|

市場調查報告書

商品編碼

2066611

東協儲能市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)ASEAN Energy Storage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

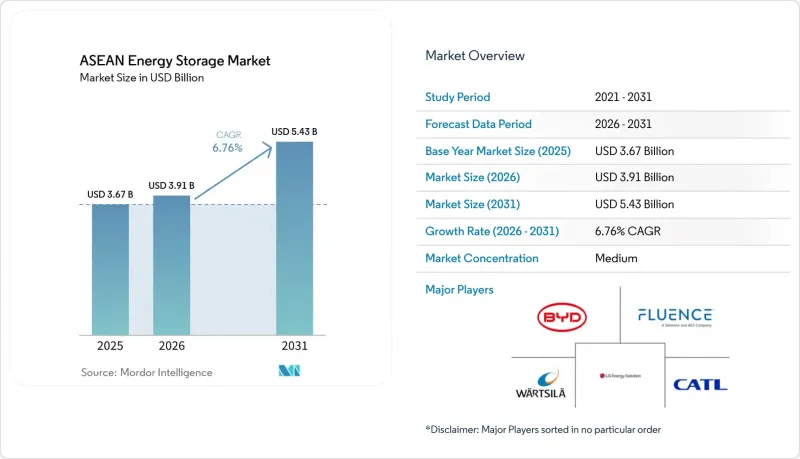

根據 Mordor Intelligence 預測,東協儲能市場規模將從 2025 年的 36.7 億美元和 2026 年的 39.1 億美元成長到 2031 年的 54.3 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 6.76%。

本報告按儲能技術(電池、抽水蓄能、熱能儲存等)、連接方式(併網、離網)、應用領域(電網級電力公司、住宅、商業和工業、資料中心、偏遠和孤立地區、其他)以及地區(印尼、越南、菲律賓、馬來西亞、泰國、新加坡和其他東南亞國協)進行細分。市場預測以美元計價。

東協儲能市場趨勢與洞察

東協的可再生能源目標將加速儲能技術的應用。

東協儲能市場正受到《2026-2030年亞太能源合作架構》(APAEC 2026-2030)中全部區域可再生能源目標提升的影響。該框架將2030年再生能源佔初級能源的比重和佔裝置容量的45%的目標分別提高到30%和45%。越南修訂後的第八個電力總體規劃體現了這一轉變,並在專案設計階段就強制要求集中式太陽能發電工程專案安裝至少相當於裝置容量10%的電池儲能系統(BESS),並提供兩小時的儲能時間。印尼的《2025-2034年再生能源總體規劃》(RUPTL 2025-2034)也賦予儲能規劃地位,將新增發電容量的15%分配給儲能設施,同時大規模發展可再生能源。這些變化意義重大,因為儲能正從一種可選的平衡工具轉變為與可再生能源競標和電網規劃直接相關的公共產業類別。國際能源總署(IEA)的東南亞一體化藍圖也表明,隨著2025年至2028年間太陽能和風能部署的加速,電網柔軟性將變得更加必要,這意味著儲能將繼續在區域電力政策中發揮核心作用。

工商業領域的電力需求正在創造用戶側儲能市場。

東協儲能市場正受到工業用戶的青睞,他們需要更穩定的電力供應,並更好地控制停電、限電和營運成本。儘管電網級系統仍佔據最大的市場佔有率,但資料中心和關鍵設施是成長最快的領域,預計到2031年將以10.3%的複合年成長率成長,這表明全部區域對可靠性的需求強勁且不斷成長。在越南,新的規劃法規以及將儲能正式納入電力框架,明確了儲能技術的應用路徑,使儲能設施更靠近工廠和工業園區。儘管批發靈活性市場仍處於起步階段,但製造商和數位營運商優先考慮業務永續營運和電力質量,因此該領域在東協儲能市場中至關重要。因此,即使在政策尚未跟上系統需求的國家,對商業和工業儲能的需求也變得更加永續。

