|

市場調查報告書

商品編碼

2066597

印度電池能源儲存系統(BESS):市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)India Battery Energy Storage System (BESS) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

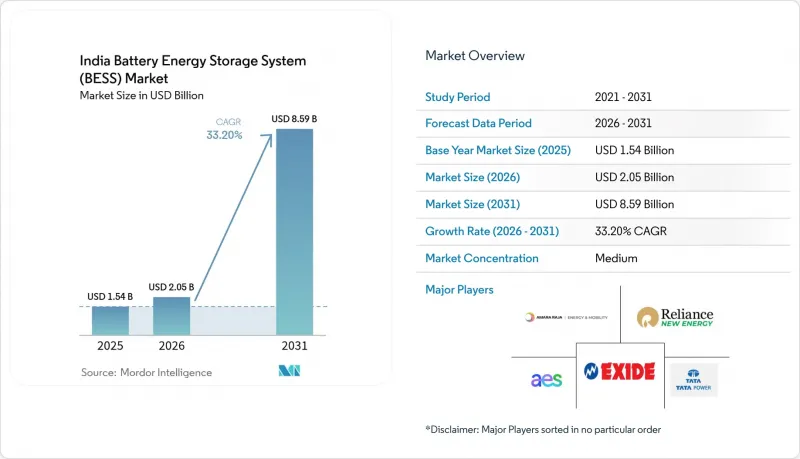

據 Mordor Intelligence 稱,2025 年印度電池能源儲存系統(BESS) 市場價值為 15.4 億美元,預計到 2031 年將從 2026 年的 20.5 億美元成長至 85.9 億美元,預測期(2026-2031 年)複合年成長率為 3.2%。

本報告按電池類型(鋰離子電池、鉛酸電池、液流電池、鈉離子電池等)、連接方式(併網和離網)、組件(電池組和支架、能源管理軟體等)、能量容量範圍(小於 10 MWh、10-100 MWh、500 MWh 及以上分類公司、商業和工業住宅)進行分類公司、商業和工業、住宅)進行。

印度電池能源儲存系統(BESS)市場趨勢與洞察

鋰離子電池成本更低

隨著中國超級工廠產能提升以及正極材料化學成分的改進,磷酸鋰鐵鋰電池的價格在2024年第二季降至每千瓦時89美元,比2023年水準下降14%。這項降幅使得100兆瓦級公共產業項目的資本支出從2022年的4000萬美元降至2024年的約3000萬美元,並且在高容量站點,平準化儲能成本已降至每千瓦時低於印度盧比。開發商已與寧德時代和比亞迪簽訂多年供應協議,涵蓋2024年68%的進口電芯,降低了短期項目受價格上漲的影響。磷酸鐵鋰電池6000次循環壽命與25年購電協議(PPA)相匹配,最大限度地降低了中期更換的風險。 2024 年初,碳酸鋰價格達到每噸 85,000 美元,之後跌至每噸 12,000 美元,但目前印度的大多數競標都包含與指數掛鉤的條款,以對沖原料價格的波動。

政府自願發展基金和生產關聯獎勵

印度電力部於2023年6月啟動了「可行性缺口資金」(VGF)計劃,為符合條件的獨立式建築儲能系統(BESS)提供最高達資本投資40%的臨時津貼,補貼上限為每兆瓦6.6印度盧比。截至2024年9月,該計畫已批准八個項目共1,200兆瓦時(4,800印度盧比)的津貼,刺激了5.8億美元的私人資本投資。同時,先進化學電池的生產關聯激勵計畫(PLI)提供五年內6%的銷售激勵,但需滿足50%的本地增值率和5吉瓦時的最低產能要求。信實集團、Ola Electric 和 Rajesh Exports 三家公司在 2024 年共獲得了 50 GWh 的電力供應,目標是在 2025 年下半年開始生產。這些措施預計將進口電池和國產電池之間的到岸成本差距從 2023 年的 22% 縮小到 2027 年的 8%。

關於資產類別和費用上限的監管模糊之處

各邦的成本回收規則不盡相同,有些邦將儲能系統(BESS)歸類為發電形式,而另一些邦則將其歸類為輸電形式。當儲能系統參與帶電輸電時,其收益取決於支出後12至18個月設定的監管費率,這阻礙了尋求穩定現金流的股權投資者。國家指導方針草案提案設立一個單獨的資產類別,並對其適用成本加成費率,但截至2024年底,最終規則仍未確定。如果加權平均資本成本超過11%,印度證券交易委員會(SECI)設定的電價上限(每度5.50至6.00印度盧比)將對收益構成壓力。貸款機構要求債務償付比率(DSCR)達到1.4倍或更高,這意味著盈虧平衡電價接近每千瓦時6.50印度盧比。在北方邦、比哈爾邦和西孟加拉邦,尚未推出任何關於儲能系統輸電和儲存費用的明確規定,不不確定性仍然存在。

