|

市場調查報告書

商品編碼

2066573

核能:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Nuclear Power - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

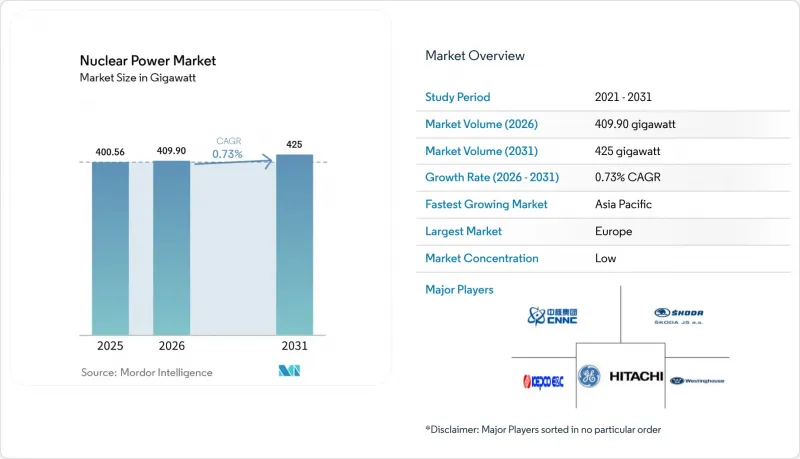

根據 Mordor Intelligence 預測,核能發電市場規模將從 2025 年的 400.56 吉瓦和 2026 年的 409.90 吉瓦成長到 2031 年的 425 吉瓦,2026 年至 2031 年的年複合成長率(CAGR)為 0.73%。

本報告按核子反應爐類型(壓水反應器、快滋生式反應爐等)、核子反應爐尺寸(大型、中型、小型)、燃料類型(低濃縮鈾等)、應用(併網發電、工業過程熱和蒸氣等)、最終用戶(電力公司和獨立發電商 (IPP)、工業和石化行業等)以及地區(歐洲、亞亞太地區等)進行分類。

全球核能發電市場趨勢與洞察

對清潔基本負載電力的需求不斷成長

隨著各國政府收緊碳排放預算,核能如今被視為唯一可快速擴展、足以彌補間歇性可再生能源缺口的可調節零排放能源。法國2024年能源法強制要求新建六座EPR2型核子反應爐;英國「大英核能計畫」的目標是到2050年實現24吉瓦的裝置容量;美國《通膨控制法》下的生產稅額扣抵正在提升非管制市場中核電項目的經濟可行性。這些措施共同恢復了過去十年因核電廠退役速度快於新建設速度而削弱的投資前景。英國的監管資產基礎模式等現代政策工具也透過降低先前導致專案取消的借貸成本,提振了投資者信心。因此,全球核能發電市場在各國脫碳藍圖中再次佔據重要地位,尤其是在可再生能源佔比高但儲能成本仍居高不下的地區。

延長營運週期和提高產量計劃

將現有核子反應爐的運作壽命從40年延長至60年,甚至80年,可以推遲耗資數十億美元的替代電廠的建設。美國美國核能管理委員會(NRC)在2024年至2025年間批准了11張許可證續約,將美國核子反應爐的平均剩餘運作壽命提高到28年。同樣,法國耗資494億歐元的Grand Carrenage維修項目,以遠低於新建設的成本,確保了未來數十年的電力供應。升級改造專案透過設備更換將發電量提高5%至20%,避免了與新建設相關的授權程序,從而使平準化發電成本低於每兆瓦時30美元,而大型新建核子反應爐的平準化發電成本則超過每兆瓦時70美元。然而,這種策略也集中了核子反應爐的風險,因此,卓越的營運管理和預測性維護至關重要,以避免意外停機,從而削弱成本優勢。