資本密集度與專案融資之間的差距

高昂的前期成本仍然是東協儲能市場最明顯的限制因素之一,尤其對於長期儲能資產和大規模獨立電池儲能專案更是如此。越南的情況就充分說明了這一點,由於缺乏關於定價規則、輔助服務補償以及根據第62/2025/TT-BCT號通知對獨立儲能進行容量支付的最終規定,越南的多個電池儲能系統(BESS)項目一直停滯到2026年初。雖然大規模抽水蓄能發電工程正在推進,但許多計畫依賴優惠貸款和多邊融資,而非商業銀行的廣泛參與,例如北愛水力發電廠的資金籌措結構以及印尼政府支持的更大規模的計畫。這減緩了整個東協儲能市場已公佈目標轉化為實際簽約和運作容量的速度。此外,由於國內貸款機構仍然將許多儲能項目視為不熟悉的風險,小規模開發商處於不利地位。

細分市場分析

到2025年,抽水蓄能將佔東協儲能市場規模的80.9%,顯示該地區將繼續依賴長期存在的社會基礎設施進行大規模儲能。印尼、越南和泰國的一系列大型計畫進一步鞏固了這一地位,這些國家的國有電力公司將抽水蓄能定位為戰略平衡資產,而非小眾技術。越南1,200兆瓦的北愛抽水發電工程將於2026年全面開工建設,並將繼續在越南努力吸收可再生能源發電蓄能裝置容量,作為「2024年電力發展計畫」(PDP 2024)的一部分,這表明抽水蓄能的重要性將遠遠超出目前的預測期。

然而,在東協儲能市場,電池技術領域正經歷最顯著的多元化發展。氫能儲能是成長最快的技術領域,預計2026年至2031年將以11.1%的複合年成長率成長,這反映出人們對長期柔軟性和在獨立電網應用方面日益成長的興趣。鋰離子電池系統仍然是公用事業規模和住宅項目的首選,而磷酸鋰鐵電池(LFP)、鎳氫電池(NMC)和新興的鈉離子化學電池系統則構成了採購組合的重要組成部分。儘管全球電池成本的下降提高了在公用事業規模專案中部署電池儲能系統(BESS)的優勢,但在熱帶運行環境下,熱穩定性和安全性變得愈發重要。液流電池、熱力儲能系統和壓縮空氣儲能系統在該地區的部署仍處於早期階段,但它們可以滿足鋰離子電池系統無法有效滿足的儲存時間需求。安全認證也正日益成為採購決策的重要因素,這使得系統整合商在公共部門和公用事業競標中擁有更明顯的優勢。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 工商業領域電力需求成長

- 電網穩定性面臨的挑戰以及減少停電的必要性。

- 東協加快實現可再生能源佔比目標。

- 降低鋰離子電池的成本

- 利用數位雙胞胎進行儲存最佳化

- 獨立系統彈性及柴油動力替代計劃

- 市場限制因素

- 專案融資的資本密集度與限制因素

- 關於存儲資產類別的法規存在歧義

- 當地社區反對抽水蓄能水力發電廠

- 鎳錳供應鏈的波動性

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 透過儲存技術

- 電池(鋰離子電池、固體鋰離子電池、鈉離子電池、鉛酸電池、鈉硫電池和液流電池(釩液流電池、鋅溴液流電池))

- 抽水蓄能水力發電(PSH)

- 熱能儲存(顯熱(熔鹽、水)、潛熱(相變材料)、熱化學)

- 壓縮空氣儲能

- 液態空氣/低溫儲存

- 氫能儲存(電轉氫再電能)

- 其他技術(飛輪儲能、重力儲能、鐵空氣式儲能、鋅空氣式儲能)

- 連結性別

- 並網型

- 離網型

- 透過使用

- 電網級電力公司(位於電錶前)

- 住宅用途(電錶內)

- 商業和工業用途(計量後)

