|

市場調查報告書

商品編碼

2066771

北美電動車電池製造:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)North America Electric Vehicle Battery Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

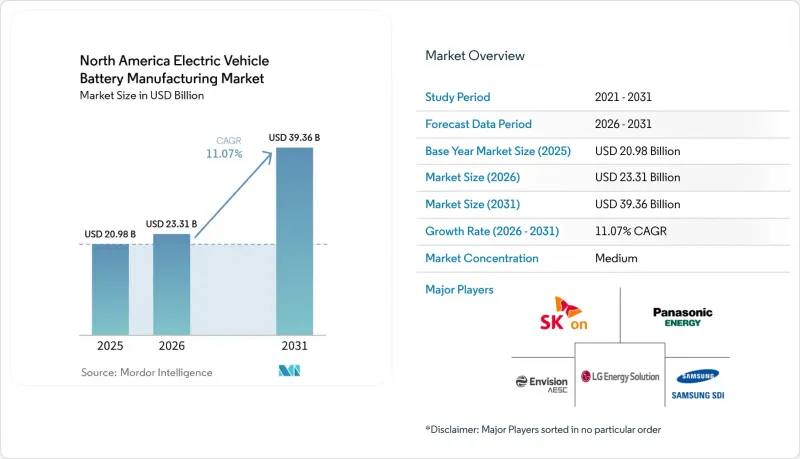

根據 Mordor Intelligence 預測,北美電動車電池製造市場規模預計將從 2025 年的 209.8 億美元成長到 2026 年的 233.1 億美元,到 2031 年將達到 393.6 億美元,2026 年至 2031 年的複合年成長率為 11.07%。

本報告按電池化學成分(鋰離子電池、新興技術電池、鉛酸電池、鎳氫電池)、電池類型(圓柱形、棱柱形、軟包型)、推進系統(電池電動車等)、車輛類型(乘用車、輕型商用車、中型和重型卡車、巴士和長途客車等)以及地區(美國、加拿大、墨西哥)進行分類。

北美電動車電池製造市場的趨勢與洞察

《通貨膨脹控制法案》(IRA)促進了超級工廠的建設擴張。

聯邦生產稅額扣抵正迫使參與企業從主導進口的供應鏈轉向本土生產線。 2024年,美國能源部向13家新建工廠提供了貸款。開發商正爭分奪秒地運作工廠建設,以確保在2032年開始逐步削減補貼之前獲得有利的單位經濟效益。繼續依賴亞洲進口的汽車製造商將面臨失去消費者稅收優惠的風險,導致其車輛售價比配備北美製造電池的車型高出7,500美元。由此引發的本土化競爭已將中西部和東南部的工業園區轉變為超級工廠集群,從而在短期內顯著提升了對本地建築商和模具供應商的需求。

OEM驅動的垂直整合競爭

Ultium Cells 和 BlueOval SK 等合資企業清楚地展現了傳統原始設備製造商 (OEM) 如何重塑其籌資策略。通用汽車 (GM) 和 LG Energy Solutions 已營運三家合資工廠,總合達 140 GWh,透過以帳面價值而非市場價格累計電池成本,降低了鋰和鎳基準價格波動帶來的風險。特斯拉的乾電極專利表明其致力於將組裝製程和核心智慧財產權 (IP) 內部化。垂直整合被視為一種保障,可在現貨原物料價格劇烈波動時保護毛利率。它還能在與正極材料供應商的談判中提供議價優勢。

原物料價格快速波動

碳酸鋰價格從2022年的每噸8.5萬美元暴跌至2023年的1.3萬美元,但隨後在不到六個月的時間裡,2024年的價格又加倍。由於印尼的出口限制和對俄羅斯的製裁導致供應緊張,鎳價波動了35%。季度重新談判取代了長期承購契約,縮小了電池製造商毛利率的緩衝空間,而此前毛利率徘徊在20%左右。 《通貨膨脹控制法案》(IRA)的國內採購要求限制了採購的柔軟性,迫使製造商即使在全球現貨價格基準較低的情況下,也必須使用價格較高的本地原料。

