|

市場調查報告書

商品編碼

2038696

物流自動化市場機會、成長要素、產業趨勢分析及2026-2035年預測Logistics Automation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

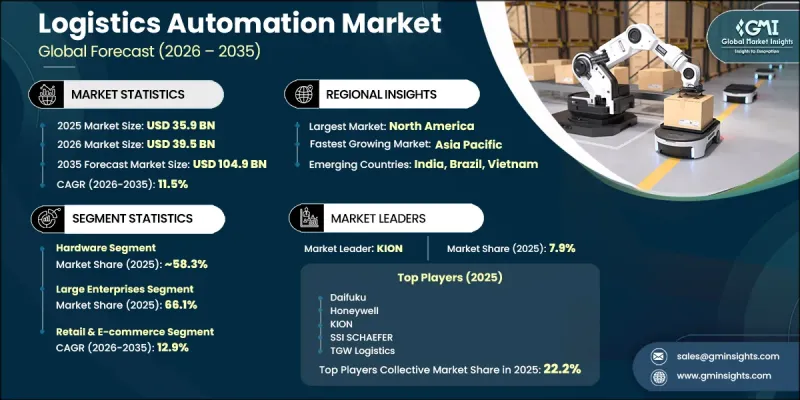

2025年全球物流自動化市場價值為359億美元,預計2035年將以11.5%的複合年成長率成長至1,049億美元。

物流市場擴張源自於其在各國經濟中重要的戰略地位,物流在許多國家對國內生產總值)貢獻顯著。各國政府和相關人員正加大對物流基礎設施的投資,以提高生產力、效率和國際競爭力。此外,正如美國聯邦統計局統計人員所指出的,物流和運輸是美國經濟產出的核心要素。現代物流營運正迅速向智慧自動化轉型,人工智慧和機器學習技術也從孤立的最佳化工具發展成為完全整合的編配系統。這些平台現在能夠即時協調庫存、勞動力和運輸,從而管理端到端的工作流程。倉庫管理和執行系統會根據營運需求和系統負載,動態地將任務分配給自主機器人、工人以及自動化工作站。運輸管理系統正擴大利用即時數據輸入(例如運作狀況和承運商活動)來最佳化路線規劃。此外,研究表明,結合有效的系統整合和勞動力適應性調整,提高自動化等級和機器人部署密度可以顯著提升營運效率。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 359億美元 |

| 預測金額 | 1049億美元 |

| 複合年成長率 | 11.5% |

預計到2025年,硬體領域將佔據58.3%的市場佔有率,市場規模將達到210億美元。這主要是由於實體自動化基礎設施的資本密集特性,包括輸送機、自動化倉庫系統(AS/RS)、碼垛設備、自動導引運輸車(AGV)和機器人升降設備。硬體仍然是物流自動化的基礎層,需要在軟體整合之前進行大量的前期投資。這些系統與倉庫管理和執行平台緊密整合,並且擴大採用人工智慧來提高路線效率、工作負載分配和預測性維護能力。

預計到2025年,大型企業將佔66.1%的市場佔有率,市場規模達238億美元。這一主導地位源自於大規模自動化部署所需的巨額資金投入,而這通常只有財力雄厚的企業才能承擔。主要採用者包括在全球多個倉庫中營運的零售連鎖企業、領先的電商公司以及第三方物流供應商。這些企業能夠有效管理長期投資週期,並在其分散式倉庫網路中部署先進的自動化技術,從而在與小規模的市場參與企業競爭中佔據明顯優勢。

美國物流自動化市場預計到2025年將達到109億美元,並在2026年至2035年間以12.3%的複合年成長率成長。美國高度發展的物流生態系統持續吸引對自動化技術的強勁投資。這一成長主要得益於電子商務的快速發展、倉儲營運中日益嚴重的勞動力短缺以及機器人和人工智慧驅動系統的廣泛應用。產業研究表明,該地區相當一部分物流決策者預計未來將更加依賴人工智慧,同時,他們對自動化供應鏈網路安全風險的擔憂也在不斷加劇。

