|

市場調查報告書

商品編碼

2066643

歐洲樓梯升降椅:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Europe Stair Lift - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

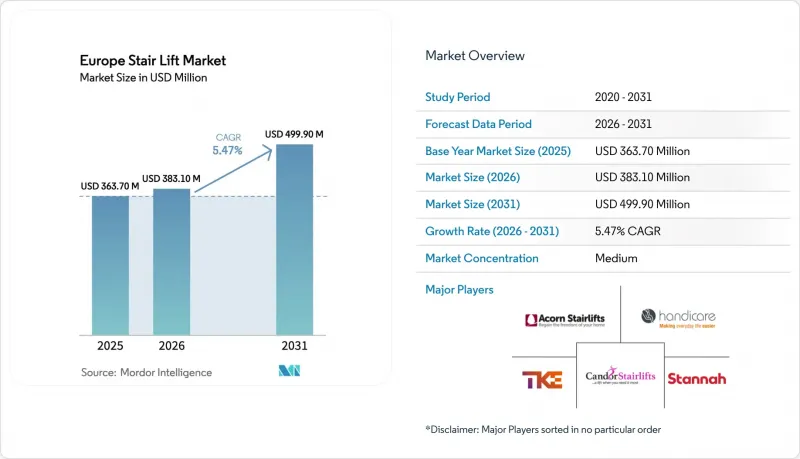

據 Mordor Intelligence 稱,2025 年歐洲樓梯升降機市場價值為 3.637 億美元,預計到 2031 年將達到 4.999 億美元,而 2026 年為 3.831 億美元,預測期(2026-2031 年)的複合年成長率為 5.47%。

本報告按軌道方向(直軌和彎軌)、用戶姿勢(坐姿、站姿、一體式)、安裝位置(室內和室外)、應用領域(住宅、醫療設施、商業設施等)以及地區(英國、德國、法國、義大利、西班牙及其他歐洲國家)進行細分。市場預測以美元計價。

歐洲樓梯升降椅市場趨勢與洞察

老年人口比例和殘障人士盛行率都在上升。

隨著嬰兒潮世代步入老年,歐洲的人口結構正向老化轉變,這擴大了無障礙產品的潛在客戶群。預計65歲及以上人口將從2019年的9,050萬增至2024年的9,780萬,並在2050年超過1.298億。隨著老齡化成長,行動不便的情況日益增多,對能夠在多層住宅內安全上下樓梯的樓梯升降椅的需求也在穩步成長。這一趨勢正在影響產品的行銷和功能重點,因為老年女性的行動不便程度往往高於男性。老年人口密度較高且配備電梯的住宅較少的農村地區,為現有住宅的改造提供了巨大的市場潛力。在義大利、葡萄牙和保加利亞等老年人口比例最高的國家,在歐洲樓梯升降椅市場有著特別巨大的長期發展潛力。

人們越來越傾向於選擇居家照護,以避免入住機構。

在歐洲各地,越來越多的家庭選擇社區或居家照護照護而非機構照護。疫情期間,75歲以上民眾居家照護服務的使用率激增,目前仍居高不下,主要得益於公共衛生部門鼓勵獨立生活。這種選擇也出於經濟方面的考慮,因為機構護理的平均每日費用往往超過入住兩年內安裝樓梯升降椅的成本。此外,許多殘疾人住宅面臨經濟壓力,因此一次性維修加上津貼和增值稅減免,比持續支付機構護理費用更具吸引力。英國的「殘障人士設施津貼」和德國的「房屋維修津貼」等政策措施透過降低初始投資成本進一步推動了這一趨勢。因此,房屋業主安裝樓梯升降椅的比例持續上升,尤其是在津貼申請流程簡化的市場。

