|

市場調查報告書

商品編碼

2066630

北美物流自動化:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)North America Logistics Automation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

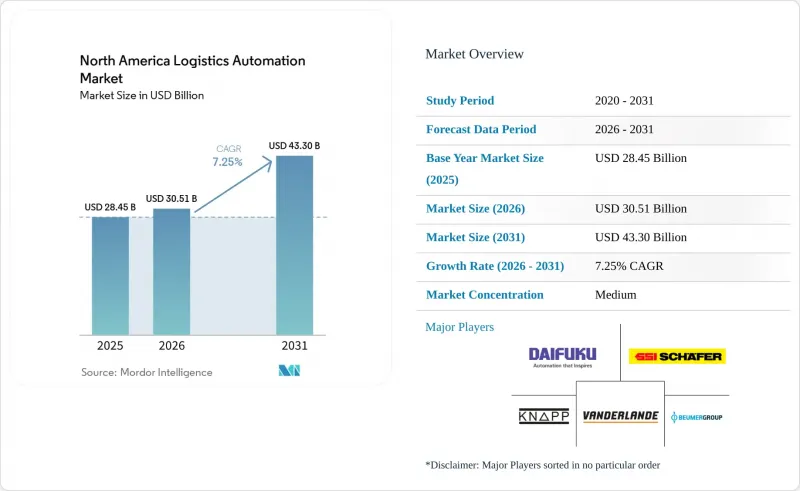

根據 Mordor Intelligence 預測,北美物流自動化市場規模將從 2025 年的 284.5 億美元成長到 2026 年的 305.1 億美元,然後在 2031 年達到 433 億美元,2026 年至 2031 年的複合年成長率為 7.25%。

本報告按功能(倉儲自動化和運輸自動化)、自動化程度(全自動系統和半自動化系統)、組件(硬體、軟體和服務)、最終用戶行業(例如,電子商務和小包裹、食品飲料、食品零售、服裝時尚)以及國家/地區進行細分。市場預測以美元計價。

北美物流自動化市場趨勢與洞察

電子商務履約密度及當日送達服務水平

在北美物流自動化市場,當日達正從加值服務轉變為一項核心營運需求。預計2026年中期,亞馬遜的當日達或隔日達訂單量將超過10億件,併計劃於2026年4月在美國中等規模的大都會區開設18個新的當日達配送中心。這進一步擴大了郊區和遠郊地區對自動化的需求。這種轉變迫使企業提高履約的處理單元數量,使得高速分類、緊湊型自動化立體倉庫(ASRS)以及「貨到人」的工作流程變得更加關鍵。同時,投資目標也從大型全方位配送中心轉向小規模的微型樞紐,而這些微型樞紐仍需要高密度自動化才能保持競爭力。在北美物流自動化市場,日益成長的服務水準壓力正在影響設施設計、人事費用和儲存密度。因此,模組化系統正加速發展,這些系統可以部署在更靠近需求的地方,而無需等待大規模的待開發區建設。

倉儲業人手不足和薪資上漲

勞動力短缺仍然是北美物流自動化市場最強勁的經濟促進因素之一。這是因為營運商正在著力解決結構性問題,而非應對短期經濟週期。美國倉儲產業的平均時薪從2025年1月的25.02美元上漲至2026年1月的26.58美元,並在2026年2月進一步上漲至26.68美元,顯示整個倉儲網路持續面臨高薪資壓力。截至2026年3月的12個月內,私部門員工的薪資成本增加了3.4%。這表明,儘管實際工資成長有限,但人事費用壓力仍然強勁。 2025年ILR評論的一項研究發現,在倉庫中引入機器人可使嚴重工傷事故減少40%,輕微工傷事故增加77%。這進一步凸顯了在人機共存的工作場所中,人體工學設計的重要性。因此,採購重點正從單純增加機器人數量轉向部署「貨到人」工作站並設計更最佳化的工作流程。在北美物流自動化市場,連接人與機器的軟體正日益受到關注,被視為提高勞動生產力的最有效途徑。

固定線路自動化需要大量初始投資

在北美物流自動化市場,固定位置自動化仍是一個重要的限制因素。這是因為大規模輸送機網路、整合分揀系統和端到端自動化立體倉庫(ASRS)系統仍需要數年的資本投資。這種壓力對中型第三方物流公司和區域經銷商的影響尤其顯著,因為他們不像大型零售商和經銷商那樣擁有柔軟性的財力。此外,鋼鐵相關設備價格的上漲延長了投資回收期,也使得承包工程項目更加謹慎,讓投資決策變得更加困難。然而,稅收方面有一些利多因素。根據美國國稅局(IRS)的指導意見,合格的、於2026年投入運作的設備的179條款扣除上限已達到256萬美元。類似的稅收框架還允許對合格的資產進行100%的特殊折舊,從而降低了符合條件的自動化資產第一年的實際成本。儘管有這些支援措施,但考慮到此類專案的高風險,北美物流自動化市場的許多買家仍然傾向於分階段部署和靈活的商業模式。