細分市場分析

到2025年,鋰離子電池將佔總裝置容量的92.15%,其中磷酸鋰電池(LFP)佔75%。這主要歸功於其6000次循環壽命和固有的熱穩定性,後者在沙漠氣候中至關重要。由於開發商優先考慮生命週期成本而非能量密度,鎳鈷錳酸鋰電池(NMC)的市佔率已降至17%。鈦酸鋰電池作為滿足超快速響應需求的細分市場選擇,市佔率不足1%。鉛酸電池的市佔率已降至4.2%,因為其1,500次循環壽命已無法彌補成本優勢。液流電池和鈉離子電池合計佔2.6%的市場佔有率,但更低的成本有望實現更持久的儲能。

隨著價格下降,鋰離子電池有望鞏固其在印度電池能源儲存系統市場的主導地位,儘管像Reliance的50兆瓦時釩液流電池這樣的試點規模液流電池正在檢驗季節性儲能的經濟性。開發商更傾向於磷酸鐵鋰電池,因為被動式空氣冷卻可以將系統總成本降低12%至15%。此外,鋰離子電池的模組化設計縮短了建造時間,這對於滿足印度太陽能公司(SECI)嚴格的運作計劃至關重要。

隨著電信塔、礦場和島嶼電網中的柴油發電機被太陽能和儲能結合的混合系統所取代,離網和微電網的部署預計將以每年36.9%的速度成長。 Bharti Airtel在2500個地點的部署將在2024年節省1800萬公升柴油,並降低140印度盧比的營運成本(OPEX)。儘管如此,在SECI競標和輔助服務收入的推動下,到2025年,併網系統仍將佔發電容量的78.30%。由於虛擬電廠(VPP)軟體能夠將小規模系統整合到電網中,預計印度的電池儲能市場將逐步轉型為分散式資產。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 降低鋰離子電池的成本

- 政府對VGF和PLI的獎勵

- 500吉瓦可再生能源目標將導致儲能能力短缺。

- 電力分配公司(DISCOM)強制儲能

- 獨立儲能系統(BESS)競標激增,持續數小時。

- 來自工商業和資料中心的峰值價格套利需求

- 市場限制因素

- 關於資產類別和關稅上限的監管模糊之處

- 高度依賴進口的電池供應鏈正在推高資本投資。

- 競標不足和執行延誤

- 從地緣政治角度看關鍵礦產的供應風險

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

- 投資分析

- PESTLE分析

第5章 市場規模與成長預測

- 依電池類型

- 鋰離子(磷酸鋰鐵(LFP)、鎳錳鈷鋰(NMC)、鈦酸鋰(LTO))

- 鉛酸

- 液流電池(釩液流電池、鋅溴液流電池)

- 鈉離子

- 其他電池技術(鎳鎘電池、混合型超級電容)

- 透過連接方式

- 併網型(與電力公司連接)

- 離網(微電網、混合電網)

- 按組件

- 電池組和支架

- 電源轉換系統(PCS)

- 能源管理軟體(EMS)

- 工廠設施和服務

- 能量容量範圍

- 小於10兆瓦時

- 10~100 MWh

- 100~500 MWh

- 500兆瓦時或以上

- 透過最終用戶應用程式

- 公用事業

- 商業和工業用途

- 住宅

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- AES Corporation

- Tata Power Renewable Energy Ltd.

- Exide Energy Solutions Ltd.

- Amara Raja Energy & Mobility Ltd.

- Reliance New Energy Ltd.

- Adani Energy Solutions Ltd.

- JSW Energy Ltd.

- Fluence Energy Inc.

- Hitachi Energy India Ltd.

- Delta Electronics India Pvt Ltd.

- Panasonic Holdings Corp.

- LG Energy Solution Ltd.

- BYD Co. Ltd.

- CATL

- Toshiba Corporation

- Sterling & Wilson Energy Storage

- Siemens Energy India

- GE Vernova(Grid Solutions)

- Sungrow Power Supply Co.(India)

- NEC Energy(India JV)

第7章 市場機會與未來展望

According to Mordor Intelligence, the india battery energy storage system market size was valued at USD 1.54 billion in 2025 and estimated to grow from USD 2.05 billion in 2026 to reach USD 8.59 billion by 2031, at a CAGR of 33.2% during the forecast period (2026-2031).

This report is Segmented by Battery Type (Lithium-Ion, Lead-Acid, Flow Battery, Sodium-Ion, and More), Connection Type (On-Grid and Off-Grid), Component (Battery Pack and Racks, Energy Management Software, and More), Energy Capacity Range (Below 10 MWh, 10 To 100 MWh, Above 500 MWh, and More), and End-User Application (Utility, Commercial and Industrial, and Residential).

