|

市場調查報告書

商品編碼

2066766

汽車顯示面板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Automotive Display Panel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

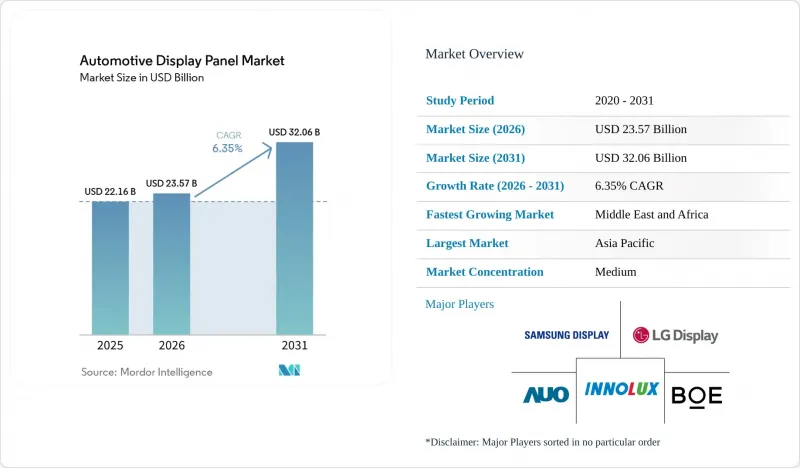

根據 Mordor Intelligence 預測,汽車顯示面板市場規模將從 2025 年的 221.6 億美元成長到 2026 年的 235.7 億美元,然後在 2031 年達到 320.6 億美元,2026 年至 2031 年的複合年成長率為 6.35%。

本報告依顯示技術(例如,非晶矽液晶顯示器)、螢幕大小(例如,5吋或更小)、車輛類型(例如,乘用車)、應用(例如,儀錶板)、整合度(例如,獨立顯示器)、觸控/控制方式(例如,觸控螢幕)、銷售管道(原廠配套安裝、售後市場)和地區進行細分。市場預測以美元計價。

全球汽車顯示面板市場趨勢及洞察

在中國和美國的豪華車市場,汽車製造商正在競相推出貫穿整個駕駛座的顯示器。

LG Display 將於 2025 年 2 月開始量產其 40 吋顯示螢幕,這標誌著顯示螢幕的功能模式轉移,它不再僅僅是功能升級,而是品牌的象徵。可切換的隱私模式允許前排乘客在不分散駕駛人注意力的情況下觀看串流內容,這既降低了監管風險,又能帶來訂閱收入。SONY本田的 AFEELA 轎車預計將成為首款搭載該模組的車型,而類似的配置也已被優先應用於 2024 年即將上市的 100 多款中國製造的電動車中。這進一步強化了以顯示器為中心的駕駛座模式,支援空中下載 (OTA) 功能解鎖,使汽車顯示面板市場成為軟體貨幣化的關鍵驅動力。

歐盟推動對先進駕駛輔助系統進行監管,從而催生了對更大尺寸數位儀錶叢集的需求。

歐盟第2019/2144號法規將強制要求所有整合基於眼動追蹤的駕駛分心警告系統的新車必須獲得型式認證,該法規將於2024年7月生效。滿足這些技術要求將鼓勵汽車製造商在其所有車型系列中標準化配備更大、感測器更豐富的儀錶叢集,而不再局限於高階車型。該法規也正透過聯合國歐洲經濟委員會(UNECE)在全球推廣,有效地提高了未來儀錶叢集規格的標準。

OLED螢幕老化問題的可靠性問題限制了其在計程車和車隊中的應用。

持續顯示靜態影像(例如票價資料)會導致像素隨時間劣化而劣化。雖然像素偏移演算法已將均勻性提高到 94.5%,但營運商仍要求在進行大規模部署前進行數年的驗證。 5-7 年的更換週期也加劇了這種猶豫,阻礙了 OLED 在高使用率車隊中的普及,而這些車隊原本會在汽車顯示面板市場創造可觀的銷售額。