高昂的初始購買和安裝成本

儘管有津貼計畫的支持,但對於低收入地區的家庭來說,新樓梯升降椅的價格仍然是一大障礙。室內線性型號的樓梯升降椅在沒有補貼的情況下通常起價約為 2,500 英鎊(3,175 美元),而需要耐候性的室外型號價格則高得驚人。電氣維修、結構加固和認證安裝服務可能會使最終費用增加數百美元。東歐和南歐地區的消費者可支配收入低於歐盟平均水平,他們往往會推遲購買或尋找二手產品,這減緩了這些地區樓梯升降椅的普及速度。租賃計劃和製造商支持的貸款方案可以減輕負擔,但無法完全消除人們對高昂價格的印象,尤其是在那些對津貼資格了解甚少的地區。公共預算持續面臨的壓力可能會限制未來津貼的擴大,「可負擔性」很可能仍將是歐洲樓梯升降椅市場競爭策略的核心。

細分市場分析

2025年,直梯式樓梯升降椅在歐洲市場仍佔67.10%的佔有率。這反映了其適用於大多數單段樓梯且安裝成本較低。受模組化生產帶來的前置作業時間縮短和單位成本降低的推動,預計到2031年,歐洲彎梯式樓梯升降椅市場規模將以10.72%的複合年成長率成長。公共住宅機構和大規模養老院連鎖機構的批量採購繼續為直梯式樓梯升降椅帶來優勢,其標準化的面積也簡化了設備維護。另一方面,彎梯式樓梯升降椅則更受歷史街區和都市區聯排住宅住宅的青睞,這些住宅的樓梯平台狹窄且有90度轉彎。各供應商都在中歐擴大工廠產能,以滿足日益成長的彎梯式樓梯升降椅需求,試圖打破「客製化產品需要漫長等待」的固有觀念。隨著生產規模擴大和租賃設備積累,直線型和曲線型產品之間的價格差異將會縮小,預計這將為歐洲樓梯升降機市場開闢更大的潛在客戶群。

安裝人員表示,模組化軌道組件可將現場組裝時間縮短數小時,最大限度地減少對居住者的干擾,並降低每個專案的人事費用。製造商還採用更輕的合金和改進的驅動系統,以提高長距離和複雜曲線運行的平穩性。這種轉向預測性維護的方式預計將吸引居住在老舊住宅中的曲線樓梯升降椅用戶,因為老舊房屋的濕度和溫度波動會加速零件磨損。因此,經銷商在提案高階曲線樓梯升降椅選項時,會重點介紹遠距離診斷套件,並強調其在設備整個使用壽命期間的總體擁有成本 (TCO) 優勢。

2025年,坐式樓梯升降椅的出貨量佔比高達71.80%,由於其廣泛的適用性和更高的舒適度,仍然是多口之家的首選。預計到2031年,站立式樓梯升降椅的複合年成長率將達到9.42%,尤其受到膝關節僵硬、部分承重能力受限或樓梯極度狹窄的用戶青睞。在歐洲樓梯升降椅市場,由於公寓和聯排別墅的樓梯踏板較淺且淨空高度有限,站立式樓梯升降椅的需求進一步成長。坐式樓梯升降椅融合了旋轉腳踏板、多點式安全帶和抗菌座椅套等功能,體現了從醫療機構採購經驗中獲得的寶貴見解。站立式樓梯升降椅還配備了折疊式腳踏板、整合式扶手和感測器鎖定門,增強了上下樓梯時的穩定性和安全性,解決了先前阻礙其廣泛應用的安全隱患。

將兩種模式整合到混合平台中,為預計未來行動能力下降的家庭提供了一個面向未來的解決方案。經銷商通常會向預計多代人使用且只需一次安裝的家庭推薦混合模式,這可以延長產品壽命並提高轉售柔軟性。隨著與方向相關的軟體功能逐漸標準化,功能差異將僅限於安裝面積和姿勢偏好,從而在無需大量額外研發成本的情況下,提高站立式升降機的毛利率。這一趨勢正在推動歐洲樓梯升降機市場的產品線多元化,幫助小規模經銷商在不積壓過多庫存的情況下滿足細分市場需求。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 宏觀經濟因素的影響

