|

市場調查報告書

商品編碼

2066724

中東和北非油田服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Middle East and North Africa Oilfield Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

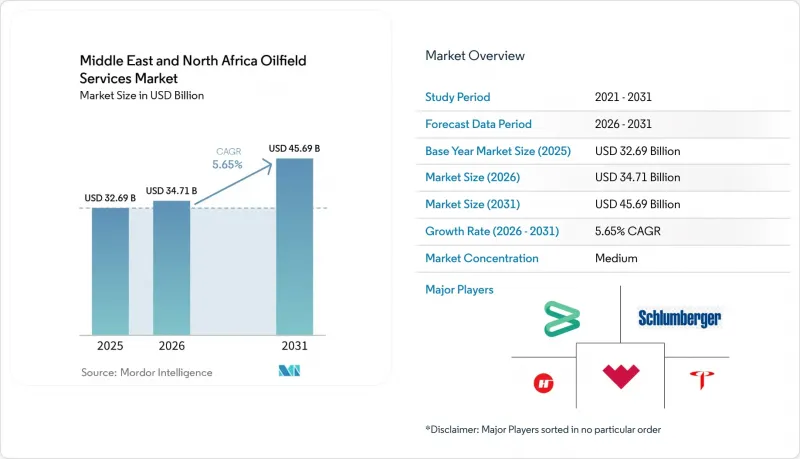

據 Mordor Intelligence 稱,2025 年中東和北非油田服務市場價值為 326.9 億美元,預計到 2031 年將達到 456.9 億美元,而 2026 年為 347.1 億美元,預測期(2026-2031 年)的複合年成長率為 5.65%。

本報告依服務類型(鑽井服務、完井服務及其他服務)、施行地點(陸上、海上)、井型(傳統型、傳統型)和地區(沙烏地阿拉伯、阿拉伯聯合大公國、卡達、科威特、阿爾及利亞、埃及、利比亞、摩洛哥以及其他中東和非洲國家)進行分類。市場預測以美元計價。

中東和北非油田服務市場趨勢與洞察

到 2030 年,探勘和生產 (E&P) 預算將達到 1,430 億美元,這將促進鑽探活動的增加。

在2025年至2030年間1,430億美元的全部區域探勘與生產(E&P)預算的支持下,國際能源總署(IEA)預測,陸上鑽機數量將比過去五年增加31%。光是沙烏地阿美就承諾投入70億美元,以確保2025年680座鑽機維持運作,凸顯了中東和北非油田服務市場對持續鑽井活動的依賴。阿爾及利亞正透過撥款600億美元用於1,450口旨在開採緻密氣蘊藏量的油井,擴大在北非的服務需求。科威特正投資39億美元用於第二階段海上探勘,目標是2035年開採45億桶油當量(BOE),實現日增產15萬桶。在高壓高溫區域,單井成本可能超過2000萬美元,因此對高品質鑽柱、泥漿錄井和控壓鑽井系統的需求日益成長。這筆資金的投資在過去幾年中增強了中東和北非油田服務市場的訂單儲備,獎勵承包商擴充設備和本地維修車間。

加速推進以天然氣開發為重點的大型企劃(JAFLA、北方氣田)

沙烏地阿美投資1,000億美元的賈夫拉計畫計畫在2030年實現日產20億立方英尺天然氣,這需要連續水平鑽井和密集的多級壓裂作業。斯倫貝謝公司獲得了一份價值數十億美元、為期五年的刺激性契約,重新定義了中東和北非油田服務市場對已完成建設服務的需求。卡達北田東西兩期工程將使液化天然氣產能在2030年達到每年1.42億噸,從而催生對長週期海底生產設施、管道和住宿船的需求。儘管Technip FMC、Saipem和中國船廠的訂單確保了製造檔期,但進度風險也高度集中。天然氣處理裝置的延誤可能導致鑽井鑽機運作,並造成整個服務鏈的成本超支。這些大型企劃是支撐中東和北非油田服務市場規模前景的支柱,但同時也增加了試運行里程碑的風險。

原油價格波動與歐佩克+產量配額

歐佩克+預計將繼續減產324萬桶/日,至2026年,4月僅增產20.6萬桶/日。 2026年第一季,布蘭特原油價格將在每桶70至85美元之間波動,這一價格區間既能支持維護性資本支出,又能抑制高成本地區超深水和緻密油的探勘。產量配額制度迫使成員國優先考慮價值而非數量,從而推遲對獲利能力較弱油田的最終投資決策,並抑制對短期鑽井鑽機的需求。簽訂固定費率船隊合約的服務公司將承受運轉率波動帶來的影響,而採用績效掛鉤定價模式的公司則能部分抵禦下行風險。這些限制將使中東和北非油田服務市場的區域成長率下降至多0.9個百分點。