成本超支和資金籌措挑戰

高昂的資本成本和工期延誤持續削弱投資者信心。沃格特爾核電廠3號和4號機組投入運作耗資350億美元,是預算的兩倍多;法國弗拉芒維爾核電廠3號機組歷時17年,耗資191億歐元。這些成本超支導致信用評級下調,迫使各國政府為電力公司的資產負債表提供擔保。全球首創的技術風險、供應鏈中斷以及不斷變化的安全法規都在推高成本。除非大量建設能夠提高專案執行能力,否則在全球放鬆管制的核能發電市場中,核電將面臨市場佔有率被更便宜的可再生能源蠶食的風險,而在這個市場中,成本均等化仍然難以實現。

細分市場分析

憑藉標準化的供應鏈和數十年的運作數據,預計到2025年,壓水反應器將佔據全球核能發電市場佔有率的72.8%。快滋生式反應爐雖然規模較小,但在俄羅斯BN-800和中國CFR-600計畫成功驗證閉式燃料循環的推動下,預計將以21.4%的複合年成長率成長。加壓重水式反應爐設計對於印度和加拿大實現天然鈾自給自足仍具有重要的戰略意義。另一方面,由於福島維修後改造導致的長期停機和運作維護成本飆升,沸水沸水式反應爐的發展則相對落後。

快滋生式反應爐的發展動能預示著全球核能發電市場結構即將發生轉變。增殖反應器每公斤鈾可提取高達60倍的能量,在需求成長的同時緩解資源緊張。它們燃燒鈽庫存的能力也符合防止核擴散的目標。然而,複雜的鈉冷卻系統帶來了消防安全的挑戰,而高昂的建造成本也使得它們在沒有政府支持的情況下難以普及。因此,儘管輕水反應器預計在2031年之前仍能維持規模經濟優勢,但增殖反應器的崛起正在加劇競爭,並可能在2035年後徹底改變供應商格局。

到2025年,全球核能發電市場中,裝置容量在500至1000兆瓦之間的中型核電廠將佔據最大佔有率,從而在規模經濟和併網柔軟性之間取得平衡。然而,裝置容量低於500兆瓦的小規模核子反應爐預計將以20.1%的複合年成長率快速成長,這主要得益於工廠化生產模式顯著降低了現場施工和資金籌措風險。

對於金融基礎薄弱的新興經濟體而言,資本投入較低的模組化反應器更具吸引力;而工業用戶只需幾百兆瓦的電力即可滿足自身需求。 NuScale 的 77 兆瓦模組化反應器和 GE-Hitachi 的 300 兆瓦 BWRX-300 反應器是實現商業化過程的核心。如果政策能夠保障長期購電,那麼超過 1000 兆瓦的大型核子反應爐在每千瓦時的成本上仍具有優勢,但其長達 10 年的建設週期會使專案發起人面臨需求不確定性。因此,這種按規模分類的分類不僅凸顯了技術上的差異,更揭示了截然不同的經營模式:前者是分階段擴容以滿足分散式需求,後者則是為集中式電網提供大規模基本負載電力。

區域分析

到2025年,歐洲將維持其39.1%的發電能力,主要依靠法國的56座核子反應爐,這些反應器將供應法國65%的電力。英國、波蘭和捷克共和國的新建設將抵消德國和比利時除役,從而穩定該地區的運作能力直到2031年。法國將於2026年在彭裡啟動其首座EPR2反應器的土木工程,而英國的欣克利角C反應器計劃於2031年投入運行,取代老舊的AGR核子反應爐。

亞太地區是成長的主要驅動力,預計在2024年至2025年間以7.2%的複合年成長率成長。其中,中國將併網22座核子反應爐,印度將投入運作兩座國產700兆瓦重水反應器。日本分階段運作以及韓國的政策調整也推動了發電能力的成長。與西方自由化市場相比,該地區柔軟性的監管環境和政府主導的資金籌措體系能夠支持大規模的專案儲備。

北美地區的電力前景取決於小型多模組反應器(SMR)示範計畫。沃格特勒核電廠的兩座AP1000核子反應爐新增了2.2吉瓦的發電量,但未來的擴建將取決於成本分攤的示範項目,例如泰拉能源公司的Natrium反應器和安大略發電公司的BWRX-300反應器。中東和非洲地區尚處於部署初期。阿拉伯聯合大公國的巴拉卡核電廠提供5.6吉瓦的基本負載電力,沙烏地阿拉伯正在進行一項2.8吉瓦競標的供應商資格預審。南美洲的計畫儲備主要集中在巴西的Angra 3反應爐和阿根廷的CAREM-25反應堆,這表明該地區對小型多模組反應器計畫保持著謹慎但持續的興趣。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對清潔基本負載電力的需求不斷成長

