|

市場調查報告書

商品編碼

2063380

汽車顯示器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Automotive Display - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

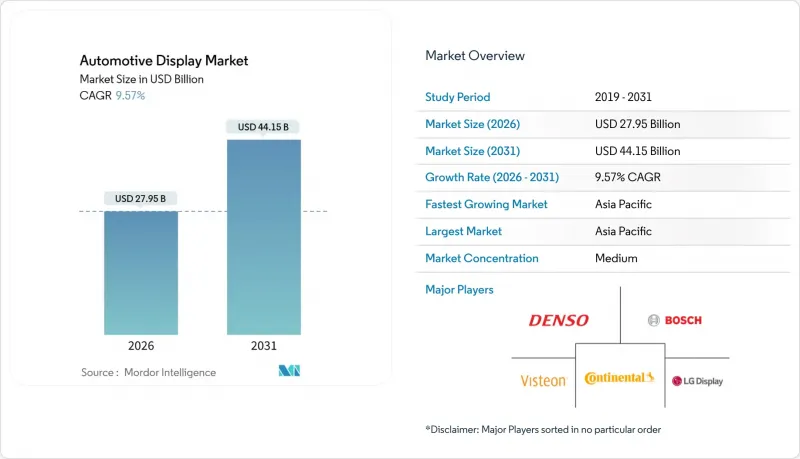

根據 Mordor Intelligence 預測,汽車顯示器市場規模預計將在 2026 年達到 279.5 億美元,到 2031 年達到 441.5 億美元,預測期內複合年成長率為 9.57%。

本報告依產品類型(例如,中控台顯示器、儀錶群顯示器)、顯示技術(例如,液晶顯示器 (LCD)、有機發光二極體(OLED))、車輛類型(乘用車和商用車)、顯示器尺寸(例如,5 吋以下、6-10 吋)和地區進行細分。市場預測以價值(美元)和銷售(台)兩種形式呈現。

全球汽車顯示器市場趨勢及洞察

對整合式數位駕駛座的需求正在激增。

汽車製造商正將儀錶板、資訊娛樂系統和空調控制系統整合到單一的網域控制器中,從而減少佈線並釋放儀表板空間,以便在汽車顯示器市場中容納更大的顯示器。 Viseon在2025年第三季獲得了價值18億美元的先進顯示器和SmartCore駕駛座訂單,這表明整合的軟硬體堆疊如何贏得採購競標。中國電動車製造商比亞迪、蔚來和小鵬正在將12.8吋AMOLED叢集與14-15吋中央顯示器結合,從而提高了全球供應商的基準規格。 LG電子的「數位座艙Alpha」整合了POLED、LCD和AR-HUD,創建了一個與駕駛員監視錄影機協同工作的統一用戶介面。這種架構轉變正在縮小供應商群體,因為基於UNECE R155的韌體和網路安全認證正成為決定供應商合格的越來越重要的因素。 AUTOSAR Adaptive R24-11 進一步簡化了空中 (OTA) 更新,並規範了車輛交付後的駕駛座更新週期。

聯網汽車和電動車的興起,需要更先進的人機互動介面。

電動驅動系統需要視覺化顯示充電狀態、再生煞車和能量流情況,但這些功能在汽車顯示市場中內燃機汽車的儀錶板上卻缺失。隨著中國電動車產量在不久的將來大幅成長,對高解析度旋轉顯示器的需求也日益成長。基於ETSI標準的5G V2X服務的引入,需要更寬廣的HUD視角才能有效地顯示協同駕駛資訊。 Aptiv面向商用車的整合式駕駛座控制器整合了遠端資訊處理和駕駛員監控功能,提供了一種經濟高效的解決方案。 OLED技術憑藉其卓越的對比度和快速響應能力,滿足了高階電動車的可視化需求。電動車和連網技術的進步,以及每輛車平均顯示面積的增加,都在推動市場的成長。

汽車用OLED的價格正在上漲。

汽車級OLED面板的價格遠高於LCD面板。這反映出汽車顯示市場OLED的良率低於消費級OLED。此外,防止燒屏的措施會增加韌體開銷,進而減少有效顯示面積,進一步推高成本。 LG Display正在大力投資建造下一代製造工廠,預計不久將投入運作,旨在大幅降低生產成本。然而,預計需要數年時間才能收回投資。由於成本溢價僅佔豪華車價格的一小部分,因此OLED的應用仍主要集中在豪華車領域,預計未來幾年其在普通市場的滲透率將受到限制。此外,供應商數量有限,例如LG Display、三星顯示器和京東方,也為OEM廠商帶來了供貨量方面的風險。