細分市場分析

2025年,鑽井服務在中東和北非油田服務市場中佔據38.9%的佔有率。這主要得益於沙烏地阿美陸上鑽井鑽機的擴張以及卡達的海洋評估宣傳活動。同時,生產和介入服務預計將以7.7%的年均成長率成長,這反映了成熟油田人工開採設施的維修、撓曲油管作業以及即時監測的開展。中東和北非油田服務市場的增產合約規模正在擴大。光是傑夫拉油田到2030年就需要1000口水平井,每口井都需要多級壓裂和支撐劑物流。雖然西方大型企業主導高科技完工建設領域,但區域承包商正在通用水泥灌漿和井口設備的製造領域競爭。其他服務,如地震探勘、海上物流、航空以及新興的退役行業,都對收入起到了補充作用,並且由於埃及計劃在 2026 年鑽探 101 口探勘井以及阿爾及利亞 24 個區塊的競標,這些服務得到了促進。

平行競爭的動態正在影響價格形成。傳統型油田的績效計費完井合約價格較高,而由於不確定性,北非地區中等深度陸上油井的成本驅動趨勢仍在持續,這有利於擁有本地供應鏈的承包商。從2026年到2031年,中東和北非油田服務市場中,生產和乾預領域的成長率將最高,但鑽井領域仍將是最大的絕對收入來源,這反映了該地區極高的鑽機密度。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 到 2030 年,探勘開發預算將達到 1,430 億美元,這將支持鑽探活動的增加。

- 加速以天然氣為重點的大型企劃(JAFRA、北方氣田)

- 國有石油公司本地化要求正在推動服務競標。

- 引進數位化油田(人工智慧鑽機、即時儲存液位監測)

- 發現需要高規格服務的超深、高壓、高溫(HP/HT)油田。

- 早期碳捕獲和氫能試點計畫正在創造小眾服務需求。

- 市場限制因素

- 原油價格波動與歐佩克+產量配額

- 地緣政治衝突點與製裁風險

- 在地採購限制正在擠壓外國公司的利潤空間。

- 下一代數位鑽機領域熟練人員嚴重短缺。

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 按服務類型

- 鑽井服務

- 完井服務(注水泥、水力壓裂)

- 生產和乾預服務

- 其他服務(海上支援船、地震探勘、退役、航空)

- 按位置

- 陸上

- 離岸

- 按井類型

- 傳統的

- 傳統型

- 按地區

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 卡達

- 科威特

- 阿爾及利亞

- 埃及

- 利比亞

- 摩洛哥

- 中東和北非其他地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- Schlumberger

- Halliburton

- Baker Hughes

- China Oilfield Services(COSL)

- Weatherford International

- Transocean

- Valaris

- Nabors Industries

- Expro Group

- National Energy Services Reunited(NESR)

- Saipem

- Petrofac

- KCA Deutag

- Arabian Drilling

- Shelf Drilling

- Maersk Drilling

- TechnipFMC

- CGG

- NOV(National Oilwell Varco)

- Halliburton Company

第7章 市場機會與未來展望

According to Mordor Intelligence, the middle east and North Africa Oilfield Services Market size was valued at USD 32.69 billion in 2025 and is estimated to grow from USD 34.71 billion in 2026 to reach USD 45.69 billion by 2031, at a CAGR of 5.65% during the forecast period (2026-2031).

This report is Segmented by Service Type (Drilling Services, Completion Services, Other Services), Location (Onshore, Offshore), Well Type (Conventional, Unconventional), and Geography (Saudi Arabia, UAE, Qatar, Kuwait, Algeria, Egypt, Libya, Morocco, Rest of Middle East and North Africa). The Market Forecasts are Provided in Terms of Value (USD).

Middle East and North Africa Oilfield Services Market Trends and Insights

Rising Drilling Activity Backed by USD 143 Billion E&P Budgets Through 2030

Regional exploration and production budgets of USD 143 billion for 2025-2030 underpin a land-rig count that the International Energy Agency expects to climb 31% over the prior five-year span. Saudi Aramco alone committed USD 7 billion in 2025 to keep 680 rigs active, accentuating the Middle East & North Africa oilfield services market's dependence on sustained drilling intensity. Algeria earmarked USD 60 billion for 1,450 wells targeting tight-gas prospects, extending service demand into North Africa. Kuwait is channeling USD 3.9 billion into offshore Phase 2 exploration to unlock 4.5 billion BOE and add 150,000 bpd by 2035. High-pressure, high-temperature zones, where a single well can cost over USD 20 million, amplify requirements for premium drillstrings, mud-logging, and managed-pressure drilling systems. These allocations reinforce a multi-year backlog across the Middle East & North Africa oilfield services market, incentivizing contractors to expand fleets and local workshops.

