|

市場調查報告書

商品編碼

2066601

樓梯升降椅:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Stair Lift - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

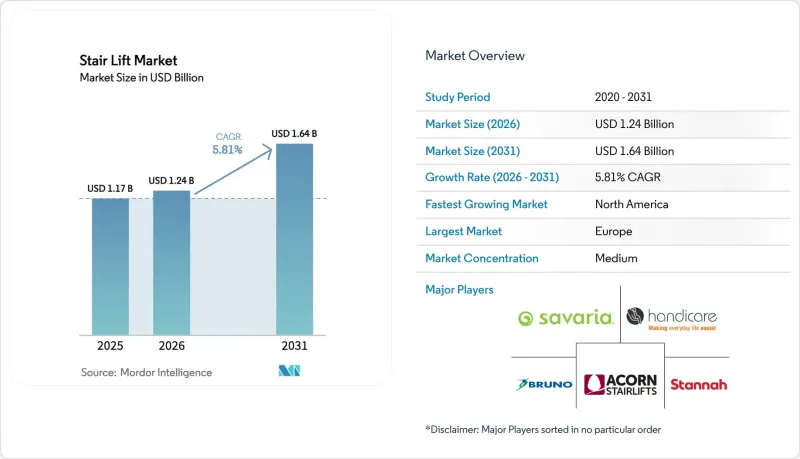

根據 Mordor Intelligence 預測,樓梯升降椅市場規模將從 2025 年的 11.7 億美元成長到 2026 年的 12.4 億美元,然後在 2031 年達到 16.4 億美元,2026 年至 2031 年的複合年成長率為 5.81%。

本報告按軌道方向(直線和曲線)、使用姿勢(坐姿、站姿和整合式)、安裝位置(室內和室外)、應用領域(住宅、醫療、政府、休閒娛樂)以及地區(北美、南美、歐洲、亞太地區以及中東和非洲)進行細分。市場預測以美元計價。

全球樓梯升降椅市場趨勢及洞察

人口老化加速和「居家養老」(在家安享晚年)的普及

65歲及以上人口的成長擴大了住宅行動輔助解決方案的基本客群,從而推動了樓梯升降椅市場的成長。隨著全球人口老化,預計到2050年,大多數地區60歲及以上人口的比例將進一步上升,因此,確保老年人安全出入住宅的需求日益成長。與過去幾十年相比,入住養老機構的老年人數量正在減少,預算轉而用於住宅維修,例如安裝樓梯升降椅和坡道門。價格在3000至5000美元之間的直梯式樓梯升降椅正成為許多家庭替代機構護理的實用選擇。國際公共衛生舉措正在推動建立老年友善社區,並強調無障礙住宅設計和維修的重要性。

自2020年起,將實施更嚴格的無障礙標準並對《建築標準法》進行修訂。

ASME A18.1-2023 標準於 2024 年 3 月生效,加強了超速測試並更新了緊急通訊要求。這提高了安全標準,並減少了僅基於安全訊號的品牌差異化。建築規範的協調統一和更清晰的許可標準使經銷商能夠以最小的延誤跨州運營,從而實現更可預測的前置作業時間和更佳的客戶體驗。同時,歐盟的協調計劃,例如 EN 81-40 和《歐洲無障礙法案》,正在統一成員國的設計要求。這明確了觸覺控制、文件可存取性和一致安全系統的技術藍圖。安全性和安裝參數的清晰度提高,減少了返工,並使建築商、建築師和檢驗員對符合標準的傾斜式升降機共用。這些變化增強了最終用戶的信心,降低了風險感知,並促進了樓梯升降機市場的更換和升級週期。

聯邦醫療保險覆蓋範圍有限且自付費用高

在最初的聯邦醫療保險(Medicare)制度下,樓梯升降椅不屬於耐用醫療設備。這意味著對於大多數受益人來說,沒有統一的聯邦福利途徑。雖然聯邦醫療保險優勢計劃(Medicare Advantage)可能提供補充福利,但資格因計劃而異,需要事先批准,且覆蓋範圍有限,導致各縣之間的服務獲取存在差異。醫療補助豁免(Medicaid waiver)福利因州而異,可能導致漫長的等待名單,即使是符合資格的消費者也可能需要等待才能獲得服務。相較之下,退伍軍人事務部(VA)的住宅津貼對符合條件的個人來說可能相當可觀,其中包括2026會計年度高達126,526美元的「特殊改造住宅」津貼,可用於資助全面的無障礙維修。直梯式樓梯升降椅的價格通常在3,000美元到5,000美元之間,而彎梯式樓梯升降椅的價格可能遠超過10,000美元。如果既沒有公共保險也沒有私人保險,那麼固定收入家庭將面臨高額的自付費用。

