|

市場調查報告書

商品編碼

2066770

義大利SLI電池:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)Italy SLI Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

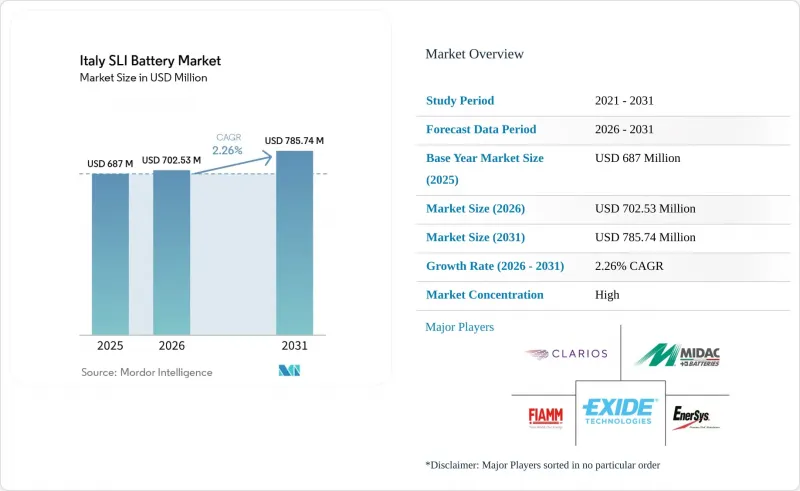

根據 Mordor Intelligence 預測,義大利 SLI 電池市場規模將從 2025 年的 6.87 億美元成長到 2026 年的 7.0253 億美元,然後在 2031 年達到 7.8574 億美元,2026 年至 2031 年的複合成長率為 2.26%。

本報告按電池類型(液態電池、改進型液態電池、AGM(吸附式玻璃纖維隔板)、膠體電池、VRLA)、電池電壓(低於 12V、12V、48V、高於 60V)和應用(乘用車、輕型商用車、重型商用車、摩托車和三輪車、農業和非公路用車輛、工業電源)進行分類/備用車輛、備後電源)。

義大利SLI電池市場的趨勢與洞察

車輛擁有量增加和更換需求上升

義大利擁有4,100萬輛汽車(平均車齡13年),這意味著大量電池即將報廢。由於車輛更新換代緩慢,新車註冊量僅佔總保有量的3-4%,2015年之前安裝的液態電解質電池如今已進入第二或第三次更換週期。儘管義大利電動車的普及速度慢於北歐國家,但這個穩定的需求群體保護了義大利固態鋰電池市場免受銷量大幅下滑的影響。使用超過五年的電池在冬季冷啟動問題激增,促使零售商積極推廣診斷檢查和季節性折扣。

啟動停止車輛中AGM/EFB電池的廣泛應用

到2024年,歐洲啟停系統的普及率將超過68%,義大利汽車製造商(OEM)也強制要求在新推出的微混動力平台上使用AGM或EFB電池。隨著這些車輛的劣化,售後市場的更換需求預計將會加速成長,而耐深度放電的AGM電池將越來越受到青睞。 Exide的雙端子AGM「B24」系列電池的適用車型已擴展至多達100萬輛,凸顯了製造商對電池通用性的重視。因此,經銷商需要投資儲備AGM電池庫存,安裝新的貨架設備,並培訓員工,以確保獲得更高的收益。

鋰離子12V輔助電池市佔率不斷擴大

EUROBAT預測,到2030年,受ADAS(高級駕駛輔助系統)和資訊娛樂系統需求激增的推動,12V輔助電池市場將呈現鉛酸電池和鋰離子電池各佔50%的格局。雖然鋰離子電池充電速度更快、重量更輕,但鉛酸電池在成本上具有60-70%的優勢,並且即使在零下溫度下也能提供更優異的冷啟動性能。義大利製造商正在加速推出薄板純鉛電池和碳增強型電池,以鞏固其在這個關鍵細分市場中的地位。

細分市場分析

AGM電池已廣泛應用於配備啟動/停止系統的車輛,預計將以6.31%的複合年成長率成長,而義大利SLI電池市場的整體成長率僅為2.26%。雖然液態電解質電池在2015年以前生產的車輛的替換電池市場仍佔據主導地位,但隨著AGM電池的普及,其市場佔有率預計將會下降。 EFB電池為車隊營運商提供了中等價位的選擇,他們需要比液態電解質電池更長的循環壽命,但又擔心AGM電池的價格過高。

隨著啟動停止功能的日益普及,義大利SLI電池市場中AGM產品市場預計將從2025年的2.27億美元成長到2031年的近3.277億美元。 Exide推出符合M3標準的AGM B24電池表明,製造商正在拓展端子選擇,以減少分銷商的庫存單位(SKU)。同時,儘管傳統的液體潤滑電池設計在成本壓力較大的南部地區仍將繼續被採用,但隨著消費者對AGM優勢的認知不斷提高,預計AGM在全國範圍內的市場佔有率將會下降。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 汽車保有量增加和更換需求上升