- 延長使用壽命和提高產量計劃

- 先進小型模組化反應器的商業化

- 與工業脫碳相關的製程熱需求

- 與核能製氫和氨相關的項目

- 核能發電

- 市場限制因素

- 成本超支和資金籌措挑戰

- 來自低成本可再生能源的競爭

- 高純度鈾燃料供應瓶頸

- 出口管制和擴散核武器審查

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 核子反應爐類型

- 壓水核子反應爐(PWR)

- 加壓重水慢化冷卻核子反應爐(PHWR)

- 沸水核子反應爐(BWR)

- 氣冷石墨慢化核子反應爐(GCR)

- 高溫反應爐(HTGR)

- 輕水冷卻石墨慢化核子反應爐(LWGR)

- 快滋生式反應爐(FBR)

- 其他

- 核子反應爐尺寸

- 大型(1000兆瓦或以上)

- 中型(500-1000兆瓦)

- 小型(小於500兆瓦;包括小型模組化反應器和微型核子反應爐)

- 按燃料類型

- 低濃縮鈾(U-235含量低於5%)

- 高含量低濃縮鈾(LEU)(U-235 含量 5-20%)

- 混合氧化物(MOX)

- 釷基燃料

- 透過使用

- 併網電力

- 離網/遠端電源

- 工業製程熱和蒸氣

- 海水淡化和區域供熱

- 國防/軍事基地

- 按最終用戶行業分類

- 公共產業及獨立電力生產商(IPP)

- 工業和石油化工

- 偏遠地區的採礦和作業

- 政府/國防

- 研究機構

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 法國

- 瑞典

- 西班牙

- 烏克蘭

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 阿拉伯聯合大公國

- 南非

- 埃及

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略性措施(併購、合資、資金籌措、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- Electricite de France SA(EDF)

- Rosatom State Atomic Energy Corporation

- China National Nuclear Corporation(CNNC)

- Westinghouse Electric Company LLC

- GE-Hitachi Nuclear Energy

- Framatome SA

- Mitsubishi Heavy Industries Ltd

- Korea Hydro & Nuclear Power/KEPCO E&C

- BWX Technologies Inc.

- Bechtel Corporation

- Doosan Enerbility Co. Ltd

- Fluor Corporation(NuScale)

- SKODA JS as

- Holtec International

- TerraPower LLC

- Rolls-Royce SMR Ltd

- X-Energy LLC

- General Fusion Inc.

- Ontario Power Generation

- Babcock International Group

- Bilfinger SE

- Duke Energy Corporation

- Japan Atomic Power Company

- Ansaldo Nucleare

第7章 市場機會與未來展望

According to Mordor Intelligence, the nuclear power market size is projected to expand from 400.56 gigawatt in 2025 and 409.90 gigawatt in 2026 to 425 gigawatt by 2031, registering a CAGR of 0.73% between 2026 to 2031.

This report is Segmented by Reactor Type (Pressurized Light-Water Moderated and Cooled Reactor, Fast Breeder Reactor, and More), Reactor Size (Large, Medium, and Small), Fuel Type (Low-Enriched Uranium, and More), Application (Grid-Connected Power, Industrial Process Heat and Steam, and More), End-User (Utilities and IPPs, Industrial and Petro-Chemical, and More), and Geography (Europe, Asia-Pacific, and More).

Global Nuclear Power Market Trends and Insights

Increase in Demand for Clean Baseload Power

Governments tightening carbon budgets now view nuclear as the only dispatchable zero-emission source that can scale quickly enough to back up intermittent renewables. France's 2024 energy law mandates six new EPR2 units, the United Kingdom's Great British Nuclear program targets 24 GW by 2050, and U.S. production tax credits under the Inflation Reduction Act improve project economics in deregulated markets. These measures collectively restore an investment thesis that had eroded after a decade of retirements outpacing new builds. Investor sentiment is also improving because modern policy instruments, such as U.K. regulated asset-base models, lower borrowing costs that previously drove project cancellations. As a result, the Global nuclear power market is regaining relevance in national decarbonization roadmaps, particularly where storage costs for high-renewables scenarios remain prohibitive.

