|

市場調查報告書

商品編碼

2066650

智慧貨架:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Smart Shelf - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

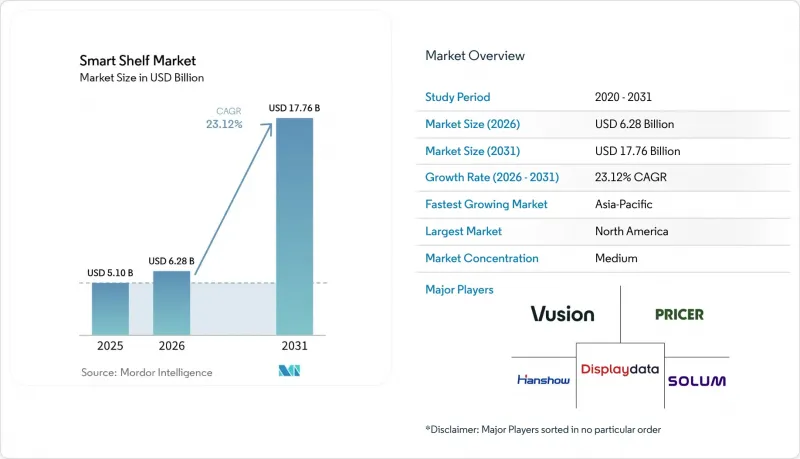

根據 Mordor Intelligence 預測,智慧貨架市場預計將從 2025 年的 51 億美元成長到 2026 年的 62.8 億美元,到 2031 年達到 177.6 億美元,2026 年至 2031 年的複合年成長率預計為 23.12%。

本報告按組件(硬體(物聯網感測器、RFID標籤和讀寫器等)、軟體、服務)、技術(基於RFID、基於重量感測器、基於視覺/攝影機等)、零售業態(大賣場和超級市場、便利商店等)、應用程式(庫存管理、定價、內容、貨架陳列圖等)和地區進行細分。市場預測以美元(USD)為單位。

全球智慧貨架市場趨勢及洞察

為提高整個零售業的即時定價準確性所做的努力

連鎖企業已取消隔夜大幅度的價格變動,因為它們現在被要求在白天同步線上線下價格,以應對競爭對手的「展示廳現象效應」。英國連鎖超市Morrisons計劃在2025年前同步其所有門市的1,080萬張電子標籤,從而消除結帳問題並確保與電商價格一致。沃爾瑪計劃在2026年初前將美國2,300家門市連網,將標籤更換所需時間從一個工作天縮短至幾分鐘,同時也提高了毛利率。印度的《法定計量法》強制要求超級市場使用防篡改價格標籤,加速了全國連鎖超市採用電子標籤的進程。基於保存期限的動態折扣有助於減少食物廢棄物,並將營運成本節約與企業永續發展目標連結起來。

人事費用上升正在加速零售業的自動化進程。

到2025年,美國零售業的平均時薪將年增4.8%,這將給仍依賴人工貼價標籤和庫存盤點的雜貨店帶來壓力。隨著電子貨架系統(ESL)的引入,員工將被重新分配到自助結帳系統和電商揀貨職位。 Waitrose預測,一旦該系統在英國於2026年全面實施,每年將節省超過800萬英鎊(1,010萬美元)的人事費用成本。 Co-op已在2400家門市部署了ESL系統,讓員工能夠重新投入線上訂單的揀貨工作。此外,配備感測器的貨架現在可以自動發出缺貨警報,從而省去了耗時的門市巡查。隨著歐洲和北美最低工資法的實施縮短了投資回收期,智慧貨架市場正變得越來越吸引區域零售商。

維修整間店需要一大筆前期投資。

在一家大型大賣場實施這項技術的成本在 50 萬美元到 150 萬美元之間,這對 EBITDA 為個位數的雜貨店來說是一筆不小的負擔。便利商店平均擁有 2500 個 SKU,但安裝和網路連接後,每個標籤的成本為 15 至 20 美元,除非透過降低人事費用和減少庫存損失節省超過 15% 的成本,否則這項技術的普及應用將受到限制。新興市場利潤率較低的企業由於交易量較小,面臨更大的挑戰。此外,除了頂級連鎖店之外,將硬體成本納入服務費用並進行攤銷的金融產品仍然很少見。