India Battery Energy Storage System (BESS) Market Trends and Insights

Declining Lithium-Ion Battery Costs

Lithium iron phosphate cell prices fell to USD 89 per kWh in Q2 2024, 14% below the 2023 level, after Chinese gigafactories ramped up their output and cathode chemistries improved. The drop cut the capex of a 100 MWh utility project from USD 40 million in 2022 to about USD 30 million in 2024, pushing levelized storage costs below INR 5 per kWh in high-utilization nodes. Developers have locked in multi-year supply contracts with CATL and BYD, covering 68% of imported cells in 2024, thereby insulating near-term projects from price spikes. LFP's 6,000-cycle life aligns with 25-year PPAs, minimizing mid-life replacement risk. Although lithium carbonate hit USD 85,000 per tonne in early 2024 before easing to USD 12,000, most Indian bids now include indexation clauses that hedge raw-material volatility.

Government VGF & PLI Incentives

The Ministry of Power's Viability Gap Funding, launched in June 2023, offers a one-time grant up to 40% of the eligible standalone BESS capex, capped at INR 6.6 crore per MW. By September 2024, the scheme had sanctioned 1,200 MWh across eight projects, valued at INR 4,800 crore, catalyzing USD 580 million of private equity investment. In parallel, the PLI program for advanced-chemistry cells provides a 6% sales incentive for five years, contingent on 50% local value addition and 5 GWh minimum capacity; Reliance, Ola Electric, and Rajesh Exports secured 50 GWh of awards in 2024 with first production targeted for late 2025. These levers shrink the landed-cost differential between imported and domestic cells from 22% in 2023 to a projected 8% by 2027.

Asset-Class & Tariff-Cap Regulatory Ambiguity

Cost-recovery rules vary by state, with some classifying BESS as a form of generation, while others classify it as a form of transmission. Where BESS is involved in tagged transmission, returns depend on regulated tariffs set 12-18 months after expenditure, which deters equity investors who seek stable cash flows. Draft national guidelines proposed a separate asset class with cost-plus tariffs, but the final rules were still pending as of late 2024. SECI tariff caps, between INR 5.50 and INR 6.00 per kWh, squeeze returns when the weighted average cost of capital exceeds 11%. Lenders request DSCR above 1.4x, implying breakeven tariffs closer to INR 6.50 per kWh. Uncertainty persists in Uttar Pradesh, Bihar, and West Bengal, where no BESS orders clarify wheeling or banking charges.

Other drivers and restraints analyzed in the detailed report include:

- 500 GW Renewables Target Creates Storage Gap

- Mandatory Energy Storage Obligation for DISCOMs

- Import-Heavy Battery Supply Chain Raises Capex

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lithium-ion batteries held 92.15% of the installed capacity in 2025, with LFP accounting for 75% due to their 6,000-cycle life and intrinsic thermal stability, which is critical for desert climates. NMC's share slipped to 17% as developers prioritized lifecycle cost over energy density. Lithium titanate remains a niche option under 1% for ultra-fast response markets, while lead-acid fell to 4.2% because its 1,500-cycle life no longer offsets capital expenditure savings. Flow and sodium-ion chemistries together make up 2.6% but offer long-duration potential once costs fall.

As prices drop, the Indian battery energy storage systems market expects lithium-ion to cement its lead, though pilot flow batteries, such as Reliance's 50 MWh vanadium unit, test seasonal storage economics. Developers favor LFP because passive air cooling reduces balance-of-system spend by 12-15%. Lithium-ion's modularity also speeds construction timelines, a key factor in meeting SECI's tight commissioning schedules.

Off-grid and microgrid installations are projected to grow at a 36.9% annual rate as telecom towers, mines, and island grids replace diesel generators with solar-plus-storage hybrids. Bharti Airtel's 2,500-site rollout saved 18 million liters of diesel in 2024 and reduced operating expenses (opex) by INR 140 crore. Nevertheless, on-grid systems still comprise 78.30% of the 2025 capacity, driven by SECI tenders and ancillary services revenues. The Indian battery energy storage systems market balance is expected to tilt gradually toward distributed assets as virtual power plant software enables the aggregation of smaller systems into grid services.

List of Companies Covered in this Report:

- AES Corporation

- Tata Power Renewable Energy Ltd.

- Exide Energy Solutions Ltd.

- Amara Raja Energy & Mobility Ltd.

- Reliance New Energy Ltd.

- Adani Energy Solutions Ltd.

- JSW Energy Ltd.

- Fluence Energy Inc.

- Hitachi Energy India Ltd.

- Delta Electronics India Pvt Ltd.

- Panasonic Holdings Corp.

- LG Energy Solution Ltd.

- BYD Co. Ltd.

