|

市場調查報告書

商品編碼

2066523

自動駕駛曳引機:市佔率分析、產業趨勢與統計、成長預測(2026-2031)Autonomous Tractors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

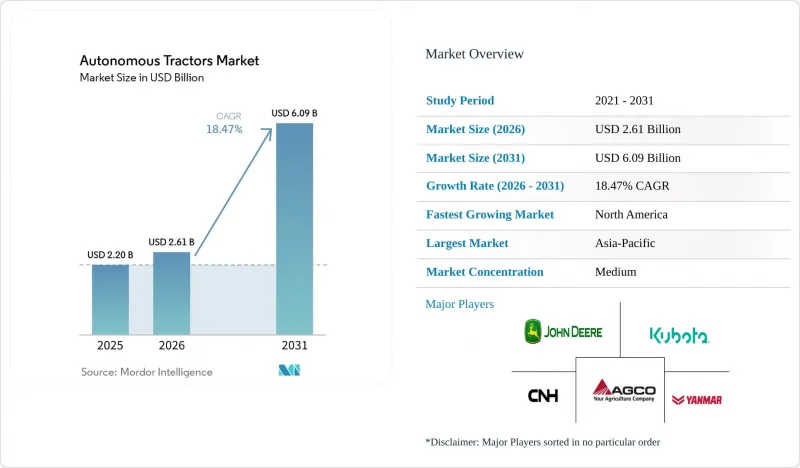

根據 Mordor Intelligence 預測,自動駕駛曳引機市場規模將從 2025 年的 22 億美元成長到 2026 年的 26.1 億美元,然後在 2031 年達到 60.9 億美元,2026 年至 2031 年的複合年成長率為 18.47%。

本報告按馬力(30馬力以下及以上)、自動化程度(全自動和半自動)、驅動系統(柴油及其他)、應用領域(犁地及其他)、組件(GPS/GNSS及其他)、農場規模(小規模、中型和大型)以及地區(北美、歐洲、亞太、南美及其他)進行細分。市場預測以美元計價。

全球自動駕駛曳引機市場趨勢及洞察

農業勞動力短缺和操作人員短缺

農業勞動力短缺仍然是推動自動駕駛曳引機需求的最主要因素。 2025會計年度,僅前三個季度,美國勞工部就批准了超過31.7萬份H-2A臨時農業工作簽證,這顯示國內勞動力供應仍無法滿足季節性農業需求。此外,外國農業工人的平均年齡不斷上升,導致勞動力供應日益緊張,難以獲得長期穩定的勞動力。因此,採用自動駕駛曳引機不僅被視為提高效率的手段,更被視為在操作員難以到崗的情況下維持農場運作的一種方式。在這種情況下,已經使用具備導航功能的曳引機的農場具有優勢,因為從人工操控功能升級到更先進的自動駕駛功能比更換整個曳引機車隊要快得多。這也推動了自動駕駛曳引機市場在那些長期依賴季節性工人會帶來營運風險的地區的擴張。

精密農業和互聯導航系統的引入

精密農業は、自律走行トラクター市場が現在、より高付加価値の自動化を構築するための基盤となっています。AGCO Corporationは2025年8月、異なるブランドの車両群間でガイダンス、圃場データ、自律走行管理を連携させる「PTx FarmENGAGE」プラットフォームを導入しました。これは、ソフトウェアの統合がトラクターのハードウェアと同様に重要になりつつあることを示しています。すでに自動ステアリング、デジタル境界設定、圃場記録を活用している農場ほど、業務への支障を最小限に抑えながら自律型ワークフローを導入しやすい状況にあります。これにより、切り替えのハードルが低くなり、単体の機械よりもコネクテッドなエコシステムの価値が高まります。また、これは自律型トラクター市場がプラットフォーム競合へと移行していることを意味しており、そこでは機械的な性能と同様に、データの継続性や車両群の互換性が重要視されます。その結果、幅広いデジタルツールを保有するメーカーは、トラクターの初期販売をはるかに超えて顧客の定着率を高めることができます。