細分市場分析

截至2025年,直梯式樓梯升降椅佔據了54%的市場。這主要歸功於預製軌道的普及,預製軌道縮短了安裝時間,並降低了首次購買者的價格。在樓梯升降椅市場,直梯式樓梯升降椅在典型住宅佈局的維修項目中更受歡迎,這有利於經銷商批量採購並保持穩定的存貨周轉。由於模組化軌道設計縮短了前置作業時間,並能適應更多類型的樓梯,預計2026年至2031年間,彎梯式樓梯升降椅的複合年成長率將達到10.34%。 Harmar的模組化彎梯平台具備連網診斷功能,並採用適用於狹窄樓梯的低矮軌道,可在部分大都會地區實現隔天送達。雙軌配置可應對急彎,從而在歐洲老舊住宅存量中進行高階安裝,這對於專注於複雜項目的經銷商而言極具優勢。使用可儲備的軌道部件進行現場快速組裝,提高了安裝速度,並為尋求定製曲線而無需長時間製造的買家擴大了選擇範圍。

從安裝模式來看,直線型升降機在標準維修項目中佔據主導地位,而曲線型升降機則主要應用於帶有螺旋樓梯、中間平台和裝飾性造型的住宅。隨著模組化設計的改進,交付時間縮短,維護性提高,曲線型升降機的市場規模預計將會擴大。鉸鍊式軌道和折疊式零件有助於確保平台和門口有足夠的通行空間,從而滿足狹窄住宅和共用樓梯間的需求。戶外曲線型升降機具有耐候性和耐腐蝕性,適用於沿海地區和紫外線照射強烈的環境,因此非常適合用於露台通道和多層戶外樓梯。這些優勢促使越來越多複雜的專案轉向曲線型系統,儘管直線型升降機仍然是高銷售樓梯升降機市場的核心。

舒適、操作直覺、座椅可調整(尤其適合膝關節活動受限的老人)的坐式升降機預計到2025年將佔據48%的市場佔有率。電動旋轉功能和符合人體工學設計的扶手有助於上下樓梯,降低跌倒風險,並方便在狹窄的頂層樓梯平台上使用。站立式和腳踏式(坐式)升降機,因其適用於無法完全坐姿的用戶,預計在2026年至2031年間將以8.76%的複合年成長率成長。腳踏式升降機採用半站立姿勢,折疊式後體積小巧,尤其適用於狹窄的樓梯,特別是人口密集城區常見的老住宅。結合坐姿和站姿的整合式升降機擴大應用於復健機構,以滿足多用戶靈活使用的需求。

這些不同的姿勢組合反映了臨床需求和家庭環境的限制,影響整個樓梯升降椅市場的產品選擇和價格敏感度。站立式解決方案適用於空間有限且有特定整形外科需求的場所,而坐式機型則代表了最廣泛用戶層的舒適標準。更新後的安全標準規定了座椅高度範圍和尺寸,以確保握持舒適度,統一了各品牌的人體工學標準,並提高了消費者的安全標準。與專注於單一姿勢類型的品牌相比,同時提供站立式和坐式產品的零售商更能滿足多用戶家庭的需求。預計進一步的人體工學改進將提高用戶對兩種配置的滿意度,並減少樓梯升降椅產業的服務問題。

區域分析

2025年,歐洲將引領全球樓梯升降椅市場,佔65%的市場。這主要得益於英國、德國和其他西歐國家樓梯升降椅市場的顯著成長。歐盟安全和文件標準的統一化簡化了跨境運營,減少了產品差異,並促進了跨國分銷策略的實施。增值稅減免計畫和地區津貼持續推動市場需求,但公共預算的波動影響了季度銷售。在北歐國家,消費者對互聯和高階型號樓梯升降椅的興趣日益濃厚,這反映了全部區域的經濟限制限制了其市場成長,使其無法與該地區較富裕的市場相提並論。歐洲清晰的政策框架和完善的分銷網路鞏固了其作為全球銷售領導者的地位。