目錄

第1章:調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 電子商務的成長和對最後一公里配送的需求。

- 人手不足和營運成本上升

- 對即時可視性和供應鏈韌性的需求

- 人工智慧、物聯網和機器人技術的進步

- 產業潛在風險與挑戰

- 前期投資額大,且投資報酬率不確定性

- 與舊有系統整合的複雜性

- 市場機遇

- 亞太地區和拉丁美洲新興市場的採用情況

- 透過雲端解決方案滲透到中小企業市場

- 自動駕駛車輛與無人機配送的融合

- 促進因素

- 科技與創新趨勢

- 目前技術

- 無線射頻識別(RFID)

- 自動化倉庫系統(AS/RS)

- 機器人流程自動化 (RPA)

- 新興技術

- 自主移動機器人(AMR)

- 人工智慧驅動的預測物流平台

- 無人機配送系統

- 用於供應鏈最佳化的數位雙胞胎

- 目前技術

- 成長潛力分析

- 監理情勢

- 北美洲

- 美國 - 聯邦汽車運輸安全管理局 (FMCSA)

- 美國職業安全與健康管理局 (OSHA)

- 加拿大 - 加拿大運輸部

- 歐洲

- 歐盟交通運輸總司(DG MOVE)

- 德國 - 聯邦數位和交通部 (BMDV)

- 亞太地區

- 中國 - 中國物流與採購聯合會(CFLP)

- 印度 - 物流部 (DoL)

- 拉丁美洲

- 巴西 - 國家陸上運輸管理局 (ANTT)

- 墨西哥 - 標準化總局

- 中東和非洲

- 阿拉伯聯合大公國 - 全國貨運和物流協會 (NAFL)

- 沙烏地阿拉伯 - 交通運輸和物流服務部

- 北美洲

- 波特五力分析

- PESTEL 分析

- 專利趨勢(基於初步調查)

- 投資與資金籌措分析

- 成本細分分析

- 研發費用

- 製造和硬體生產成本

- 軟體開發和授權成本

- 實施、設定和客戶整合成本

- 多式聯運的整合

- 多模態自動化

- 港口和碼頭自動化整合

- 鐵路、公路和航空運輸及數據的互通性

- 跨境物流自動化面臨的挑戰

- 網路安全和資料基礎設施

- 自動化物流網路中的網路安全風險

- 雲端基礎設施和安全資料整合

- 智慧物流營運中的物聯網安全挑戰

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 針對特定領域的生成式人工智慧應用案例和實施藍圖

- 風險、限制和監管考量

- 預測假設和情境分析(基於初步研究)

- 基本案例-驅動複合年成長率的關鍵宏觀經濟與產業變量

- 樂觀情境-宏觀經濟與產業的順風

- 悲觀情景-宏觀經濟放緩或產業逆風

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲(MEA)

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃及資金籌措

- 企業級分層基準測試

- 層級分類標準與選擇標準

- 按收入、地區和創新能力分類的層級定位矩陣。

第5章 市場估計與預測:依組件分類,2022-2035年

- 硬體

- 自主機器人

- 自動化倉庫系統(AS/RS)

- 自動分類系統

- 輸送機系統

- 卸垛/碼垛系統

- 自動識別和數據採集(AIDC)

- 軟體

- 倉庫管理系統(WMS)

- 運輸管理系統(TMS)

- 服務

- 諮詢

- 實施與整合

- 支援和維護

第6章 市場估計與預測:依應用領域分類,2022-2035年

- 倉庫/儲存管理

- 運輸管理

第7章 市場估計與預測:依公司規模分類,2022-2035年

- 大公司

- 中小企業

第8章 市場估算與預測:依最終用途分類,2022-2035年

- 製造業

- 零售與電子商務

- 食品/飲料

- 醫療和藥品

- 車

- 郵件和小包裹

- 石油和天然氣

- 其他

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 荷蘭

- 挪威

- 瑞典

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 澳洲

- 印尼

- 新加坡

- 越南

- 菲律賓

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 智利

- 中東和非洲(MEA)

