|

市場調查報告書

商品編碼

2066599

亞太地區柴油發電機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Asia-Pacific Diesel Generator - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

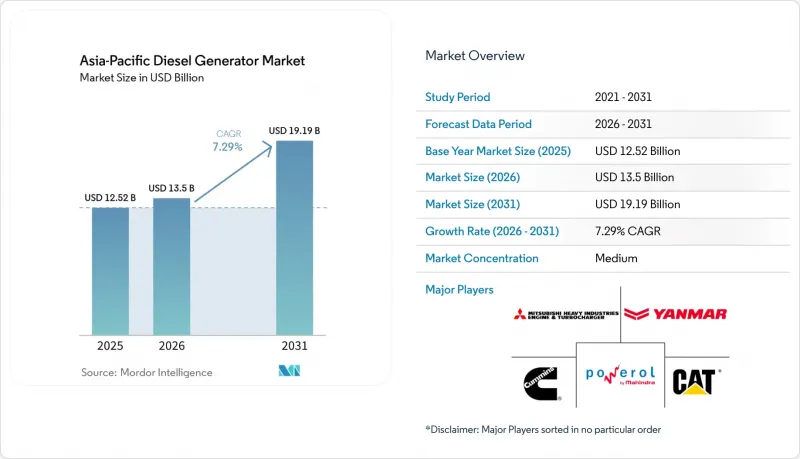

根據 Mordor Intelligence 預測,亞太柴油發電機市場規模將從 2025 年的 125.2 億美元和 2026 年的 135 億美元成長到 2031 年的 191.9 億美元,2026 年至 2031 年的複合年成長率為 7.29%。

本報告按容量(小於 75 kVA、75–350 kVA、375–750 kVA、750–2,000 kVA 和大於 2,000 kVA)、應用(備用/後備電源、主用/連續電源、尖峰用電調節/負載管理)、最終用戶(住宅、商業、工業分類)和其他地區(中國、東南亞國協)和日本地區。

亞太地區柴油發電機市場趨勢及洞察。

快速工業化與都市化

在印度,到2025年,將有300億美元的「生產連結獎勵計畫」應用於14個產業,這將進一步加劇泰米爾納德邦和北方邦的電力需求激增,這兩個邦夏季的電力短缺率已高達15%。同樣,越南北寧和海防的電子產業園區預計在2024年將吸引200億美元的外國直接投資(FDI),也面臨類似的電力緊張局面,但電網升級改造卻落後需求長達三年之久。因此,採購公司正在為額定輸出功率為750至2000千伏安的發電機組制定預算,將發電機組的成本從設施營運費用轉移到核心資本投資,並將更換週期延長至10年。隨著持續運作成為主要的採購要求,燃油效率和符合第四階段排放標準已成為董事會層面的關鍵績效指標(KPI)。

資料中心建設熱潮

到2025年,全部區域計畫新增19,371兆瓦的IT負荷,需要1.2至1.5倍的冗餘度。如果所有專案都能順利進行,這將相當於23,000至29,000兆瓦的柴油備用電源需求。光是阿達尼集團承諾在印度建設的5吉瓦人工智慧園區,預計到2035年就需要7,500兆瓦的發電機組。資料主權法規,例如印尼的國內託管法規,正在加速電力系統脆弱地區的在地化建設,並確保即使可再生能源日益普及,兆瓦級發電機組仍然至關重要。

加強有利於天然氣和可再生能源的排放法規

中國的「國六」排放標準和印度的「CPCB第四階段」排放標準將柴油發電機的資本投資成本提高了15%至20%,縮小了與燃氣渦輪機和太陽能+儲能混合系統的成本差距。在新加坡,碳排放稅計畫到2030年將最高提高到每噸80新元(2024年為每噸25新元),這將加速向低碳備用電源的轉型。

細分市場分析

到2025年,375-750千伏安(kVA)級柴油發電機將佔據亞太地區柴油發電機市場45.1%的佔有率。其面積小、價格實惠是通訊塔、中層辦公大樓和小規模工廠等應用的關鍵因素。然而,預計2000千伏安以上的機型將以8.7%的複合年成長率成長,成為亞太地區柴油發電機市場擴張最快的成長要素。超大規模資料中心業者中心正在透過並聯2-3兆瓦的機組建構20兆瓦的陣列,而印尼和澳洲的礦場正在部署多個兆瓦級獨立系統,用於離網運輸作業。

雖然太陽能和電池儲能正日益取代都市區住宅中75千伏安以下的電力系統,但對於偏遠地區的診所而言,電力系統仍然至關重要。 75-375千伏安的頻寬正受益於印度5G的部署。 2024年至2025年間,計畫新建20萬座宏塔,每座宏塔將配備30-50千伏安的備用電源。對於超過500千伏安的型號,ISO 8528認證是強制性的,因為買家現在要求產品具備瞬態負載處理能力和諧波控制能力。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 快速工業化與都市化

