|

市場調查報告書

商品編碼

2065530

學習體驗平台(LXP):市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031 年)Learning Experience Platform (LXP) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

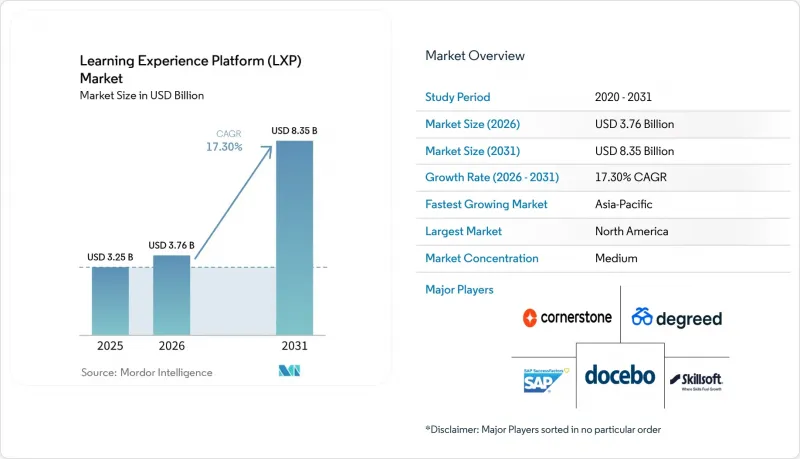

據 Mordor Intelligence 稱,學習體驗平台 (LXP) 市場預計將從 2025 年的 32.5 億美元成長到 2026 年的 37.6 億美元,到 2031 年達到 83.5 億美元,預計 2026 年至 2031 年的複合年成長率為 17.30%。

本報告按元件(平台[例如,學習內容聚合平台]、服務)、部署方式(雲端、本地部署、混合部署)、企業規模(大型企業、中小企業)、最終用戶產業(企業、教育機構、政府/非營利組織等)和地區進行細分。市場預測以價值(美元)表示。

全球學習體驗平台(LXP)市場趨勢與洞察。

快速轉向遠距和混合式人才培養。

隨著混合辦公模式的日益普及,學習體驗平台 (LXP) 市場持續受益。如今,企業需要同時培訓完全遠距辦公、混合辦公和現場辦公的員工。到 2025 年,美國大多數具備遠距辦公能力的員工將採用混合辦公模式,這表明柔軟性已成為一種結構性特徵,而非臨時措施。在此背景下,學習體驗平台的普及速度正在加快。非同步內容、行動存取、人工智慧驅動的學習路徑提案以及一致的使用者體驗,使企業能夠在不同的工作環境中提供同等的學習成果。這種轉變也帶來了對學習者自主性的更高期望,因為選擇自主工作方式的員工往往也希望在學習方式和時間上擁有類似的自主權。如果企業在靈活的平台架構上強加統一的學習順序,則在初期階段,員工的參與度往往會下降。因此,平台設計和內容策略同等重要。

對人工智慧驅動的個人化學習路徑的需求

學習體驗平台 (LXP) 市場的發展也受到從簡單的內容推薦轉向人工智慧驅動的技能差距彌合轉變的推動。 Docebo 在 2026 年人工智慧準備差距報告中指出,儘管採用和利用人工智慧的能力是企業學習領導者面臨的最大挑戰,但許多組織仍然使用無法適應不斷變化的角色的靜態學習模型。因此,個人化品質已成為關鍵的購買標準,因為職位或部門等弱訊號建構的平台往往會提供學習者會忽略的推薦。 TalentLMS 在 2026 年報告中指出,73% 的人力資源負責人將拓展數位技能視為首要任務。這凸顯了對能夠映射、推薦和檢驗特定能力而非提供通用目錄的系統的需求。因此,擁有豐富、獨特的技能圖譜的供應商在學習體驗平台市場中具有優勢,因為他們可以隨著學習者活動數據在其系統中的累積而不斷改進推薦。