細分市場分析

2025年,鋰離子電池在北美電動車電池製造市場仍將佔據90.85%的佔有率,這得益於其成熟的良率(超過95%)和250-300 Wh/kg的能量密度。隨著OEM廠商試生產進入小批量生產階段,固態電池、鋰硫電池和鈉離子電池產品線預計到2031年將以34.08%的複合年成長率成長。鎳基複合材料(NMC)仍然是續航里程超過300英里的溢價率車的首選化學成分,但鈷價波動正在加速向高鎳NMC 811混合物(鈷含量僅為10%)的轉變。磷酸鐵鋰電池(LFP)雖然能量密度較低,但由於其不含鈷的設計降低了組件成本風險,因此在北美市場正在復甦。

北美電動車電池新興化學成分市場的擴張基於兩個假設:一是到2028年,全固體電池的產量將縮小與傳統生產線的差距;二是自動化將使每吉瓦時(GWh)的資本投資減半。鈉離子電池由於能量密度低,目前僅限於固定式儲能和都市區通勤車型,但其豐富的原料使其成為應對鋰短缺的可行方案。儘管對鋰硫電池的研究顯示其循環壽命超過150次,但其實用化仍存在不確定性。總體而言,即使到2030年它們無法完全取代鋰離子電池,新的化學成分仍將有助於分散供應風險並拓寬區域技術發展曲線。

2025年,圓柱形電池的需求佔比達51.90%。這反映了特斯拉早期採用筆記型電腦式電池設計以及高速繞線技術的成熟。由於汽車製造商青睞體積效率提升20%且組裝更簡單的方形電池,預計到2031年,方形電池的年複合成長率將達到25.32%。軟包電池仍保持著15%左右的市場佔有率,但因膨脹事故導致的召回事件凸顯了大規模生產中品管的挑戰。

棱柱形電池的成長正在推動北美電動車電池製造市場規模的擴大。在該地區,新的生產線採用直接將電芯組裝成電池組的方法,省去了模組外殼,從而每千瓦時可節省5至8美元的成本。特斯拉的4680圓柱形電池策略仍旨在透過片狀電極降低50%的成本,但其奧斯汀工廠低於80%的良率凸顯了大規模生產該製程的難度。比亞迪和寧德時代憑藉刀片式棱柱形電池組樹立了行業標桿,其電池組能量密度達到了160瓦時/公斤,並通過了釘刺測試,證明了其碰撞安全性。汽車製造商正努力在提高體積效率和應對過渡到不熟悉的生產設備所帶來的風險之間取得平衡。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 愛爾蘭共和軍推動超級工廠建設擴張

- OEM垂直整合競爭

- 正負極材料供應的區域化

- 固態中試管線的突破性進展

- 二次生命和回收信用市場

- 北美重要礦產協定

- 市場限制因素

- 原物料價格劇烈波動

- 電網容量和授權瓶頸

- 千兆級技術工人短缺

- 電動車需求的周期性波動仍在持續。

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 電池化學成分

- 鋰離子電池(NMC、LFP、NCA)

- 新興技術(全固體、鋰硫、鈉離子)

- 鉛酸

- 鎳氫電池

- 按單元格格式

- 圓柱形

- 棱柱型

- 小袋

- 透過推進力

- 電池式電動車(BEV)

- 插電式混合動力車(PHEV)

- 混合動力電動車(HEV)

- 按車輛類型

- 搭乘用車

- 輕型商用車

- 中型和大型卡車

- 巴士和長途汽車

- 二輪車和三輪車

- 按地區

- 美國

- 加拿大

- 墨西哥

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- LG Energy Solution

- Panasonic Energy(w/Tesla)

- SK On

- Samsung SDI

- AESC Envision

- Ultium Cells(GM+LG)

- CATL USA

- FREYR Battery

- BYD Motors NA

- Contemporary Amperex Technology Ltd.

- American Battery Solutions

- EnerSys

- GS Yuasa Corp

- Exide Industries NA

- Sionic Energy

- Clarios LLC

- Redwood Materials

- Li-Cycle Holdings

- QuantumScape

- Solid Power

第7章 市場機會與未來展望

According to Mordor Intelligence, the north america electric vehicle battery manufacturing market size is expected to grow from USD 20.98 billion in 2025 to USD 23.31 billion in 2026 and is forecast to reach USD 39.36 billion by 2031 at 11.07% CAGR over 2026-2031.

This report is Segmented by Battery Chemistry (Lithium-Ion, Emerging, Lead-Acid, and Nickel-Metal-Hydride), Cell Format (Cylindrical, Prismatic, and Pouch), Propulsion (Battery Electric Vehicle, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, Medium and Heavy Trucks, Buses and Coaches, and More), and Geography (United States, Canada, and Mexico).

