|

市場調查報告書

商品編碼

2066604

數位體驗平台:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Digital Experience Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

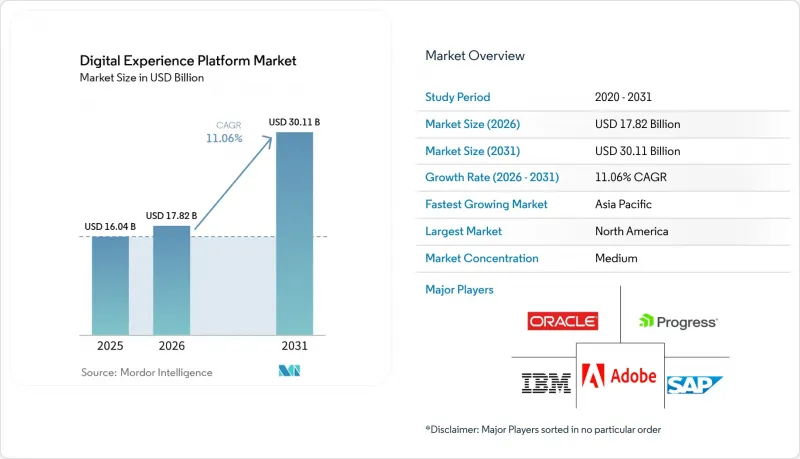

根據 Mordor Intelligence 預測,數位體驗平台市場預計將在 2026 年達到 178.2 億美元,並在 2031 年擴大到 301.1 億美元,在預測期內以 11.06% 的複合年成長率成長。

本報告按組件(平台和服務)、部署模式(本地部署和雲端部署)、最終用戶行業(零售和電子商務、IT和電信、銀行、金融服務和保險、醫療保健、製造業以及其他最終用戶行業)、組織規模(大型企業和中小企業)以及地區進行細分。市場預測以價值(美元)表示。

全球數位體驗平台市場趨勢與洞察

「雲端優先」的企業 IT 策略正在加速 DXP 的採用。

企業正擴大用軟體即服務 (SaaS) 模式取代本地部署許可證,這種模式將運算、儲存和內容傳送頻寬捆綁在一起,可在五年內將總體擁有成本 (TCO) 降低高達 40%。雲端平台還支援持續交付,使團隊能夠每天多次部署程式碼更新,而無需等待維護視窗。 Microsoft Azure 和 Amazon Web Services 提供一鍵式市場,將概念驗證(PoC) 週期從數月縮短至數週。多重雲端支援進一步降低了供應商鎖定風險,並滿足資料主權要求,加速了大型企業關鍵業務工作負載的遷移。

快速向全通路和人工智慧主導的個人化轉型。

目前,消費者在購買前平均會與商家接觸 6 到 8 個接點,這催生了對能夠整合身分、行為和即時情境資訊的平台的需求。 2025 年的營收成長主要由零售和電子商務產業推動,因為企業正在採用能夠在毫秒內呈現相關產品的建議引擎。 Adobe 整合了 Firefly 的生成模型,實現了 29 種語言的自動產品描述生成,從而加快了宣傳活動迭代速度並提高了轉換率。銀行、金融和保險 (BFSI) 機構正在利用開放銀行 API 來匯總餘額並提供個人化貸款提案,從而降低客戶獲取成本並縮短轉換週期。

與傳統技術棧相關的整合複雜性

大型企業通常經營 15 到 20 個行銷和商務應用程式,這些應用程式依賴專有 API 和批次進行整合。遷移到可組合的 DXP 需要進行資料模式對應、重複記錄核對以及確保交易一致性,這通常會導致專案耗時 18 個月,並消耗 40% 的預算。金融機構面臨更大的挑戰,因為如果沒有大量的現代化投資,它們就無法從其主機核心系統中公開 RESTful API。雖然現成的連接器可以滿足標準用例,但自訂工作流程和合規性要求仍然需要手動編寫中間件,這增加了對專業系統整合商的需求。