實施和內容規劃成本高昂

高昂的初始實施成本仍然是學習體驗平台市場的一大障礙,尤其對於預算遠超過大型企業的組織而言更是如此。買家往往發現,訂閱費用僅佔其總支出的一小部分,因為實施、技能框架設計、內容授權和部署支援等費用並不包含在平台的基礎費用中。運作後,負擔依然存在,因為由多個來源組成的學習環境需要持續編輯,以移除過時的內容、維護學習路徑的質量,並更新學習庫以滿足不斷變化的角色需求。對於學習團隊人員有限、無法安排全職員工負責內容管理的中小型企業和組織而言,這種壓力更為顯著。儘管供應商正透過捆綁內容和人工智慧驅動的內容管理來緩解部分挑戰,但維護高品質、最新學習體驗的成本仍然是廣泛採用的主要障礙。

細分市場分析

到2025年,平台解決方案將佔總收入的61.26%,這表明在學習體驗平台(LXP)市場,企業負責人仍然更傾向於整合套件而非單一功能工具。在這一類別中,需求主要集中在人工智慧驅動的個人化學習模組、技能智慧層、內容聚合以及能夠將學習活動與員工績效關聯起來的分析工具。學習分析平台日益受到關注,因為高階主管負責人對功能的需求不再局限於完成情況儀表板,而是需要可審計的技能提升證據。內容聚合平台也依然重要,因為它們為企業進入學習體驗平台市場提供了一種切實可行的途徑,而無需企業完全取代現有的內容關係。

預計到2031年,服務業將以18.37%的複合年成長率成長,成為市場中成長最快的產業。這一趨勢反映出買家的優先事項正在轉變,從單純部署軟體轉向利用、管治和可衡量的部署。Adecco SA集團在2026年報告中指出,只有33%的公司積極投資於數據洞察,以了解員工的技能和能力,這顯示對部署支援和技能架構服務有著巨大的需求。實際上,這意味著技能框架、管理分析和學習營運方面的諮詢服務正在從一次性設置服務轉變為經常性收入來源。因此,在學習體驗平台(LXP)市場,那些能夠將產品功能與營運支援相結合,使平台易於企業領導者存取和使用的供應商備受青睞。

預計到2025年,基於雲端的採用將佔營收的76.24%,並在2031年之前維持21.49%的複合年成長率,繼續保持領先地位和成長速度。學習體驗平台(LXP)市場的這一細分領域正受益於持續交付,因為雲端原生系統能夠比本地環境更快地反映人工智慧模型更新、連接器發布和技能圖譜改進。這種速度至關重要,因為推理品質取決於最新的數據、頻繁的模型更新以及與其他企業系統的廣泛互通性。亞太和南美等新興市場也直接轉向雲端優先架構,進一步鞏固了雲端在學習體驗平台(LXP)市場的長期主導地位。

在某些環境中,由於主權法規或隔離網路的限制,員工學習記錄無法儲存在雲端,因此本地部署仍然佔據一定的地位。國防相關企業、機密政府機構和某些產業仍然傾向於這種模式,因為合規性要求超過了完全基於雲端的交付所帶來的柔軟性優勢。因此,混合部署正成為一種切實可行的折衷方案。特別是歐洲金融服務業,允許將敏感資料儲存在本地基礎設施上,而個人化和進階分析則由雲端模組處理。這種混合架構使得學習體驗平台 (LXP) 市場即使在高度監管的行業中也能擴展,而不會完全犧牲人工智慧功能或安全要求。

區域分析

到2025年,北美將佔全球銷售額的42.36%,佔據學習體驗平台(LXP)市場最大佔有率。美國憑藉其大型企業密集的基礎設施、成熟的人力資源資訊系統(HRIS)生態系統以及對以結果為導向的人才培養的強烈投資意願,仍然是該市場的主要驅動力。加拿大金融服務和政府機構的需求也十分強勁,雲端安全認證正日益成為供應商選擇的重要因素。在墨西哥,隨著跨國製造和技術服務公司投資擴充性的西班牙語培訓基礎設施以支援更複雜的跨境業務,該市場正在迅速崛起。雖然南美洲的市場應用仍處於起步階段,但巴西和阿根廷對行動優先、多語言雲端部署的學習體驗平台市場需求穩定成長。