Lifetime Extension & Uprate Programs

Extending the operating life of existing reactors from 40 to 60 or even 80 years defers multi-billion-dollar replacement builds. The U.S. Nuclear Regulatory Commission approved 11 subsequent license renewals in 2024-2025, lifting the average remaining life of the domestic fleet to 28 years. France's EUR 49.4 billion Grand Carenage upgrades similarly add decades of output at a fraction of new-build cost. Uprate projects boost generation by 5-20% through equipment replacements that avoid greenfield permitting, achieving levelized costs below USD 30 per MWh versus more than USD 70 per MWh for new large reactors. This strategy, however, concentrates fleet-age risk, making operational excellence and predictive maintenance critical to avoid unplanned outages that erode cost advantages.

Cost Overruns & Financing Challenges

High capital costs and construction delays continue to erode investor confidence. Vogtle 3-4 entered service at USD 35 billion, more than double the budget, while France's Flamanville 3 consumed EUR 19.1 billion over 17 years. These overruns led to credit downgrades and forced governments to backstop utility balance sheets. First-of-a-kind engineering risk, supply-chain fragmentation, and evolving safety regulations all drive cost blowouts. Unless serial builds improve project delivery, the Global nuclear power market risks ceding ground to cheaper renewables in deregulated markets where levelized cost parity remains elusive.

Other drivers and restraints analyzed in the detailed report include:

- Commercialization of Advanced SMRs

- Industrial Decarbonization Process-Heat Demand

- HALEU Fuel-Supply Bottlenecks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Pressurized light-water reactors captured 72.8% of the Global nuclear power market share in 2025, underpinned by standardized supply chains and decades of operational data. Fast breeder reactors, although a minor base, are forecast to grow at 21.4% CAGR, driven by Russia's BN-800 and China's CFR-600 programs that validate closed fuel cycles. Pressurized heavy-water designs remain strategically important for India and Canada, offering natural-uranium autonomy. Boiling water reactors lag due to post-Fukushima retrofits that extend outages and inflate O&M costs.

Fast breeder momentum signals a structural pivot for the Global nuclear power market. Breeders extract up to 60 times more energy per kilogram of uranium, easing resource constraints as demand climbs. Their ability to burn plutonium stockpiles also aligns with non-proliferation objectives. However, complex sodium-cooling systems pose fire-safety challenges, and high capital costs deter adoption without sovereign backing. Consequently, light-water designs will preserve scale advantage through 2031, but breeders introduce competitive tension that could reshape vendor landscapes after 2035.

Medium-sized plants between 500 and 1,000 MWe represented the largest slice of the Global nuclear power market size in 2025, balancing economies of scale with grid integration flexibility. Yet small reactors below 500 MWe are projected to surge at 20.1% CAGR, propelled by factory fabrication that slashes onsite labor and financing risk.

Capital-light modules appeal to emerging economies with weaker balance sheets, while industrial buyers need only a few hundred megawatts for captive loads. NuScale's 77 MWe module and GE-Hitachi's 300 MWe BWRX-300 anchor the commercial pipeline. Large reactors above 1,000 MWe retain a cost-per-kilowatt edge where policy guarantees long-term offtake, but decade-long build times expose sponsors to demand uncertainty. The size segmentation, therefore, emphasizes contrasting business models rather than mere engineering: incremental capacity for distributed demand versus bulk baseload for centralized grids.

Geography Analysis

Europe retained 39.1% of capacity in 2025, anchored by France's 56-unit fleet that supplied 65% of national electricity. New builds in the United Kingdom, Poland, and the Czech Republic offset retirements in Germany and Belgium, stabilizing the region's capacity through 2031. France started civil works on its first EPR2 at Penly in 2026, while Hinkley Point C in the U.K. targets a 2031 start to replace aging AGR reactors.