細分市場分析

預計到2025年,服務部門將佔總營收的31.27%,複合年成長率(CAGR)為12.34%,是該板塊中成長最快的部分。這一成長動能主要歸功於企業將數位體驗平台(DXP)市場預算的40%至50%用於系統整合、託管營運和策略諮詢。到2025年,該平台仍將透過定期訂閱、內容傳送和API呼叫收費貢獻68.73%的收入。然而,向可組合技術堆疊的轉變正在使第三方觸點翻倍,並增加了對具備跨平台專業知識的整合商的需求。全球顧問公司透過聘請無頭內容管理、客戶資料平台和行銷自動化方面的專家來拓展其DXP業務。培訓專案現在指導行銷團隊進行低程式碼開發、API管理和實驗方法論的培訓,使曾經僅限於技術部門的任務變得標準化。服務還包括持續最佳化生成式 AI 模組,以便客戶能夠根據品牌和監管要求微調提示和防護措施。

儘管授權收入仍然至關重要,但向基於使用量的收費模式的穩步轉變正重塑收入結構。供應商現在將精細化的實施支援、效能調優和持續的實驗整合到高級套餐中,從而培育高利潤的經常性收入來源。同時,託管服務透過提供全天候的網站可靠性和最佳化來解決人才短缺問題,使客戶能夠專注於內容和商業策略,而不是基礎設施維護。這些趨勢正在使服務成為在市場中獲得永續佔有率的主要手段。

預計到 2025 年,雲端業務將佔總收入的 57.83%,年成長率達 13.11%,遠超本地部署。彈性可擴展性、付費使用制和自動化安全性修補程式對尋求可預測成本和快速試驗的企業極具吸引力。即使是安全敏感型產業也在嘗試混合架構,將敏感資料保留在本地,同時將內容傳送和分析任務卸載到公共雲端,從而在合規性和敏捷性之間取得平衡。 Oracle 的多重雲端功能反映了對工作負載可攜性日益成長的需求,使企業能夠在滿足主權法規要求的同時,與不同的雲端服務供應商協商有利的條款。

持續整合 (CI) 管線借助容器編排管理和基礎架構即程式碼 (IaC) 技術,支援每天多次程式碼推送,從而實現即時庫存同步和 AI 驅動的個人化。然而,由於其依賴第三方服務的正常運作,因此容易受到服務等級協定 (SLA) 的影響。企業透過多區域容錯移轉、API 速率限制監控以及針對停機時間的合約處罰來降低這種風險。雖然隨著工具的成熟,混合模式有望逐步獲得市場佔有率,公共雲端仍將是市場成長的主要引擎。

區域分析

到2025年,北美將佔全球營收的38.73%,這主要得益於財富500強企業在管治。美國14個州的隱私法分散,要求制定區域性的同意和資料保存政策,這降低了小規模供應商的准入門檻,同時也為合規專業人士創造了諮詢收入機會。加拿大公司優先考慮法語和英語雙語內容傳送,而墨西哥零售商則投資於跨境電子商務框架,將庫存、課稅和物流連接起來,貫穿美墨加貿易走廊。

亞太地區預計將以12.74%的複合年成長率(CAGR)實現最高成長。印度的行動商務市場規模預計在2025年達到1,500億美元,這主要得益於2025年12月透過統一支付介面(UPI)完成的134億筆交易。印尼、越南和菲律賓的「智慧型手機優先」消費習慣正在推動對本地語言內容、本地付款閘道和低延遲交付的需求。在中國,行動支付的普及正在穩步推進,其核心是超級應用生態系統,這需要小程式API並遵守《個人資料保護法》。在日本和韓國,舊有系統正在遷移到雲端以支援全角字符集;而在新加坡、馬來西亞和泰國,跨境電商框架正被用於簡化海關手續和提升支付互通性。

歐洲佔據了相當大的市場佔有率,這得益於GDPR和資料法律對互通性和明確同意的強制要求,以及對開放原始碼、以API為中心的平台的青睞。德國、英國和法國繼續在汽車、奢侈品和金融等行業的全通路體驗方面投入大量資金。 「互通性歐洲法」強制公共實體採用標準化API,從而擴大了尋找合規供應商的機會。南歐國家正利用歐盟的復甦基金加速現代化進程,而北歐地區則正朝著完全無伺服器環境邁進。南美、中東和非洲仍然是新興市場,其中巴西透過對零售和金融科技的投資引領拉丁美洲,沙烏地阿拉伯和阿拉伯聯合大公國優先發展智慧城市,而南非儘管面臨基礎設施挑戰,但仍是撒哈拉以南非洲的技術中心。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 「雲端優先」的企業 IT 策略正在加速 DXP 的採用。