- 資料中心和關鍵設施

- 偏遠及離網/微電網地區

- 其他(交通運輸和鐵路電氣化、電動車充電基礎設施、電力傳輸和分配延遲)

- 按地區

- 印尼

- 越南

- 菲律賓

- 馬來西亞

- 泰國

- 新加坡

- 其他東南亞國協

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- BYD Co Ltd

- Contemporary Amperex Technology Ltd(CATL)

- LG Energy Solution

- Wartsila Oyj Abp

- GS Yuasa Corporation

- NGK Insulators Ltd

- Fluence Energy Inc

- Sungrow Power Supply Co Ltd

- Tesla Inc(Megapack)

- Siemens Energy AG

- Hitachi Energy Ltd

- Toshiba Corp

- Samsung SDI Co Ltd

- Kokam Co Ltd

- Pylon Technologies Co Ltd

- AlphaESS Co Ltd

- NEC ES(portfolio legacy)

- SEC Battery Company

- Mitsubishi Power

- EnerSys

第7章 市場機會與未來展望

According to Mordor Intelligence, the aSEAN energy storage market size is projected to expand from USD 3.67 billion in 2025 and USD 3.91 billion in 2026 to USD 5.43 billion by 2031, registering a CAGR of 6.76% between 2026 and 2031.

This report is Segmented by Storage Technology (Batteries, Pumped-Storage Hydroelectricity, Thermal Energy Storage, and More), Connectivity (On-Grid, Off-Grid), Application (Grid-Scale Utility, Residential, C&I, Data Centers, Remote/Off-Grid, Others), and Geography (Indonesia, Vietnam, Philippines, Malaysia, Thailand, Singapore, Rest of ASEAN). The Market Forecasts are Provided in Terms of Value (USD).

ASEAN Energy Storage Market Trends and Insights

ASEAN Renewable-Portfolio Targets Accelerating Storage Deployment

The ASEAN energy storage market is being shaped by a higher regional renewable ambition under APAEC 2026-2030, which raised the 2030 target to 30% of primary energy and 45% of installed power capacity. Vietnam's adjusted Power Master Plan VIII moved this shift into project design by requiring centralised solar projects to install BESS equal to at least 10% of installed capacity for 2-hour storage. Indonesia's RUPTL 2025-2034 also gave storage a planned role by assigning 15% of new capacity additions to storage assets alongside a wider renewable build-out. These changes matter because they shift storage from a discretionary balancing tool into a utility procurement category with direct links to renewable auctions and grid planning. The IEA's integration roadmap for Southeast Asia also shows that faster solar and wind additions will need more system flexibility between 2025 and 2028, which keeps storage near the center of regional power policy.

Electricity Demand from C&I Sector Creating Behind-the-Meter Storage Markets

The ASEAN energy storage market is also gaining support from industrial users that need more stable power and better control over outages, curtailment, and operating costs. Grid-scale systems still take the largest application share, but data centres and critical facilities are the fastest-growing application block at 10.3% CAGR through 2031, which shows how strongly reliability-led demand is rising across the region. In Vietnam, storage is moving closer to factories and industrial parks as new planning rules and the formal recognition of storage in the power framework create a clearer path for deployment. This part of the ASEAN energy storage market is important because manufacturers and digital operators value continuity and power quality even when wholesale flexibility markets remain immature. That makes commercial and industrial storage demand more durable in countries where policy is still catching up with system needs.

Capital-Intensity and the Project Finance Gap

High upfront costs remain one of the clearest brakes on the ASEAN energy storage market, especially for long-duration assets and large standalone battery projects. Vietnam shows this clearly because multiple BESS projects remained stalled into early 2026 while pricing rules for standalone storage, ancillary compensation, and capacity payments were still being finalised under Circular 62/2025/TT-BCT. Large pumped hydro projects are moving forward, but many depend on concessional or multilateral funding rather than broad commercial bank participation, as seen in Bac Ai's financing structure and Indonesia's wider state-backed pipeline. This slows the conversion of announced targets into contracted and commissioned capacity across the ASEAN energy storage market. It also leaves smaller developers at a disadvantage because domestic lenders still treat many storage structures as unfamiliar risk.