- 啟動停止車輛中AGM/EFB電池的廣泛應用

- 都市區車隊中微混動力改裝的蓬勃發展

- 歐盟推動鉛回收循環經濟

- 碳足跡標籤鼓勵本地採購。

- 汽車售後市場電子商務的擴張

- 市場限制因素

- 鋰離子12V輔助電源的市佔率正在擴大。

- 依照 2030 年目標,減少內燃機 (ICE) 的產量。

- 中小企業電池護照符合成本

- 鉛廢料價格波動與出口限制

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

- PESTLE分析

第5章 市場規模與成長預測

- 依電池類型

- 液體型(常規型)

- 增強型泛光(EFB)

- 吸收式玻璃纖維隔板(AGM)

- 凝膠細胞VRLA

- 電池電壓

- 12伏特或更低

- 12 V

- 48 V

- 60伏特或以上

- 透過使用

- 搭乘用車

- 輕型商用車

- 大型商用車輛

- 兩輪/三輪車

- 農業和非公路用車輛

- 工業動力設備(堆高機、物料搬運設備)

- 備用/備援(通訊、UPS)

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- FIAMM Energy Technology SpA

- Clarios(Johnson Controls)

- Exide Technologies

- Midac SpA

- Sunlight Group

- EnerSys

- GS Yuasa Corporation

- Banner GmbH

- C&D Technologies Inc.

- Leoch International Tech. Ltd.

- Accumulatori Ariete SRL

- Trojan Battery Company

- NorthStar Battery

- Bosch(Battery Division)

- Varta AG

- Yuasa Battery(Europe)Ltd.

- East Penn Mfg.(Deka)

- TAB Batteries

- Moll Batterien GmbH

- VoltA Batteries

第7章 市場機會與未來展望

According to Mordor Intelligence, the italy sLI battery market size is expected to grow from USD 687 million in 2025 to USD 702.53 million in 2026 and is forecast to reach USD 785.74 million by 2031 at 2.26% CAGR over 2026-2031.

This report is Segmented by Battery Type (Flooded, Enhanced Flooded, Absorbent Glass Mat, and Gel Cell VRLA), Battery Voltage (Up To 12V, 12V, 48V, and Above 60V), Application (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Two-/Three-Wheelers, Agricultural and Off-Highway Vehicles, Industrial Motive Power, and Stand-by/Backup).

Italy SLI Battery Market Trends and Insights

Growing vehicle-parc & replacement demand

Italy's 41 million-unit parc, averaging 13 years in age, generates a deep pool of batteries nearing end-of-life. Slow fleet turnover, new registrations equal only 3-4% of total parc, means flooded batteries installed before 2015 are now cycling through second or third replacements. The stability of this demand segment shields the Italy SLI battery market from abrupt volume declines even as EV adoption lags Northern Europe. Winter cold-cranking failures rise sharply in batteries older than five years, prompting retailers to promote diagnostic checks and seasonal discounts.

Rising AGM/EFB adoption in start-stop cars

Start-stop systems topped 68% penetration in Europe by 2024, and Italian OEMs mandate AGM or EFB fitment on new micro-hybrid platforms. As these vehicles age, aftermarket replacements are set to accelerate, favoring AGM chemistry that tolerates deep cycling. Exide's dual-terminal AGM B24 series widened fitment coverage by up to 1 million units, underscoring the priority manufacturers place on versatility. Distributors must therefore invest in AGM stocking, new racking, and staff training to capture the revenue upswing.

Li-ion 12 V auxiliaries gaining share

EUROBAT projects a 50/50 split between lead-acid and lithium-ion in 12 V auxiliary batteries by 2030 as ADAS and infotainment loads soar. Lithium-ion offers faster recharge and lighter weight, but lead-acid holds a 60-70% cost edge and better cold-cranking at sub-zero temperatures. Italian manufacturers are racing to introduce Thin-Plate Pure Lead and carbon-enhanced variants to hold ground in this critical niche.

Other drivers and restraints analyzed in the detailed report include:

- Micro-hybrid retrofit boom in urban fleets

- EU circular-economy push for lead recycling

- Shrinking ICE production under 2030 targets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

AGM already serves the majority of start-stop cars and is forecast to expand at a 6.31% CAGR, compared with the Italy SLI battery market's overall 2.26% growth. Flooded batteries still dominate replacement sales for vehicles built before 2015, but their share will erode as the AGM replacement wave matures. EFB provides a mid-price option for fleet operators who need higher cycle life than flooded units can provide, yet balk at full-AGM pricing.

The Italy SLI battery market size for AGM units is projected to rise from USD 227 million in 2025 to nearly USD 327.7 million by 2031 as start-stop penetration deepens. Exide's M3-rated AGM B24 launch shows how manufacturers are broadening terminal options to trim SKU counts for distributors. Meanwhile, flooded designs will persist in cost-pressured Southern regions but decline nationally as consumer education on AGM benefits increases.

List of Companies Covered in this Report:

- FIAMM Energy Technology S.p.A.