- CATL

- Toshiba Corporation

- Sterling & Wilson Energy Storage

- Siemens Energy India

- GE Vernova (Grid Solutions)

- Sungrow Power Supply Co. (India)

- NEC Energy (India JV)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Declining lithium-ion battery costs

- 4.2.2 Government VGF & PLI incentives

- 4.2.3 500 GW renewables target creates storage gap

- 4.2.4 Mandatory Energy Storage Obligation for DISCOMs

- 4.2.5 Surge of multi-hour standalone BESS tenders

- 4.2.6 Peak-tariff arbitrage demand from C&I & data centers

- 4.3 Market Restraints

- 4.3.1 Asset-class & tariff-cap regulatory ambiguity

- 4.3.2 Import-heavy battery supply chain raises capex

- 4.3.3 Tender undersubscription & execution delays

- 4.3.4 Geopolitical critical-minerals supply risks

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products & Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

- 4.9 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Battery Type

- 5.1.1 Lithium-ion (Lithium Iron Phosphate (LFP), Nickel-Manganese-Cobalt (NMC), Lithium Titanate (LTO))

- 5.1.2 Lead-acid

- 5.1.3 Flow Battery (Vanadium Redox, Zinc-Bromine)

- 5.1.4 Sodium-ion

- 5.1.5 Other Battery Technologies (NiCd, Hybrid Super-capacitors)

- 5.2 By Connection Type

- 5.2.1 On-Grid (Utility Interconnected)

- 5.2.2 Off-Grid (Micro-Grid, Hybrid)

- 5.3 By Component

- 5.3.1 Battery Pack and Racks

- 5.3.2 Power Conversion System (PCS)

- 5.3.3 Energy Management Software (EMS)

- 5.3.4 Balance-of-Plant and Services

- 5.4 By Energy Capacity Range

- 5.4.1 Below 10 MWh

- 5.4.2 10 to 100 MWh

- 5.4.3 100 to 500 MWh

- 5.4.4 Above 500 MWh

- 5.5 By End-user Application

- 5.5.1 Utility

- 5.5.2 Commercial and Industrial

- 5.5.3 Residential

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 AES Corporation

- 6.4.2 Tata Power Renewable Energy Ltd.

- 6.4.3 Exide Energy Solutions Ltd.

- 6.4.4 Amara Raja Energy & Mobility Ltd.

- 6.4.5 Reliance New Energy Ltd.

- 6.4.6 Adani Energy Solutions Ltd.

- 6.4.7 JSW Energy Ltd.

- 6.4.8 Fluence Energy Inc.

- 6.4.9 Hitachi Energy India Ltd.

- 6.4.10 Delta Electronics India Pvt Ltd.

- 6.4.11 Panasonic Holdings Corp.

- 6.4.12 LG Energy Solution Ltd.

- 6.4.13 BYD Co. Ltd.

- 6.4.14 CATL

- 6.4.15 Toshiba Corporation

- 6.4.16 Sterling & Wilson Energy Storage

- 6.4.17 Siemens Energy India

- 6.4.18 GE Vernova (Grid Solutions)

- 6.4.19 Sungrow Power Supply Co. (India)

- 6.4.20 NEC Energy (India JV)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

電池能源儲存系統市場預測至2034年—按電池技術、輸出容量、應用、最終用戶和地區分類的全球分析

電池能源儲存系統市場預測至2034年—按電池技術、輸出容量、應用、最終用戶和地區分類的全球分析 電池能源儲存系統(BESS):市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

電池能源儲存系統(BESS):市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 電池能源儲存系統市場:按組件、電池類型、能量容量、連接方式、部署方式和應用分類-2026年至2032年全球市場預測

電池能源儲存系統市場:按組件、電池類型、能量容量、連接方式、部署方式和應用分類-2026年至2032年全球市場預測 2026年全球電錶前電池市場報告2026年全球電池租賃即服務市場報告

2026年全球電錶前電池市場報告2026年全球電池租賃即服務市場報告 全球電池能源儲存系統市場:按電池類型、應用、所有權/部署模式、連接方式、國家和地區分類-產業分析、市場規模、佔有率及預測(2025-2032年)

全球電池能源儲存系統市場:按電池類型、應用、所有權/部署模式、連接方式、國家和地區分類-產業分析、市場規模、佔有率及預測(2025-2032年) 全球電池能源儲存系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年)2026年全球電池能源儲存系統市場報告北美電池能源儲存系統(BESS)-市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

全球電池能源儲存系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年)2026年全球電池能源儲存系統市場報告北美電池能源儲存系統(BESS)-市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 電池儲能系統市場-全球產業規模、佔有率、趨勢、機會及預測(依電池類型、連接類型、能源容量、應用、區域及競爭格局分類,2021-2031年預測)

電池儲能系統市場-全球產業規模、佔有率、趨勢、機會及預測(依電池類型、連接類型、能源容量、應用、區域及競爭格局分類,2021-2031年預測)