|

市場調查報告書

商品編碼

2066743

薄膜電池:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Thin Film Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

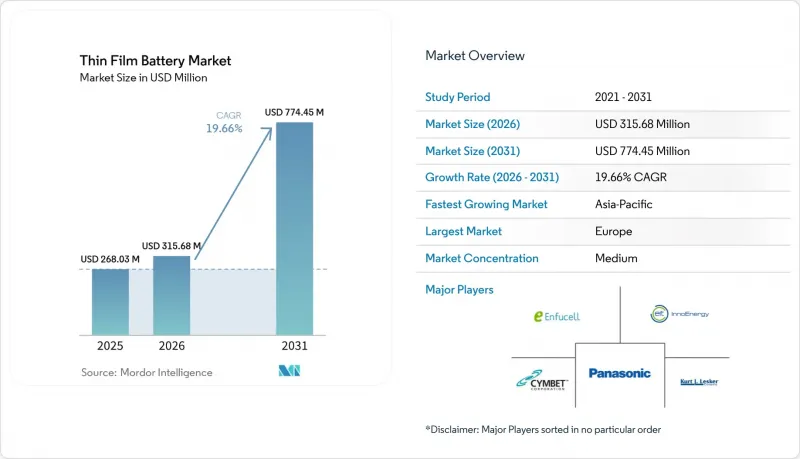

根據 Mordor Intelligence 預測,薄膜電池市場規模將從 2025 年的 2.6803 億美元和 2026 年的 3.1568 億美元成長到 2031 年的 7.7445 億美元,2026 年至 2031 年的年複合成長率(CAGR)。

本報告按電池類型(可充電電池、不可充電電池)、技術(印刷電池、陶瓷電池及其他技術)、應用領域(家用電子電器、醫療設備、穿戴式技術、智慧卡、RFID 及其他)和地區(北美、歐洲、亞太、南美以及中東和非洲)進行細分。市場預測以美元計價。

全球薄膜電池市場趨勢及洞察

穿戴式裝置和物聯網設備的產量迅速成長

智慧型手錶、耳機、服務機器人和工業感測器等產品的全球出貨量不斷成長,推動了容量小於1安時的平面電池需求持續上升。 TDK推出的薄膜電感器最初應用於真無線立體聲耳機,它無需傳統的紐扣電池,尤其適用於空間寸土寸金(小至立方毫米)的設備。這款電感器可在25分鐘內充電90%,讓設備無需笨重機殼即可日常佩戴。三星SDI預測,機器人需求將從2025年的50萬台成長到2030年的204萬台,並已發表固體軟包電池以滿足這項需求激增。諸如Dracula Technologies的LayerVault OPV薄膜等能源採集模組,可補充物流感測器的間歇性電源,從而拓展薄膜電池在消費和工業領域的市場。環境光採集器和軟性微型電池的協同作用,正在推動溫度記錄器和資產標籤中CR2032電池的替代品。

家用電子電器小型化趨勢

設備製造商的目標是將智慧卡、AR眼鏡和生物識別標籤的機殼厚度控制在5毫米以下,這需要轉向扁平電池。 BTRY的1S4P電池就是一個創新典範,它厚度僅0.1毫米,容量為50mAh,充電時間僅需1分鐘,從而實現了ID卡的主動安全認證。扁平電池直接層壓到軟性電路基板,無需使用焊線夾具,縮短了組裝時間,即使體積能量密度低於18650標準,也能為OEM廠商帶來極具吸引力的總體擁有成本(TCO)。這種設計靈活性使得智慧型手錶背面可以採用曲面設計,並可實現無邊框顯示螢幕,同時保持設備的剛性。由於其工作模式是間歇性的而非連續性的,消費者為了更輕的穿戴式設備,可以接受每天充電,這推動了薄膜電池市場的重複訂單成長。