細分市場分析

2025年,倉儲自動化佔北美物流自動化市場銷售額的61.34%,佔核心地位。營運商將重點放在倉庫內的揀貨、儲存、分類和輸送機密集型物流。倉儲自動化在2025年佔據北美物流自動化市場61.34%的佔有率,這在可控的室內環境中歷來是最容易實現投資回報(ROI)的領域。 「貨到人」模式,例如自動化立體倉庫系統(ASRS)、自主移動機器人(AMR)車隊和倉庫執行軟體,持續推動著這一領域的發展,因為它們能夠直接提高處理能力、勞動生產率和訂單準確性。 2026年5月,美敦力(Medline)在其位於科羅拉多科羅拉多的物流中心部署了第24個自動化倉庫(AutoStore),進一步擴大了這一趨勢。該自動化倉庫新增了96台機器人和38,000個貨位,以滿足當地需求。室內運輸仍然是北美物流自動化市場的重點,大規模業者率先在全國範圍內實現自動化標準化。

儘管運輸自動化起步規模小規模,但它是成長最快的領域,預計到2031年將以7.94%的複合年成長率成長,這反映了SAE 4級貨運路線的早期商業化。 2026年1月,Gatik成為美國首家完成大規模全自動商業配送的公司,為德克薩斯州、阿肯色州和亞利桑那州的財富50強零售商成功完成了6萬筆無人配送訂單,且未發生任何事故。同樣在2026年5月,Aurora Innovation和McLane在德克薩斯州達拉斯和德克薩斯州之間開通了無人運輸服務,並宣布計劃將業務擴展到全部區域。

到2025年,半自動化系統將佔銷售額的55.90%,這反映了北美物流自動化市場中大多數運作中倉庫所採用的實際模式。如此高的比例源於許多現有設施(棕地)仍然採用人工操作(透過倉庫管理系統WMS)與機器人相結合的模式,這些機器人專門負責重複性任務,例如從人工手中揀貨、移動托盤和碼垛。這種模式使營運商能夠在不承擔系統全面遷移相關成本和營運風險的情況下提高處理能力。 2025年,Staples Canada在其溫哥華履約中心部署了50台Locus Robotics自主移動機器人(AMR),並在短短四天內實現了全面運營整合,充分展現了這種模式的優勢。在北美物流自動化產業,這種混合模式仍然是處理量波動較大、存在季節性需求高峰或無法重新設計現有佈局的設施的標準選擇。

全自動化系統正以更快的速度成長,預計到2031年將以8.13%的複合年成長率成長。這主要歸功於待開發區專案和大規模網路現代化改造中擴大採用無人或近乎無人的工作流程。感測器成本的降低、感知軟體的進步以及人們對機器人持續運作信心的增強,都推動了這一趨勢。在2026年的MODEX展會上,Locus Robotics發布了Locus Array,這是一款全自主的履約系統,它結合了移動機器人、整合式揀選臂和人工智慧驅動的感知功能,目前已在北美DHL供應鏈中部署。隨後,在2026年5月,Locus收購了Nexera Robotics,並透過引進NeuraGrasp技術擴展了系統的SKU支援範圍。因此,在北美物流自動化市場,隨著移動機器人和機器人操作擴大在共用的編配層上協同工作,部分自動化和完全自主之間的差距正在縮小。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電子商務履約密度及當日送達水平

- 倉儲業人手不足和薪資上漲

- 履約中心 AMR 與 AI編配實施現狀

- 墨西哥和美國近岸外包主導的網路重組

- 降低高產能履約中心的工效學風險

- 國內和跨境自動化投資的稅收優惠

- 市場限制因素

- 固定系統自動化需要較高的初始資本投入

- 整合舊有系統和棕地維修的複雜性。

- 鋼鐵關稅的變化以及自動化投資回收期的延長

- 機器人單元安全和網路安全方面的合規負擔

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 市場宏觀經濟趨勢的評估

第5章 市場規模與成長預測

- 按功能

- 倉庫自動化

- 成分

- 硬體

- 移動機器人

- 自動化倉庫系統

- 自動分類系統

- 傳送系統

- 自動識別和數據採集(AIDC)

- 揀貨

- 軟體

- 服務

- 硬體

- 成分

- 交通自動化

- 成分

- 硬體

- 軟體

- 服務

- 成分

- 倉庫自動化

- 按自動化級別

- 全自動系統

- 半自動系統

- 按組件

- 硬體

- 軟體

- 服務

- 按最終用戶行業分類

- 電子商務和小包裹遞送

- 食品/飲料

- 食品零售

- 服裝與時尚

- 製造業

- 其他終端用戶產業

- 國家

- 美國

- 加拿大

- 墨西哥

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Daifuku Co., Ltd.