- 資料中心建設熱潮

- 電網可靠度缺陷和停電頻率

- 島上旅遊中心的混合微電網

- 因排放氣體法規(CPCB IV+)導致的車輛更換週期

- 透過數位雙胞胎技術進行預測性維護,降低整體擁有成本

- 市場限制因素

- 更嚴格的排放法規將促進天然氣和可再生能源的發展。

- 柴油價格波動劇烈

- 企業可再生能源購電協議可減少發電機運作時間。

- 四級技術工人短缺

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按容量(千伏安)

- 小於75千伏安

- 75~375 kVA

- 375~750 kVA

- 750~2,000 kVA

- 2000千伏安或以上

- 透過使用

- 備用電源

- 主電源/持續電源

- 尖峰用電調節/負載管理

- 最終用戶

- 住宅

- 商業的

- 產業

- 按地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 澳洲和紐西蘭

- 其他亞太國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和市場佔有率)

- 公司簡介

- Caterpillar Inc.

- Cummins Inc.

- Mitsubishi Heavy Industries Engine & Turbocharger Ltd.

- Yanmar Holdings Co. Ltd.

- Mahindra Powerol Ltd.

- Generac Power Systems

- Doosan Corporation

- Kohler Co.

- Kirloskar Oil Engines Ltd.

- Perkins Engines Company Ltd.

- Atlas Copco AB

- Himoinsa(SA de CV)

- Rolls-Royce Power Systems(MTU)

- Honda Motor Co. Ltd.

- Aksa Power Generation

- Weichai Power Co. Ltd.

- Aggreko plc

- Briggs & Stratton LLC

- Wartsila Corporation

- SG Generator Pvt Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the asia-Pacific diesel generator market size is projected to expand from USD 12.52 billion in 2025 and USD 13.5 billion in 2026 to USD 19.19 billion by 2031, registering a CAGR of 7.29% between 2026 to 2031.

This report is Segmented by Capacity (Below 75 KVA, 75 To 350 KVA, 375 To 750 KVA, 750 To 2, 000 KVA, and Above 2, 000 KVA), Application (Stand-by/Backup Power, Prime/Continuous Power, and Peak-shaving/Load Management), End-User (Residential, Commercial, and Industrial), and Geography (China, India, Japan, South Korea, ASEAN Countries, Australia and New Zealand, and Rest of Asia-Pacific).

Asia-Pacific Diesel Generator Market Trends and Insights

Rapid Industrialization & Urbanization

India's Production-Linked Incentive outlays of USD 30 billion across 14 sectors by 2025 deepened power-demand spikes in Tamil Nadu and Uttar Pradesh, where summer deficits touched 15%. Similar strains emerged in Vietnam's Bac Ninh and Hai Phong electronics belts after USD 20 billion of FDI arrived in 2024, yet transmission upgrades trail demand by up to three years. Buyers, therefore, budget for 750-2,000 kVA prime-rated sets, moving gensets from facilities overhead to core capex and extending replacement cycles to ten years. Fuel efficiency and Stage IV compliance have become board-level KPIs because continuous duty now dominates procurement briefs.

Data-Center Build-Out Boom

A 19,371 MW IT-load pipeline across Asia-Pacific in 2025 requires 1.2-1.5X redundancies, translating into 23,000-29,000 MW of diesel backup demand if all projects proceed. Adani's pledged 5 GW AI campus in India alone implies 7,500 MW in gensets by 2035. Data-sovereignty statutes, such as Indonesia's in-country hosting rule, accelerate localized build-outs in weak-grid markets, ensuring multi-megawatt gensets stay relevant even as renewable penetration rises.

Stricter Emission Regulations Favoring Gas & Renewables

China's National VI and India's CPCB Stage IV add 15-20% to diesel genset capex, eroding the cost gap versus gas turbines and solar-plus-storage hybrids. Singapore's carbon tax of SGD 25 per ton in 2024 rises to as high as SGD 80 by 2030, accelerating shifts to low-carbon backup.

Other drivers and restraints analyzed in the detailed report include:

- Grid-Reliability Gaps & Outage Frequency

- Hybrid Micro-Grids on Island Tourism Hubs

- Volatile Diesel Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 375-750 kVA class captured 45.1% of the Asia-Pacific diesel generator market share in 2025. Telecom towers, mid-rise offices, and light factories prize its footprint and price. However, above-2,000 kVA units are forecast to post an 8.7% CAGR, making them the fastest contributor to the Asia-Pacific diesel generator market size growth. Hyperscalers parallel 2-3 MW blocks to reach 20 MW arrays, while Indonesian and Australian mines deploy multi-MW islands for off-grid hauling operations.

Below-75 kVA sets face solar-plus-battery substitution in urban homes, yet remain essential in remote clinics. The 75-375 kVA band benefits from India's 5G rollout; 200,000 new macro towers in 2024-2025, each specified 30-50 kVA backup. ISO 8528 certification is now non-negotiable above 500 kVA as buyers demand transient load handling and harmonic control.