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- 世界公司

- Daifuku

- KION Group

- Honeywell

- SSI SCHAEFER Group

- Toyota Industries

- Rockwell Automation

- KNAPP

- KUKA Global(Midea)

- ABB

- Beumer Group

- Korber

- TGW Logistics

- 當地公司

- FORTNA

- WITRON

- Fives Group

- SAVOYE

- FANUC

- 新興企業

- Locus Robotics

- GreyOrange

- Symbotic

The Global Logistics Automation Market was valued at USD 35.9 billion in 2025 and is estimated to grow at a CAGR of 11.5% to reach USD 104.9 billion by 2035.

The market expansion is influenced by the strategic importance of logistics in national economies, as it significantly contributes to gross domestic product (GDP) across multiple countries. Governments and private stakeholders are increasingly investing in upgrading logistics infrastructure to improve productivity, efficiency, and global competitiveness. Logistics and transportation also form a core component of economic output in the United States, as highlighted by federal statistical authorities responsible for national economic data tracking. Modern logistics operations are rapidly shifting toward intelligent automation, where AI and machine learning technologies are evolving from isolated optimization tools into fully integrated orchestration systems. These platforms now manage end-to-end workflows by coordinating inventory, labor, and transportation in real time. Warehouse management and execution systems dynamically assign tasks across autonomous mobile robots, manual workers, and automated stations based on operational demand and system load. Transportation management systems are increasingly using live data inputs such as traffic conditions and carrier availability to optimize routing decisions. Research findings also indicate that higher levels of automation and robotics density significantly improve operational efficiency when supported by effective system integration and workforce adaptation.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $35.9 Billion |

| Forecast Value | $104.9 Billion |

| CAGR | 11.5% |

The hardware segment accounted for 58.3% share in 2025, generating USD 21 billion attributed to the capital-intensive nature of physical automation infrastructure, including conveyors, automated storage and retrieval systems, palletizing units, autonomous mobile robots, automated guided vehicles, and robotic lift equipment. Hardware remains the foundational layer of logistics automation, requiring significant upfront investment before software integration. These systems are closely integrated with warehouse control and execution platforms, which increasingly incorporate artificial intelligence to enhance routing efficiency, workload distribution, and predictive maintenance capabilities.

The large enterprises segment held a 66.1% share in 2025, valued at USD 23.8 billion. This leadership position is driven by the high capital requirements associated with large-scale automation deployments, which are typically accessible to financially strong organizations. Major adopters include global retail chains, e-commerce leaders, and third-party logistics providers that operate across multiple facilities. These enterprises are better positioned to manage long investment cycles and implement advanced automation technologies across distributed warehouse networks, giving them a clear advantage over smaller market participants.

U.S. Logistics Automation Market reached USD 10.9 billion in 2025 and is projected to grow at a CAGR of 12.3% from 2026 to 2035. The country's highly developed logistics ecosystem continues to attract strong investments in automation technologies. Growth is supported by rapid expansion of e-commerce, increasing labor shortages in warehouse operations, and widespread adoption of robotics and AI-driven systems. Industry surveys indicate that a significant share of logistics decision-makers in the region expect growing reliance on artificial intelligence while also highlighting rising concerns around cybersecurity risks in automated supply chains.

Key companies operating in the Logistics Automation Industry include ABB, Honeywell, Daifuku, KION (Dematic), SSI SCHAEFER, KUKA, Korber, KNAPP, TGW Logistics, and Symbotic. Companies in the Logistics Automation Market are focusing on expanding their technology portfolios by integrating advanced artificial intelligence, machine learning, and robotics into end-to-end supply chain solutions. Many players are investing heavily in scalable automation systems that support flexible warehouse configurations and real-time decision-making capabilities. Strategic partnerships with e-commerce platforms, logistics service providers, and industrial operators are helping firms expand deployment opportunities across multiple sectors. Companies are also prioritizing software-hardware integration to improve system interoperability and operational efficiency. In addition, continuous investment in predictive analytics, digital twin technologies, and cloud-based warehouse management systems is strengthening performance optimization.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Application