截至2025年,北美市場規模相對小規模,但預計到2031年將以10.50%的複合年成長率穩定成長。該地區(尤其是美國)可支配收入的成長和成熟的經銷商網路,促進了消費者自費購買和頻繁更換產品。老年人口的成長擴大了行動輔助解決方案和住宅安全維修的潛在基本客群。聯邦政府的各項舉措,例如退伍軍人事務部提供的住宅津貼和非營利組織推廣的住宅維修項目,正在幫助減輕符合條件的家庭的經濟負擔。此外,墨西哥樓梯升降椅製造商的擴張提高了供應柔軟性,並降低了美國陽光地帶和中西部地區經銷商網路的運輸成本。

在亞太地區,隨著政策措施和人口結構變化重塑市場需求,市場正蓬勃發展。分銷商網路的擴張和政策對無障礙住宅日益成長的關注正在推動該地區的成長。中國等主要經濟體的快速老化、澳洲的「在熟悉的地方退休」政策以及較高的家庭收入,都促進了都市區樓梯升降椅的穩步普及。在東南亞和南亞,樓梯升降椅的初期普及主要集中在主要城市的中高所得家庭,這反映了早期的市場趨勢。隨著供應鏈適應區域需求,亞太地區的樓梯升降椅市場預計將在2031年之前保持持續成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 人口老化加速以及「居家養老」理念日益普及

- 自2020年起,將實施更嚴格的無障礙標準並對《建築標準法》進行修訂。

- 多層住宅住宅維修維修工程的趨勢

- 電池備用電源、感測器和遠距離診斷的進步

- 利用醫療補助豁免和政府津貼實現住宅維修。

- 在州一級採用 ASME A18.1 標準,並透過明確許可要求來減少程序摩擦。

- 市場限制因素

- 聯邦醫療保險的覆蓋範圍有限,且自付費用高昂。

- 弧形軌道和複雜的安裝需要較高的客製化成本。

- 非住宅樓梯間的疏散和《美國殘障人士法案》(ADA)限制

- 對產品召回和法律責任的擔憂可能會影響採購信心。

- 產業價值鏈分析

- 宏觀經濟因素對市場的影響

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 軌道方向

- 直線

- 曲線

- 按使用者屬性

- 坐式

- 直立式

- 融合的

- 按安裝類型

- 室內的

- 戶外的

- 透過使用

- 住宅

- 衛生保健

- 政府

- 休閒娛樂

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 荷蘭

- 瑞典

- 瑞士

- 波蘭

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 紐西蘭

- 印尼

- 馬來西亞

- 泰國

- 越南

- 菲律賓

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 以色列

- 卡達

- 科威特

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 埃及

- 摩洛哥

- 肯亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Savaria Corporation

- Stannah Lifts Holdings Ltd.

- Acorn Mobility Services Limited

- Bruno Independent Living Aids, Inc.

- TK Access Solutions Limited

- Handicare AB

- Platinum Stairlifts Limited

- Bespoke Stairlifts Limited

- Otolift Trapliften BV

- Harmar Mobility, LLC

- AmeriGlide, Inc.

- Lehner Lifttechnik GmbH

- Hawle Treppenlifte GmbH

- HIRO LIFT Hillenkatter+Ronsieck GmbH

- Vimec Srl

- Garaventa(Canada)Ltd.

- Lifeway Mobility Holdings LLC

- Brooks Stairlifts Limited

- Otis Worldwide Corporation

- TK Elevator GmbH

- Access BDD(TK Elevator)

第7章 市場機會與未來展望

According to Mordor Intelligence, the stair lift market size is expected to grow from USD 1.17 billion in 2025 to USD 1.24 billion in 2026 and is forecast to reach USD 1.64 billion by 2031 at 5.81% CAGR over 2026-2031.