細分市場分析

隨著汽車製造商追求旗艦車型無與倫比的亮度和能源效率,MicroLED預計將以10.85%的複合年成長率成長。友達光電(AUO)在2025年發表的透明車頂面板與變形控制技術,展現了標準LCD無法實現的極致設計自由。儘管非晶矽(a-Si) LCD仍佔50.74%的市場佔有率,但在高階車型中,用戶體驗指標的重要性超過了單價,其成本優勢正在逐漸減弱。氧化銦鎵鋅(IGZO) LCD正被應用於高解析度儀錶群,以最大限度地降低待機功耗;而Mini-LED背光LCD則憑藉接近OLED的對比度,填補了這一空白。雖然防燒螢幕演算法的進步延長了OLED的使用壽命,但車隊採購商仍保持謹慎。這些並行的趨勢表明,汽車顯示面板市場正在擁抱共存而非完全替換,從而實現全系車型功能的逐步升級。

各大汽車製造商目前正透過同時批准MicroLED和OLED用於未來的駕駛座來規避採購風險。三星顯示器已開始提供12吋MicroLED叢集樣品,計畫於2028年投入量產。同時,一級供應商正在整合通用圖形堆疊,透過允許僅需少量軟體變更即可更換儀錶板面板類型,從而支援「軟體定義汽車」的目標。這種柔軟性確保了現有LCD製造工廠能夠維持產能水平,並在下一代顯示面板行業的多元化。

儘管2024年12吋以上的顯示器仍屬於小眾市場,但它們為駕駛座架構開闢了新的可能性,例如貫穿式儀錶板和車頂顯示器。 LG Display的40吋模組支援多區域調光,可在同一螢幕上同時顯示叢集、資訊娛樂系統和乘客劇院。 5.1吋至8吋的中型面板在主流資訊娛樂系統中仍然佔據主導地位,預計到2025年將佔37.12%的銷量,但成長趨勢正轉向更大尺寸的面板。與此同時,小於5英寸的螢幕銷量依然強勁,擴大被用作後視鏡替代品和空調控制面板。這種兩極分化顯而易見:高階車型需要大尺寸顯示螢幕,而量產車型則傾向於叢集尺寸較小、分佈更廣的面板。隨著軟體層打破功能與安裝位置之間的聯繫,尺寸的選擇現在更多地基於美觀性和材料清單(BOM),而不是固定的儀表位置,這進一步增強了汽車顯示面板市場的設計靈活性。

市場領先的公司正在實施自適應使用者介面框架,該框架可根據駕駛模式重新配置佈局。例如,在駕駛過程中,它們會顯示高對比度的ADAS(高級駕駛輔助系統)疊加層;而在停車時,則會切換到劇院級寬螢幕顯示。這種適應性正在推動未來的策略發展,而大尺寸汽車顯示面板市場也將受益於基於使用量的獲利模式,例如在自動駕駛模式下啟動的串流訂閱服務。

儘管預計到2025年乘用車將佔汽車出貨量的83.58%,但重型商用車市場正以13.55%的複合年成長率快速成長,這主要得益於安全法規和遠端資訊處理技術的融合。車隊營運商正在積極採用高解析度叢集,將胎壓監測、路線分析和駕駛引導等功能整合到單一介面,從而減少車輛停機時間。輕型商用車也緊跟著,力求在提供與乘用車媲美的使用者體驗的同時,最佳化裝載效率。預計到2031年,商用車顯示面板的市場規模將超過15.24%的銷售佔有率,這凸顯了顯示面板正從可選配置轉變為營運必需品。

面板供應商正透過提供抗衝擊和抗振動能力超過 70G 的組件以及可承受日常清潔的防眩光蓋板玻璃來應對這項挑戰。空中下載 (OTA) 更新使貨運公司能夠在現有儀錶板上利用先進的遠端資訊處理功能,從而將硬體轉化為持續的服務收入來源。這種經營模式將顯示器視為收入來源而非折舊免稅額資產,從而提升了整個汽車顯示面板產業的價值創造。