- 市場促進因素

- 老年人口比例不斷增加以及殘障人士人口普遍增多

- 人們越來越傾向於選擇居家照護,以避免入住機構。

- 模組化鐵路製造和改裝套件的進步

- 行動輔助設備的補貼和增值稅豁免計劃

- 租賃和訂閱模式的興起

- 透過物聯網與智慧家庭和遠距離診斷整合。

- 市場限制因素

- 初始購買和安裝成本相對較高。

- 由於樓梯形狀複雜,定製成本飆升。

- 對輔助器具的偏見

- 仿單標示外用藥的保險覆蓋範圍限制

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 軌道方向

- 直的

- 曲線

- 透過使用者姿勢

- 坐姿

- 常設

- 一體化

- 按安裝類型

- 室內的

- 戶外的

- 透過使用

- 住宅

- 醫療機構

- 商業

- 其他用途

- 國家

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Handicare Group AB

- Stannah Lifts Holdings Limited

- Acorn Mobility Services Limited

- TK Elevator GmbH

- Bruno Independent Living Aids, Inc.

- Platinum Stairlifts Limited

- Bespoke Stairlifts Limited

- Mobility Stairlift Limited

- Dolphin Mobility Limited

- Ableworld(UK)Limited

- Weigl Liftsysteme GmbH

- HIRO Lift Hillenkotter und Ronsieck GmbH

- Otolift Trapliften BV

- Vimec Srl

- Lehner Lifttechnik GmbH

- Aritco Lift AB

- Extrema Srl

- Access BDD Limited

- Anglian Lifts Limited

第7章 市場機會與未來展望

According to Mordor Intelligence, the europe stair lift market size was valued at USD 363.70 million in 2025 and is estimated to grow from USD 383.10 million in 2026 to reach USD 499.90 million by 2031, at a CAGR of 5.47% during the forecast period (2026-2031).

This report is Segmented by Rail Orientation (Straight, and Curved), User Orientation (Seated, Standing, and Integrated), Installation (Indoor, and Outdoor), Application (Residential, Healthcare Facilities, Commercial, and More), and Geography (United Kingdom, Germany, France, Italy, Spain, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

Europe Stair Lift Market Trends and Insights

Rising Proportion of Aged People and Disability Prevalence

Europe's age structure is shifting toward older cohorts as the baby-boomer generation enters advanced years, lifting the potential customer pool for accessibility products. The population aged 65 and above climbed from 90.5 million in 2019 to 97.8 million in 2024 and is projected to top 129.8 million by 2050. Mobility limitations intensify with age, creating sustained demand for stair lifts that enable safe vertical movement inside multi-story homes. Elderly women experience higher mobility constraints than men, a dynamic that influences product marketing and feature emphasis. Rural regions, where older residents are more concentrated and elevator-equipped housing is scarce, represent fertile ground for retrofit activity. Countries such as Italy, Portugal, and Bulgaria, which post the largest elderly shares, carry particularly strong long-term potential for the Europe stair lift market.

Growing Home-Care Preference to Avoid Institutionalization

Households across Europe increasingly opt for community-based or domiciliary care rather than nursing-home placement. Uptake of home-care services among people aged 75 and over climbed sharply during the pandemic and remains elevated as public health authorities promote independent living. Financial prudence underpins this choice; average daily nursing-home charges often exceed the cost of installing a stair lift within two years of residency. Disabled homeowners also display a higher incidence of income strain, making one-time retrofits supplemented by grants or VAT exemptions more attractive than recurring institutional fees. Policy instruments such as the United Kingdom's Disabled Facilities Grant and Germany's adaptation allowances strengthen this preference by lowering capital outlays. As a result, conversion rates in owner-occupied dwellings continue to advance, particularly in markets with streamlined grant-application processes.