- SSI SCHAEFER AG

- KNAPP AG

- Vanderlande Industries BV

- BEUMER Group GmbH & Co. KG

- Dematic Corp.

- Mecalux, SA

- Swisslog Holding AG

- TGW Logistics Group GmbH

- WITRON Logistik+Informatik GmbH

- Kardex Holding AG

- AutoStore Holdings Ltd.

- Exotec SAS

- Geekplus Technology Co., Ltd.

- Hai Robotics Co., Ltd.

- GreyOrange Pte. Ltd.

- Locus Robotics Corp.

- Cimcorp Oy

- System Logistics SpA

- Bastian Solutions

第7章 市場機會與未來展望

According to Mordor Intelligence, the north america logistics automation market size is expected to grow from USD 28.45 billion in 2025 to USD 30.51 billion in 2026 and is forecast to reach USD 43.30 billion by 2031 at 7.25% CAGR over 2026-2031.

This report is Segmented by Function (Warehouse Automation and Transportation Automation), Automation Level (Fully-Automated Systems and Semi-Automated Systems), Component (Hardware, Software, and Services), End-User Industry (E-Commerce and Parcel, Food and Beverage, Grocery Retail, Apparel and Fashion, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

North America Logistics Automation Market Trends and Insights

E-Commerce Fulfillment Density and Same-Day Service Levels

Same-day delivery has moved from a premium service into a core operating requirement across the North America logistics automation market. Amazon exceeded 1 billion same-day or overnight deliveries in the year-to-date period through mid-2026 and added 18 same-day facilities in mid-sized US metro areas in April 2026, which pushed automation demand deeper into suburban and exurban nodes. That shift forces operators to process more units per square meter, which strengthens the case for high-speed sortation, compact ASRS, and goods-to-person workflows. It also redirects investment away from only very large fulfillment centers and toward smaller micro-hubs that still need dense automation to stay competitive. In the North America logistics automation market, service-level pressure is now shaping facility design as much as labor cost or storage density. The result is a faster move toward modular systems that can be deployed close to demand without waiting for full-scale greenfield construction.

Warehouse Labor Scarcity and Wage Inflation

Labor scarcity remains one of the strongest economic drivers in the North America logistics automation market because operators are responding to a structural problem rather than a short-term cycle. Average hourly earnings in US warehousing and storage reached USD 26.58 in January 2026 and USD 26.68 in February 2026, up from USD 25.02 in January 2025, which kept wage pressure elevated across warehouse networks. Compensation costs for private industry workers rose 3.4% in the 12 months to March 2026, which shows that payroll pressure remained firm even as real gains stayed limited. A 2025 ILR Review study found that warehouse robotics was associated with a 40% reduction in severe injuries and a 77% rise in non-severe injuries, which reinforced the need for better ergonomic design at human-robot workstations. This has shifted procurement priorities toward goods-to-person stations and better workflow design rather than only toward higher robot counts. In the North America logistics automation market, software that coordinates people and machines is increasingly viewed as the clearest path to labor-productivity gains.

High Upfront Capital Outlays for Fixed Automation

Fixed automation remains a real constraint on the North America logistics automation market because large conveyor networks, integrated sortation, and end-to-end ASRS systems still require multiyear capital commitments. This pressure is strongest among mid-market 3PLs and regional distributors that do not have the same balance sheet flexibility as large retailers or large distributors. Steel-related equipment inflation has also made investment decisions harder by extending payback periods and increasing caution around turnkey projects. Operators do have some relief through tax policy, as the Section 179 deduction ceiling for qualifying equipment placed in service in 2026 reached USD 2,560,000 under IRS guidance. The same tax framework also supports 100% bonus depreciation for qualifying property, which lowers the effective first-year cost of eligible automation assets. Even with that support, many buyers in the North America logistics automation market still prefer phased deployments or flexible commercial models when project risk remains high.