區域分析

預計到2025年,亞太地區將佔全球銷量的48.12%,成為領先地區,這主要得益於中國龐大的電動車開發平臺和日本較早訂定的後視攝影機相關法規。該地區的汽車製造商正大力推廣32吋乘客顯示器和AR抬頭顯示器作為標準配置,迫使全球競爭對手採用類似規格。京東方等本土面板製造商已開始交付9K氧化物TFT原型,展現了國內產業生態系統的深度。同時,一家在印度的合資企業正在實現LCD模組組裝的在地化,既滿足了對成本高度敏感的市場需求,也增強了供應鏈抵禦外部衝擊的能力。

在北美,豪華SUV需求的成長以及無後視鏡設計的法規核准進程正推動著市場發展。貫穿式儀錶板成為高階車型的標配,而寬螢幕顯示器則被應用於卡車駕駛室,以提升拖車時的可視性。大規模的半導體投資,例如在美國新建一座價值600億美元的晶圓廠,增強了上游工程的穩定性,並有助於面板控制器供應的穩定性。這些因素將鞏固北美在2025年成為全球第二大汽車顯示面板市場的地位。

在歐洲,高階駕駛輔助系統 (ADAS) 的普及主要受安全導向應用的推動,而這又得益於 2019/2144 號法規的實施。汽車製造商正在整合眼動追蹤叢集和跨域顯示技術,以滿足歐洲新車安全評估協會 (Euro NCAP) 的藍圖目標。 「全景視覺」概念車計畫於 2025 年投產,它展示了德國汽車製造商如何將 ADAS 資訊整合到大面積玻璃表面。儘管面臨成本壓力,德國和捷克共和國的供應商叢集(專注於光學黏合和汽車塗層)仍在努力維持歐洲製造零件的比例。

中東和非洲地區以8.17%的複合年成長率位居榜首。為了因應極端高溫,市場對亮度高達45,000尼特、即使在85°C高溫下也能保持色彩還原的Mini-LED面板需求旺盛。共乘車輛正在升級乘客舒適度,進口豪華轎車也配備了波灣合作理事會娛樂系統。海灣合作理事會(GCC)各國政府制定的電氣化目標進一步推動了對高效率、高亮度顯示器的需求。儘管南美洲高級產品的滲透率落後於其他地區,但該地區預計將逐步擴大其在汽車顯示面板行業的佔有率,並透過從巴西和越南到南方共同市場(Mercosur)供應鏈中的本地玻璃加工廠,為成長奠定基礎。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 中國和美國高階汽車製造商在推出貫穿式駕駛座顯示器方面展開了激烈的競爭。

- 歐盟監管機構推動採用更大尺寸的數位儀錶板的高級駕駛輔助系統。

- OLED面板平均售價(ASP)的下降正在推動OEM廠商在中檔乘用車中採用OLED面板。

- 半導體迷你LED背光燈可提高高溫中東市場電動車的亮度。

- 消費者對車載串流媒體和遊戲的需求不斷成長,推動了對大於 12 吋的後座娛樂螢幕的需求。

- 在日本和韓國獲得型式認證後,引入了數位側視鏡。

- 市場限制因素

- OLED螢幕老化問題的可靠性問題限制了其在計程車和車隊車輛的應用。

- 由於IGZO背板產能不足,預計2025年機型的發表將會延後。

- 曲面自由曲面顯示器的高額物料清單 (BOM) 成本阻礙了其在印度和巴西等大眾市場的廣泛應用。

- 網路安全合規成本正在延緩售後維修。

- 產業生態系分析

- 技術概述

- 波特五力分析

第5章 市場規模與成長預測

- 顯示技術

- a-Si LCD

- 氧化物液晶(IGZO)

- LTPS LCD

- OLED(AMOLED、PMOLED)

- MicroLED

- 其他(電子紙、Mini-LED背光)

- 按螢幕尺寸

- 5英吋或更小

- 5.1 至 8 英寸

- 8.1 至 12 英寸

- 12吋或更大

- 車輛類型

- 搭乘用車

- 輕型商用車

- 大型商用車輛

- 透過使用

- 儀表板

- 中控台/資訊娛樂系統

- 抬頭顯示器

- 後座娛樂系統

- 數位側視鏡/智慧後視鏡

- 其他(屋頂、暖通空調)