High Upfront Purchase and Installation Cost

Despite supportive grant mechanisms, the sticker price of a new stair lift remains a hurdle for households in lower-income regions. Indoor straight models commonly start around GBP 2,500 (USD 3,175) when purchased without subsidies, and price escalates sharply for outdoor units requiring weatherproofing. Electrical upgrades, structural reinforcements, and certified installation services can add several hundred dollars to the final invoice. Buyers in Eastern and Southern Europe, where disposable income trails the EU average, often defer purchase or seek second-hand units, slowing penetration in these territories. Rental programs and manufacturer-backed financing mitigate the burden but do not fully offset the perception of high cost, especially where awareness of grant eligibility is limited. Continued pressure on public budgets could temper future subsidy growth, keeping affordability at the center of competitive strategy within the Europe stair lift market.

Other drivers and restraints analyzed in the detailed report include:

- Advancements in Modular Rail Manufacturing and Retrofit Kits

- Subsidies and VAT-Exempt Schemes for Mobility Aids

- Complex Staircase Geometries Inflating Customization Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Straight units maintained 67.10% of the Europe stair lift market share in 2025, reflecting their compatibility with most single-flight staircases and lower installed cost. The Europe stair lift market size for curved installations is projected to expand at a 10.72% CAGR through 2031 as modular manufacturing trims lead times and reduces per-unit expense. Straight models continue to benefit from bulk procurement by public housing authorities and large care-home chains, where standardized footprints simplify fleet maintenance. Curved systems attract homeowners in historic districts and urban row houses that feature tight landings or 90-degree turns. Vendors are expanding factory capacity in Central Europe to handle rising curved demand, combating the perception that customization equals prohibitively long waits. As production ramps and rental fleets accumulate, price differentials between straight and curved products should narrow, unlocking additional addressable households for the Europe stair lift market.

Installation crews report that modular rail segments now shave multiple hours off onsite assembly, reducing occupant disruption and decreasing labour cost per project. Manufacturers also incorporate lighter alloys and updated drive trains that improve ride smoothness on longer or more complex curves. The shift toward predictive maintenance is expected to resonate with curved owners, who often occupy older properties susceptible to humidity and temperature swings that can accelerate component wear. Accordingly, dealers highlight remote-diagnostic packages when pitching premium curved options, reinforcing total cost-of-ownership advantages across the equipment's service life.

Seated lifts constituted 71.80% of shipments in 2025 and remain the default choice for multi-user households due to universal appeal and enhanced comfort. Standing units are forecast to log a 9.42% CAGR to 2031, appealing to users with knee stiffness, partial weight-bearing capacity, or highly constrained stair widths. The Europe stair lift market size for standing variants is further buoyed by condominiums and terraced homes where stair treads are shallow and headroom is limited. Seated models are gaining refinements such as swivel-away footplates, multi-point harnesses, and antimicrobial seat covers that reflect lessons from healthcare facility procurement. Standing lifts now incorporate fold-down perches, integrated grab rails, and sensor-locked doors that add stability and confidence during ascent, addressing safety concerns that once limited uptake.

Integration of both modes in hybrid platforms provides futureproofing for households anticipating progressive mobility decline. Dealers often recommend hybrid models to families expecting multiple generations to use a single installation, promoting longevity and resale flexibility. As software features standardize across orientations, functional differences dwindle to physical footprint and posture preference, enabling higher gross margin on standing sales without major incremental R&D expense. This trend supports greater product-line diversification inside the Europe stair lift market, assisting smaller dealers in catering to niche requirements without bloating inventory.

List of Companies Covered in this Report:

- Handicare Group AB

- Stannah Lifts Holdings Limited

- Acorn Mobility Services Limited

- TK Elevator GmbH

- Bruno Independent Living Aids, Inc.

- Platinum Stairlifts Limited

- Bespoke Stairlifts Limited

- Mobility Stairlift Limited

- Dolphin Mobility Limited

- Ableworld (UK) Limited

- Weigl Liftsysteme GmbH

- HIRO Lift Hillenkotter und Ronsieck GmbH

- Otolift Trapliften B.V.

- Vimec S.r.l.

- Lehner Lifttechnik GmbH

- Aritco Lift AB

- Extrema S.r.l.