細分市場分析

截至2025年,中控台螢幕將佔汽車顯示市場40.12%的佔有率,但抬頭顯示器(HUD)的市場佔有率正以10.01%的複合年成長率成長,這主要得益於歐洲新車安全評鑑協會(Euro NCAP)的獎勵。大眾ID.7搭載的大陸集團AR-HUD系統,能夠減少駕駛員將視線轉移到儀表板上的時間,從而顯著提升安全性。叢集。

在中控台市場,中國供應商正大量湧入10.25吋液晶顯示模組,其價格優勢顯著,遠超日韓產品,給利潤空間帶來壓力。然而,由於聯合國歐洲經濟委員會(UNECE)的網路安全法規,歐美汽車製造商(OEM)不願拓展供應商。Panasonic為Subaru開發的眼動追蹤抬頭顯示器(HUD)具備瞳孔大小自動調整亮度的功能,使其在日益同質化的中控台顯示器市場中脫穎而出。預計到2030年,汽車抬頭顯示器市場將顯著成長,其中擴增實境抬頭顯示器(AR-HUD)有望實現最快成長。後排娛樂系統目前仍屬於小眾市場,訂閱費用限制了其普及率,但寶馬推出的31英寸超寬“影院螢幕”表明,豪華車市場對後排娛樂系統存在潛在需求。

液晶顯示(LCD)技術憑藉其低成本和成熟的供應鏈,預計到2025年仍將佔據汽車顯示市場65.13%的佔有率。同時,有機發光二極體(OLED)顯示器以10.64%的複合年成長率成長,主要得益於梅賽德斯-邁巴赫48英寸軟性儀錶板和比亞迪15英寸AMOLED叢集等產品的廣泛應用。而LTPS-LCD技術相比OLED成本更低、解析度更高,預計到2026年將在汽車LCD生產中佔據相當大的佔有率。

正如友達光電即將出貨的先進多區域面板所展示的那樣,Mini-LED 可作為過渡性的高對比度解決方案。而 Micro-LED 目前仍處於商業化前期階段,目前的量產良率不足以滿足汽車產業嚴苛的標準。因此,從技術層級來看,LCD 定位於主流平台,OLED 定位於豪華車,而 Mini-LED 則是一種折衷方案,Micro-LED 預計將在 2028 年後成熟。

區域分析

預計到2025年,亞太地區將引領汽車顯示器市場,佔46.33%的市場佔有率,並將以12.05%的複合年成長率持續成長至2031年。中國電動車的激增正推動駕駛座技術的顯著進步,旋轉螢幕和AR抬頭顯示器等創新技術備受關注。主要顯示器製造商大規模投資產能,以確保國內OEM廠商擁有遠超過西方供應鏈水準的充足庫存。同時,在智慧型手機市場被中國競爭對手蠶食市場佔有率後,日本老牌企業正將重點轉向汽車顯示器領域。這一戰略轉變伴隨著旨在重奪市場佔有率的合作。在韓國,為應對持續的供應鏈挑戰,主要汽車品牌的顯示器生產垂直整合正在穩步推進。

在歐洲和北美,儘管汽車銷售成長放緩,但先進功能的普及速度卻在迅速加快。歐洲的法規正在推動AR抬頭顯示器在各大車型系列中的應用,儘管這導致成本上升。網路安全法規也正在重塑供應商格局,對於缺乏必要認證的新參與企業而言,整合難度更高。在北美,由於缺乏類似的監管政策,相關功能的普及速度落後於歐洲。然而,豪華汽車品牌正積極採用先進的顯示技術,以期達到歐洲的標準。

南美洲、中東和非洲等新興市場蘊藏成長機會。在南美,價格親民的安卓車載主機進入售後市場,推動了改裝市場的活躍度,但監管方面的挑戰限制了其市場滲透。在中東,進口豪華車偏好高階顯示螢幕,但較小的車輛基數限制了市場規模的擴張。在土耳其,商用車生產正在調整以符合歐洲安全標準;而在南非,高關稅限制了高階產品的市場推廣。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場促進因素

- 對整合式數位駕駛座的需求激增

- 聯網汽車和電動車的興起:需要更先進的人機互動介面。

- 原始設備製造商正在推動增大A柱之間的螢幕尺寸。

- 快速降低高亮度汽車液晶顯示器的成本

- NCAP 的分心評分標準正在加速 HUD 的普及。

- 軟體定義車輛 (SDV) OTA 使用者體驗更新周期

- 市場限制因素

- 汽車OLED螢幕採用高價定價

- 玻璃和半導體供應波動

- 網路安全合規成本不斷上升

- 大型軟性顯示器的可靠性挑戰

- 價值/供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 依產品類型

- 中控台顯示螢幕

- 儀表板顯示

- 抬頭顯示器

- 後座娛樂顯示器

- 顯示技術

- 液晶顯示器(LCD)