與大型鋰離子電池相比,能量密度受限

薄膜電池的能量密度為100–200 Wh/L,約為目前能量密度接近320 Wh/kg的先進21,700圓柱形電池的三分之一。 LiPON的離子電導率仍維持在10⁻⁶ S/cm的水平,限制了其放電速率,使其難以在電動工具中得到應用。隨著矽-石墨負極在電動車電池組中的應用,性能差距進一步擴大,使得薄膜電池難以在需要長時間運行和高放電電流的領域獲得市場佔有率。智慧型手錶製造商為了實現數天的連續運作,不得不重新採用紐扣電池;而AR頭戴裝置的OEM製造商則開始使用小型鋰聚合物軟包電池作為輔助電源。複合電解質的研發有望使電導率提高一倍,但由於商業化預計要到2027年後才能實現,因此在目前的預測期內不太可能取得顯著改進。

細分市場分析

預計到2025年,可充電薄膜電池將佔薄膜電池銷售額的73.57%,複合年成長率達20.69%,進一步鞏固其在薄膜電池市場的主導地位。智慧型手錶、人形機器人和醫療植入等需要數千次充電循環的應用,使得這個細分市場受益匪淺。三星SDI的「SolidStack」原型產品可使服務機器人實現8小時的運作週期,從而在換班期間實現快速充電。雖然由於其經濟優勢(每個標籤的成本僅為幾美分),不可充電一次電池仍被用於一次性智慧包裝,但隨著物聯網設備營運商逐漸認知到可充電電池的生命週期成本優勢,其在薄膜電池市場的佔有率正在萎縮。

ISO/IEC 7810耐久性測試和UN 38.3運輸認證正在塑造藍圖,迫使供應商檢驗其熱穩定性超過1000次循環,保存期限超過5年。在國防後勤領域,STUB標準採用可充電形式,顯著減少了運往戰場的電池數量,因此發展勢頭更加強勁。由此,薄膜電池產業正集中研發預算改善LiPON技術,並透過無負極堆疊設計延長循環壽命,進一步鞏固二次電池化學公司的市場佔有率優勢。

區域分析

預計到2025年,歐洲將佔薄膜電池市場收入的52.11%。歐盟電池法規(2023/1542)為此提供了支持,該法規將強制要求披露碳足跡,並從2027年起引入電池護照制度。瑞士公司BTRY已籌集570萬美元用於無溶劑捲對捲固態電池的產業化,展現了該地區深科技的活力。法國ITEN和英國電池產業化中心已將Ilika公司「Goliath」原型電池在試生產線上的良率提高至93%,確保了穩定的供應。北歐製造商正大力推廣水力發電,以凸顯其低碳特性,但鋰和鈷的開採許可仍是限制其發展的瓶頸。

亞太地區是成長的主要驅動力,年複合成長率高達22.35%,正在重塑薄膜電池的市場格局。三星SDI在2026年國際電池技術展覽會(InterBattery 2026)上發布了一款用於人形機器人的軟包式全固態電池原型,並擁有約1100項專利,從而進一步鞏固了其競爭優勢。中國正在「中國製造2025」補貼計畫的支持下,擴大用於互聯封裝的印刷電池的生產;同時,日本TDK公司正在將陶瓷電池商業化,用於工業電子產品。隨著生產基地從中國向外多元化,越南和泰國正在吸引組裝能,但上游原料仍集中在東北亞地區。

北美在薄膜電池的國防和醫療技術領域佔據主導地位。美國國防高級研究計劃局 (DARPA) 的資助和矽谷新創企業的湧現,正推動著穩定的需求成長。同時,Amprius 公司根據《國防授權法案》(NDAA) 正在建造的矽負極製造工廠,預示著一旦薄膜電池技術成熟,回歸國內生產將產生協同效應。在南美洲,耐高溫陶瓷薄膜電池正被應用於巴西的智慧農業先導計畫和中東油田的物聯網部署。在非洲,儘管可再生能源驅動的微電網仍處於發展初期,但其未來可能對感測器產生需求,進而帶動對高柔軟性微型電池的需求成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 穿戴式裝置和物聯網設備的產量迅速成長

- 家用電子電器小型化趨勢

- 醫療植入對固體微型電池的需求日益成長

- 透過擴大卷對卷PVD製程規模降低單位成本

- 與具備能源採集功能的工業物聯網感測器整合

- 國防預算用於士兵佩戴的電源和智慧彈藥。

- 市場限制因素

- 替代電池化學系統的可用性

- 低能量密度鋰離子電池與大容量鋰離子電池的比較

- 真空沉澱設備的高資本投資成本

- LiPON電解專利瓶頸

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 依電池類型

- 可充電的

- 不可充電(一次電池)