細分市場分析

隨著零售商從一次性採購轉向包含分析、維護和軟體升級等服務的週期性契約,服務業的成長速度超過了硬體產業,複合年成長率 (CAGR) 達到 23.51%。智慧貨架服務市場正在快速擴張,因為託管服務使供應商能夠處理電池更換、韌體更新和網路監控等任務,從而釋放企業內部的 IT 資源。硬體仍將是最大的收入來源,到 2025 年將佔銷售額的 55.11%,但隨著中國 ESL 產能的擴大和電子紙良率的提高,硬體價格呈下降趨勢。在硬體領域,物聯網重量感測器和邊緣 AI 攝影機正在不斷擴大市場佔有率,因為它們可以與被動式RFID讀取器配合使用,並在幾秒鐘內檢測到空貨架或錯放的商品。

目前,支援這些服務的軟體平台每年對每家門市收取 5,000 至 15,000 美元,用於提供視覺化庫存損耗熱圖、貨架陳列圖合規性以及零售媒體競標狀態的儀表板。 E Ink 和 Himax 共同開發的終端人工智慧技術已將影像識別從雲端轉移到貨架,從而降低了頻寬成本和延遲。同時,超高頻 RFID Gen2v2 閱讀器每秒鐘可讀取多達 1,000 個標籤,拓展了智慧貨架市場在倉庫和物流中心的應用前景。

基於RFID技術的貨架無需視線距離,且符合全球供應鏈標準,目前佔據智慧貨架市場40.18%的佔有率。克羅格公司已將RFID的應用範圍從服裝擴展到新鮮烘焙產品,透過自動化保存期限管理,證明了其在硬線商品以外的應用場景中的有效性。同時,受邊緣人工智慧運算成本降低和貨架陳列圖精度提高的推動,視覺和攝影機系統市場正以24.28%的複合年成長率快速成長。光是Trax一家公司就已在全球拍攝了超過40萬家門市,證明在某些商品陳列作業中,基於影像的審核可以與RFID一樣有效,甚至更有效。

電子貨架標籤融合了兩種技術,並整合了近距離通訊 (NFC) 晶片。這使得消費者只需輕觸即可查看原料訊息,從而將實體貨架與數位內容連接起來。配備重量感測器的貨架正被應用於安全至關重要的領域,例如藥房的藥品追蹤,透過即時移除警報防止藥品被盜用。由 Energous 和喬治亞理工學院共同開發的新型無電池 RFID 原型進一步提升了 RFID 在智慧貨架市場的重要性,因為它降低了維護成本,並實現了以前經濟上不可行但超高密度的標籤應用。

區域分析

沃爾瑪和克羅格已在北美地區擴展了電子標籤(ESL)和無線射頻識別(RFID)項目,預計到2025年,北美地區的銷售額將佔全球總銷售額的34.16%。不斷上漲的勞動力成本和成熟的供應商生態系統正在推動美國市場的主流化應用;而在加拿大,隨著沃爾瑪加拿大公司要求供應商為服裝和家居用品貼上標籤,試點部署也在加速推進。墨西哥的主要食品零售商正在試點使用電子標籤,以規範全通路定價並減少結帳問題,但高昂的初始投資成本阻礙了其在中端市場的廣泛應用。

歐洲是第二大市場,其中英國處於領先地位。在英國,Morrisons、Co-op 和 Waitrose 已承諾在全國範圍內實施 ESL(電子購物指南)。德國的 Kaufland、法國的家樂福以及一家西班牙連鎖藥局正在推動 ESL 在歐洲大陸的普及,歐盟的人工智慧法案也正在促成更透明的消費者分析的引入。北歐和東歐的 ESL 實施過程更為穩健,挪威正嘗試基於需求的動態定價。

亞太地區是成長最快的地區,預計複合年成長率將達到24.55%。中國「新零售」的先驅、印度對法定計量法的遵守以及日本便利商店連鎖面臨的人手不足,都是推動這一成長動能的因素。同時,韓國本土電子貨架製造商正在擴大出口。在澳洲藥局和新加坡便利商店進行的試點部署,在成熟的細分市場中取得了穩步成效,而東南亞地區的部署則因資金籌措謹慎進行。中東地區的營運商正在利用政府的現代化資金,以色列的家樂福引入了智慧購物車,沙烏地阿拉伯的大賣場也將其電子貨架納入了「2030願景」。在非洲,南非主導試點部署,而南美洲的情況與北美洲類似,主要受通貨膨脹的驅動。巴西和阿根廷的零售連鎖店由於日常商品價格波動,正在加速採用電子貨架。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 為提高整個零售業的即時定價準確性所做的努力

- 人事費用上升正在加速零售業的自動化進程。

- 大型超市必須減少庫存損失。

- ESG壓力促使人們取消紙質貨架標籤

- 基於電腦視覺的貨架分析技術賦能動態店內媒體

- 無電池RFID標籤的研發:實現超低成本部署

- 市場限制因素

- 整個店鋪維修需要大量的初始投資。

- 與傳統POS和ERP系統整合的複雜性。

- 資料隱私合規(GDPR、CCPA)帶來的負擔

- 仿冒品智慧貨架組件供應的風險日益增加。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 硬體

- 物聯網感測器

- RFID標籤和讀寫器

- 電子貨架標籤(ESL)