- 有機發光二極體(OLED)

- MiniLED/MicroLED

- 車輛類型

- 搭乘用車

- 商用車輛

- 按顯示尺寸

- 5英吋或更小

- 6-10英寸

- 10吋或更大

- 按地區

- 北美洲

- 美國

- 加拿大

- 其他北美國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太國家

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 埃及

- 土耳其

- 南非

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- LG Display Co., Ltd.

- Samsung Display Co., Ltd.

- Robert Bosch GmbH

- Continental AG

- Denso Corporation

- Visteon Corporation

- Panasonic Automotive Systems Co., Ltd.

- Nippon Seiki Co., Ltd.

- AUO Corporation

- Japan Display Inc.

- Sharp Corporation

- BOE Technology Group Co., Ltd.

- Hyundai Mobis Co., Ltd.

- Valeo SA

- Tianma Microelectronics Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the automotive display market size stood at USD 27.95 billion in 2026 and is forecast to reach USD 44.15 billion by 2031, translating into a 9.57% CAGR during the forecast period.

This report is Segmented by Product Type (Center Stack Display, Instrument Cluster Display, and More), Display Technology (Liquid Crystal Display (LCD), Organic Light-Emitting Diode (OLED), and More), Vehicle Type (Passenger Cars and Commercial Vehicles), Display Size (≤5-Inch, 6-10 Inch, and More), and Geography. Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Global Automotive Display Market Trends and Insights

Soaring Demand for Integrated Digital Cockpits

Automakers are consolidating instrument clusters, infotainment systems, and climate controls into single domain controllers, reducing wiring mass and freeing up dashboard real estate for larger displays in the automotive display market. Visteon secured USD 1.8 billion in advanced display and SmartCore cockpit orders during Q3 2025, demonstrating how integrated hardware-software stacks win sourcing bids. Chinese EV makers BYD, NIO, and Xpeng have normalized 12.8-inch AMOLED clusters paired with 14-15-inch center screens, raising the baseline specification for global suppliers. LG Electronics' Digital Cockpit Alpha fuses POLED, LCD, and AR-HUD into a unified UI linked to driver-monitoring cameras. The architecture shift compresses the supply base because firmware and cybersecurity credentials under UNECE R155 increasingly define vendor eligibility. AUTOSAR Adaptive R24-11 further streamlines over-the-air (OTA) updates, standardizing cockpit refresh cycles well beyond vehicle delivery.

Rise of Connected and Electric Vehicles Needing Richer HMI

Electric drivetrains require visualizations of charging status, regenerative braking, and energy flow, which are absent in internal-combustion dashboards within the automotive display market. China is expected to significantly increase EV production in the near future, boosting the demand for high-resolution rotating displays. The adoption of 5G-enabled V2X services, standardized under ETSI guidelines, is driving the need for expanded HUD fields of view to effectively display cooperative-driving information. Aptiv's Integrated Cockpit Controller for commercial vehicles integrates telematics and driver monitoring, offering cost-efficient solutions. OLED technology, with its superior contrast ratio and rapid response time, addresses the visualization requirements of premium EVs in the higher price segment. Together, advancements in EVs and connectivity are contributing to an increase in the average display area per vehicle.

Premium Pricing of Automotive-Grade OLEDs

Automotive OLED panels are significantly more expensive than their LCD counterparts, reflecting lower manufacturing yields for OLEDs compared to consumer OLEDs within the automotive display market. Additionally, burn-in mitigation introduces firmware overhead, which reduces the usable area and further increases costs. LG Display is investing heavily in its next-generation manufacturing facility, which is expected to become operational in the near future, aiming to significantly reduce production costs. However, the return on this investment is anticipated to take several years. Since the cost premium represents a small fraction of a luxury car's price, adoption remains concentrated in the luxury segment, with limited penetration in the mass market expected over the next several years. Moreover, the limited number of suppliers, including LG Display, Samsung Display, and BOE, poses volume risks for OEMs.

