|

市場調查報告書

商品編碼

1939099

柴油發電機:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Diesel Generator - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

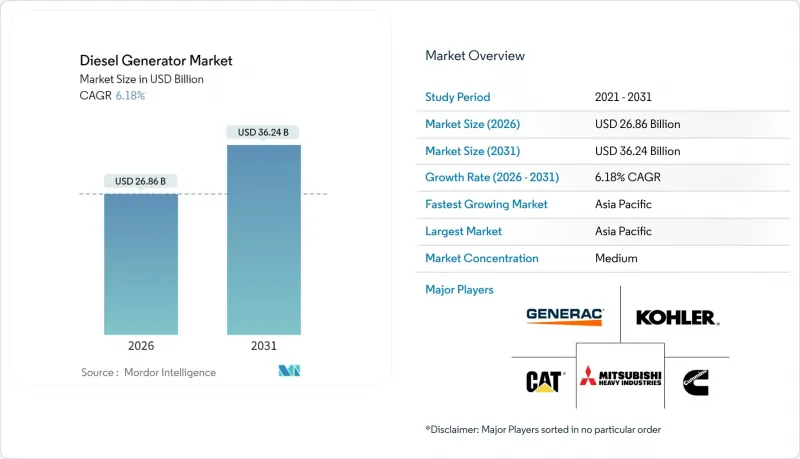

預計柴油發電機市場規模將從 2025 年的 253 億美元成長到 2026 年的 268.6 億美元,到 2031 年將達到 362.4 億美元,2026 年至 2031 年的複合年成長率為 6.18%。

即便可再生能源併網比例不斷提高,監管機構收緊排放限制,這項預測依然凸顯了市場的重要性。市場需求主要受三大結構性因素驅動:一是需要可靠的電力保障數位化營運;二是電力供應不足地區工業的快速擴張;三是採用先進的Tier 4 Final引擎,顯著降低顆粒物和氮氧化物的排放。同時,混合微電網將電池和太陽能與柴油發電結合,在不影響電力運轉率的前提下降低了燃料消耗。中型(75-375kVA)機組憑藉遠端監控、後處理裝置和並聯運轉開關設備等功能,正在擴大其目標用戶群體,而這些功能先前僅限於兆瓦級機組。

全球柴油發電機市場趨勢與洞察

關鍵基礎設施對不間斷電源的需求日益成長

醫院、金融交易所和半導體製造廠將停電視為與網路攻擊同等重要的業務永續營運風險。位於加州的沃爾什資料中心安裝了96兆瓦的柴油備用電源,以保護雲端工作負載。這項投資表明,營運商認知到發電機容量與收入保障之間的直接關聯。控制設備韌體中內建的預測分析功能可根據運作負載規劃維護,從而降低生命週期成本,並將發電機轉化為活躍資產。對許多數位公司而言,平均停機成本超過每小時10萬美元,因此採購部門越來越重視柴油發電機的可靠性,而非降低資本支出。這一趨勢支撐了符合Tier 4 Final排放標準的柴油發電機的溢價,這些發電機結合了遠距離診斷功能,並可減少99%的顆粒物排放,從而在日益嚴格的法規面前保持了柴油發電機行業的價值提案。

亞太地區和非洲的快速工業化和基礎設施發展

東南亞和非洲的工廠生產成長速度超過了電力公司加強電網建設的速度。工業園區通常會安裝10-20兆瓦的現場發電設備,這些設備可以與薄弱的電網同步運行,或在停電期間獨立運行。 Aggreko和康明斯提供的承包租賃設備能夠確保撒哈拉以南非洲地區新建礦山在永久電網線路建成之前持續運營,從而大大縮短了計劃工期。柴油發電機組的交付、試運行和負載測試只需幾個月即可交付,而電網擴建則需要數年時間。這種速度優勢形成了一個良性循環:工業成長推動了對發電能力的需求,從而促進了發電能力的進一步擴張,並使新興經濟體的柴油發電機產業保持穩定成長。

更嚴格的排放標準有利於燃氣和混合動力發電機。

加州空氣資源委員會正推動降低柴油顆粒物和氮氧化物(NOx)排放標準,使其低於Tier 4 Final標準,這促使一些車隊所有者考慮改用天然氣機組或混合微電網。歐洲第五階段排放法規要求功率超過19千瓦的引擎必須配備選擇性催化還原(SCR)和顆粒物過濾器(DPF),這增加了安裝成本並使維護計畫更加複雜。儘管面臨這些監管挑戰,引擎製造商正透過冷卻式廢氣再循環(EGR)燃燒技術、先進的燃油噴射系統以及可再生柴油相容技術來應對,以在不犧牲性能的前提下滿足法規要求。柴油的高能量密度在關鍵任務負載設施中仍然備受重視,這有助於柴油發電機行業在高階市場保持其地位。