小規模農場前期投入成本高,投資報酬率不確定

高昂的初始成本仍然是自動駕駛曳引機市場最明顯的障礙之一,尤其對於規模小於商業規模的農場更是如此。一套完整的自動駕駛系統通常包括曳引機本身、感知硬體、軟體以及持續的平台維護費用,其投資回收期遠遠超出了許多小規模農場的承受能力。因此,早期採用自動駕駛曳引機的主要是那些能夠將固定成本分攤到更大耕地面積和更長機器運作的大規模糧食農場,以及資金雄厚的專業農場主。在農作物價格波動和現金流前景惡化的背景下,這種壓力進一步加劇。雖然訂閱模式和附加選項正在逐步降低採用門檻,但更低的硬體價格和更標準化的資金籌措方案對於在中型市場廣泛普及仍然至關重要。在此之前,成本將繼續阻礙自動駕駛曳引機市場在小規模農業占主導地位地區的擴張。

細分市場分析

到2025年,31-100馬力細分市場將佔據38.9%的市場佔有率,這反映出中功率曳引機在大規模田間作物中已被廣泛應用。北美和歐洲的許多農場已經使用這一功率範圍內的帶導航功能的曳引機,因此,改裝升級比整車更換更具可行性,從而確保了該細分市場繼續保持最大佔有率。這些曳引機非常適合播種、噴灑和犁地等重複性作業,這些作業在商業性環境下易於自動化。因此,即使高功率的平台越來越受到關注,市場需求仍保持穩定。自動駕駛曳引機行業仍然高度依賴這一輸出範圍,因為它彌合了輔助轉向技術引入和更廣泛的自動駕駛技術應用之間的差距。

100馬力及以上馬力段是成長最快的馬力段,預計從2026年到2031年將以23.4%的複合年成長率成長,因為大規模農場正在將犁地和糧食處理作業轉向無人化作業。 AGCO公司於2025年底推出了配備原廠整合OutRun自動駕駛系統的Fendt 1000 Vario Gen4系列,並於2026年開始交付400-520馬力型號。迪爾公司也正在擴大其8R、8RX、9R和9RX系列曳引機的自動駕駛功能,以支援大規模商業農場的高功率田間作業。

預計到2025年,半自動系統將佔據67.6%的市場。其在自動駕駛曳引機市場的主導地位源於大多數商業應用中操作員仍然扮演著監督者的角色。該細分市場包含自動轉向、地頭轉彎和分段控制等功能,經銷商可以使用熟悉的工具和成熟的介面來安裝和支援這些系統。由於責任更接近機器操作員,農民也認為這些系統的風險較低。因此,該細分市場是目前自動駕駛曳引機市場中最大的商業應用管道。此外,它也更符合大多數國家的現行保險和監管要求。

完全自律型システムは最も急成長しているセグメントであり、ソフトウェア、知覚技術、および車両管理ツールの向上に伴い、2026年から2031年にかけてCAGR22.5%で拡大すると予測されています。AGCOコーポレーションは、2030年までに耕作から播種、散布、収穫の調整に至るまで自律性を拡大し、完全なサイクルをカバーする自律型作物生産システムを実現するという目標を掲げています。多くの農場では、まず半自動運転を通じて圃場の境界設定、デジタル記録の構築、そして信頼関係を築くことから始めるため、導入の道筋は段階的なものとなります。つまり、現在導入されている監視付きシステムの導入基盤は、将来的な無人化へのアップグレードに向けた供給源としても機能しているのです。自律走行トラクター市場において、この構造的な移行は、現在のシェアと将来の成長を単純に比較することよりも重要な意味を持ちます。

區域分析

到2025年,亞太地區將佔據全球自動駕駛曳引機市場45.8%的佔有率,成為以金額為準最高的地區。日本憑藉著先進的農業機器人研發以及穩步推進的自動化機械應用政策,鞏固了其市場地位。中國則受惠於其大力推動機械化普及的策略。印度雖然由於小規模農戶眾多、基礎設施不平衡,其向全自動駕駛的轉型速度較慢,但憑藉其高年曳引機銷量,市場規模正在不斷擴大。洋馬控股持續開發利用人工智慧和邊緣運算的農業作業輔助技術,這反映了該地區向實用型遠端自動化農業作業的轉型趨勢。韓國和澳洲仍然是重要的市場,老化的農業勞動力和廣大的耕地面積以不同的方式推動自動駕駛技術的應用。