- 相機

- 軟體

- 服務

- 硬體

- 透過技術

- 配備RFID功能的智慧貨架

- 帶重量感測器的智慧貨架

- 帶有視覺/攝影機的智慧貨架

- 電子貨架標籤(ESL)系統

- 其他技術

- 按零售業態

- 大賣場和超級市場

- 便利商店

- 專賣店

- 藥局

- 倉庫和物流中心

- 其他零售業態

- 透過使用

- 庫存管理

- 價格管理

- 內容管理

- 貨架陳列圖管理

- 其他用途

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太國家

- 中東

- 以色列

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- VusionGroup SA

- Pricer AB

- Hanshow Technology Co., Ltd.

- Displaydata Limited

- SoluM Co., Ltd.

- Opticon Sensors Europe BV

- E Ink Holdings Inc.

- Keonn Technologies SL

- RAINUS Co., Ltd.

- Avery Dennison Corporation

- Zebra Technologies Corporation

- Honeywell International Inc.

- Impinj, Inc.

- Trax Technology Solutions Pte. Ltd.

- Focal Systems Inc.

- Digi International Inc.

- Checkpoint Systems, Inc.

- SATO Holdings Corporation

- Teraoka Seiko Co., Ltd.

- Altierre Corporation

第7章 市場機會與未來展望

According to Mordor Intelligence, the smart shelf market size is expected to increase from USD 5.10 billion in 2025 to USD 6.28 billion in 2026 and reach USD 17.76 billion by 2031, growing at a CAGR of 23.12% over 2026-2031.

This report is Segmented by Component (Hardware (IoT Sensors, RFID Tags and Readers, and More), Software, and Services), Technology (RFID-Based, Weight Sensor-Based, Vision/Camera-Based, and More), Retail Format (Hypermarkets and Supermarkets, Convenience Stores, and More), Application (Inventory, Pricing, Content, Planogram, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Smart Shelf Market Trends and Insights

Retail-Wide Push For Real-Time Pricing Accuracy

Chains are discarding batch overnight price changes because competitive show-rooming demands intraday updates that sync in-store and online prices. United Kingdom grocer Morrisons synchronized 10.8 million ESLs across its estate in 2025, eliminating checkout disputes and aligning with e-commerce prices. Walmart connected 2,300 U.S. stores by early 2026, cutting a full workday of label changes down to minutes while improving gross margin. India's Legal Metrology Act obliges supermarkets to display tamper-proof prices, accelerating ESL adoption among national chains. Dynamic markdowns tied to expiration windows now help reduce food waste, linking operational savings to corporate sustainability targets.

Rising Labor Costs Accelerating Retail Automation

Average hourly retail wages in the United States rose 4.8% year over year in 2025, putting pressure on grocers that still rely on manual label swaps and stock audits. ESLs redeploy associates toward assisted checkout and e-commerce picking, with Waitrose forecasting annual labor savings exceeding GBP 8 million (USD 10.1 million) once its United Kingdom rollout finishes in 2026. Co-op freed staff for online fulfillment after fitting 2,400 stores with ESLs, and sensor-based shelves now flag out-of-stocks automatically, replacing time-consuming aisle walks. Minimum-wage legislation across Europe and North America is shortening investment payback periods, making the smart shelf market attractive to regional retailers.

High Up-Front Capital For Store-Wide Retrofits

A single hypermarket installation can cost between USD 500,000 and USD 1.5 million, placing a strain on grocers operating on single-digit EBITDA. Convenience stores average 2,500 SKUs yet pay USD 15-20 per label after installation and networking, limiting deployments unless labor and shrinkage savings exceed 15%. Low-margin operators in emerging markets confront even steeper hurdles because transaction values are smaller, while financing products that amortize hardware into service fees remain scarce outside tier-one chains.

Other drivers and restraints analyzed in the detailed report include:

- Shrinkage Reduction Mandates By Large Grocers

- Computer-Vision Shelf Analytics Enabling Dynamic In-Store Media

- Integration Complexity With Legacy POS And ERP

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services with 23.51% CAGR growth outpace hardware as retailers convert one-time purchases into recurring contracts that bundle analytics, maintenance, and software upgrades. The smart shelf market for services is scaling rapidly because managed programs offload battery changes, firmware updates, and network monitoring to vendors, freeing internal IT capacity. Hardware, while still the largest revenue contributor at 55.11% in 2025, is undergoing price deflation as Chinese ESL production expands and e-paper yields climb. Within hardware, IoT weight sensors and edge AI cameras are capturing share because they detect shelf gaps and misplacements within seconds, complementing passive RFID readers.