This report is Segmented by Rail Orientation (Straight, and Curved), User Orientation (Seated, Standing, and Integrated), Installation (Indoor, and Outdoor), Application (Residential, Healthcare, Government, and Leisure and Entertainment), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Stair Lift Market Trends and Insights

Accelerating Population Aging and Aging-In-Place Adoption

The 65-plus population continues to expand, which enlarges the addressable base for residential mobility solutions and supports unit growth for the stair lift market. Globally, aging is widespread with the share of individuals aged 60-plus rising across most regions through 2050, which increases the need for safe home access interventions. Fewer older adults reside in institutional settings compared with prior decades, which shifts budgets toward home modifications such as stair lifts and ramped entries. Straight stair lifts priced in the USD 3,000 to USD 5,000 range provide a practical alternative to facility-based care for many households. International public health initiatives promoting age-friendly communities emphasize the importance of accessible housing design and retrofits.

Stricter Accessibility Standards and Code Updates Since 2020

ASME A18.1-2023 came into effect in March 2024 with enhanced testing for overspeed and updated emergency communication requirements, which raises baseline safety and reduces brand differentiation based on safety signaling alone. Code harmonization and explicit permitting standards help dealers operate across states with fewer delays, which supports more predictable lead times and better customer experience. In parallel, EU harmonization programs such as EN 81-40 and the European Accessibility Act standardize design requirements across member countries, which channels engineering roadmaps toward tactile controls, documentation accessibility, and consistent safety systems. Greater clarity around safety and installation parameters helps reduce rework and aligns builders, architects, and inspectors with consistent expectations for compliant inclined lifts. These changes improve end-user trust and lower perceived risk, which supports replacement and upgrade cycles in the stair lift market.

Limited Medicare Coverage and High Out-of-Pocket Burden

Original Medicare does not classify stairlifts as durable medical equipment, which means there is no standardized federal coverage pathway for most beneficiaries. Medicare Advantage plans can offer supplemental benefits, yet inclusion is plan-specific, subject to prior authorization, and limited in scope, which produces uneven access across counties. Medicaid waiver coverage varies by state and can involve long waitlists, which slows conversion even for eligible consumers. By contrast, Veterans Affairs housing grants can be substantial for those who meet the criteria, including the Specially Adapted Housing grant of up to USD 126,526 in fiscal year 2026, which can fund comprehensive accessibility upgrades. Straight stairlifts typically cost USD 3,000 to USD 5,000, and curved lifts can reach well above USD 10,000, which places a significant out-of-pocket expense on fixed-income households when no public or private coverage applies.

Other drivers and restraints analyzed in the detailed report include:

- Residential Renovation and Retrofit Momentum in Multi-Story Homes

- Advancements in Battery Backup, Sensors, and Remote Diagnostics

- High Customization Costs for Curved Rails and Complex Installs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Straight stairlifts held 54% of the stair lift market share in 2025, with pre-fabricated rails that shorten installation windows and lower price points for first-time buyers. The stair lift market favors straight runs in retrofit scenarios that involve common residential layouts, which supports dealer volume purchases and consistent inventory turns. Curved systems are forecast to expand at a 10.34% CAGR from 2026 to 2031 as modular rail designs compress lead times and broaden eligible staircase types. Harmar's modular curved platform introduced connected diagnostics and a thin-rail profile for narrow runs, which helped enable next-day deliveries in select metro areas. Twin-rail configurations for tight bends support premium placements in older European housing stock, which benefits dealers that specialize in high-complexity projects. Faster on-site assembly using stock-able rail sections has improved installation speed and widened choice for buyers who require custom turns without extended fabrication windows.

Comparing adoption patterns shows straight models dominate standardized retrofits while curved lifts concentrate in homes with spirals, mid-landings, and ornate profiles. The stair lift market size for curved lifts is projected to rise in line with modular engineering improvements that cut delivery time and improve serviceability. Hinged rail options and fold-away sections help preserve egress widths at landings and entries, which supports compliance in smaller dwellings and shared stairways. Outdoor curved variants add weatherproofing and corrosion resistance for coastal and high-UV settings, which expands their appeal for deck access and multi-level exterior stairs. Collectively, these features tilt a larger share of complex projects toward curved systems while straight rails remain the high-volume core of the stair lift market.