- 2.2.4 Organization Size

- 2.2.5 End Use

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 E-Commerce Growth & Last-Mile Delivery Demands

- 3.2.1.2 Labor Shortage & Rising Operational Costs

- 3.2.1.3 Need for Real-Time Visibility & Supply Chain Resilience

- 3.2.1.4 Advancements in AI, IoT & Robotics Technologies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Initial Capital Investment & ROI Uncertainties

- 3.2.2.2 Integration Complexity with Legacy Systems

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging Markets Adoption in Asia Pacific & Latin America

- 3.2.3.2 SME Market Penetration Through Cloud-Based Solutions

- 3.2.3.3 Autonomous Vehicles & Drone Delivery Integration

- 3.2.1 Growth drivers

- 3.3 Technology and innovation landscape

- 3.3.1 Current technologies

- 3.3.1.1 Radio Frequency Identification (RFID)

- 3.3.1.2 Automated Storage and Retrieval Systems (AS/RS)

- 3.3.1.3 Robotic Process Automation (RPA)

- 3.3.2 Emerging technologies

- 3.3.2.1 Autonomous Mobile Robots (AMRs)

- 3.3.2.2 Artificial Intelligence (AI)-Driven Predictive Logistics Platforms

- 3.3.2.3 Drone-Based Delivery Systems

- 3.3.2.4 Digital Twins for Supply Chain Optimization

- 3.3.1 Current technologies

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.1.1 US - Federal Motor Carrier Safety Administration (FMCSA)

- 3.5.1.2 US - Occupational Safety and Health Administration (OSHA)

- 3.5.1.3 Canada - Transport Canada

- 3.5.2 Europe

- 3.5.2.1 EU - Directorate-General for Mobility and Transport (DG MOVE)

- 3.5.2.2 Germany - Federal Ministry for Digital and Transport (BMDV)

- 3.5.3 Asia Pacific

- 3.5.3.1 China - China Federation of Logistics & Purchasing (CFLP)

- 3.5.3.2 India - Directorate of Logistics (DoL)

- 3.5.4 Latin America

- 3.5.4.1 Brazil - National Land Transport Agency (ANTT)

- 3.5.4.2 Mexico - General Bureau of Standards

- 3.5.5 Middle East & Africa

- 3.5.5.1 UAE - National Association of Freight and Logistics (NAFL)

- 3.5.5.2 Saudi Arabia - The Ministry of Transport and Logistics Services

- 3.5.1 North America

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Patent landscape (Driven by Primary Research)

- 3.9 Investment & funding analysis

- 3.10 Cost breakdown analysis

- 3.10.1 Research & development costs

- 3.10.2 Manufacturing & hardware production costs

- 3.10.3 Software development & licensing costs

- 3.10.4 Deployment, installation & customer integration costs

- 3.11 Intermodal Logistics Integration

- 3.11.1 Multi-modal transportation automation

- 3.11.2 Port & terminal automation integration

- 3.11.3 Rail-road-air connectivity & data interoperability

- 3.11.4 Cross-border logistics automation challenges

- 3.12 Cybersecurity & Data Infrastructure

- 3.12.1 Cybersecurity risks in automated logistics networks

- 3.12.2 Cloud infrastructure and secure data integration

- 3.12.3 IoT security challenges in smart logistics operations

- 3.13 Impact of AI & Generative AI on the Market

- 3.13.1 AI-driven disruption of existing business models

- 3.13.2 GenAI use cases & adoption roadmap by segment

- 3.13.3 Risks, limitations & regulatory considerations

- 3.14 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.14.1 Base Case - key macro & industry variables driving CAGR

- 3.14.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.14.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates and Forecast, By Component, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Autonomous Robots

- 5.2.2 Automated Storage & Retrieval Systems (AS/RS)

- 5.2.3 Automated Sorting Systems

- 5.2.4 Conveyor Systems

- 5.2.5 De-palletizing/Palletizing Systems

- 5.2.6 Automatic Identification & Data Collection (AIDC)