Other drivers and restraints analyzed in the detailed report include:

- OEM Push for Larger Pillar-to-Pillar Screens

- Rapid Cost-Down of High-Brightness Automotive LCDs

- Glass and Semiconductor Supply Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Center stack screens held a 40.12% share of the automotive display market in 2025; however, Head-Up Display (HUD) shipments are rising at a 10.01% CAGR, driven by Euro NCAP incentives. Continental's AR-HUD on the Volkswagen ID.7 shortens dashboard glance time, adding tangible safety benefits . Instrument clusters, historically analog-digital hybrids, are undergoing 12.3-inch full-digital upgrades in commercial vehicles as EU General Safety Rules demand clear ADAS readouts.

Center stacks face margin compression as Chinese suppliers flood the market with 10.25-inch LCD modules, offering a significant discount to Japanese and Korean units. However, Western OEMs hesitate to dual-source due to UNECE cybersecurity stipulations. Panasonic's eye-tracking HUD for Subaru adapts brightness to pupil dilation, differentiating itself from competitors in an increasingly commoditized center-stack space. The automotive display market size for HUDs is forecast to expand significantly by 2030, with AR-HUD capturing the steepest curve. Rear-seat entertainment remains a niche market, with lower adoption rates restrained by subscription costs, but ultra-wide 31-inch Theatre Screens from BMW suggest pent-up demand for luxury.

Liquid crystal technology maintained a 65.13% share of the automotive display market in 2025, due to its low cost and established supply chain. Organic Light-Emitting Diode (OLED), however, is expanding at 10.64% CAGR, buoyed by Mercedes-Maybach's 48-inch flexible dash and BYD's adoption of 15-inch AMOLED clusters. By delivering high resolutions at a significantly lower cost compared to OLED, LTPS-LCD is expected to dominate a substantial share of the automotive LCD output by 2026.

Mini-LED serves as a temporary high-contrast solution, as demonstrated by AUO's advanced panel featuring numerous zones set to ship soon. While Micro-LED is still in its pre-commercial phase, its current mass-transfer yields result in defects that do not meet the stringent standards required in the automotive industry. Thus, the technological hierarchy positions LCDs for mainstream platforms, OLEDs for luxury cabins, mini-LEDs as a compromise, and anticipates micro-LEDs to mature post-2028.

Geography Analysis

The Asia-Pacific region led with a 46.33% automotive display market share in 2025 and is projected to expand at a 12.05% CAGR through 2031. China's EV surge is driving significant advancements in cockpit technology, with innovations such as rotating screens and AR-HUDs gaining traction. Leading display manufacturers are heavily investing in production capacities to ensure domestic OEMs maintain robust inventory buffers, surpassing the norms seen in Western supply chains. Meanwhile, Japan's established players are shifting their focus to vehicle displays after losing ground in the smartphone market to Chinese competitors. This strategic pivot is accompanied by partnerships aimed at revitalizing their market presence. In South Korea, efforts are underway to vertically integrate display production for key automotive brands, addressing ongoing supply chain challenges.

Europe and North America are witnessing slower growth in vehicle units, but are rapidly adopting advanced features. Regulatory standards in Europe are driving the integration of AR-HUDs across major automotive line-ups, despite the associated cost premiums. Cybersecurity regulations are also reshaping the supplier landscape, increasing the complexity of integration for new entrants without the necessary certifications. In North America, feature adoption lags behind Europe due to the absence of similar regulatory policies. However, premium automotive brands are incorporating advanced display technologies to align with European benchmarks.

Emerging markets in South America and the Middle East & Africa present growth opportunities. In South America, retrofitting activities are gaining momentum as affordable Android head units enter the aftermarket space, although regulatory challenges limit broader adoption. In the Middle East, there is a preference for premium displays in luxury imports, but smaller vehicle bases constrain scalability. Turkey is adapting its commercial vehicle production to meet European safety standards, while in South Africa, high tariffs are restricting adoption to premium segments.

- LG Display Co., Ltd.

- Samsung Display Co., Ltd.

- Robert Bosch GmbH

- Continental AG

- Denso Corporation

- Visteon Corporation

- Panasonic Automotive Systems Co., Ltd.

- Nippon Seiki Co., Ltd.

- AUO Corporation

- Japan Display Inc.

- Sharp Corporation

- BOE Technology Group Co., Ltd.

- Hyundai Mobis Co., Ltd.