North America Electric Vehicle Battery Manufacturing Market Trends and Insights

IRA-Fuelled Giga-Factory Build-Out

Federal production credits have pushed North America's electric vehicle battery manufacturing market participants to shift from import-led supply toward domestic lines, with 13 new U.S. plants securing Department of Energy loan offers in 2024. Developers are racing to commission facilities before subsidies taper after 2032, locking in advantageous unit economics. Automakers that continue to rely on Asian imports risk forfeiting consumer tax incentives, effectively pricing their vehicles USD 7,500 above models with North American batteries. The resulting localization sprint has converted Midwest and Southeast industrial parks into giga-factory corridors and supplied a visible near-term lift to regional construction and tooling suppliers.

OEM Vertical-Integration Race

Ultium Cells, BlueOval SK, and other captive ventures illustrate how legacy OEMs are rewriting procurement doctrine. General Motors and LG Energy Solution already run three joint plants totaling 140 GWh of capacity, embedding cell cost at book value instead of market value and moderating exposure to volatile lithium and nickel benchmarks. Tesla's dry-electrode patents show an ambition to internalize both assembly and core IP. Vertical integration is viewed as insurance that protects gross margins when spot raw-material contracts swing widely; it also provides bargaining leverage in negotiations with cathode suppliers.

Raw-Material Price Whiplash

Lithium carbonate plunged from USD 85,000 per tonne in 2022 to USD 13,000 per tonne in 2023, then doubled inside six months in 2024. Nickel saw a 35% swing after Indonesian export curbs and Russian sanctions tightened supply. Quarterly renegotiations have replaced long-term offtake contracts, shrinking the gross-margin buffer for cell producers that once hovered near 20%. IRA domestic-content rules restrict sourcing flexibility and lock manufacturers into higher-cost regional feedstock even when global spot benchmarks are cheaper.

Other drivers and restraints analyzed in the detailed report include:

- Regionalisation of Cathode & Anode Supply

- Solid-State Pilot-Line Breakthroughs

- Grid-Capacity & Permitting Bottlenecks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lithium-ion retained 90.85% of the 2025 North America electric vehicle battery manufacturing market share thanks to mature yields exceeding 95% and energy densities between 250 and 300 Wh/kg. Solid-state, lithium-sulfur, and sodium-ion lines will grow at a 34.08% CAGR through 2031 as OEM pilots graduate to low-volume series production. NMC remains the preferred chemistry for premium ranges above 300 miles, but cobalt cost volatility is accelerating the pivot toward high-nickel NMC 811 blends with just 10% cobalt content. LFP packs are rebounding in North America because their cobalt-free design reduces bill-of-materials risk despite lower energy density.

The North America electric vehicle battery manufacturing market size expansion for emerging chemistries rests on two assumptions: solid-state yields close the gap with conventional lines by 2028, and capex per GWh falls by half through automation. Sodium-ion's lower density constrains it to stationary storage and urban commuter models, yet its abundant raw material offers a hedge against lithium scarcity. Lithium-sulfur research pushes cycle life beyond 150, though deployment remains speculative. Collectively, new chemistries diversify supply risk and extend the regional technology curve without displacing lithium-ion before 2030.

Cylindrical cells held 51.90% of 2025 demand, reflecting Tesla's early laptop-derived designs and mature high-speed winding lines. Prismatic alternatives will move ahead with a 25.32% CAGR through 2031 as automakers favor 20% better volumetric efficiency and simplified pack assembly. Pouch formats keep a mid-teens niche, but recalls tied to swelling episodes highlight quality-control hurdles at scale.

Prismatic growth boosts the North America electric vehicle battery manufacturing market size, where new lines integrate cells directly into the pack, cutting module housings and saving USD 5-8 per kilowatt-hour. Tesla's 4680 cylindrical strategy still aims for a 50% cost cut through tab-less electrodes, though yields under 80% in Austin show the difficulty of scaling the process. BYD and CATL have set a benchmark with blade-style prismatic packs that reach 160 Wh/kg at the pack level and demonstrate crash safety during nail-penetration tests. Automakers are balancing volumetric gains with the risk of shifting to less familiar production tooling.

List of Companies Covered in this Report:

- LG Energy Solution

- Panasonic Energy (w/ Tesla)

- SK On

- Samsung SDI

- AESC Envision

- Ultium Cells (GM + LG)

- CATL USA

- FREYR Battery

- BYD Motors NA

- Contemporary Amperex Technology Ltd.