- 快速轉向全通路、人工智慧驅動的個人化

- 可組合/無頭 DXP 的普及

- 利用生成式人工智慧進行內容管理,可以縮短宣傳活動的上市時間。

- 亞洲新興市場行動商務的快速成長正在推動中階市場的需求。

- 歐盟資料法和美國開放資料舉措都要求互通性。

- 市場限制因素

- 與傳統技術棧整合的複雜性

- 資料隱私合規成本不斷上升

- MACH架構的專家人才短缺

- 由於採用了專有架構而導致的 Vault 遷移會增加遷移風險。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 對與市場相關的宏觀經濟趨勢進行評估

第5章 市場規模與成長預測

- 按組件

- 平台

- 服務

- 部署模式

- 現場

- 雲

- 按最終用戶行業分類

- 零售與電子商務

- 資訊科技/通訊

- 銀行、金融服務和保險(BFSI)

- 衛生保健

- 製造業

- 其他終端用戶產業

- 按組織規模

- 大公司

- 小型企業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- ASEAN

- 其他亞太國家

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Adobe Inc.

- Salesforce, Inc.

- Sitecore Holding II A/S

- SAP SE

- Oracle Corporation

- IBM Corporation

- Microsoft Corporation

- Progress Software Corporation

- OpenText Corporation

- Acquia Inc.

- Optimizely Inc.

- RWS Holdings plc

- Liferay, Inc.

- Kentico Software sro

- Bloomreach, Inc.

- Crownpeak Technology Inc.

- Magnolia International Ltd.

- Jahia Solutions Group SA

- Ibexa AS

- Squiz Pty Ltd

- Contentstack Inc.

- CoreMedia AG

- Contentful GmbH

- Pimcore GmbH

第7章 市場機會與未來展望

According to Mordor Intelligence, the digital experience platform market size reached USD 17.82 billion in 2026 and is projected to climb to USD 30.11 billion by 2031, advancing at an 11.06% CAGR during the forecast period.

This report is Segmented by Component (Platform and Services), Deployment Mode (On-Premises and Cloud), End-User Industry (Retail and E-Commerce, IT and Telecom, BFSI, Healthcare, Manufacturing, and Other End-User Industries), Organization Size (Large Enterprises and Small and Medium Enterprises), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Digital Experience Platform Market Trends and Insights

Cloud-First Enterprise IT Strategies Accelerate DXP Adoption

Organizations continue to replace on-premises licenses with software-as-a-service models that bundle compute, storage, and content-delivery bandwidth, trimming total cost of ownership by up to 40% over five years. Cloud platforms also enable continuous delivery, letting teams deploy code updates multiple times per day instead of waiting for maintenance windows. Microsoft Azure and Amazon Web Services offer one-click marketplaces that shorten proof-of-concept cycles from months to weeks. Multi-cloud support further reduces vendor-lock-in fears and satisfies sovereignty requirements, spurring large enterprises to migrate mission-critical workloads.

Rapid Shift to Omnichannel, AI-Driven Personalization

Consumers now engage across six to eight touchpoints before purchase, creating demand for platforms that unify identity, behavior, and real-time context. Retail and e-commerce dominated 2025 revenue because merchants deploy recommendation engines that surface relevant items within milliseconds. Adobe integrated Firefly generative models to automate product copy in 29 languages, accelerating campaign iterations and boosting conversion potential. BFSI institutions leverage open-banking APIs to deliver balance aggregation and personalized loan offers, trimming acquisition costs and shortening conversion cycles.

Integration Complexity with Legacy Stacks

Large enterprises run 15 to 20 marketing and commerce applications that rely on proprietary APIs and batch integrations. Re-platforming to composable DXPs requires mapping data schemas, reconciling duplicate records, and ensuring transaction consistency, often stretching projects to 18 months and absorbing 40% of budgets. Financial institutions face additional hurdles because mainframe cores cannot expose RESTful APIs without expensive modernization. Pre-built connectors cover standard use cases, but custom workflows and compliance rules still demand hand-coded middleware, fueling demand for specialized systems integrators.