- 依整合程度

- 獨立顯示器

- 一體式駕駛座/柱間

- 觸控/控制類型

- 觸控螢幕(電容式、電阻式)

- 非觸控式(僅顯示)

- 按銷售管道

- OEM配備型

- 改裝

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 北歐的

- 其他歐洲國家

- 南美洲

- 巴西

- 其他南美國家

- 亞太地區

- 中國

- 日本

- 印度

- 東南亞

- 其他亞太國家

- 中東和非洲

- 中東

- 波灣合作理事會(GCC)成員國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 供應商排名分析

- 市佔率分析

- 公司簡介

- LG Display

- Samsung Display

- BOE Technology Group

- AUO Corporation

- Innolux Corporation

- Sharp Corporation

- Japan Display Inc.

- Tianma Micro-electronics

- CSOT(TCL China Star)

- Visionox

- Truly Semiconductors

- HKC Corporation

- Continental AG

- Denso Corporation

- Robert Bosch GmbH

- Visteon Corporation

- Panasonic Automotive

- Nippon Seiki

- Magna International

- Marelli

- Yazaki Corporation

- Faurecia(Forvia)

- Desay SV

- Foryou General Electronics

- Hyundai Mobis

第7章 市場機會與未來展望

According to Mordor Intelligence, the automotive display panel market size is expected to grow from USD 22.16 billion in 2025 to USD 23.57 billion in 2026 and is forecast to reach USD 32.06 billion by 2031 at 6.35% CAGR over 2026-2031.

This report is Segmented by Display Technology (a-Si LCD, and More), Screen Size (Up To 5 Inch, and More), Vehicle Type (Passenger Cars, and More), Application (Instrument Cluster, and More), Integration Level (Stand-Alone Displays, and More), Touch/Control (Touchscreen, and More), Sales Channel (OEM-Fitted, and Aftermarket), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Automotive Display Panel Market Trends and Insights

Automaker race to deliver pillar-to-pillar cockpit displays in China and US premium segments

Mass-production of LG Display's 40-inch unit since February 2025 signals a paradigm shift whereby displays act as brand signatures instead of functional upgrades. Switchable Privacy Mode permits front-seat streaming without distracting the driver, alleviating regulatory risk while enabling subscription revenue. Sony-Honda's AFEELA sedan will debut the module, and more than 100 Chinese EV launches in 2024 already prioritized similar configurations. This reinforces a display-centric cockpit model that supports over-the-air feature unlocks, making the automotive display panel market a software monetization anchor

Regulatory push for advanced driver assistance requiring larger digital instrument clusters in EU

Regulation (EU) 2019/2144 forces new type approvals from July 2024 to integrate driver-distraction warning functions that rely on gaze tracking. Meeting the technical files persuades OEMs to standardize larger, sensor-rich clusters across model lines rather than limit such panels to premium trims. The rule also propagates globally through UNECE channels, effectively lifting the baseline specification for forthcoming instrument clusters.

OLED burn-in reliability concerns limiting deployment in taxis/fleets

Continuous static images such as fare data create uneven pixel aging. Pixel-shift algorithms raise uniformity to 94.5%, yet operators demand multi-year proof before large rollouts. Replacement cycles of 5-7 years amplify the hesitancy, stalling OLED penetration into high-utilization fleets that otherwise would contribute sizable volumes to the automotive display panel market.

Other drivers and restraints analyzed in the detailed report include:

- Falling OLED panel ASPs triggering OEM adoption in mid-range passenger cars

- Mini-LED backlighting enhancing brightness for EVs in high-temperature Middle-East markets

- Scarcity of IGZO backplane capacity causing 2025 model-year delays

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

MicroLED is set to grow at 10.85% CAGR as carmakers target unmatched brightness and efficiency for flagship models. AUO's transparent roof panels and morphing controls presented in 2025 validate design freedom that standard LCD cannot match. While a-Si LCD still commanded 50.74% revenue, its cost advantage wanes in upper trims where user-experience metrics trump unit price. Oxide LCD (IGZO) powers high-resolution instrument clusters that need minimal standby draw, and Mini-LED backlit LCD bridges the gap with quasi-OLED contrast. OLED breakthroughs in burn-in algorithms lengthen usable life, yet fleet buyers stay wary. These parallel tracks confirm that the automotive display panel market accommodates coexistence rather than outright substitution, enabling tiered feature packaging across vehicle lines.