Asia-Pacific is the growth engine, expanding at 7.2% CAGR as China connected 22 reactors in 2024-2025 and India commissioned two indigenous 700 MWe heavy-water units. Japan's phased restarts and South Korea's policy reversal also add incremental capacity. The region's regulatory agility and sovereign financing structures underpin bigger project pipelines than in liberalized Western markets.

North America's outlook hinges on SMR demonstrations. Vogtle's two AP1000 units added 2.2 GW, but future scale depends on cost-shared pilots such as TerraPower's Natrium and Ontario Power Generation's BWRX-300. The Middle East and Africa are early-cycle adopters: the UAE's Barakah delivers 5.6 GW of baseload power, and Saudi Arabia has pre-qualified vendors for a 2.8 GW tender. South America's pipeline centers on Brazil's Angra 3 and Argentina's CAREM-25, signaling a cautious but persistent regional interest.

- Electricite de France SA (EDF)

- Rosatom State Atomic Energy Corporation

- China National Nuclear Corporation (CNNC)

- Westinghouse Electric Company LLC

- GE-Hitachi Nuclear Energy

- Framatome SA

- Mitsubishi Heavy Industries Ltd

- Korea Hydro & Nuclear Power / KEPCO E&C

- BWX Technologies Inc.

- Bechtel Corporation

- Doosan Enerbility Co. Ltd

- Fluor Corporation (NuScale)

- SKODA JS a.s.

- Holtec International

- TerraPower LLC

- Rolls-Royce SMR Ltd

- X-Energy LLC

- General Fusion Inc.

- Ontario Power Generation

- Babcock International Group

- Bilfinger SE

- Duke Energy Corporation

- Japan Atomic Power Company

- Ansaldo Nucleare

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increase in demand for clean baseload power

- 4.2.2 Lifetime extension & uprate programs

- 4.2.3 Commercialization of advanced SMRs

- 4.2.4 Industrial decarbonization process-heat demand

- 4.2.5 Nuclear-produced hydrogen & ammonia initiatives

- 4.2.6 Emergence of nuclear-powered data-center & marine applications

- 4.3 Market Restraints

- 4.3.1 Cost overruns & financing challenges

- 4.3.2 Competition from low-cost renewables

- 4.3.3 HALEU fuel-supply bottlenecks

- 4.3.4 Export-control & proliferation scrutiny

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Reactor Type

- 5.1.1 Pressurized Light-Water Moderated and Cooled Reactor (PWR)

- 5.1.2 Pressurized Heavy-Water Moderated and Cooled Reactor (PHWR)

- 5.1.3 Boiling Light-Water Cooled and Moderated Reactor (BWR)

- 5.1.4 Gas Cooled, Graphite Moderated Reactor (GCR)

- 5.1.5 High-Temperature Gas-Cooled Reactor (HTGR)

- 5.1.6 Light-Water Cooled, Graphite Moderated Reactor (LWGR)

- 5.1.7 Fast Breeder Reactor (FBR)

- 5.1.8 Others

- 5.2 By Reactor Size

- 5.2.1 Large (Above 1,000 MWe)

- 5.2.2 Medium (500 to 1,000 MWe)

- 5.2.3 Small (Below 500 Mwe; includes SMRs and Micro-reactors)

- 5.3 By Fuel Type

- 5.3.1 Low-Enriched Uranium (Below 5% U-235)

- 5.3.2 High-Assay LEU (5 to 20% U-235)

- 5.3.3 Mixed Oxide (MOX)

- 5.3.4 Thorium-based Fuels

- 5.4 By Application

- 5.4.1 Grid-Connected Power

- 5.4.2 Off-grid/Remote Electrification

- 5.4.3 Industrial Process Heat and Steam

- 5.4.4 Desalination and District Heating

- 5.4.5 Defense and Military Bases

- 5.5 By End-User Sector

- 5.5.1 Utilities and IPPs

- 5.5.2 Industrial and Petro-chemical

- 5.5.3 Mining and Remote Operations

- 5.5.4 Government/Defense

- 5.5.5 Research Institutions

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 France

- 5.6.2.3 Sweden

- 5.6.2.4 Spain

- 5.6.2.5 Ukraine

- 5.6.2.6 Russia

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 South Africa

- 5.6.5.3 Egypt

- 5.6.5.4 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, JVs, Funding, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Products & Services, Recent Developments)