- 透過技術

- 印刷電池

- 陶瓷電池

- 鋰聚合物電池

- 固體晶片電池

- 其他技術

- 透過使用

- 家用電子產品

- 醫療器材

- 穿戴式科技

- 智慧卡

- RFID

- 物聯網感測器

- 軍事/國防

- 智慧包裝

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 北歐國家

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 澳洲和紐西蘭

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 埃及

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略性舉措(併購、合資、資金籌措)

- 市場排名和佔有率分析

- 公司簡介

- STMicroelectronics

- Panasonic Corporation

- Samsung SDI Co., Ltd.

- Cymbet Corporation

- BrightVolt Inc.

- Ilika plc

- Imprint Energy, Inc.

- Enfucell Oy

- Kurt J. Lesker Company

- Blue Spark Technologies

- Front Edge Technology

- Thinfilm Electronics ASA

- BASQUEVOLT

- EIT InnoEnergy SE

- The Batteries Sp. z oo

- Renata SA

- Power Paper Ltd.

- VARTA AG

- EnerVenue Inc.

- NEO Battery Materials Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the thin film battery market size is projected to expand from USD 268.03 million in 2025 and USD 315.68 million in 2026 to USD 774.45 million by 2031, registering a CAGR of 19.66% between 2026 and 2031.

This report is Segmented by Battery Type (Rechargeable, Non-Rechargeable), Technology (Printed Battery, Ceramic Battery, Other Technologies), Application (Consumer Electronics, Medical Devices, Wearable Technology, Smart Cards, RFID, Others), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Thin Film Battery Market Trends and Insights

Surge in Wearable & IoT Device Production

Global shipments of smartwatches, earbuds, service robots, and industrial sensors are creating sustained pull for sub-1 Ah planar cells. TDK's thin-film inductors introduced for true-wireless-stereo earbuds make mechanical coin cells obsolete in devices where every cubic millimeter counts. Ensure batteries reach 90% charge in under 25 minutes, supporting daily-wear gadgets without bulky housings. Samsung SDI forecasts robot demand rising from 500,000 units in 2025 to 2.04 million by 2030, and it unveiled a solid-state pouch cell to serve that wave. Energy-harvesting modules such as Dracula Technologies' LayerVault OPV sheets buffer intermittent power for logistics sensors, lifting thin film battery market volumes across consumer and industrial use cases. The synergy between ambient-light harvesters and flexible micro-cells underpins the replacement of CR2032 batteries in temperature loggers and asset tags.

Miniaturization Trend in Consumer Electronics

Device makers are setting chassis thickness targets below 5 mm for smart cards, AR glasses, and biometric tags, forcing a pivot to flat battery geometries. BTRY's 1S4P cell, barely 0.1 mm thick yet delivering 50 mAh in one-minute charges, exemplifies innovation that unlocks active security authentication inside ID cards. Planar cells laminate directly onto flex circuits, skip wire-bond fixtures, and cut assembly time, giving OEMs a compelling cost-of-ownership story even when volumetric energy is lower than 18650 standards. The design freedom enables curved smartwatch backs and bezel-less displays while maintaining device rigidity. Because the operating profile is intermittent rather than continuous, consumers accept daily re-charging in exchange for lighter wearables, driving repeat orders across the thin film battery market.

Limited Energy Density Versus Bulk Li-ion Batteries

Thin-film cells provide 100-200 Wh/L, about one-third of advanced 21700 cylindrical formats now touching 320 Wh/kg. Ionic conductivity in LiPON remains at the 10-6 S/cm level, capping discharge rates and precluding use in power tools. As EV-grade packs adopt silicon-graphite anodes, the performance contrast widens, making it harder for the thin film battery market to win long-duration or high-drain slots. Smartwatch makers chasing multiday runtimes sometimes revert to coin cells, and AR headset OEMs blend small lithium-polymer pouches for auxiliary loads. Composite electrolyte R&D could double conductivity, yet commercialization after 2027 offers no relief during the current forecast window.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Solid-State Micro-Batteries in Medical Implants

- Roll-to-Roll PVD Scale-Ups Reducing Per-Unit Costs

- High CAPEX for Vacuum Deposition Tooling

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Rechargeable thin-film cells accounted for 73.57% of 2025 revenue and are forecast to grow at 20.69% CAGR, reinforcing their dominance in the thin film battery market. This cohort benefits from smartwatch, humanoid-robot, and medical-implant workloads that demand thousands of charge cycles. Samsung SDI's SolidStack prototypes deliver eight-hour duty cycles in service robots and promise fast top-ups during shift changes. Non-rechargeable primary cells still power disposable smart packaging where unit economics dictate pennies per label, yet their share in the thin film battery market is shrinking as IoT device operators calculate life-cycle cost advantages of rechargeability.