Software platforms powering those services now charge USD 5,000-15,000 annually per store for dashboards that visualize shrinkage heat maps, planogram compliance, and retail-media bidding. E Ink's collaboration with Himax on on-device AI has shifted image recognition from cloud to shelf, reducing bandwidth costs and latency. Meanwhile, ultra-high-frequency RFID Gen2v2 readers interrogate up to 1,000 tags per second, opening warehouse and distribution center cases for the smart shelf market.

RFID-based shelves hold 40.18% smart shelf market share because they work without line-of-sight and plug into global supply-chain standards. Kroger extended RFID from apparel into the fresh bakery to automate expiry, validating use cases beyond hardlines. Yet vision and camera systems are scaling at a 24.28% CAGR, driven by falling edge AI compute costs and improved planogram accuracy. Trax alone photographs more than 400,000 stores worldwide, proving image-based audits can match or exceed RFID for some merchandising tasks.

Electronic shelf labels overlap both technologies and now carry near-field communication chips that let shoppers tap for ingredient data, uniting physical shelves with digital content. Weight-sensor shelves fill safety-critical niches such as pharmacy narcotics tracking, where instant removal alerts deter diversion. New battery-free RFID prototypes from Energous and Georgia Tech promise to eliminate maintenance costs and unlock ultra-dense tagging that was previously uneconomic, reinforcing RFID relevance in the smart shelf market.

Geography Analysis

North America generated 34.16% of 2025 revenue as Walmart and Kroger scaled ESL and RFID programs. U.S. labor inflation and an established vendor ecosystem underpin mainstream adoption, while Canadian pilots accelerate following Walmart Canada's requirement that suppliers tag apparel and home goods. Mexico's leading grocers are testing ESLs to align omnichannel prices and curb checkout disputes, yet high capital costs are slowing broad mid-market adoption.

Europe follows as the second-largest region, led by the United Kingdom, where Morrisons, Co-op, and Waitrose each committed to nationwide ESL coverage. Germany's Kaufland, France's Carrefour, and Spain's pharmacy chains illustrate the breadth of the continent, and the EU AI Act is shaping transparent shopper analyticsshopper analytics deployments. Northern and Eastern Europe are rolling out at a steadier pace, with Norway experimenting with demand-based dynamic pricing.

Asia-Pacific is the fastest-growing region, projected at 24.55% CAGR. China's new retail pioneers, India's Legal Metrology compliance, and Japan's labor-scarce convenience chains all drive momentum, while South Korea's domestic ESL makers scale exports. Australia's pharmacies and Singapore's convenience pilots showcase incremental wins in mature sub-markets, whereas wider Southeast Asia adopts cautiously amid financing limitations. Middle East operators leverage government modernization funds, with Israel's Carrefour deploying smart carts and Saudi hypermarkets embracing ESLs under Vision 2030. South Africa leads African pilots, and South America mirrors inflation-driven North American logic, with Brazil and Argentina retail chains using daily commodity swings to justify ESL speed.

- VusionGroup S.A.

- Pricer AB

- Hanshow Technology Co., Ltd.

- Displaydata Limited

- SoluM Co., Ltd.

- Opticon Sensors Europe B.V.

- E Ink Holdings Inc.

- Keonn Technologies S.L.

- RAINUS Co., Ltd.

- Avery Dennison Corporation

- Zebra Technologies Corporation

- Honeywell International Inc.

- Impinj, Inc.

- Trax Technology Solutions Pte. Ltd.

- Focal Systems Inc.

- Digi International Inc.

- Checkpoint Systems, Inc.

- SATO Holdings Corporation

- Teraoka Seiko Co., Ltd.

- Altierre Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Retail-Wide Push for Real-Time Pricing Accuracy

- 4.2.2 Rising Labor Costs Accelerating Retail Automation

- 4.2.3 Shrinkage Reduction Mandates by Large Grocers

- 4.2.4 ESG Pressure to Eliminate Paper Shelf Labels

- 4.2.5 Computer-Vision Shelf Analytics Enabling Dynamic In-Store Media

- 4.2.6 Battery-Free RFID Tag Research and Development Unlocking Ultra-Low-Cost Deployments