- 6.4.1 Electricite de France SA (EDF)

- 6.4.2 Rosatom State Atomic Energy Corporation

- 6.4.3 China National Nuclear Corporation (CNNC)

- 6.4.4 Westinghouse Electric Company LLC

- 6.4.5 GE-Hitachi Nuclear Energy

- 6.4.6 Framatome SA

- 6.4.7 Mitsubishi Heavy Industries Ltd

- 6.4.8 Korea Hydro & Nuclear Power / KEPCO E&C

- 6.4.9 BWX Technologies Inc.

- 6.4.10 Bechtel Corporation

- 6.4.11 Doosan Enerbility Co. Ltd

- 6.4.12 Fluor Corporation (NuScale)

- 6.4.13 SKODA JS a.s.

- 6.4.14 Holtec International

- 6.4.15 TerraPower LLC

- 6.4.16 Rolls-Royce SMR Ltd

- 6.4.17 X-Energy LLC

- 6.4.18 General Fusion Inc.

- 6.4.19 Ontario Power Generation

- 6.4.20 Babcock International Group

- 6.4.21 Bilfinger SE

- 6.4.22 Duke Energy Corporation

- 6.4.23 Japan Atomic Power Company

- 6.4.24 Ansaldo Nucleare

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

- 7.2 Advanced Small Modular Reactors

- 7.3 Floating Nuclear Plants

- 7.4 Nuclear Hydrogen & Ammonia Production

- 7.5 Data-Center & Marine Micro-reactors

- 7.6 Lifetime Extension Services Market

- 7.7 Decommissioning & Waste-Management Services

核能市場規模、佔有率和趨勢分析報告:按核子反應爐類型、應用、地區和細分市場預測(2026-2033 年)

核能市場規模、佔有率和趨勢分析報告:按核子反應爐類型、應用、地區和細分市場預測(2026-2033 年) 核能發電市場-全球產業規模、佔有率、趨勢、機會和預測:按應用、反應器類型、地區和競爭格局分類,2021-2031年

核能發電市場-全球產業規模、佔有率、趨勢、機會和預測:按應用、反應器類型、地區和競爭格局分類,2021-2031年 核能發電市場:依核子反應爐類型、電廠生命週期階段、電廠類型、應用、最終用戶和地區分類:產業趨勢與全球市場預測(至2035年)

核能發電市場:依核子反應爐類型、電廠生命週期階段、電廠類型、應用、最終用戶和地區分類:產業趨勢與全球市場預測(至2035年) 核能市場:依核子反應爐類型、應用和地區分類

核能市場:依核子反應爐類型、應用和地區分類 全球核能服務市場:策略洞察與預測(2026-2031年)

全球核能服務市場:策略洞察與預測(2026-2031年) 2026年全球核能發電市場報告2026年全球核能發電廠運作、燃料和儀器市場報告

2026年全球核能發電市場報告2026年全球核能發電廠運作、燃料和儀器市場報告 三通道二極體功率感測器市場:按產品類型、頻寬、分銷管道、應用和最終用戶分類的全球預測(2026-2032年)核能發電市場按反應器類型、運作類型、電廠規模、燃料類型、階段和應用分類-全球預測,2026-2032年核能發電廠服務市場按服務類型、核子反應爐類型、合約類型和最終用戶分類 - 全球預測 2026-2032

三通道二極體功率感測器市場:按產品類型、頻寬、分銷管道、應用和最終用戶分類的全球預測(2026-2032年)核能發電市場按反應器類型、運作類型、電廠規模、燃料類型、階段和應用分類-全球預測,2026-2032年核能發電廠服務市場按服務類型、核子反應爐類型、合約類型和最終用戶分類 - 全球預測 2026-2032