Accelerated Gas-Focused Megaprojects (Jafurah, North Field)

Saudi Aramco's USD 100 billion Jafurah program targets 2 bcf/d of sales gas by 2030, necessitating continuous horizontal drilling and intensive multi-stage fracturing. Schlumberger captured a multi-billion-dollar five-year stimulation contract that redefines completion-service intensity in the Middle East & North Africa oilfield services market. Qatar's North Field East and West phases will lift LNG capacity to 142 mtpa by 2030, creating long-cycle subsea-tree, pipeline, and accommodation-vessel demand. Awards to TechnipFMC, Saipem, and Chinese yards secure fabrication slots yet concentrate schedule risk: delays in gas-processing trains can idle rigs and spread cost overruns across the service chain. These megaprojects anchor the Middle East & North Africa oilfield services market size outlook, but they also heighten exposure to commissioning milestones.

Oil-Price Volatility and OPEC+ Production Quotas

OPEC+ carried 3.24 million bpd of cuts into 2026, adding only a 206,000 bpd uptick for April. Brent traded between USD 70 and USD 85 per barrel in Q1 2026, a band that supports maintenance capital but discourages ultra-deepwater or tight-oil exploration in high-cost areas. Quota discipline presses member states to prioritize value over volume, postponing marginal field final-investment decisions and dampening short-cycle rig demand. Service companies with fixed-rate fleet contracts shoulder utilization swings, whereas those with performance-linked pricing secure partial downside protection. The constraint subtracts up to 0.9 percentage points from the regional growth trajectory of the Middle East & North Africa oilfield services market.

Other drivers and restraints analyzed in the detailed report include:

- National Oil Companies' Localization Mandates Boosting Service Tenders

- Digital-Oilfield Adoption (AI Rigs, Real-Time Reservoirs)

- Geopolitical Flashpoints and Sanctions Risk

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Drilling services retained 38.9% of the Middle East and North Africa oilfield services market share in 2025, driven by Saudi Aramco's land-rig fleet expansion and Qatar's offshore appraisal campaigns. Yet production and intervention services are forecast to grow at 7.7% annually, reflecting artificial-lift retrofits, coiled-tubing jobs, and real-time surveillance across maturing assets. The Middle East & North Africa oilfield services market size for stimulation contracts is rising as Jafurah alone will require 1,000 horizontal wells by 2030, each demanding multi-stage fracturing and proppant logistics. Western majors capture high-tech completion scopes, while regional contractors compete on commodity cementing and wellhead fabrication. Other services, seismic, marine logistics, aviation, and nascent decommissioning, round out revenue, buoyed by Egypt's 101 exploration wells in 2026 and Algeria's 24-block bid round.

Parallel competitive dynamics shape pricing: performance-based completion contracts in unconventional plays fetch premiums, whereas drilling day-rates remain range-bound by OPEC+ quota uncertainty. High-pressure, high-temperature projects off the UAE and Kuwait's Mutriba field require specialized drilling fluids and downhole tools, allowing suppliers to command higher margins. In contrast, mid-depth land wells across North Africa stay cost-focused, favoring contractors with localized supply chains. Over 2026-2031, the Middle East & North Africa oilfield services market sees the fastest percentage growth in production and intervention, but drilling retains the largest absolute revenue pool, reflecting the region's sheer rig intensity.

List of Companies Covered in this Report:

- Schlumberger

- Halliburton

- Baker Hughes

- China Oilfield Services (COSL)

- Weatherford International

- Transocean

- Valaris

- Nabors Industries

- Expro Group

- National Energy Services Reunited (NESR)

- Saipem

- Petrofac

- KCA Deutag

- Arabian Drilling

- Shelf Drilling

- Maersk Drilling

- TechnipFMC

- CGG

- NOV (National Oilwell Varco)

- Halliburton Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising drilling activity backed by $143 bn E&P budgets through 2030

- 4.2.2 Accelerated gas-focused megaprojects (Jafurah, North Field)