在學習體驗平台市場,歐洲是一個高價值且合規性要求極高的地區。德國和英國仍然是最大的國內市場,其中德國的需求主要受製造業數位化以及與職業培訓和學徒計劃相關的技能提升需求的驅動。在法國,職業訓練市場已成長至超過320億歐元,以2025年歐元兌美元平均外匯1.10計算,約352億美元。 Qualiopi的要求也使得內容管治和稽核追蹤能力在供應商選擇中變得更加重要。 2026年3月,Unow發布報告稱,基於對500多位人力資源和培訓負責人的調查,學習形式的平衡正在趨於穩定。這表明,成長重心正從單純的遠距學習轉向最佳化混合式學習。雖然西班牙和義大利的中端市場商機正在擴大,但由於制裁相關的限制,俄羅斯的市場佔有率持續下降,導致區域焦點轉向德語區(德國、奧地利和瑞士)、法國和英國。在沙烏地阿拉伯和阿拉伯聯合大公國的主導,中東地區的國家級技能發展計畫正在迅速推進,而非洲仍處於起步階段,需求主要集中在南非的金融服務業和奈及利亞不斷成長的技能型勞動力。

預計到2031年,亞太地區將以18.11%的複合年成長率成長,成為LXP市場成長最快的區域板塊。印度尤為突出,其持續嚴重的技能短缺問題以及企業對應用人工智慧能力、安全行為和合規相關學習的持續高需求,使其在技能發展方面保持領先地位。 Workera在2026年報告中指出,只有13%的企業員工具備理解和利用人工智慧代理所需的關鍵技能,凸顯了當前技能水準的不足。中國的人工智慧應用路徑受到勞動政策和資料本地化法規的影響,這些政策有利於國內人工智慧學習供應商,並限制了國際平台的部署。日本、澳洲和紐西蘭仍然是成熟的中型市場,擁有較高的用戶購買力和對人才規劃的濃厚興趣,因此對技能智慧能力的需求持續旺盛。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 快速轉向遠距和混合式員工學習

- 對人工智慧驅動的個人化學習路徑的需求

- 與人力資源資訊系統生產力套件整合

- 技能發展以實現企業數位轉型目標

- 技能本體與人才市場的整合

- 支援 XAPI 的 LRS Analytics 展示了 ROI

- 市場限制因素

- 實施和內容規劃成本高昂

- 受監管領域的資料隱私和安全問題

- 專有的技能分類系統會導致供應商鎖定。

- 與舊版學習管理系統整合給我們的IT資源帶來了巨大壓力。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 平台

- 學習體驗平台

- 人工智慧驅動的個人化學習平台

- 技能智慧平台

- 學習內容聚合平台

- 學習分析與互動平台

- 服務

- 平台

- 透過部署方法

- 基於雲端的 LXP

- 本地部署 LXP

- 混合動力 LXP

- 按公司規模

- 大公司

- 小型企業

- 按最終用戶行業分類

- 公司

- 教育機構(K-12、高等教育)

- 政府和非營利組織

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲和紐西蘭

- 其他亞太國家

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Cornerstone OnDemand, Inc.

- Docebo Inc.

- SAP SuccessFactors(SAP SE)

- Skillsoft Corporation(SumTotal)

- Degreed, Inc.

- Valamis Group Oy

- Fuse Universal Ltd.

- Absorb Software Inc.

- Learn Amp Ltd.

- Schoox, Inc.

- D2L Corporation(formerly Desire2Learn)

- LinkedIn Corporation

- Udemy, Inc.

- 360Learning SA

- Thrive Learning Ltd.

- Learning Pool Ltd.

- Litmos

- Axonify Inc.

- Emerald Works Limited(Mind Tools)

- Mind Tools(Emerald Works)

第7章 市場機會與未來展望

According to Mordor Intelligence, the learning experience platform (LXP) market size is expected to increase from USD 3.25 billion in 2025 to USD 3.76 billion in 2026 and reach USD 8.35 billion by 2031, growing at a CAGR of 17.30% over 2026-2031.