細分市場分析

截至2025年,75kVA以下的柴油發電機組將佔柴油發電機市場43.25%的佔有率,反映出市場對中等負載(例如住宅、小規模商業和電信站點)的強勁需求,這些負載非常適合使用緊湊型發電機組。然而,375-750kVA功率段的市場成長速度將達到7.55%,到2031年將超過所有其他細分市場,因為工廠、資料處理中心和大型零售設施都在尋求兼顧成本和可靠性的解決方案。目前,中型發電機組已標配Tier 4-Final後後處理、混合動力控制系統和雲遙測技術,而這些功能以前僅限於兆瓦級機組。

Caterpillar的緊湊型設計在完全符合美國環保署 (EPA) 法規的前提下,減少了 31% 的安裝空間。這項設計創新降低了總安裝成本,加速了現有設施的採用。高階的 750-2,000kVA 和 2,000kVA+ 機組專為礦業和超大規模資料中心而設計,這些場所需要長時間運作並具備公用事業級電壓調節能力。入門級和高階機型之間性能差距的擴大,標誌著柴油發電機產業的成熟。應用需求(而不僅僅是價格)決定了採購標準,這為原始設備製造商 (OEM) 提供了將自身定位為高階發電機的機會。

本柴油發電機市場報告按容量(小於 75kVA、75-375kVA、375-750kVA、750-2,000kVA、大於 2,000kVA)、應用(緊急/備用電源、主電源/不間斷電源、抑低尖峰負載/負載管理)、最終用戶(住宅、商業、工業細分)和主要電源/歐洲地區工業、削峰/負載管理)。

區域分析

亞太地區在柴油發電機產業佔據最大佔有率,2025年市佔率達48.55%,預計到2031年將以7.12%的複合年成長率成長。強勁的工廠生產、新建的交通基礎設施以及雲端支出的激增,推動了市場需求遠超過區域電網升級改造。中國和印度佔據了大部分裝機量,製造商依靠現場發電機來保護生產免受電壓波動的影響。目前區域資料中心容量為12,206兆瓦,另有14,338兆瓦正在興建中。每兆瓦的IT負載大約需要1兆瓦的備用電源。新加坡暫停新建伺服器機房的政策,使得投資轉向柔佛州和雅加達大都會大都會圈,擴大了發電機銷售的地理覆蓋範圍。 5G的快速部署將需要新增數千座通訊塔,這需要緊湊可靠的發電機組。同時,澳洲和東南亞的遠端礦山管理正在指定使用大型柴油-太陽能混合動力裝置,以避免高成本的電網擴建。

北美是收入排名第二的地區,隨著公用事業公司加強電網建設以減少因天氣災害造成的停電,該地區正經歷穩定成長。預計到2027年,住宅出貨量將以5.82%的複合年成長率成長,因為住宅購買發電機是為了應對颶風、野火和冰暴造成的長時間停電。加州嚴格的排放法規有利於Tier 4 Final引擎和可再生柴油混合燃料,從而催生了一個高階細分市場,該市場對合規性的重視程度與價格不相上下。維吉尼亞、德克薩斯州和北加州不斷成長的需求也在推動柴油發電機產業的發展。這些地區聚集了大量超大規模資料中心,即使是像96兆瓦的沃爾什資料中心這樣的單一園區,也需要訂購數十台中速發電機來確保雲端服務的運作。在歐洲,碳減量目標促使買家選擇混合發電機組和符合第五階段排放標準的後處理系統,以減少粒狀物和氮氧化物(NOx)的排放。

中東和非洲地區正經歷接近兩位數的成長,這主要得益於各國政府對機場、鐵路走廊和礦場建設的投資,這些計畫旨在遠離不可靠的電網。開發商正擴大將柴油發電與太陽能電池板和儲能電池結合,以降低燃料成本並簡化沙漠和高海拔地區的物流。南美洲也呈現類似的趨勢,智利、秘魯和阿根廷的銅礦和鋰礦正在部署貨櫃式主用機組,因為電網建設進度落後於計劃進度。巴西和阿根廷的柴油發電機產業也在為食品加工和石化產業增加產能,從而將基本客群擴展到採礦業之外。國際能源總署(IEA)2025年報告對全球柴油供應的穩定展望支撐了全部區域的發電機供應和定價。這些因素共同造就了多元化的需求結構,有利於將柴油的可靠性與可再生能源投入相結合的整合解決方案。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 關鍵基礎設施對不斷電系統的需求不斷成長