Seated lifts held 48% share in 2025 based on comfort, intuitive controls, and adjustable seating that suits older adults with limited knee flexibility. Powered swivel options and ergonomic armrests aid transfers at landings, which reduces fall risk and eases use in tight top landings. Standing and perch configurations are projected to grow at an 8.76% CAGR from 2026 to 2031, supported by clinical recommendations for users who cannot tolerate full sitting. Perch designs utilize a semi-standing posture and compact folded depth, which works well on narrow staircases, particularly in legacy homes common in dense urban cores. Integrated models that combine seated and standing options are gaining more use in rehabilitation settings where multi-user flexibility is crucial.

This orientation mix reflects clinical needs and household constraints, which shape product selection and price sensitivity across the stair lift market. Standing solutions fit narrow spaces and certain orthopedic profiles, while seated models set the comfort baseline for the largest user group. Updated safety standards outline seat height ranges and graspability dimensions that help standardize ergonomics across brands, which raises the baseline safety signal for purchasers. Dealers that carry both standing and seated portfolios address multi-user households better than single-orientation brands. Over time, incremental ergonomic refinements are expected to lift satisfaction and reduce service issues in both configurations in the stair lift industry.

Geography Analysis

Europe led the global stair lift market in 2025, accounting for 65% of the market, driven by significant deployment in the United Kingdom, Germany, and other Western European countries. Harmonized EU safety and documentation standards have streamlined cross-border operations, reducing product variations and enabling multi-country dealer strategies. VAT relief programs and localized grants continue to drive demand, although fluctuations in public budgets impact quarterly volumes. Nordic countries are witnessing increased interest in connected and premium models, reflecting the region's advanced adoption of smart homes. In contrast, affordability constraints in Eastern Europe limit growth compared to wealthier markets in the region. Europe's clear policy framework and well-established distribution networks solidify its position as the global revenue leader.

Although North America represented a smaller market base in 2025, it is projected to grow at a robust CAGR of 10.50% through 2031. Higher disposable incomes and mature dealer networks in the region, particularly in the United States, support out-of-pocket purchases and frequent upgrades. The increasing older adult population expands the potential customer base for mobility solutions and home safety retrofits. Federal initiatives, such as Veterans Affairs housing grants and home modification programs facilitated by non-profits, help reduce affordability barriers for eligible households. Additionally, the growing presence of stair lift manufacturers in Mexico enhances supply flexibility and reduces delivery costs for dealer networks in the U.S. Sun Belt and Midwest regions.

The Asi-Pacific region is experiencing growing momentum as policy initiatives and demographic changes reshape market demand. Expanding dealer networks and increased policy focus on barrier-free housing are driving growth in the region. Rapid population aging in major economies like China and Australia's aging-in-place policies, coupled with high household incomes, support steady adoption in urban centers. In Southeast Asia and South Asia, early-stage adoption is concentrated among middle- and upper-income households in major cities, reflecting typical early-market trends. As supply chains adapt to localized demand, the Asia-Pacific stair lift market is well-positioned for sustained growth through 2031.

- Savaria Corporation

- Stannah Lifts Holdings Ltd.

- Acorn Mobility Services Limited

- Bruno Independent Living Aids, Inc.

- TK Access Solutions Limited

- Handicare AB

- Platinum Stairlifts Limited

- Bespoke Stairlifts Limited

- Otolift Trapliften B.V.

- Harmar Mobility, LLC

- AmeriGlide, Inc.

- Lehner Lifttechnik GmbH

- Hawle Treppenlifte GmbH

- HIRO LIFT Hillenkatter + Ronsieck GmbH

- Vimec S.r.l.

- Garaventa (Canada) Ltd.

- Lifeway Mobility Holdings LLC

- Brooks Stairlifts Limited

- Otis Worldwide Corporation

- TK Elevator GmbH

- Access BDD (TK Elevator)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Population Aging and Aging-In-Place Adoption