This report is Segmented by Component (Platform [Learning Content Aggregation Platform, and More], and Services), Deployment Model (Cloud-Based, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry (Corporate, Academic, Government and Non-Profit, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Learning Experience Platform (LXP) Market Trends and Insights

Rapid Shift to Remote and Hybrid Workforce Learning

The learning experience platform (LXP) market continues to benefit from the normalization of hybrid work because organizations now train fully remote, hybrid, and on-site employees at the same time. In 2025, most remote-capable US workers were operating in hybrid arrangements, indicating that flexibility had become structural rather than temporary. In this environment, learning experience platform deployments are gaining traction because asynchronous content, mobile access, AI-curated pathways, and consistent user experience help organizations deliver the same learning outcome across different work settings. This shift also raises expectations around learner control, since employees who choose how they work increasingly expect similar control over how and when they learn. Companies that place rigid learning sequences on top of flexible platform architecture often see weaker engagement early in rollout, which makes platform design and content strategy equally important.

Need For AI-Driven Personalized Learning Paths

The learning experience platform (LXP) market is also being driven forward by the shift from simple content recommendations to AI-driven skill-gap closure. Docebo stated in its 2026 AI Readiness Gap Report that AI adoption and fluency had become the main pressure point for enterprise learning leaders, while many organizations were still using static learning models that could not keep pace with role change. That makes personalization quality a central buying criterion, because platforms built on weak signals, such as job title or department, often produce recommendations that learners ignore. TalentLMS reported in 2026 that 73% of HR managers saw expanded digital skills as their main priority, which supports demand for systems that can map, recommend, and validate specific capabilities rather than present generic catalogs. Vendors with greater proprietary skills graphs therefore hold an advantage in the learning experience platform market because they can keep improving recommendations as more learner activity enters the system.

High Implementation And Content-Curation Costs

High first-year activation costs remain a real barrier for the learning experience platform market, especially outside large-enterprise budgets. Buyers often find that subscription pricing is only one part of the total outlay because implementation, skills-framework design, content licensing, and rollout support sit outside the core platform fee. The burden continues after go-live because multi-source learning environments require ongoing editorial work to retire outdated content, maintain pathway quality, and keep libraries aligned with changing role needs. That pressure is felt more sharply by SMEs and by organizations with lean learning teams that cannot dedicate staff to full-time curation. Vendors are reducing some friction with bundled content and AI-assisted curation, but the economics of maintaining high-quality, current learning experiences still slow broader adoption.

Other drivers and restraints analyzed in the detailed report include:

- Upskilling For Enterprise Digital-Transformation Goals

- Integrations With HRIS and Productivity Suites

- Data-Privacy and Security Concerns in Regulated Sectors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Platform solutions held 61.26% of revenue in 2025, which shows that enterprise buyers still favor integrated suites over point tools in the learning experience platform (LXP) market. Within this category, demand has centered on AI-driven personalized learning modules, skills intelligence layers, content aggregation, and analytics tools that can connect learning activity to workforce performance. Learning analytics platforms have gained traction because executive buyers want more than completion dashboards and increasingly ask for auditable evidence of capability improvement. Content aggregation platforms also remain relevant because they give enterprises a practical route into the learning experience platform market without forcing a full replacement of existing content relationships.

Services are projected to grow at an 18.37% CAGR through 2031, which makes them the fastest-expanding component in the market. That pattern reflects a shift in buyer priorities from software deployment alone toward activation, governance, and measurable adoption. The Adecco Group reported in 2026 that only 33% of companies were actively investing in data insights to understand workforce skills capabilities, which points to a large need for implementation support and skills architecture services. In practice, this means consulting around skills frameworks, managed analytics, and learning operations has become a recurring revenue stream rather than a one-time setup function. As a result, the LXP market is rewarding vendors that can combine product capability with operational support that makes the platform usable and visible to business leaders.