- 亞太地區和非洲的快速工業化和基礎設施發展

- 異常天氣導致電網不穩定

- 在區域城市部署邊緣資料中心

- 5G通訊塔安裝量快速成長

- 在離網採礦部署柴油混合微電網

- 市場限制

- 更嚴格的排放氣體法規有利於燃氣混合動力發電機

- 電池供電型UPS越來越受歡迎

- 四級引擎稀土供應瓶頸

- 由於柴油廢氣風險,都市區的保險費上漲。

- 供應鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按容量(千伏安)

- 小於75千伏安

- 75~375 kVA

- 375~750 kVA

- 750~2000 kVA

- 2000千伏安或以上

- 透過使用

- 緊急電源/備用電源

- 主電源/持續電源

- 尖峰用電調節/負載管理

- 最終用戶

- 住宅

- 商業的

- 產業

- 區域分析

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 北歐國家

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 亞太其他地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 埃及

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略性舉措(併購、夥伴關係、購電協議)

- 市場佔有率分析(主要企業的市場排名和佔有率)

- 公司簡介

- Caterpillar Inc.

- Cummins Inc.

- Generac Holdings Inc.

- Kohler Co.

- Mitsubishi Heavy Industries Ltd.

- Rolls-Royce Holdings plc(MTU)

- Atlas Copco AB

- Doosan Corp.

- Kirloskar Oil Engines Ltd

- Aggreko plc

- FG Wilson(Caterpillar)

- Perkins Engines Co. Ltd

- MAN Energy Solutions

- Wartsila Oyj Abp

- Yanmar Holdings Co. Ltd

- MTU Onsite Energy

- SDMO Industries(KOHLER-SDMO)

- Weichai Power Co. Ltd

- Baudouin Engines

- Mahindra Powerol

第7章 市場機會與未來展望

The Diesel Generator market is expected to grow from USD 25.30 billion in 2025 to USD 26.86 billion in 2026 and is forecast to reach USD 36.24 billion by 2031 at 6.18% CAGR over 2026-2031.

The forecast underscores the market's continued relevance even as grids add more renewables and regulators tighten emission limits. Demand pivots on three structural forces: the need for resilient power to protect digitalized operations, the rapid industrial build-out in regions where grids cannot keep pace, and the availability of advanced Tier 4 Final engines that sharply cut particulate matter and nitrogen oxides. At the same time, hybrid microgrids combine batteries and photovoltaics with diesel generation, enabling operators to limit fuel consumption without compromising availability. Mid-range 75-375 kVA sets now incorporate remote monitoring, aftertreatment, and parallel-ready switchgear once reserved for megawatt-class units, widening the addressable user base.

Global Diesel Generator Market Trends and Insights

Rising Demand for Uninterrupted Power in Critical Infrastructure

Hospitals, financial exchanges, and semiconductor fabs now categorise power loss as a business-continuity risk on par with cyberattacks. The Walsh Data Center in California installed 96 MW of diesel backup to protect cloud workloads, an investment illustrating how operators equate generator capacity with revenue protection. Predictive analytics embedded in controller firmware schedule maintenance around live loads, lowering lifecycle costs and turning generators into active facility assets. As average downtime costs exceed USD 100,000 per hour for many digital businesses, procurement teams increasingly prioritize proven diesel reliability over capital expenditure savings. This trend supports premium pricing for Tier 4 Final sets that combine remote diagnostics with 99% lower particulate emissions, preserving the diesel generator industry's value proposition even under stricter regulations.

Rapid Industrialisation and Infrastructure Build-out in APAC & Africa

Factory output in Southeast Asia and Africa rises faster than utilities can reinforce transmission. Industrial parks frequently integrate 10-20 MW of on-site generation that synchronises with weak grids or runs islanded during outages. Turnkey rental fleets supplied by Aggreko and Cummins keep green-field mines in Sub-Saharan Africa operational until permanent lines arrive, shortening project schedules by several years. Diesel generators are delivered, commissioned, and load-tested in months, compared with multi-year grid-extension timelines. This speed advantage fuels a virtuous cycle where industrial growth demands more generation capacity, enabling further expansion and keeping the diesel generator industry on a steady upward trajectory in emerging economies.

Stricter Emission Norms Favouring Gas & Hybrid Sets

California's Air Resources Board is pushing diesel particulate and NOx thresholds below Tier 4 Final, motivating some fleet owners to switch to natural-gas units or hybrid microgrids. The European Stage V rule set mandates the use of selective catalytic reduction and particulate filters on engines exceeding 19 kW, thereby increasing acquisition costs and complicating maintenance schedules. While these standards pose a headwind, engine manufacturers have responded with cooled-EGR combustion strategies, advanced fuel injection, and renewable diesel compatibility that meet compliance without eroding performance. Facilities with mission-critical loads continue to value diesel's energy density, thereby preserving the diesel generator industry's relevance in premium segments.

