趨勢和成長預測(2025-2030)南美混合電動汽車電池:市場佔有率分析、行業趨勢和成長預測(2025-2030)印度混合電動汽車電池 -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030)德國混合動力電動車電池:市場佔有率分析、產業趨勢、成長預測(2025-2030)東南亞國協混合動力汽車電池:市場佔有率分析、產業趨勢與成長預測(2025-2030)