Other drivers and restraints analyzed in the detailed report include:

- AMR and AI Orchestration Adoption Across Fulfillment Centers

- Nearshoring-Led Network Redesign in Mexico and The United States

- Legacy-System Integration and Brownfield Retrofit Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Warehouse automation held 61.34% of revenue in 2025, which placed it at the center of the North America logistics automation market as operators focused on picking, storage, sortation, and conveyor-intensive flows inside the facility. Warehouse automation accounted for 61.34% of the North America logistics automation market share in 2025 because the return on investment has historically been easiest to capture inside controlled indoor environments. Goods-to-person ASRS, AMR fleets, and warehouse execution software continue to define this segment because they directly improve throughput, labor productivity, and order accuracy. Medline expanded that pattern in May 2026 when it deployed its 24th AutoStore installation at its Aurora, Colorado distribution center, adding 96 robots and 38,000 bins to support regional demand. The North America logistics automation market continues to treat indoor handling as the first place where high-volume operators standardize automation across a national footprint.

Transportation automation started from a smaller base, but it is the fastest-growing function at a 7.94% CAGR through 2031, and that growth reflects the early commercialization of SAE Level 4 freight lanes. Gatik became the first US company to complete fully driverless commercial deliveries at scale in January 2026, recording 60,000 driverless orders for Fortune 50 retailers in Texas, Arkansas, and Arizona without incident. Aurora Innovation and McLane also announced in May 2026 that they would begin driverless hauls in Texas between Dallas and Houston, with plans to expand across the US Sun Belt.

Semi-automated systems held 55.90% of revenue in 2025, which reflected the practical structure of most active warehouses in the North America logistics automation market. Semi-automated systems carried 55.90% of revenue because most brownfield sites still combine WMS-directed human labor with targeted robotics for repetitive tasks such as goods-to-person picking, pallet movement, or palletizing. This model helps operators improve throughput without taking on the cost and operational risk of a full cutover. Staples Canada showed the appeal of this approach in 2025 when it deployed 50 Locus Robotics AMRs in a Vancouver fulfillment center and reached full operational integration within 4 days. In the North America logistics automation industry, this hybrid structure remains the default for facilities with variable volumes, seasonal spikes, and existing layouts that are not easy to redesign.

Fully-automated systems are growing faster, with an 8.13% CAGR through 2031, because greenfield projects and major network refreshes are now being designed for unattended or near-unattended workflows. Falling sensor costs, better perception software, and stronger confidence in continuous robotic operation are supporting that move. Locus Robotics launched Locus Array at MODEX 2026 as a fully autonomous fulfillment system that combines mobile robotics, an integrated picking arm, and AI-powered perception, with early deployments already underway at DHL Supply Chain in North America. Locus then acquired Nexera Robotics in May 2026 to add NeuraGrasp technology and widen the system's SKU-handling range. The North America logistics automation market is therefore narrowing the gap between partial automation and full autonomy as mobile robotics and robotic manipulation increasingly run on a shared orchestration layer.

List of Companies Covered in this Report:

- Daifuku Co., Ltd.

- SSI SCHAEFER AG

- KNAPP AG

- Vanderlande Industries B.V.

- BEUMER Group GmbH & Co. KG

- Dematic Corp.

- Mecalux, S.A.

- Swisslog Holding AG

- TGW Logistics Group GmbH

- WITRON Logistik + Informatik GmbH

- Kardex Holding AG

- AutoStore Holdings Ltd.

- Exotec SAS

- Geekplus Technology Co., Ltd.

- Hai Robotics Co., Ltd.

- GreyOrange Pte. Ltd.

- Locus Robotics Corp.

- Cimcorp Oy

- System Logistics S.p.A.

- Bastian Solutions

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-commerce Fulfillment Density and Same-day Service Levels

- 4.2.2 Warehouse Labor Scarcity and Wage Inflation

- 4.2.3 AMR and AI Orchestration Adoption Across Fulfillment Centers

- 4.2.4 Nearshoring-led Network Redesign in Mexico and the United States

- 4.2.5 Ergonomic-risk Mitigation in High-throughput Fulfillment Sites

- 4.2.6 Tax Incentives for Domestic and Cross-border Automation Investments

- 4.3 Market Restraints

- 4.3.1 High Upfront Capital Outlays for Fixed Automation

- 4.3.2 Legacy-system Integration and Brownfield Retrofit Complexity

- 4.3.3 Steel Tariff Volatility and Longer Automation Payback

- 4.3.4 Robot-cell Safety and Cybersecurity Compliance Burden

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Function

- 5.1.1 Warehouse Automation

- 5.1.1.1 Component

- 5.1.1.1.1 Hardware

- 5.1.1.1.1.1 Mobile Robots

- 5.1.1.1.1.2 Automated Storage and Retrieval Systems

- 5.1.1.1.1.3 Automated Sorting Systems

- 5.1.1.1.1.4 Conveyor Systems

- 5.1.1.1.1.5 Automatic Identification and Data Collection (AIDC)