Other drivers and restraints analyzed in the detailed report include:

- Grid Instability Caused by Extreme Weather Events

- Edge Data-Centre Roll-outs in Tier-2 Cities

- Growing Penetration of Battery-Storage-Backed UPS

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The below-75 kVA class retained the largest 43.25% slice of the diesel generator industry share in 2025, reflecting strong uptake in residential, small commercial, and telecom sites where modest loads warrant compact sets. Yet the 375-750 kVA band is advancing at a 7.55% CAGR to 2031, outpacing every other bracket as factories, data-processing hubs, and large retail footprints migrate to solutions that balance cost and resiliency. Mid-range models now ship with Tier 4-Final aftertreatment, hybrid-ready controls, and cloud telemetry once reserved for multi-megawatt units.

Caterpillar's compact architecture reduces installation space by 31% while maintaining full EPA compliance, a design leap that lowers total installed costs and accelerates adoption in brownfield facilities. At the top end, 750-2,000 kVA and >2,000 kVA sets power mines and hyperscale data centers, which require extended runtime with utility-grade voltage regulation. The widening performance gap between entry-level and feature-rich models signals a maturing diesel generator industry, in which application demands, rather than price alone, dictate buying criteria and open premium positioning for OEMs.

The Diesel Generator Market Report is Segmented by Capacity (Below 75 KVA, 75 To 375 KVA, 375 To 750 KVA, 750 To 2, 000 KVA, and Above 2, 000 KVA), Application (Stand-by/Backup Power, Prime/Continuous Power, and Peak-shaving/Load Management), End User (Residential, Commercial, and Industrial), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa).

Geography Analysis

The Asia-Pacific region holds a leading 48.55% share of the diesel generator industry in 2025 and is projected to expand at a 7.12% CAGR through 2031. Strong factory output, new transport links, and a sharp rise in cloud spending keep demand well ahead of local grid upgrades. China and India account for the majority of installations, as manufacturers rely on on-site sets to protect production from voltage fluctuations. Regional data-center capacity now totals 12,206 MW, with another 14,338 MW under construction, each megawatt of IT load matched by roughly one megawatt of standby power. Singapore's moratorium on new server farms has redirected investment to Johor and Greater Jakarta, widening the geographic spread of generator sales. A rapid 5G rollout requires the addition of thousands of telecom towers, which necessitate small but reliable units. Meanwhile, remote mine sites in Australia and Southeast Asia specify larger hybrid diesel-solar packages to avoid costly grid extensions.

North America is the second-largest region by revenue and exhibits steady growth as utilities enhance their networks to mitigate weather-driven outages. Residential shipments rise 5.82% CAGR to 2027 because homeowners buy protection from longer blackouts caused by hurricanes, wildfires, and ice storms. California's strict emission rules favor Tier 4 Final engines and renewable diesel blends, creating premium sub-segments that value compliance as much as price. The diesel generator industry also benefits from rising demand in Virginia, Texas, and Northern California. They host clusters of hyperscale data centers, and a single campus, such as the 96 MW Walsh facility, can order dozens of medium-speed generators to guarantee uptime for cloud services. In Europe, carbon-reduction goals are prompting buyers to opt for hybrid sets and Stage V-compliant aftertreatment systems that reduce particulate matter and NOx emissions.

The Middle East and Africa are experiencing high single-digit growth as governments invest in building airports, rail corridors, and mines that are far from reliable grids. Developers often pair diesel with solar arrays and batteries to trim fuel costs and simplify logistics in desert or high-altitude terrain. South America mirrors this pattern: copper and lithium miners in Chile, Peru, and Argentina deploy containerized, prime-rated units because grid connections often lag behind project timelines. The diesel generator industry in Brazil and Argentina also adds capacity for food processing and petrochemicals, widening the customer base beyond extractive industries. A stable outlook for global diesel supply, outlined in the International Energy Agency's 2025 report, supports generator availability and pricing across emerging regions. Together, these factors create a diverse demand landscape where integrated solutions that combine diesel reliability with renewable inputs gain traction.

- Caterpillar Inc.

- Cummins Inc.

- Generac Holdings Inc.

- Kohler Co.

- Mitsubishi Heavy Industries Ltd.

- Rolls-Royce Holdings plc (MTU)

- Atlas Copco AB

- Doosan Corp.