Other drivers and restraints analyzed in the detailed report include:

- Gen-AI Content Operations Cut Time-to-Market for Campaigns

- Mobile-Commerce Boom in Emerging Asia Drives Mid-Market Demand

- Escalating Data-Privacy Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The services segment accounted for 31.27% of 2025 revenue and is on track for a 12.34% CAGR, the quickest growth among component groups. This trajectory stems from enterprises allocating 40-50% of Digital Experience Platform market budgets to systems integration, managed operations, and strategic consulting. Platforms still generated 68.73% of sales in 2025 through recurring subscriptions, content-delivery capacity, and API-call metering. Yet the pivot toward composable stacks multiplies third-party touchpoints, escalating demand for integrators with cross-platform credentials. Global consultancies broadened their DXP practices by onboarding specialists in headless content management, customer data platforms, and marketing automation. Training engagements now teach marketing teams low-code development, API management, and experimentation methods, democratizing tasks once reserved for technical departments. Services also encompass ongoing optimization for generative-AI modules, as clients fine-tune prompts and guardrails to comply with brand and regulatory requirements.

While license revenue remains essential, a steady shift toward usage-driven billing models is poised to reshape earnings portfolios. Vendors now bundle white-glove onboarding, performance tuning, and continuous experimentation as premium tiers, cultivating high-margin annuity streams. At the same time, managed-service offerings address talent shortages by providing 24/7 site reliability and optimization, enabling customers to focus on content and commerce strategy rather than infrastructure maintenance. This dynamic positions services as the primary lever for sustained wallet share in the market.

The cloud segment secured 57.83% revenue in 2025 and is expanding at 13.11% annually, well ahead of on-premises deployments. Elastic scalability, consumption-based pricing, and automated security patching appeal to organizations seeking predictable costs and rapid experimentation. Even security-sensitive industries now pilot hybrid frameworks that keep sensitive data on-premises while offloading content delivery and analytics to public clouds, balancing compliance with agility. Oracle's multi-cloud support illustrates growing demand for workload portability, letting enterprises negotiate favorable terms across providers while meeting sovereignty rules.

Continuous integration pipelines, enabled by container orchestration and infrastructure-as-code, enable multiple code pushes daily, supporting real-time inventory synchronization and AI personalizers. However, reliance on third-party uptime exposes the service to service-level breaches. Enterprises mitigate risks through multi-region failovers, API rate-limit monitoring, and contractual penalties for downtime. As tooling matures, hybrid models should capture incremental share, but public cloud is set to remain the growth engine for the market.

Geography Analysis

North America generated 38.73% of 2025 revenue, anchored by Fortune 500 spend on enterprise-grade governance, SOC 2 Type II and ISO 27001 certifications, and multi-tenant architectures. United States privacy legislation, fragmented across 14 states, compels geo-fenced consent and retention policies, lifting entry barriers for smaller vendors but opening advisory revenue for compliance specialists. Canadian enterprises prioritize bilingual French-English content delivery, while Mexican retailers invest in cross-border e-commerce frameworks linking inventory, taxation, and logistics across United States-Mexico-Canada trade corridors.

Asia Pacific is forecast to post the highest 12.74% CAGR. India's mobile-commerce sector hit USD 150 billion in 2025, fueled by the Unified Payments Interface's 13.4 billion December 2025 transactions. Smartphone-first behavior in Indonesia, Vietnam, and the Philippines drives demand for vernacular content, local payment gateways, and low-latency delivery. China centers adoption on super-app ecosystems that require mini-program APIs and Personal Information Protection Law compliance. Japan and South Korea migrate legacy systems to cloud to support double-byte character sets, while Singapore, Malaysia, and Thailand leverage cross-border e-commerce frameworks to simplify customs and payment interoperability.

Europe commands significant share, underpinned by GDPR and the Data Act, which mandate interoperability and explicit consent, favoring open-source, API-centric platforms. Germany, the United Kingdom, and France continue heavy investment in omnichannel experiences across automotive, luxury, and finance sectors. The Interoperable Europe Act obliges public agencies to adopt standardized APIs, expanding procurement opportunities for compliant vendors. Southern European nations accelerate modernization using European Union recovery funds, while the Nordic region advances fully serverless deployments. South America, the Middle East, and Africa remain emerging markets; Brazil leads Latin America through retail and fintech investments, Saudi Arabia and the United Arab Emirates prioritize smart-city initiatives, and South Africa acts as the sub-Saharan technology hub despite infrastructure challenges.

- Adobe Inc.

- Salesforce, Inc.

- Sitecore Holding II A/S

- SAP SE

- Oracle Corporation

- IBM Corporation

- Microsoft Corporation

- Progress Software Corporation

- OpenText Corporation

- Acquia Inc.