- Access BDD Limited

- Anglian Lifts Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions AND Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors

- 4.3 Market Drivers

- 4.3.1 Rising proportion of aged people and disability prevalence

- 4.3.2 Growing home-care preference to avoid institutionalisation

- 4.3.3 Advancements in modular rail manufacturing and retrofit kits

- 4.3.4 Subsidies and VAT-exempt schemes for mobility aids

- 4.3.5 Emergence of rental and subscription models

- 4.3.6 Smart-home integration and IoT remote diagnostics

- 4.4 Market Restraints

- 4.4.1 High upfront purchase and installation cost

- 4.4.2 Complex staircase geometries inflating customisation prices

- 4.4.3 Perceived stigma associated with assistive devices

- 4.4.4 Limited reimbursement coverage outside medical indication

- 4.5 Industry Value-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Rail Orientation

- 5.1.1 Straight

- 5.1.2 Curved

- 5.2 By User Orientation

- 5.2.1 Seated

- 5.2.2 Standing

- 5.2.3 Integrated

- 5.3 By Installation

- 5.3.1 Indoor

- 5.3.2 Outdoor

- 5.4 By Application

- 5.4.1 Residential

- 5.4.2 Healthcare Facilities

- 5.4.3 Commercial

- 5.4.4 Other Applications

- 5.5 By Country

- 5.5.1 United Kingdom

- 5.5.2 Germany

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Handicare Group AB

- 6.4.2 Stannah Lifts Holdings Limited

- 6.4.3 Acorn Mobility Services Limited

- 6.4.4 TK Elevator GmbH

- 6.4.5 Bruno Independent Living Aids, Inc.

- 6.4.6 Platinum Stairlifts Limited

- 6.4.7 Bespoke Stairlifts Limited

- 6.4.8 Mobility Stairlift Limited

- 6.4.9 Dolphin Mobility Limited

- 6.4.10 Ableworld (UK) Limited

- 6.4.11 Weigl Liftsysteme GmbH

- 6.4.12 HIRO Lift Hillenkotter und Ronsieck GmbH

- 6.4.13 Otolift Trapliften B.V.

- 6.4.14 Vimec S.r.l.

- 6.4.15 Lehner Lifttechnik GmbH

- 6.4.16 Aritco Lift AB

- 6.4.17 Extrema S.r.l.

- 6.4.18 Access BDD Limited

- 6.4.19 Anglian Lifts Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and unmet-need assessment

樓梯升降椅市場 - 全球產業規模、佔有率、趨勢、機會、預測:軌道方向、使用者導向、安裝方式、應用、區域及競爭格局,2021-2031年

樓梯升降椅市場 - 全球產業規模、佔有率、趨勢、機會、預測:軌道方向、使用者導向、安裝方式、應用、區域及競爭格局,2021-2031年 樓梯升降椅市場:按產品類型、安裝類型、最終用戶和分銷管道分類 - 2026-2032年全球市場預測

樓梯升降椅市場:按產品類型、安裝類型、最終用戶和分銷管道分類 - 2026-2032年全球市場預測 樓梯升降椅市場:按產品類型、模式類型、操作方式、最終用戶和地區分類

樓梯升降椅市場:按產品類型、模式類型、操作方式、最終用戶和地區分類 樓梯升降椅:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)美國樓梯升降椅:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

樓梯升降椅:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)美國樓梯升降椅:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 全球樓梯升降椅市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球樓梯升降椅市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球樓梯升降機與攀爬設備市場報告

2026年全球樓梯升降機與攀爬設備市場報告 2026-2030年全球樓梯升降機市場

2026-2030年全球樓梯升降機市場 樓梯升降椅市場規模、佔有率和成長分析(按設備類型、用戶群、安裝方式、最終用戶和地區分類)-2026-2033年產業預測全球樓梯升降機市場規模(按產品類型、應用、最終用戶、區域範圍和預測)

樓梯升降椅市場規模、佔有率和成長分析(按設備類型、用戶群、安裝方式、最終用戶和地區分類)-2026-2033年產業預測全球樓梯升降機市場規模(按產品類型、應用、最終用戶、區域範圍和預測)