ISO/IEC 7810 durability tests and UN 38.3 transport certification shape R&D roadmaps, pushing vendors to validate thermal stability above 1,000 cycles and shelf life beyond five years. Defense logistics add momentum as the STUB standard adopts rechargeable formats to slash field battery shipments. Consequently, the thin film battery industry is funneling R&D budgets toward cycle-life extension through LiPON refinement and anode-free stack designs, reinforcing the share supremacy of secondary chemistries.

Geography Analysis

Europe generated 52.11% of thin film battery market revenue in 2025, underpinned by the EU Batteries Regulation (2023/1542) that enforces carbon-footprint disclosure and battery passports from 2027. Switzerland's BTRY raised USD 5.7 million to industrialize solvent-free roll-to-roll solid-state cells, showing deep-tech vigor in the region. France's ITEN and the UK's Battery Industrialisation Centre pushed Ilika's Goliath prototypes toward 93% pilot-line yield, anchoring supply resilience. Nordic producers tout hydropower-sourced electricity for low-carbon credentials, but mining permits for lithium and cobalt remain a bottleneck.

Asia-Pacific is the momentum engine, expanding at 22.35% CAGR and reshaping the thin film battery market landscape. Samsung SDI presented a pouch-type all-solid-state prototype for humanoid robots at InterBattery 2026 and owns about 1,100 patents, fortifying its moat. China scales printed-battery output for connected packaging under Made in China 2025 subsidies, while Japan's TDK commercializes ceramic variants for industrial electronics. Vietnam and Thailand lure assembly capacity as diversification away from China accelerates, although upstream materials remain concentrated in Northeast Asia.

North America captures defense and med-tech niches within the thin film battery market. DARPA funding and Silicon Valley start-ups provide steady demand, while Amprius' silicon-anode facility under NDAA alignment hints at onshoring synergies should thin-film versions mature. South America's pilot projects in Brazilian smart agriculture and the Middle East's oil-field IoT deployments use ceramic thin-film batteries for high-temperature resilience. Africa remains embryonic, though renewable-energy micro-grids may later seed sensor demand that benefits flexible micro-batteries.

- STMicroelectronics

- Panasonic Corporation

- Samsung SDI Co., Ltd.

- Cymbet Corporation

- BrightVolt Inc.

- Ilika plc

- Imprint Energy, Inc.

- Enfucell Oy

- Kurt J. Lesker Company

- Blue Spark Technologies

- Front Edge Technology

- Thinfilm Electronics ASA

- BASQUEVOLT

- EIT InnoEnergy SE

- The Batteries Sp. z o. o.

- Renata SA

- Power Paper Ltd.

- VARTA AG

- EnerVenue Inc.

- NEO Battery Materials Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in wearable & IoT device production

- 4.2.2 Miniaturization trend in consumer electronics

- 4.2.3 Rising demand for solid-state micro-batteries in medical implants

- 4.2.4 Roll-to-roll PVD scale-ups reducing per-unit costs

- 4.2.5 Integration with energy-harvesting IIoT sensors

- 4.2.6 Defense funding for soldier-worn power sources & smart munitions

- 4.3 Market Restraints

- 4.3.1 Availability of alternative battery chemistries

- 4.3.2 Limited energy density versus bulk Li-ion batteries

- 4.3.3 High CAPEX for vacuum deposition tooling

- 4.3.4 LiPON electrolyte patent bottlenecks

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products & Services

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Battery Type

- 5.1.1 Rechargeable

- 5.1.2 Non-Rechargeable (Primary)