List of Companies Covered in this Report:

- Caterpillar Inc.

- Cummins Inc.

- Mitsubishi Heavy Industries Engine & Turbocharger Ltd.

- Yanmar Holdings Co. Ltd.

- Mahindra Powerol Ltd.

- Generac Power Systems

- Doosan Corporation

- Kohler Co.

- Kirloskar Oil Engines Ltd.

- Perkins Engines Company Ltd.

- Atlas Copco AB

- Himoinsa (SA de CV)

- Rolls-Royce Power Systems (MTU)

- Honda Motor Co. Ltd.

- Aksa Power Generation

- Weichai Power Co. Ltd.

- Aggreko plc

- Briggs & Stratton LLC

- Wartsila Corporation

- SG Generator Pvt Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid industrialisation & urbanisation

- 4.2.2 Data-centre build-out boom

- 4.2.3 Grid-reliability gaps & outage frequency

- 4.2.4 Hybrid micro-grids on island tourism hubs

- 4.2.5 Emission-norm driven replacement cycle (CPCB IV+)

- 4.2.6 Predictive-maintenance digital twins lowering TCO

- 4.3 Market Restraints

- 4.3.1 Stricter emission regulations favouring gas & RE

- 4.3.2 Volatile diesel prices

- 4.3.3 Corporate renewable PPAs cutting genset run-time

- 4.3.4 Shortage of Tier-4 skilled technicians

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Capacity (kVA)

- 5.1.1 Below 75 kVA

- 5.1.2 75 to 375 kVA

- 5.1.3 375 to 750 kVA

- 5.1.4 750 to 2,000 kVA

- 5.1.5 Above 2,000 kVA

- 5.2 By Application

- 5.2.1 Stand-by/Backup Power

- 5.2.2 Prime/Continuous Power

- 5.2.3 Peak-shaving/Load Management

- 5.3 By End User

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial

- 5.4 By Geography

- 5.4.1 China

- 5.4.2 India

- 5.4.3 Japan

- 5.4.4 South Korea

- 5.4.5 ASEAN Countries

- 5.4.6 Australia and New Zealand

- 5.4.7 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Caterpillar Inc.

- 6.4.2 Cummins Inc.

- 6.4.3 Mitsubishi Heavy Industries Engine & Turbocharger Ltd.

- 6.4.4 Yanmar Holdings Co. Ltd.

- 6.4.5 Mahindra Powerol Ltd.

- 6.4.6 Generac Power Systems

- 6.4.7 Doosan Corporation

- 6.4.8 Kohler Co.

- 6.4.9 Kirloskar Oil Engines Ltd.

- 6.4.10 Perkins Engines Company Ltd.

- 6.4.11 Atlas Copco AB

- 6.4.12 Himoinsa (SA de CV)

- 6.4.13 Rolls-Royce Power Systems (MTU)

- 6.4.14 Honda Motor Co. Ltd.

- 6.4.15 Aksa Power Generation

- 6.4.16 Weichai Power Co. Ltd.

- 6.4.17 Aggreko plc

- 6.4.18 Briggs & Stratton LLC

- 6.4.19 Wartsila Corporation

- 6.4.20 SG Generator Pvt Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

全球柴油發電機市場(至2031年):按設計(固定式和可攜式)、應用(備用、抑低尖峰負載、主用和連續用)、最終用戶(工業、商業和住宅)、額定功率和地區分類

全球柴油發電機市場(至2031年):按設計(固定式和可攜式)、應用(備用、抑低尖峰負載、主用和連續用)、最終用戶(工業、商業和住宅)、額定功率和地區分類 柴油發電機市場報告:按容量、應用、便攜性、最終用戶和地區分類(2026-2034 年)

柴油發電機市場報告:按容量、應用、便攜性、最終用戶和地區分類(2026-2034 年) 柴油發電機市場:2026-2032年全球市場預測(依額定千伏安、冷卻方式、安裝方式、應用及銷售管道)

柴油發電機市場:2026-2032年全球市場預測(依額定千伏安、冷卻方式、安裝方式、應用及銷售管道) 柴油發電機市場:按應用、功率輸出、最終用戶和地區分類

柴油發電機市場:按應用、功率輸出、最終用戶和地區分類 全球柴油發電機市場規模、佔有率、趨勢和成長分析報告(2026-2034年)柴油發電機市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並提供2026-2034年的洞察和預測液氣冷卻劑分配單元市場:依產品類型、技術、應用、終端用戶產業及通路分類,全球預測,2026-2032年

全球柴油發電機市場規模、佔有率、趨勢和成長分析報告(2026-2034年)柴油發電機市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並提供2026-2034年的洞察和預測液氣冷卻劑分配單元市場:依產品類型、技術、應用、終端用戶產業及通路分類,全球預測,2026-2032年 柴油發電機:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

柴油發電機:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2026年全球空氣冷發電機市場報告2026年全球柴油發電機市場報告

2026年全球空氣冷發電機市場報告2026年全球柴油發電機市場報告