- 5.3 Software

- 5.3.1 Warehouse Management System (WMS)

- 5.3.2 Transportation Management System (TMS)

- 5.4 Services

- 5.4.1 Consulting

- 5.4.2 Deployment & Integration

- 5.4.3 Support & Maintenance

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Warehouse & Storage Management

- 6.3 Transportation Management

Chapter 7 Market Estimates and Forecast, By Organization Size, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Large Enterprises

- 7.3 Small & Medium Enterprises (SMEs)

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Manufacturing

- 8.3 Retail & E-Commerce

- 8.4 Food & Beverage

- 8.5 Healthcare & Pharmaceuticals

- 8.6 Automotive

- 8.7 Post & Parcel

- 8.8 Oil & Gas

- 8.9 Others

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Netherlands

- 9.3.8 Norway

- 9.3.9 Sweden

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 South Korea

- 9.4.4 India

- 9.4.5 Australia

- 9.4.6 Indonesia

- 9.4.7 Singapore

- 9.4.8 Vietnam

- 9.4.9 Philippines

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Chile

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global players

- 10.1.1 Daifuku

- 10.1.2 KION Group

- 10.1.3 Honeywell

- 10.1.4 SSI SCHAEFER Group

- 10.1.5 Toyota Industries

- 10.1.6 Rockwell Automation

- 10.1.7 KNAPP

- 10.1.8 KUKA Global (Midea)

- 10.1.9 ABB

- 10.1.10 Beumer Group

- 10.1.11 Korber

- 10.1.12 TGW Logistics

- 10.2 Regional players

- 10.2.1 FORTNA

- 10.2.2 WITRON

- 10.2.3 Fives Group

- 10.2.4 SAVOYE

- 10.2.5 FANUC

- 10.3 Emerging players

- 10.3.1 Locus Robotics

- 10.3.2 GreyOrange

- 10.3.3 Symbotic

物流自動化市場:按組件、物流類型、技術、運作模式、部署類型、應用和最終用戶產業分類-2026-2032年全球市場預測

物流自動化市場:按組件、物流類型、技術、運作模式、部署類型、應用和最終用戶產業分類-2026-2032年全球市場預測 物流自動化市場規模、佔有率、趨勢和預測:按組件、功能、公司規模、行業和地區分類,2026-2034 年

物流自動化市場規模、佔有率、趨勢和預測:按組件、功能、公司規模、行業和地區分類,2026-2034 年 2026年全球容器化物流系統市場報告2026年全球數位雙胞胎物流控制塔顯示器市場報告

2026年全球容器化物流系統市場報告2026年全球數位雙胞胎物流控制塔顯示器市場報告 物流自動化市場分析與預測(至2035年):依類型、產品類型、服務、技術、元件、應用、流程、部署模式、最終使用者、解決方案分類2026年全球物流自動化市場報告

物流自動化市場分析與預測(至2035年):依類型、產品類型、服務、技術、元件、應用、流程、部署模式、最終使用者、解決方案分類2026年全球物流自動化市場報告 物流自動化市場-全球產業規模、佔有率、趨勢、機會及預測(按組件、功能、產業垂直領域、地區及競爭格局分類,2021-2031年)按車輛類型、自動駕駛等級、推進類型、應用程式和最終用戶分類的全球自動駕駛物流解決方案市場預測(2026-2032 年)

物流自動化市場-全球產業規模、佔有率、趨勢、機會及預測(按組件、功能、產業垂直領域、地區及競爭格局分類,2021-2031年)按車輛類型、自動駕駛等級、推進類型、應用程式和最終用戶分類的全球自動駕駛物流解決方案市場預測(2026-2032 年) 歐洲物流自動化市場:市場佔有率分析、產業趨勢、統計數據和成長預測(2026-2031 年)物流自動化:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

歐洲物流自動化市場:市場佔有率分析、產業趨勢、統計數據和成長預測(2026-2031 年)物流自動化:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)