- American Battery Solutions

- EnerSys

- GS Yuasa Corp

- Exide Industries NA

- Sionic Energy

- Clarios LLC

- Redwood Materials

- Li-Cycle Holdings

- QuantumScape

- Solid Power

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 IRA-fuelled giga-factory build-out

- 4.2.2 OEM vertical-integration race

- 4.2.3 Regionalisation of cathode & anode supply

- 4.2.4 Solid-state pilot-line breakthroughs

- 4.2.5 Second-life & recycling credit markets

- 4.2.6 North-American critical-minerals pacts

- 4.3 Market Restraints

- 4.3.1 Raw-material price whiplash

- 4.3.2 Grid-capacity & permitting bottlenecks

- 4.3.3 Skilled-labour shortfall for giga-scale

- 4.3.4 Persisting EV-demand cyclicality

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Battery Chemistry

- 5.1.1 Lithium-ion (NMC, LFP, NCA)

- 5.1.2 Emerging (Solid-state, Li-S, Na-ion)

- 5.1.3 Lead-acid

- 5.1.4 Nickel-metal-hydride

- 5.2 By Cell Format

- 5.2.1 Cylindrical

- 5.2.2 Prismatic

- 5.2.3 Pouch

- 5.3 By Propulsion

- 5.3.1 Battery Electric Vehicle (BEV)

- 5.3.2 Plug-in Hybrid Electric Vehicle (PHEV)

- 5.3.3 Hybrid Electric Vehicle (HEV)

- 5.4 By Vehicle Type

- 5.4.1 Passenger Cars

- 5.4.2 Light Commercial Vehicles

- 5.4.3 Medium and Heavy Trucks

- 5.4.4 Buses and Coaches

- 5.4.5 Two and Three-wheelers

- 5.5 By Geography

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 LG Energy Solution

- 6.4.2 Panasonic Energy (w/ Tesla)

- 6.4.3 SK On

- 6.4.4 Samsung SDI

- 6.4.5 AESC Envision

- 6.4.6 Ultium Cells (GM + LG)

- 6.4.7 CATL USA

- 6.4.8 FREYR Battery

- 6.4.9 BYD Motors NA

- 6.4.10 Contemporary Amperex Technology Ltd.

- 6.4.11 American Battery Solutions

- 6.4.12 EnerSys

- 6.4.13 GS Yuasa Corp

- 6.4.14 Exide Industries NA

- 6.4.15 Sionic Energy

- 6.4.16 Clarios LLC

- 6.4.17 Redwood Materials

- 6.4.18 Li-Cycle Holdings

- 6.4.19 QuantumScape

- 6.4.20 Solid Power

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

中國電動汽車電池製造設備:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)中國電動汽車電池製造:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)中東和非洲電動車電池製造設備:市場佔有率分析、產業趨勢和成長預測(2025-2030)中東和非洲電動車電池製造:市場佔有率分析、產業趨勢和成長預測(2025-2030)亞太地區電動汽車電池製造設備:市場佔有率分析、產業趨勢與成長預測(2025-2030)亞太地區電動汽車電池製造:市場佔有率分析、產業趨勢與成長預測(2025-2030)北美電動車電池製造設備:市場佔有率分析、產業趨勢、成長預測(2025-2030)南美洲電動汽車電池製造設備:市場佔有率分析、產業趨勢、成長預測(2025-2030)南美洲電動車電池製造:市場佔有率分析、產業趨勢與成長預測(2025-2030)印度電動汽車電池製造設備:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)

中國電動汽車電池製造設備:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)中國電動汽車電池製造:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)中東和非洲電動車電池製造設備:市場佔有率分析、產業趨勢和成長預測(2025-2030)中東和非洲電動車電池製造:市場佔有率分析、產業趨勢和成長預測(2025-2030)亞太地區電動汽車電池製造設備:市場佔有率分析、產業趨勢與成長預測(2025-2030)亞太地區電動汽車電池製造:市場佔有率分析、產業趨勢與成長預測(2025-2030)北美電動車電池製造設備:市場佔有率分析、產業趨勢、成長預測(2025-2030)南美洲電動汽車電池製造設備:市場佔有率分析、產業趨勢、成長預測(2025-2030)南美洲電動車電池製造:市場佔有率分析、產業趨勢與成長預測(2025-2030)印度電動汽車電池製造設備:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)