- Kirloskar Oil Engines Ltd

- Aggreko plc

- FG Wilson (Caterpillar)

- Perkins Engines Co. Ltd

- MAN Energy Solutions

- Wartsila Oyj Abp

- Yanmar Holdings Co. Ltd

- MTU Onsite Energy

- SDMO Industries (KOHLER-SDMO)

- Weichai Power Co. Ltd

- Baudouin Engines

- Mahindra Powerol

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for uninterrupted power in critical infrastructure

- 4.2.2 Rapid industrialisation & infrastructure build-out in APAC & Africa

- 4.2.3 Grid instability caused by extreme weather events

- 4.2.4 Edge-data-centre roll-outs in Tier-2 cities

- 4.2.5 Surge in telecom tower deployments for 5G

- 4.2.6 Diesel-hybrid micro-grid adoption in off-grid mining

- 4.3 Market Restraints

- 4.3.1 Stricter emission norms favouring gas & hybrid sets

- 4.3.2 Growing penetration of battery-storage backed UPS

- 4.3.3 Rare-earth supply bottlenecks for Tier-4 engines

- 4.3.4 Higher urban insurance premiums for diesel exhaust risks

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Capacity (kVA)

- 5.1.1 Below 75 kVA

- 5.1.2 75 to 375 kVA

- 5.1.3 375 to 750 kVA

- 5.1.4 750 to 2000 kVA

- 5.1.5 Above 2000 kVA

- 5.2 By Application

- 5.2.1 Stand-by/Backup Power

- 5.2.2 Prime/Continuous Power

- 5.2.3 Peak-shaving/Load Management

- 5.3 By End User

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial

- 5.4 Geographic Analysis

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 NORDIC Countries

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 ASEAN Countries

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Egypt

- 5.4.5.5 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Caterpillar Inc.

- 6.4.2 Cummins Inc.

- 6.4.3 Generac Holdings Inc.

- 6.4.4 Kohler Co.

- 6.4.5 Mitsubishi Heavy Industries Ltd.

- 6.4.6 Rolls-Royce Holdings plc (MTU)

- 6.4.7 Atlas Copco AB

- 6.4.8 Doosan Corp.

- 6.4.9 Kirloskar Oil Engines Ltd

- 6.4.10 Aggreko plc

- 6.4.11 FG Wilson (Caterpillar)

- 6.4.12 Perkins Engines Co. Ltd

- 6.4.13 MAN Energy Solutions

- 6.4.14 Wartsila Oyj Abp

- 6.4.15 Yanmar Holdings Co. Ltd

- 6.4.16 MTU Onsite Energy

- 6.4.17 SDMO Industries (KOHLER-SDMO)

- 6.4.18 Weichai Power Co. Ltd

- 6.4.19 Baudouin Engines

- 6.4.20 Mahindra Powerol

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

亞太地區柴油發電機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

亞太地區柴油發電機:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 全球柴油發電機市場(至2031年):按設計(固定式和可攜式)、應用(備用、抑低尖峰負載、主用和連續用)、最終用戶(工業、商業和住宅)、額定功率和地區分類

全球柴油發電機市場(至2031年):按設計(固定式和可攜式)、應用(備用、抑低尖峰負載、主用和連續用)、最終用戶(工業、商業和住宅)、額定功率和地區分類 柴油發電機市場報告:按容量、應用、便攜性、最終用戶和地區分類(2026-2034 年)

柴油發電機市場報告:按容量、應用、便攜性、最終用戶和地區分類(2026-2034 年) 柴油發電機市場:2026-2032年全球市場預測(依額定千伏安、冷卻方式、安裝方式、應用及銷售管道)

柴油發電機市場:2026-2032年全球市場預測(依額定千伏安、冷卻方式、安裝方式、應用及銷售管道) 柴油發電機市場:按應用、功率輸出、最終用戶和地區分類

柴油發電機市場:按應用、功率輸出、最終用戶和地區分類 全球柴油發電機市場規模、佔有率、趨勢和成長分析報告(2026-2034年)柴油發電機市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並提供2026-2034年的洞察和預測液氣冷卻劑分配單元市場:依產品類型、技術、應用、終端用戶產業及通路分類,全球預測,2026-2032年

全球柴油發電機市場規模、佔有率、趨勢和成長分析報告(2026-2034年)柴油發電機市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並提供2026-2034年的洞察和預測液氣冷卻劑分配單元市場:依產品類型、技術、應用、終端用戶產業及通路分類,全球預測,2026-2032年 2026年全球空氣冷發電機市場報告2026年全球柴油發電機市場報告

2026年全球空氣冷發電機市場報告2026年全球柴油發電機市場報告