- 4.2.3 National oil companies' localisation mandates boosting service tenders

- 4.2.4 Digital-oilfield adoption (AI rigs, real-time reservoirs)

- 4.2.5 Ultra-deep HP/HT discoveries demanding high-spec services

- 4.2.6 Early carbon-capture & hydrogen pilots creating niche service demand

- 4.3 Market Restraints

- 4.3.1 Oil-price volatility and OPEC+ production quotas

- 4.3.2 Geopolitical flashpoints & sanctions risk

- 4.3.3 Local-content rules squeezing foreign firms' margins

- 4.3.4 Critical talent shortage for next-gen digital rigs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products & Services

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Service Type

- 5.1.1 Drilling Services

- 5.1.2 Completion Services (Cementing, Hydraulic Fracturing)

- 5.1.3 Production and Intervention Services

- 5.1.4 Other Services (OSV, seismic, decomm., aviation)

- 5.2 By Location

- 5.2.1 Onshore

- 5.2.2 Offshore

- 5.3 By Well Type

- 5.3.1 Conventional

- 5.3.2 Unconventional

- 5.4 By Geography

- 5.4.1 Saudi Arabia

- 5.4.2 United Arab Emirates

- 5.4.3 Qatar

- 5.4.4 Kuwait

- 5.4.5 Algeria

- 5.4.6 Egypt

- 5.4.7 Libya

- 5.4.8 Morocco

- 5.4.9 Rest of Middle East and North Africa

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Schlumberger

- 6.4.2 Halliburton

- 6.4.3 Baker Hughes

- 6.4.4 China Oilfield Services (COSL)

- 6.4.5 Weatherford International

- 6.4.6 Transocean

- 6.4.7 Valaris

- 6.4.8 Nabors Industries

- 6.4.9 Expro Group

- 6.4.10 National Energy Services Reunited (NESR)

- 6.4.11 Saipem

- 6.4.12 Petrofac

- 6.4.13 KCA Deutag

- 6.4.14 Arabian Drilling

- 6.4.15 Shelf Drilling

- 6.4.16 Maersk Drilling

- 6.4.17 TechnipFMC

- 6.4.18 CGG

- 6.4.19 NOV (National Oilwell Varco)

- 6.4.20 Halliburton Company

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

油田服務市場-全球產業規模、佔有率、趨勢、機會、預測(依服務類型、地點、區域和競爭格局分類,2021-2031年)

油田服務市場-全球產業規模、佔有率、趨勢、機會、預測(依服務類型、地點、區域和競爭格局分類,2021-2031年) 油田服務市場:依服務類型、油井類型、生命週期階段、營運環境和應用分類-全球市場預測(2026-2032 年)

油田服務市場:依服務類型、油井類型、生命週期階段、營運環境和應用分類-全球市場預測(2026-2032 年) 油田服務市場:全球產業分析、市場規模、市場佔有率及按服務、應用、類型、國家和地區分類的預測-2026-2033年

油田服務市場:全球產業分析、市場規模、市場佔有率及按服務、應用、類型、國家和地區分類的預測-2026-2033年 全球油田服務市場:按應用、服務、類型和地區分類

全球油田服務市場:按應用、服務、類型和地區分類 2026-2034年全球油田生產和運輸化學品市場規模、佔有率、趨勢和成長分析報告全球油田服務市場規模、佔有率、趨勢和成長分析報告(2026-2034年)油田生產服務及設備市場-全球產業規模、佔有率、趨勢、機會及預測(依服務類型、設備類型、應用、地區及競爭格局分類,2021-2031年)水井鑽頭市場按鑽頭類型、鑽井方法、材質、最終用途產業和分銷管道分類-2026-2032年全球預測乾冰生產設備市場按產品類型、產能、原料氣體類型、動力來源、形式、自動化水平、最終用途和配銷通路分類 - 全球預測 2025-2030

2026-2034年全球油田生產和運輸化學品市場規模、佔有率、趨勢和成長分析報告全球油田服務市場規模、佔有率、趨勢和成長分析報告(2026-2034年)油田生產服務及設備市場-全球產業規模、佔有率、趨勢、機會及預測(依服務類型、設備類型、應用、地區及競爭格局分類,2021-2031年)水井鑽頭市場按鑽頭類型、鑽井方法、材質、最終用途產業和分銷管道分類-2026-2032年全球預測乾冰生產設備市場按產品類型、產能、原料氣體類型、動力來源、形式、自動化水平、最終用途和配銷通路分類 - 全球預測 2025-2030 油田服務(OFS) -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)

油田服務(OFS) -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)