- Clarios (Johnson Controls)

- Exide Technologies

- Midac SpA

- Sunlight Group

- EnerSys

- GS Yuasa Corporation

- Banner GmbH

- C&D Technologies Inc.

- Leoch International Tech. Ltd.

- Accumulatori Ariete S.R.L.

- Trojan Battery Company

- NorthStar Battery

- Bosch (Battery Division)

- Varta AG

- Yuasa Battery (Europe) Ltd.

- East Penn Mfg. (Deka)

- TAB Batteries

- Moll Batterien GmbH

- VoltA Batteries

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing vehicle-parc & replacement demand

- 4.2.2 Rising AGM/EFB adoption in start-stop cars

- 4.2.3 Micro-hybrid retrofit boom in urban fleets

- 4.2.4 EU circular-economy push for lead recycling

- 4.2.5 Carbon-footprint labelling favours local supply

- 4.2.6 Expansion of automotive aftermarket e-commerce

- 4.3 Market Restraints

- 4.3.1 Li-ion 12 V auxiliaries gaining share

- 4.3.2 Shrinking ICE production under 2030 targets

- 4.3.3 Battery-passport compliance cost for SMEs

- 4.3.4 Lead-scrap price volatility & export curbs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Battery Type

- 5.1.1 Flooded (Conventional)

- 5.1.2 Enhanced Flooded (EFB)

- 5.1.3 Absorbent Glass Mat (AGM)

- 5.1.4 Gel Cell VRLA

- 5.2 By Battery Voltage

- 5.2.1 Up to 12 V

- 5.2.2 12 V

- 5.2.3 48 V

- 5.2.4 Above 60 V

- 5.3 By Application

- 5.3.1 Passenger Cars

- 5.3.2 Light Commercial Vehicles

- 5.3.3 Heavy Commercial Vehicles

- 5.3.4 Two-/Three-Wheelers

- 5.3.5 Agricultural and Off-Highway Vehicles

- 5.3.6 Industrial Motive Power (Forklifts, Material-Handling)

- 5.3.7 Stand-by/Backup (Telecom, UPS)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 FIAMM Energy Technology S.p.A.

- 6.4.2 Clarios (Johnson Controls)

- 6.4.3 Exide Technologies

- 6.4.4 Midac SpA

- 6.4.5 Sunlight Group

- 6.4.6 EnerSys

- 6.4.7 GS Yuasa Corporation

- 6.4.8 Banner GmbH

- 6.4.9 C&D Technologies Inc.

- 6.4.10 Leoch International Tech. Ltd.

- 6.4.11 Accumulatori Ariete S.R.L.

- 6.4.12 Trojan Battery Company

- 6.4.13 NorthStar Battery

- 6.4.14 Bosch (Battery Division)

- 6.4.15 Varta AG

- 6.4.16 Yuasa Battery (Europe) Ltd.

- 6.4.17 East Penn Mfg. (Deka)

- 6.4.18 TAB Batteries

- 6.4.19 Moll Batterien GmbH

- 6.4.20 VoltA Batteries

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

SLI電池市場規模、佔有率和趨勢分析報告:按類型、容量、應用、地區和細分市場預測(2026-2033年)

SLI電池市場規模、佔有率和趨勢分析報告:按類型、容量、應用、地區和細分市場預測(2026-2033年) SLI電池市場機會、成長要素、產業趨勢分析及2026-2035年預測。

SLI電池市場機會、成長要素、產業趨勢分析及2026-2035年預測。 SLI電池市場-全球產業規模、佔有率、趨勢、機會和預測,按類型(富液式電池、增強型富液式電池)、應用、銷售通路、地區和競爭格局分類,2021-2031年預測商用車SLI電池市場-全球產業規模、佔有率、趨勢、機會及預測,依類型、應用、車輛類型、銷售通路、地區及競爭格局分類,2021-2031年預測

SLI電池市場-全球產業規模、佔有率、趨勢、機會和預測,按類型(富液式電池、增強型富液式電池)、應用、銷售通路、地區和競爭格局分類,2021-2031年預測商用車SLI電池市場-全球產業規模、佔有率、趨勢、機會及預測,依類型、應用、車輛類型、銷售通路、地區及競爭格局分類,2021-2031年預測 SLI電池市場規模、佔有率和成長分析(按類型、應用、電壓、容量和地區分類)-產業預測(2026-2033年)美國 SLI 電池市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

SLI電池市場規模、佔有率和成長分析(按類型、應用、電壓、容量和地區分類)-產業預測(2026-2033年)美國 SLI 電池市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 SLI 電池市場,按類型、按應用、按配銷通路、按國家和地區 - 2025 年至 2032 年的行業分析、市場規模、市場佔有率和預測

SLI 電池市場,按類型、按應用、按配銷通路、按國家和地區 - 2025 年至 2032 年的行業分析、市場規模、市場佔有率和預測 SLI 電池:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030 年)中國SLI電池:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)中東和非洲的 SLI 電池:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)

SLI 電池:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030 年)中國SLI電池:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)中東和非洲的 SLI 電池:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)