Cloud-based deployment accounted for 76.24% of revenue in 2025 and remained both the leading and the fastest-growing model, with a 21.49% CAGR through 2031. This part of the learning experience platform market benefits from continuous delivery because cloud-native systems can push AI-model updates, connector releases, and skills-graph improvements faster than on-premises installations. That speed matters because inference quality depends on current data, frequent model refresh, and broad interoperability with other enterprise systems. Growth markets in Asia-Pacific and South America are also moving directly to cloud-first architectures, which strengthens the long-term lead of cloud in the learning experience platform (LXP) market.

On-premises deployment still holds a place in environments where sovereignty rules or isolated networks limit cloud storage of employee learning records. Defense contractors, classified government entities, and certain industrial operations continue to favor this model because compliance limits outweigh the flexibility benefits of full cloud delivery. Hybrid deployment is therefore emerging as a practical middle path, especially in European financial services where sensitive data can stay on local infrastructure while cloud modules handle personalization and advanced analytics. This blended architecture allows the LXP market to expand in tightly governed sectors without forcing a full compromise on AI capability or security requirements.

Geography Analysis

North America held 42.36% of revenue in 2025, which gave the region the largest share of the learning experience platform (LXP) market. The United States remains the main anchor because it combines a dense base of large enterprises, mature HRIS ecosystems, and high willingness to spend on trackable workforce development. Canada also shows strong demand in financial services and government, where cloud security certifications increasingly shape vendor selection. Mexico is emerging faster as multinational manufacturers and technology-services firms invest in scalable Spanish-language training infrastructure for more complex cross-border operations. South America remains earlier in adoption, but Brazil and Argentina are creating steady demand for mobile-first and multi-language cloud deployments within the learning experience platform market.

Europe represents a high-value but compliance-heavy part of the learning experience platform market. Germany and the United Kingdom remain the largest national markets, with German demand supported by manufacturing digitization and workforce reskilling needs tied to vocational and apprenticeship pathways. In France, the professional training market exceeded EUR 32 billion, which equals USD 35.2 billion at the 2025 average EUR/USD rate of 1.10, and Qualiopi requirements have made content governance and audit-trail capability more important in vendor screening. Unow reported in 2026 that a March survey of more than 500 HR and training professionals showed learning modality balance was stabilizing, which indicates a shift from remote-only growth toward deliberate blended optimization. Spain and Italy are building mid-market opportunity, while sanctions-related constraints continue to reduce Russia's role and shift regional weight toward the DACH cluster, France, and the United Kingdom. The Middle East, led by Saudi Arabia and the UAE, is advancing quickly on national upskilling agendas, while Africa remains earlier stage with demand centered on South Africa's financial services base and Nigeria's expanding technology workforce.

Asia-Pacific is projected to grow at an 18.11% CAGR through 2031, which makes it the fastest-growing regional block in the LXP market. India stands out because skill shortages remain acute and enterprise demand for applied AI capability, safety behavior, and compliance-linked learning continues to rise. Workera reported in 2026 that only 13% of enterprise employees possessed the critical skills needed to understand and work with AI agents, which shows how limited the current skills baseline remains. China's adoption path is shaped by workforce policy and data-localization rules, which favor domestic AI-learning providers and limit the reach of international platforms. Japan, Australia, and New Zealand remain mature mid-sized markets where high per-seat purchasing power and strong interest in workforce planning support ongoing demand for skills-intelligence features.

- Cornerstone OnDemand, Inc.

- Docebo Inc.

- SAP SuccessFactors (SAP SE)

- Skillsoft Corporation (SumTotal)

- Degreed, Inc.

- Valamis Group Oy

- Fuse Universal Ltd.

- Absorb Software Inc.

- Learn Amp Ltd.

- Schoox, Inc.

- D2L Corporation (formerly Desire2Learn)

- LinkedIn Corporation

- Udemy, Inc.

- 360Learning SA

- Thrive Learning Ltd.

- Learning Pool Ltd.

- Litmos

- Axonify Inc.