- Optimizely Inc.

- RWS Holdings plc

- Liferay, Inc.

- Kentico Software s.r.o.

- Bloomreach, Inc.

- Crownpeak Technology Inc.

- Magnolia International Ltd.

- Jahia Solutions Group SA

- Ibexa AS

- Squiz Pty Ltd

- Contentstack Inc.

- CoreMedia AG

- Contentful GmbH

- Pimcore GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-first enterprise IT strategies accelerate DXP adoption

- 4.2.2 Rapid shift to omnichannel, AI-driven personalisation

- 4.2.3 Democratization of composable / headless DXPs

- 4.2.4 Gen-AI content-operations cuts time-to-market for campaigns

- 4.2.5 Mobile-commerce boom in emerging Asia drives mid-market demand

- 4.2.6 EU Data Act and US Open Data initiatives mandate interoperability

- 4.3 Market Restraints

- 4.3.1 Integration complexity with legacy stacks

- 4.3.2 Escalating data-privacy compliance costs

- 4.3.3 Shortage of skilled MACH-architecture talent

- 4.3.4 Proprietary schema lock-in raises migration risk

- 4.4 Indusy Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of Macroeconomic Trends on Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Platform

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 On-Premises

- 5.2.2 Cloud

- 5.3 By End-User Industry

- 5.3.1 Retail and E-commerce

- 5.3.2 IT and Telecom

- 5.3.3 Banking, Financial Services and Insurance (BFSI)

- 5.3.4 Healthcare

- 5.3.5 Manufacturing

- 5.3.6 Other End-User Industries

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 ASEAN

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Adobe Inc.

- 6.4.2 Salesforce, Inc.

- 6.4.3 Sitecore Holding II A/S

- 6.4.4 SAP SE

- 6.4.5 Oracle Corporation

- 6.4.6 IBM Corporation

- 6.4.7 Microsoft Corporation

- 6.4.8 Progress Software Corporation

- 6.4.9 OpenText Corporation

- 6.4.10 Acquia Inc.

- 6.4.11 Optimizely Inc.

- 6.4.12 RWS Holdings plc

- 6.4.13 Liferay, Inc.

- 6.4.14 Kentico Software s.r.o.

- 6.4.15 Bloomreach, Inc.

- 6.4.16 Crownpeak Technology Inc.

- 6.4.17 Magnolia International Ltd.

- 6.4.18 Jahia Solutions Group SA

- 6.4.19 Ibexa AS

- 6.4.20 Squiz Pty Ltd

- 6.4.21 Contentstack Inc.

- 6.4.22 CoreMedia AG

- 6.4.23 Contentful GmbH

- 6.4.24 Pimcore GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

2026-2030年全球數位體驗監測市場

2026-2030年全球數位體驗監測市場 學習體驗平台市場預測至2034年-按組件、部署模式、組織規模、學習類型、功能、最終用戶和地區分類的全球分析

學習體驗平台市場預測至2034年-按組件、部署模式、組織規模、學習類型、功能、最終用戶和地區分類的全球分析 2026-2030年全球通訊業數位體驗監測市場

2026-2030年全球通訊業數位體驗監測市場 學習體驗平台(LXP):市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031 年)

學習體驗平台(LXP):市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031 年) 2026年全球數位網路工具市場報告數位社群體驗平台市場預測-全球分析(按組件、部署模式、組織規模、技術、應用、最終用戶和地區分類)——2034年數位銀行體驗平台市場預測至2034年-全球分析(按體驗功能、平台類型、技術、部署模式和最終用戶分類)

2026年全球數位網路工具市場報告數位社群體驗平台市場預測-全球分析(按組件、部署模式、組織規模、技術、應用、最終用戶和地區分類)——2034年數位銀行體驗平台市場預測至2034年-全球分析(按體驗功能、平台類型、技術、部署模式和最終用戶分類) Frost Radar™ - 數位體驗平台,2026 年

Frost Radar™ - 數位體驗平台,2026 年 數位體驗平台市場:按組件、部署模式、企業規模和產業分類-2026年至2032年全球市場預測全球數位體驗平台市場規模、佔有率、趨勢和成長分析報告(2026-2034)

數位體驗平台市場:按組件、部署模式、企業規模和產業分類-2026年至2032年全球市場預測全球數位體驗平台市場規模、佔有率、趨勢和成長分析報告(2026-2034)