Large automakers now hedge sourcing risk by approving both MicroLED and OLED for future cockpits; Samsung Display already samples 12-inch MicroLED clusters for 2028 production. Meanwhile, Tier-1 suppliers embed common graphics stacks so dashboards can interchange panel types with minor software changes, supporting software-defined vehicles goals. This flexibility sustains volume for incumbent LCD fabs even as next-gen formats expand, keeping the automotive display panel industry diversified.

Displays above 12 inches, though niche in 2024, unlock new cockpit architectures such as pillar-to-pillar dashboards and roof installations. LG Display's 40-inch module supports multi-zone dimming, allowing simultaneous cluster, infotainment, and passenger cinema in one surface. Mid-sized 5.1-8 inch panels remain primary for mainstream infotainment and secure 37.12% 2025 revenue, but growth momentum shifts upward. Conversely, up-to-5-inch screens gain traction in mirror replacements and HVAC touch bars, keeping unit volumes high. The bifurcation is clear: premium vehicles order expansive canvases; mass models opt for distributed clusters of small panels. As software layers decouple function from location, size selection hinges on aesthetics and bill-of-materials rather than fixed gauge placement, reinforcing flexible design in the automotive display panel market.

Market leaders deploy adaptive UI frameworks that reconfigure layout based on driving mode, from high-contrast ADAS overlays during motion to cinematic widescreen when parked. Such adaptability steers future strategy, where automotive display panel market size for large formats benefits from time-of-use monetization, for instance, streaming subscriptions activated in autonomous mode.

Passenger cars keep 83.58% of 2025 shipments, yet heavy commercial vehicles grow faster at 13.55% CAGR as safety mandates and telematics converge. Fleet operators justify high-resolution clusters that synthesize tire pressure, route analytics, and driver coaching on a single interface, cutting downtime. Light commercial vans follow, blending passenger-car UX expectations with cargo optimization tools. The automotive display panel market size for commercial classes is projected to cross 15.24% revenue share by 2031, underscoring a shift from optional extras to operational necessities.

Panel suppliers respond with shock-and-vibration-rated assemblies exceeding 70 Gs and anti-glare cover glass that withstands daily cleanings. Over-the-air upgrades permit freight companies to unlock advanced telematics on existing dashboards, converting hardware into recurrent service income. This business model cements displays as revenue generators rather than depreciating assets, amplifying value capture across the automotive display panel industry.

Geography Analysis

Asia-Pacific led with 48.12% revenue in 2025 owing to China's prolific EV pipelines and Japan's early legalization of camera mirrors. Regional automakers tout 32-inch passenger screens and AR HUDs as baseline features, forcing global competitors to match specs. Indigenous panel makers like BOE ship 9K oxide TFT prototypes, proving domestic ecosystem depth. Meanwhile, joint ventures in India localize LCD module assembly, fulfilling cost-sensitive markets and insulating supply from external shocks.

North America benefits from luxury SUV appetite and regulatory momentum toward mirrorless approvals. Pillar-to-pillar dashboards differentiate premium trims, while truck cabins embrace wide displays for towing visualization. Massive semiconductor investments, such as USD 60 billion in new US wafer fabs, strengthen upstream resilience, smoothing panel controller availability. These factors cement North America as the second-largest region by 2025 for the automotive display panel market.

Europe centers on safety-oriented adoption driven by Regulation 2019/2144. Automakers integrate gaze-tracking clusters and cross-domain displays that meet Euro NCAP roadmap targets. Panoramic Vision concepts slated for 2025 production reveal how German OEMs merge ADAS feeds with expansive glass surfaces. Supplier clusters in Germany and Czechia specialize in optical bonding and auto-grade coatings, anchoring European content despite cost pressures.