Other drivers and restraints analyzed in the detailed report include:

- Grid-Stability Issues and Outage Mitigation as an Immediate Procurement Signal

- Island-Grid Resiliency Creating a Parallel Off-Grid Storage Economy

- Ambiguous Storage Asset-Class Regulation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Pumped-Storage Hydroelectricity held 80.9% of the ASEAN energy storage market size in 2025, which shows how strongly the region still depends on long-established civil infrastructure for bulk storage. That position is reinforced by major project pipelines in Indonesia, Vietnam, and Thailand, where state utilities continue to treat pumped hydro as a strategic balancing asset rather than a niche technology. Vietnam's 1,200 MW Bac Ai pumped storage project entered its main construction phase in 2026 and remains central to the country's effort to absorb more renewable output from high-curtailment regions. Thailand also plans 2,472 MW of additional pumped hydro under PDP 2024 through the Chulabhorn, Vajiralongkorn, and Krathun projects, which confirms that PSH will stay important well beyond the current forecast period.

Battery technologies, however, are where most incremental diversification is taking place in the ASEAN energy storage market. Hydrogen-based storage is the fastest-growing technology segment at 11.1% CAGR from 2026 to 2031, which reflects growing interest in longer-duration flexibility and island-grid applications. Lithium-ion systems remain the main battery choice across utility and behind-the-meter projects, with LFP, NMC, and emerging sodium-ion chemistries shaping the procurement mix. Lower global battery costs are improving the case for utility-scale BESS, while thermal stability and safety are becoming more important in tropical operating conditions. Flow batteries, thermal systems, and compressed air are still early in the region, but they address storage durations that lithium-ion does not serve as efficiently. Safety certification is also becoming a stronger buying factor, which gives structured system integrators a clearer advantage in public and utility tenders.

List of Companies Covered in this Report:

- BYD Co Ltd

- Contemporary Amperex Technology Ltd (CATL)

- LG Energy Solution

- Wartsila Oyj Abp

- GS Yuasa Corporation

- NGK Insulators Ltd

- Fluence Energy Inc

- Sungrow Power Supply Co Ltd

- Tesla Inc (Megapack)

- Siemens Energy AG

- Hitachi Energy Ltd

- Toshiba Corp

- Samsung SDI Co Ltd

- Kokam Co Ltd

- Pylon Technologies Co Ltd

- AlphaESS Co Ltd

- NEC ES (portfolio legacy)

- SEC Battery Company

- Mitsubishi Power

- EnerSys

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth in electricity demand from C&I sector

- 4.2.2 Grid-stability issues & outage mitigation needs

- 4.2.3 ASEAN renewable-portfolio targets acceleration

- 4.2.4 Falling Li-ion battery costs

- 4.2.5 Digital twin-enabled optimisation of storage

- 4.2.6 Island-grid resiliency & diesel-offset programmes

- 4.3 Market Restraints

- 4.3.1 Capital-intensity & limited project finance

- 4.3.2 Ambiguous storage asset-class regulation

- 4.3.3 Community push-back on pumped hydro

- 4.3.4 Nickel-manganese supply-chain volatility

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Storage Technology

- 5.1.1 Batteries (Lithium-ion, Solid-State Li, Sodium-ion, Lead-acid, Sodium-Sulfur, and Flow Batteries (Vanadium, Zinc-Bromine))

- 5.1.2 Pumped-Storage Hydroelectricity (PSH)

- 5.1.3 Thermal Energy Storage (Sensible Heat (Molten Salt, Water), Latent Heat (Phase-Change Materials), Thermochemical)

- 5.1.4 Compressed Air Energy Storage

- 5.1.5 Liquid Air/Cryogenic Storage

- 5.1.6 Hydrogen-Based Storage (Power-to-H2-to-Power)