- 4.2.2 Stricter Accessibility Standards and Code Updates Since 2020

- 4.2.3 Residential Renovation and Retrofit Momentum in Multi-Story Homes

- 4.2.4 Advancements in Battery Backup, Sensors, and Remote Diagnostics

- 4.2.5 Medicaid Waivers and National Grants Unlocking Home Modifications

- 4.2.6 State-Level Adoption of ASME A18.1 and Permit Clarity Reducing Friction

- 4.3 Market Restraints

- 4.3.1 Limited Medicare Coverage and High Out-of-Pocket Burden

- 4.3.2 High Customization Costs for Curved Rails and Complex Installs

- 4.3.3 Egress and ADA Constraints in Non-Residential Stairways

- 4.3.4 Recalls and Liability Concerns Impacting Procurement Confidence

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Rail Orientation

- 5.1.1 Straight

- 5.1.2 Curved

- 5.2 By User Orientation

- 5.2.1 Seated

- 5.2.2 Standing

- 5.2.3 Integrated

- 5.3 By Installation

- 5.3.1 Indoor

- 5.3.2 Outdoor

- 5.4 By Application

- 5.4.1 Residential

- 5.4.2 Healthcare

- 5.4.3 Government

- 5.4.4 Leisure and Entertainment

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Netherlands

- 5.5.3.8 Sweden

- 5.5.3.9 Switzerland

- 5.5.3.10 Poland

- 5.5.3.11 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 New Zealand

- 5.5.4.7 Indonesia

- 5.5.4.8 Malaysia

- 5.5.4.9 Thailand

- 5.5.4.10 Vietnam

- 5.5.4.11 Philippines

- 5.5.4.12 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Israel

- 5.5.5.5 Qatar

- 5.5.5.6 Kuwait

- 5.5.5.7 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Egypt

- 5.5.6.4 Morocco

- 5.5.6.5 Kenya

- 5.5.6.6 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Savaria Corporation

- 6.4.2 Stannah Lifts Holdings Ltd.

- 6.4.3 Acorn Mobility Services Limited

- 6.4.4 Bruno Independent Living Aids, Inc.

- 6.4.5 TK Access Solutions Limited

- 6.4.6 Handicare AB

- 6.4.7 Platinum Stairlifts Limited

- 6.4.8 Bespoke Stairlifts Limited

- 6.4.9 Otolift Trapliften B.V.

- 6.4.10 Harmar Mobility, LLC

- 6.4.11 AmeriGlide, Inc.

- 6.4.12 Lehner Lifttechnik GmbH

- 6.4.13 Hawle Treppenlifte GmbH

- 6.4.14 HIRO LIFT Hillenkatter + Ronsieck GmbH

- 6.4.15 Vimec S.r.l.

- 6.4.16 Garaventa (Canada) Ltd.

- 6.4.17 Lifeway Mobility Holdings LLC

- 6.4.18 Brooks Stairlifts Limited

- 6.4.19 Otis Worldwide Corporation

- 6.4.20 TK Elevator GmbH

- 6.4.21 Access BDD (TK Elevator)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and unmet-need assessment

樓梯升降椅市場 - 全球產業規模、佔有率、趨勢、機會、預測:軌道方向、使用者導向、安裝方式、應用、區域及競爭格局,2021-2031年

樓梯升降椅市場 - 全球產業規模、佔有率、趨勢、機會、預測:軌道方向、使用者導向、安裝方式、應用、區域及競爭格局,2021-2031年 樓梯升降椅市場:按產品類型、安裝類型、最終用戶和分銷管道分類 - 2026-2032年全球市場預測

樓梯升降椅市場:按產品類型、安裝類型、最終用戶和分銷管道分類 - 2026-2032年全球市場預測 樓梯升降椅市場:按產品類型、模式類型、操作方式、最終用戶和地區分類

樓梯升降椅市場:按產品類型、模式類型、操作方式、最終用戶和地區分類 歐洲樓梯升降椅:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)美國樓梯升降椅:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

歐洲樓梯升降椅:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)美國樓梯升降椅:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 全球樓梯升降椅市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球樓梯升降椅市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球樓梯升降機與攀爬設備市場報告

2026年全球樓梯升降機與攀爬設備市場報告 2026-2030年全球樓梯升降機市場

2026-2030年全球樓梯升降機市場 樓梯升降椅市場規模、佔有率和成長分析(按設備類型、用戶群、安裝方式、最終用戶和地區分類)-2026-2033年產業預測全球樓梯升降機市場規模(按產品類型、應用、最終用戶、區域範圍和預測)

樓梯升降椅市場規模、佔有率和成長分析(按設備類型、用戶群、安裝方式、最終用戶和地區分類)-2026-2033年產業預測全球樓梯升降機市場規模(按產品類型、應用、最終用戶、區域範圍和預測)