Middle East and Africa posts the highest 8.17% CAGR. Extreme heat calls for 45,000-nit Mini-LED panels that maintain chroma at 85 °C. Luxury imports equip rear entertainment suites as ride-hailing fleets upgrade passenger amenities. Government electrification targets in Gulf Cooperation Council nations further accelerate demand for efficient, high-brightness displays. South America lags in premium penetration but seeds growth through local glass finishing plants in Brazil and Vietnam-to-Mercosur supply chains, positioning the region for gradual uptake in the automotive display panel industry.

- LG Display

- Samsung Display

- BOE Technology Group

- AUO Corporation

- Innolux Corporation

- Sharp Corporation

- Japan Display Inc.

- Tianma Micro-electronics

- CSOT (TCL China Star)

- Visionox

- Truly Semiconductors

- HKC Corporation

- Continental AG

- Denso Corporation

- Robert Bosch GmbH

- Visteon Corporation

- Panasonic Automotive

- Nippon Seiki

- Magna International

- Marelli

- Yazaki Corporation

- Faurecia (Forvia)

- Desay SV

- Foryou General Electronics

- Hyundai Mobis

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Automaker Race to Deliver Pillar-to-Pillar Cockpit Displays in China and US Premium Segments

- 4.2.2 Regulatory Push for Advanced Driver Assistance Requiring Larger Digital Instrument Clusters in EU

- 4.2.3 Falling OLED Panel ASPs Triggering OEM Adoption in Mid-Range Passenger Cars

- 4.2.4 Semiconductor Mini-LED Backlighting Enhancing Brightness for EVs in High-Temperature Middle-East Markets

- 4.2.5 Consumer Shift Toward In-Vehicle Streaming and Gaming Driving Demand for Above 12-inch Rear Entertainment Screens

- 4.2.6 Integration of Digital Side Mirrors in Japan and South Korea Following Homologation Approvals

- 4.3 Market Restraints

- 4.3.1 OLED Burn-in Reliability Concerns Limiting Deployment in Taxis/Fleet Vehicles

- 4.3.2 Scarcity of IGZO Backplane capacity Causing 2025 Model Year Delays

- 4.3.3 High BOM Cost of Curved Free-Form Displays Hindering Mass-Market Adoption in India and Brazil

- 4.3.4 Cyber-security Compliance Costs Slowing Aftermarket Retrofits

- 4.4 Industry Ecosystem Analysis

- 4.5 Technology Snapshot

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Display Technology

- 5.1.1 a-Si LCD

- 5.1.2 Oxide LCD (IGZO)

- 5.1.3 LTPS LCD

- 5.1.4 OLED (AMOLED, PMOLED)

- 5.1.5 MicroLED

- 5.1.6 Others (E-paper, Mini-LED Backlit)

- 5.2 By Screen Size

- 5.2.1 Upto 5 inch

- 5.2.2 5.1-8 inch

- 5.2.3 8.1-12 inch

- 5.2.4 Above 12 inch

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Light Commercial Vehicles

- 5.3.3 Heavy Commercial Vehicles

- 5.4 By Application

- 5.4.1 Instrument Cluster

- 5.4.2 Center Stack/Infotainment

- 5.4.3 Head-Up Display

- 5.4.4 Rear Seat Entertainment

- 5.4.5 Digital Side/Smart Mirror

- 5.4.6 Others (Roof, HVAC)

- 5.5 By Integration Level

- 5.5.1 Stand-alone Displays

- 5.5.2 Integrated Cockpit/Pillar-to-Pillar

- 5.6 By Touch/Control

- 5.6.1 Touchscreen (capacitive, Resistive)

- 5.6.2 Non-Touch (Display-only)