- 5.1.7 Other Technologies (Flywheel Energy Storage, Gravity-Based Storage, Iron-Air, Zinc-Air)

- 5.2 By Connectivity

- 5.2.1 On-Grid

- 5.2.2 Off-Grid

- 5.3 By Application

- 5.3.1 Grid-Scale Utility (Front-of-Meter)

- 5.3.2 Residential Behind-the-Meter

- 5.3.3 Commercial and Industrial Behind-the-Meter

- 5.3.4 Data Centers and Critical Facilities

- 5.3.5 Remote and Off-Grid/Microgrids

- 5.3.6 Others (Transportation and Rail Electrification, EV-Charging Infrastructure, Transmission and Distribution Deferral)

- 5.4 By Geography

- 5.4.1 Indonesia

- 5.4.2 Vietnam

- 5.4.3 Philippines

- 5.4.4 Malaysia

- 5.4.5 Thailand

- 5.4.6 Singapore

- 5.4.7 Rest of ASEAN

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, Recent Developments)

- 6.4.1 BYD Co Ltd

- 6.4.2 Contemporary Amperex Technology Ltd (CATL)

- 6.4.3 LG Energy Solution

- 6.4.4 Wartsila Oyj Abp

- 6.4.5 GS Yuasa Corporation

- 6.4.6 NGK Insulators Ltd

- 6.4.7 Fluence Energy Inc

- 6.4.8 Sungrow Power Supply Co Ltd

- 6.4.9 Tesla Inc (Megapack)

- 6.4.10 Siemens Energy AG

- 6.4.11 Hitachi Energy Ltd

- 6.4.12 Toshiba Corp

- 6.4.13 Samsung SDI Co Ltd

- 6.4.14 Kokam Co Ltd

- 6.4.15 Pylon Technologies Co Ltd

- 6.4.16 AlphaESS Co Ltd

- 6.4.17 NEC ES (portfolio legacy)

- 6.4.18 SEC Battery Company

- 6.4.19 Mitsubishi Power

- 6.4.20 EnerSys

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

2026年全球儲能市場報告

2026年全球儲能市場報告 冰儲能市場預測—全球儲能容量、技術、應用、最終用戶與區域分析—2034年熱量儲能市場預測—按儲能容量、技術、應用、最終用戶和地區分類的全球分析—2034年電錶後端儲能系統市場預測——按所有權/營運模式、發電容量範圍、技術、應用、最終用戶和地區分類的全球分析——2034年

冰儲能市場預測—全球儲能容量、技術、應用、最終用戶與區域分析—2034年熱量儲能市場預測—按儲能容量、技術、應用、最終用戶和地區分類的全球分析—2034年電錶後端儲能系統市場預測——按所有權/營運模式、發電容量範圍、技術、應用、最終用戶和地區分類的全球分析——2034年 商業和工業儲能:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

商業和工業儲能:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 高容量電池市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、最終用戶、地區和競爭格局分類,2021-2031年氨能源儲存系統市場預測至2034年-按儲能類型、技術、應用、最終用戶和地區分類的全球分析

高容量電池市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、最終用戶、地區和競爭格局分類,2021-2031年氨能源儲存系統市場預測至2034年-按儲能類型、技術、應用、最終用戶和地區分類的全球分析 儲能市場:依技術、時長、配置和最終用戶分類-2026-2032年全球市場預測可再生能源儲存市場預測至2034年-全球分析(按儲存技術、再生能源來源整合、系統類型、容量、所有權、連接方式、組件、應用、最終用戶和地區分類)

儲能市場:依技術、時長、配置和最終用戶分類-2026-2032年全球市場預測可再生能源儲存市場預測至2034年-全球分析(按儲存技術、再生能源來源整合、系統類型、容量、所有權、連接方式、組件、應用、最終用戶和地區分類) 2026-2030年全球人工智慧資料中心可再生能源儲存市場

2026-2030年全球人工智慧資料中心可再生能源儲存市場