- Valeo SA

- Tianma Microelectronics Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Drivers

- 4.1.1 Soaring Demand for Integrated Digital Cockpits

- 4.1.2 Rise of Connected and Electric Vehicles Needing Richer HMI

- 4.1.3 OEM Push for Larger Pillar-to-Pillar Screens

- 4.1.4 Rapid Cost-Down of High-Brightness Automotive LCDs

- 4.1.5 NCAP Distraction-Score Rules Accelerating HUD Fitment

- 4.1.6 Software-Defined Vehicle OTA UX Refresh Cycles

- 4.2 Market Restraints

- 4.2.1 Premium Pricing of Automotive-Grade OLEDs

- 4.2.2 Glass and Semiconductor Supply Volatility

- 4.2.3 Rising Cyber-Security Compliance Costs

- 4.2.4 Reliability Issues with Large Flexible Displays

- 4.3 Value/Supply-Chain Analysis

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Product Type

- 5.1.1 Center Stack Display

- 5.1.2 Instrument Cluster Display

- 5.1.3 Head-Up Display

- 5.1.4 Rear-Seat Entertainment Display

- 5.2 By Display Technology

- 5.2.1 Liquid Crystal Display (LCD)

- 5.2.2 Organic Light-Emitting Diode (OLED)

- 5.2.3 MiniLED / MicroLED

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Commercial Vehicles

- 5.4 By Display Size

- 5.4.1 Less than equal to 5-inch

- 5.4.2 6 to 10 inch

- 5.4.3 Above 10 inch

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Egypt

- 5.5.5.4 Turkey

- 5.5.5.5 South Africa

- 5.5.5.6 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 LG Display Co., Ltd.

- 6.4.2 Samsung Display Co., Ltd.

- 6.4.3 Robert Bosch GmbH

- 6.4.4 Continental AG

- 6.4.5 Denso Corporation

- 6.4.6 Visteon Corporation

- 6.4.7 Panasonic Automotive Systems Co., Ltd.

- 6.4.8 Nippon Seiki Co., Ltd.

- 6.4.9 AUO Corporation

- 6.4.10 Japan Display Inc.

- 6.4.11 Sharp Corporation

- 6.4.12 BOE Technology Group Co., Ltd.

- 6.4.13 Hyundai Mobis Co., Ltd.

- 6.4.14 Valeo SA

- 6.4.15 Tianma Microelectronics Co., Ltd.

7 Market Opportunities & Future Outlook

- 7.1 Growing AR-HUD Monetization Potential

- 7.2 MicroLED Roadmaps Promise 30% Power Savings

- 7.3 Over-the-air Subscription Models for Display-Based Features

- 7.4 China-Centric Cockpit-Display Supply Chain Localization

- 7.5 Aftermarket Retrofit Demand for Screens Above 12-inch in Developing Markets

軟性透明顯示器市場-全球市場預測(2026-2032年)中控台顯示器市場:按技術、車輛類型、顯示器尺寸、解析度、觸控技術、最終用戶和銷售管道分類——2026-2032年全球市場預測

軟性透明顯示器市場-全球市場預測(2026-2032年)中控台顯示器市場:按技術、車輛類型、顯示器尺寸、解析度、觸控技術、最終用戶和銷售管道分類——2026-2032年全球市場預測 汽車顯示器市場預測至2034年-全球分析(按顯示器類型、顯示技術、螢幕大小、驅動系統、觸控技術、應用和地區分類)汽車顯示系統市場:2026-2032年全球市場預測(依顯示類型、顯示技術、介面技術、連接方式、解析度、車輛類型、最終用戶和銷售管道)

汽車顯示器市場預測至2034年-全球分析(按顯示器類型、顯示技術、螢幕大小、驅動系統、觸控技術、應用和地區分類)汽車顯示系統市場:2026-2032年全球市場預測(依顯示類型、顯示技術、介面技術、連接方式、解析度、車輛類型、最終用戶和銷售管道) 汽車顯示單元市場分析及預測(至2035年):依類型、產品、技術、組件、應用、形狀、材料類型、設備、功能及安裝類型分類

汽車顯示單元市場分析及預測(至2035年):依類型、產品、技術、組件、應用、形狀、材料類型、設備、功能及安裝類型分類 全球汽車顯示系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球汽車顯示系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 汽車顯示面板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

汽車顯示面板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 汽車顯示器、中控台和儀表板市場(2026 年)

汽車顯示器、中控台和儀表板市場(2026 年) 汽車顯示系統市場規模、佔有率、趨勢和預測:按技術、顯示尺寸、應用、車輛類型、銷售管道和地區分類(2026-2034 年)

汽車顯示系統市場規模、佔有率、趨勢和預測:按技術、顯示尺寸、應用、車輛類型、銷售管道和地區分類(2026-2034 年) 2026年全球動態著色汽車顯示器市場報告

2026年全球動態著色汽車顯示器市場報告