- 5.7 By Sales Channel

- 5.7.1 OEM-fitted

- 5.7.2 Aftermarket Retrofit

- 5.8 By Geography

- 5.8.1 North America

- 5.8.1.1 United States

- 5.8.1.2 Canada

- 5.8.1.3 Mexico

- 5.8.2 Europe

- 5.8.2.1 Germany

- 5.8.2.2 United Kingdom

- 5.8.2.3 France

- 5.8.2.4 Nordics

- 5.8.2.5 Rest of Europe

- 5.8.3 South America

- 5.8.3.1 Brazil

- 5.8.3.2 Rest of South America

- 5.8.4 Asia-Pacific

- 5.8.4.1 China

- 5.8.4.2 Japan

- 5.8.4.3 India

- 5.8.4.4 South-East Asia

- 5.8.4.5 Rest of Asia-Pacific

- 5.8.5 Middle East and Africa

- 5.8.5.1 Middle East

- 5.8.5.1.1 Gulf Cooperation Council Countries

- 5.8.5.1.2 Turkey

- 5.8.5.1.3 Rest of Middle East

- 5.8.5.2 Africa

- 5.8.5.2.1 South Africa

- 5.8.5.2.2 Rest of Africa

- 5.8.5.1 Middle East

- 5.8.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Vendor Ranking Analysis

- 6.4 Market Share Analysis

- 6.5 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.5.1 LG Display

- 6.5.2 Samsung Display

- 6.5.3 BOE Technology Group

- 6.5.4 AUO Corporation

- 6.5.5 Innolux Corporation

- 6.5.6 Sharp Corporation

- 6.5.7 Japan Display Inc.

- 6.5.8 Tianma Micro-electronics

- 6.5.9 CSOT (TCL China Star)

- 6.5.10 Visionox

- 6.5.11 Truly Semiconductors

- 6.5.12 HKC Corporation

- 6.5.13 Continental AG

- 6.5.14 Denso Corporation

- 6.5.15 Robert Bosch GmbH

- 6.5.16 Visteon Corporation

- 6.5.17 Panasonic Automotive

- 6.5.18 Nippon Seiki

- 6.5.19 Magna International

- 6.5.20 Marelli

- 6.5.21 Yazaki Corporation

- 6.5.22 Faurecia (Forvia)

- 6.5.23 Desay SV

- 6.5.24 Foryou General Electronics

- 6.5.25 Hyundai Mobis

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

軟性透明顯示器市場-全球市場預測(2026-2032年)中控台顯示器市場:按技術、車輛類型、顯示器尺寸、解析度、觸控技術、最終用戶和銷售管道分類——2026-2032年全球市場預測

軟性透明顯示器市場-全球市場預測(2026-2032年)中控台顯示器市場:按技術、車輛類型、顯示器尺寸、解析度、觸控技術、最終用戶和銷售管道分類——2026-2032年全球市場預測 汽車顯示器市場預測至2034年-全球分析(按顯示器類型、顯示技術、螢幕大小、驅動系統、觸控技術、應用和地區分類)汽車顯示系統市場:2026-2032年全球市場預測(依顯示類型、顯示技術、介面技術、連接方式、解析度、車輛類型、最終用戶和銷售管道)

汽車顯示器市場預測至2034年-全球分析(按顯示器類型、顯示技術、螢幕大小、驅動系統、觸控技術、應用和地區分類)汽車顯示系統市場:2026-2032年全球市場預測(依顯示類型、顯示技術、介面技術、連接方式、解析度、車輛類型、最終用戶和銷售管道) 汽車顯示單元市場分析及預測(至2035年):依類型、產品、技術、組件、應用、形狀、材料類型、設備、功能及安裝類型分類

汽車顯示單元市場分析及預測(至2035年):依類型、產品、技術、組件、應用、形狀、材料類型、設備、功能及安裝類型分類 全球汽車顯示系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球汽車顯示系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 汽車顯示器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

汽車顯示器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 汽車顯示器、中控台和儀表板市場(2026 年)

汽車顯示器、中控台和儀表板市場(2026 年) 汽車顯示系統市場規模、佔有率、趨勢和預測:按技術、顯示尺寸、應用、車輛類型、銷售管道和地區分類(2026-2034 年)

汽車顯示系統市場規模、佔有率、趨勢和預測:按技術、顯示尺寸、應用、車輛類型、銷售管道和地區分類(2026-2034 年) 2026年全球動態著色汽車顯示器市場報告

2026年全球動態著色汽車顯示器市場報告