- Emerald Works Limited (Mind Tools)

- Mind Tools (Emerald Works)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Shift to Remote and Hybrid Workforce Learning

- 4.2.2 Need For Ai-driven Personalized Learning Paths

- 4.2.3 Integrations With HRIS and Productivity Suites

- 4.2.4 Upskilling For Enterprise Digital-Transformation Goals

- 4.2.5 Skills-ontology Linkage to Talent Marketplaces

- 4.2.6 Xapi-enabled LRS Analytics Proving ROI

- 4.3 Market Restraints

- 4.3.1 High Implementation and Content-Curation Costs

- 4.3.2 Data-Privacy/Security Concerns in Regulated Sectors

- 4.3.3 Proprietary Skills Taxonomies Create Vendor Lock-in

- 4.3.4 Legacy-LMS Integration Drains IT Bandwidth

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Platform

- 5.1.1.1 Learning Experience Platforms

- 5.1.1.2 AI-driven Personalized Learning Platforms

- 5.1.1.3 Skills Intelligence Platforms

- 5.1.1.4 Learning Content Aggregation Platforms

- 5.1.1.5 Learning Analytics and Engagement Platforms

- 5.1.2 Services

- 5.1.1 Platform

- 5.2 By Deployment Model

- 5.2.1 Cloud-Based LXP

- 5.2.2 On-Premises LXP

- 5.2.3 Hybrid LXP

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By End-user Industry

- 5.4.1 Corporate

- 5.4.2 Academic (K-12, Higher Ed)

- 5.4.3 Government and Non-profit

- 5.4.4 Other End-user Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of the Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Cornerstone OnDemand, Inc.

- 6.4.2 Docebo Inc.

- 6.4.3 SAP SuccessFactors (SAP SE)

- 6.4.4 Skillsoft Corporation (SumTotal)

- 6.4.5 Degreed, Inc.

- 6.4.6 Valamis Group Oy

- 6.4.7 Fuse Universal Ltd.

- 6.4.8 Absorb Software Inc.

- 6.4.9 Learn Amp Ltd.

- 6.4.10 Schoox, Inc.

- 6.4.11 D2L Corporation (formerly Desire2Learn)

- 6.4.12 LinkedIn Corporation

- 6.4.13 Udemy, Inc.

- 6.4.14 360Learning SA

- 6.4.15 Thrive Learning Ltd.

- 6.4.16 Learning Pool Ltd.

- 6.4.17 Litmos

- 6.4.18 Axonify Inc.

- 6.4.19 Emerald Works Limited (Mind Tools)

- 6.4.20 Mind Tools (Emerald Works)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2026-2030年全球數位體驗監測市場

2026-2030年全球數位體驗監測市場 學習體驗平台市場預測至2034年-按組件、部署模式、組織規模、學習類型、功能、最終用戶和地區分類的全球分析

學習體驗平台市場預測至2034年-按組件、部署模式、組織規模、學習類型、功能、最終用戶和地區分類的全球分析 2026-2030年全球通訊業數位體驗監測市場

2026-2030年全球通訊業數位體驗監測市場 數位體驗平台:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

數位體驗平台:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2026年全球數位網路工具市場報告數位社群體驗平台市場預測-全球分析(按組件、部署模式、組織規模、技術、應用、最終用戶和地區分類)——2034年數位銀行體驗平台市場預測至2034年-全球分析(按體驗功能、平台類型、技術、部署模式和最終用戶分類)

2026年全球數位網路工具市場報告數位社群體驗平台市場預測-全球分析(按組件、部署模式、組織規模、技術、應用、最終用戶和地區分類)——2034年數位銀行體驗平台市場預測至2034年-全球分析(按體驗功能、平台類型、技術、部署模式和最終用戶分類) Frost Radar™ - 數位體驗平台,2026 年

Frost Radar™ - 數位體驗平台,2026 年 數位體驗平台市場:按組件、部署模式、企業規模和產業分類-2026年至2032年全球市場預測全球數位體驗平台市場規模、佔有率、趨勢和成長分析報告(2026-2034)

數位體驗平台市場:按組件、部署模式、企業規模和產業分類-2026年至2032年全球市場預測全球數位體驗平台市場規模、佔有率、趨勢和成長分析報告(2026-2034)