- 5.2 By Technology

- 5.2.1 Printed Battery

- 5.2.2 Ceramic Battery

- 5.2.3 Lithium-Polymer Battery

- 5.2.4 Solid-State Chip Battery

- 5.2.5 Other Technologies

- 5.3 By Application

- 5.3.1 Consumer Electronics

- 5.3.2 Medical Devices

- 5.3.3 Wearable Technology

- 5.3.4 Smart Cards

- 5.3.5 RFID

- 5.3.6 IoT Sensors

- 5.3.7 Military & Defense

- 5.3.8 Smart Packaging

- 5.3.9 Others

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Spain

- 5.4.2.5 Nordic Countries

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 ASEAN Countries

- 5.4.3.6 Australia and New Zealand

- 5.4.3.7 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Egypt

- 5.4.5.5 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, JV, Funding)

- 6.3 Market Ranking/Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 STMicroelectronics

- 6.4.2 Panasonic Corporation

- 6.4.3 Samsung SDI Co., Ltd.

- 6.4.4 Cymbet Corporation

- 6.4.5 BrightVolt Inc.

- 6.4.6 Ilika plc

- 6.4.7 Imprint Energy, Inc.

- 6.4.8 Enfucell Oy

- 6.4.9 Kurt J. Lesker Company

- 6.4.10 Blue Spark Technologies

- 6.4.11 Front Edge Technology

- 6.4.12 Thinfilm Electronics ASA

- 6.4.13 BASQUEVOLT

- 6.4.14 EIT InnoEnergy SE

- 6.4.15 The Batteries Sp. z o. o.

- 6.4.16 Renata SA

- 6.4.17 Power Paper Ltd.

- 6.4.18 VARTA AG

- 6.4.19 EnerVenue Inc.

- 6.4.20 NEO Battery Materials Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment

薄膜電池市場機會、成長要素、產業趨勢分析及2026-2035年預測。

薄膜電池市場機會、成長要素、產業趨勢分析及2026-2035年預測。 薄膜電池市場規模、佔有率、趨勢和預測:按技術、電池類型、電壓類型、應用和地區分類,2026-2034年

薄膜電池市場規模、佔有率、趨勢和預測:按技術、電池類型、電壓類型、應用和地區分類,2026-2034年 薄膜電池市場:市場規模、佔有率、成長率、全球產業分析、按類型、應用和地區分類的分析以及未來預測(2026-2034 年)

薄膜電池市場:市場規模、佔有率、成長率、全球產業分析、按類型、應用和地區分類的分析以及未來預測(2026-2034 年) 軟性、印刷和薄膜電池市場分析及預測(至2035年):按類型、產品類型、技術、應用、材料類型、裝置、製程、最終用戶、功能和安裝類型分類全球薄膜電池市場規模、佔有率、趨勢和成長分析報告(2026-2034)

軟性、印刷和薄膜電池市場分析及預測(至2035年):按類型、產品類型、技術、應用、材料類型、裝置、製程、最終用戶、功能和安裝類型分類全球薄膜電池市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2026年全球印刷薄膜電池市場報告

2026年全球印刷薄膜電池市場報告 薄膜電池市場-全球產業規模、佔有率、趨勢、機會和預測,按電池類型、電壓、應用、地區和競爭格局分類,2021-2031年預測軟性印刷薄膜電池市場-全球產業規模、佔有率、趨勢、機會及預測(按電池類型、應用、地區和競爭格局分類,2021-2031年預測)

薄膜電池市場-全球產業規模、佔有率、趨勢、機會和預測,按電池類型、電壓、應用、地區和競爭格局分類,2021-2031年預測軟性印刷薄膜電池市場-全球產業規模、佔有率、趨勢、機會及預測(按電池類型、應用、地區和競爭格局分類,2021-2031年預測) 可充電薄膜電池市場規模、佔有率及成長分析(按技術、電解液類型、應用和地區分類)-2026-2033年產業預測

可充電薄膜電池市場規模、佔有率及成長分析(按技術、電解液類型、應用和地區分類)-2026-2033年產業預測 全球軟性、印刷和薄膜電池市場:市場規模、市場佔有率、趨勢分析(按類型、應用和地區)、展望和未來預測(2024-2031 年)

全球軟性、印刷和薄膜電池市場:市場規模、市場佔有率、趨勢分析(按類型、應用和地區)、展望和未來預測(2024-2031 年)