- 4.3 Market Restraints

- 4.3.1 High Up-Front Capital for Store-Wide Retrofits

- 4.3.2 Integration Complexity with Legacy POS and ERP

- 4.3.3 Data-Privacy Compliance (GDPR, CCPA) Burden

- 4.3.4 Growing Counterfeit Smart-Shelf Components Supply Risk

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.1.1 IoT Sensors

- 5.1.1.2 RFID Tags and Readers

- 5.1.1.3 Electronic Shelf Lables (ESL)

- 5.1.1.4 Cameras

- 5.1.2 Software

- 5.1.3 Services

- 5.1.1 Hardware

- 5.2 By Technology

- 5.2.1 RFID-Based Smart Shelves

- 5.2.2 Weight Sensor-Based Smart Shelves

- 5.2.3 Vision/Camera-Based Smart Shelves

- 5.2.4 Electronic Shelf Label (ESL) Systems

- 5.2.5 Other Technologies

- 5.3 By Retail Format

- 5.3.1 Hypermarkets and Supermarkets

- 5.3.2 Convenience Stores

- 5.3.3 Specialty Stores

- 5.3.4 Pharmacies

- 5.3.5 Warehouses and Distribution Centers

- 5.3.6 Other Retail Formats

- 5.4 By Application

- 5.4.1 Inventory Management

- 5.4.2 Pricing Management

- 5.4.3 Content Management

- 5.4.4 Planogram Management

- 5.4.5 Other Applications

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Middle East

- 5.5.4.1 Israel

- 5.5.4.2 Saudi Arabia

- 5.5.4.3 United Arab Emirates

- 5.5.4.4 Turkey

- 5.5.4.5 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Egypt

- 5.5.5.3 Rest of Africa

- 5.5.6 South America

- 5.5.6.1 Brazil

- 5.5.6.2 Argentina

- 5.5.6.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 VusionGroup S.A.

- 6.4.2 Pricer AB

- 6.4.3 Hanshow Technology Co., Ltd.

- 6.4.4 Displaydata Limited

- 6.4.5 SoluM Co., Ltd.

- 6.4.6 Opticon Sensors Europe B.V.

- 6.4.7 E Ink Holdings Inc.

- 6.4.8 Keonn Technologies S.L.

- 6.4.9 RAINUS Co., Ltd.

- 6.4.10 Avery Dennison Corporation

- 6.4.11 Zebra Technologies Corporation

- 6.4.12 Honeywell International Inc.

- 6.4.13 Impinj, Inc.

- 6.4.14 Trax Technology Solutions Pte. Ltd.

- 6.4.15 Focal Systems Inc.

- 6.4.16 Digi International Inc.

- 6.4.17 Checkpoint Systems, Inc.

- 6.4.18 SATO Holdings Corporation

- 6.4.19 Teraoka Seiko Co., Ltd.

- 6.4.20 Altierre Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2026-2030年全球電子貨架標籤(ESL)市場

2026-2030年全球電子貨架標籤(ESL)市場 電子貨架標籤市場報告:按類型、組件、技術、應用和地區分類(2026-2034 年)

電子貨架標籤市場報告:按類型、組件、技術、應用和地區分類(2026-2034 年) 電子貨架標籤市場:2026-2032年全球市場預測(按產品類型、組件、通訊技術、顯示尺寸、應用和分銷管道分類)

電子貨架標籤市場:2026-2032年全球市場預測(按產品類型、組件、通訊技術、顯示尺寸、應用和分銷管道分類) 電子貨架標籤市場:按技術、產品類型、應用和地區分類

電子貨架標籤市場:按技術、產品類型、應用和地區分類 全球電子貨架標籤市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球電子貨架標籤市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2026年全球電子貨架標籤市場報告

2026年全球電子貨架標籤市場報告 電子貨架標籤市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、形式、材料類型、部署方式及最終用戶分類

電子貨架標籤市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、形式、材料類型、部署方式及最終用戶分類 電子貨架標籤市場機會、成長要素、產業趨勢分析及2026年至2035年預測

電子貨架標籤市場機會、成長要素、產業趨勢分析及2026年至2035年預測 電子貨架標籤市場 - 全球產業規模、佔有率、趨勢、機會及預測(按產品類型、通訊方式、最終用戶、地區和競爭格局分類,2021-2031年)

電子貨架標籤市場 - 全球產業規模、佔有率、趨勢、機會及預測(按產品類型、通訊方式、最終用戶、地區和競爭格局分類,2021-2031年) 電子貨架標籤(ESL)市場規模、佔有率和成長分析(按組件、類型、通訊技術、尺寸、應用和地區分類)-2026-2033年產業預測

電子貨架標籤(ESL)市場規模、佔有率和成長分析(按組件、類型、通訊技術、尺寸、應用和地區分類)-2026-2033年產業預測