- 5.1.1.1.1.6 Order Picking

- 5.1.1.1.2 Software

- 5.1.1.1.3 Services

- 5.1.1.1.1 Hardware

- 5.1.1.1 Component

- 5.1.2 Transportation Automation

- 5.1.2.1 Component

- 5.1.2.1.1 Hardware

- 5.1.2.1.2 Software

- 5.1.2.1.3 Services

- 5.1.2.1 Component

- 5.1.1 Warehouse Automation

- 5.2 By Automation Level

- 5.2.1 Fully-Automated Systems

- 5.2.2 Semi-Automated Systems

- 5.3 By Component

- 5.3.1 Hardware

- 5.3.2 Software

- 5.3.3 Services

- 5.4 By End-User Industry

- 5.4.1 E-commerce and Parcel

- 5.4.2 Food and Beverage

- 5.4.3 Grocery Retail

- 5.4.4 Apparel and Fashion

- 5.4.5 Manufacturing

- 5.4.6 Other End-User Industries

- 5.5 By Country

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Daifuku Co., Ltd.

- 6.4.2 SSI SCHAEFER AG

- 6.4.3 KNAPP AG

- 6.4.4 Vanderlande Industries B.V.

- 6.4.5 BEUMER Group GmbH & Co. KG

- 6.4.6 Dematic Corp.

- 6.4.7 Mecalux, S.A.

- 6.4.8 Swisslog Holding AG

- 6.4.9 TGW Logistics Group GmbH

- 6.4.10 WITRON Logistik + Informatik GmbH

- 6.4.11 Kardex Holding AG

- 6.4.12 AutoStore Holdings Ltd.

- 6.4.13 Exotec SAS

- 6.4.14 Geekplus Technology Co., Ltd.

- 6.4.15 Hai Robotics Co., Ltd.

- 6.4.16 GreyOrange Pte. Ltd.

- 6.4.17 Locus Robotics Corp.

- 6.4.18 Cimcorp Oy

- 6.4.19 System Logistics S.p.A.

- 6.4.20 Bastian Solutions

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

物流自動化市場機會、成長要素、產業趨勢分析及2026-2035年預測

物流自動化市場機會、成長要素、產業趨勢分析及2026-2035年預測 物流自動化市場:按組件、物流類型、技術、運作模式、部署類型、應用和最終用戶產業分類-2026-2032年全球市場預測

物流自動化市場:按組件、物流類型、技術、運作模式、部署類型、應用和最終用戶產業分類-2026-2032年全球市場預測 物流自動化市場規模、佔有率、趨勢和預測:按組件、功能、公司規模、行業和地區分類,2026-2034 年

物流自動化市場規模、佔有率、趨勢和預測:按組件、功能、公司規模、行業和地區分類,2026-2034 年 2026年全球容器化物流系統市場報告2026年全球數位雙胞胎物流控制塔顯示器市場報告

2026年全球容器化物流系統市場報告2026年全球數位雙胞胎物流控制塔顯示器市場報告 物流自動化市場:依組件、公司規模、產業、地區分類

物流自動化市場:依組件、公司規模、產業、地區分類 物流自動化市場分析與預測(至2035年):依類型、產品類型、服務、技術、元件、應用、流程、部署模式、最終使用者、解決方案分類2026年全球物流自動化市場報告

物流自動化市場分析與預測(至2035年):依類型、產品類型、服務、技術、元件、應用、流程、部署模式、最終使用者、解決方案分類2026年全球物流自動化市場報告 物流自動化市場-全球產業規模、佔有率、趨勢、機會及預測(按組件、功能、產業垂直領域、地區及競爭格局分類,2021-2031年)按車輛類型、自動駕駛等級、推進類型、應用程式和最終用戶分類的全球自動駕駛物流解決方案市場預測(2026-2032 年)

物流自動化市場-全球產業規模、佔有率、趨勢、機會及預測(按組件、功能、產業垂直領域、地區及競爭格局分類,2021-2031年)按車輛類型、自動駕駛等級、推進類型、應用程式和最終用戶分類的全球自動駕駛物流解決方案市場預測(2026-2032 年)