北米は、自律型トラクター市場において最も急成長している地域セグメントであり、2026年から2031年にかけてCAGR22.6%で拡大すると予測されています。この地域は、広大な農地、高い人事費用、そして自律的な犁地、散布、穀物運搬のワークフローを導入する正当な理由となる農業構造といった利点に恵まれています。Deere &Companyは2026年にかけて自律犁地製品の提供を拡大しており、これにより大規模農業における初の実質的な商用導入基盤が構築される見込みです。カナダもまた、「カナダ農業食品自動化,インテリジェンス,ネットワーク(Canadian Agri-Food Automation and Intelligence Network)」への公的資金提供を通じて、よりクリーンで自動化された農業技術を支援しています。一方、メキシコでは、農場の規模が比較的小さいため、完全自律化による即時の経済効果が限定的であることから、導入は依然として初期段階にとどまっています。

歐洲憑藉其高度成熟的精密農業以及嚴格的安全和監管要求,仍然是自動駕駛曳引機市場的重要參與者。儘管歐盟的氣候和農業機械政策鼓勵投資低排放、數位化管理的農業機械,但與其他地區相比,自動駕駛應用案例仍面臨更嚴格的合規要求。從區域來看,德國、法國和英國的需求主導,而中東和非洲仍處於起步階段,主要集中在試點計畫和大型商業性農場運作。在南美洲,巴西和阿根廷擁有巨大的長期潛力,但進口成本、通訊基礎設施差異以及位置資料可靠性問題仍然阻礙自動駕駛曳引機的快速普及。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 農業勞動力短缺和企業管理人員短缺

- 精密農業和互聯導航系統的引入

- 政府支持智慧、低排放農業機械

- 透過 24 小時現場操作和監控多台機器,提高了生產效率。

- 改裝自動駕駛套件和具備自動駕駛功能的曳引機平台

- 果園和葡萄園特種作物的機械化

- 市場限制因素

- 小規模農場的初始成本高,投資報酬率不確定性。

- 無人野外作業中的安全、責任和監管方面的模糊之處

- 互聯車隊中的GNSS可靠性、連接性差距和網路風險

- 互通性實施和經銷商服務準備方面的瓶頸

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- By Horsepower

- 30馬力或以下

- 31~100 HP

- 100馬力或以上

- 按自動化級別

- 半自動

- 完全自主

- 透過驅動系統

- 柴油引擎

- 混合

- 電池式電動車

- 透過使用

- 犁地

- 播種

- 收成

- 果園和葡萄園的經營

- 按組件

- GPS/GNSS

- 感測器和視覺系統

- LiDAR和雷達模組

- 控制和導航軟體

- 按農場規模

- 小規模(不足100公頃)

- 中等規模(100-500公頃)

- 大型(超過500公頃)

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 其他北美國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- UAE

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Deere & Company

- AGCO Corporation

- CNH Industrial NV

- Kubota Corporation

- Mahindra & Mahindra

- Monarch Tractor

- AutoNext Automation

- YANMAR HOLDINGS CO., LTD.

- CLAAS KGaA mbH

- TYM Corporation

- SDF Group

- ZETOR TRACTORS as(HTC Corporation)

- Sonalika

- Kioti(daedong)

- ISEKI & Co., Ltd

第7章 市場機會與未來展望

According to Mordor Intelligence, the autonomous tractor market size is projected to grow from USD 2.20 billion in 2025 to USD 2.61 billion in 2026 and is forecast to reach USD 6.09 billion by 2031 at 18.47% CAGR over 2026-2031.

This report is Segmented by Horsepower (Up To 30 HP, and More), by Automation Level (Fully Automated and Semi-Automated), by Drive Type (Diesel, and More), by Application (Tillage, and More), by Component (GPS/GNSS, and More), by Farm Size (Small, Medium, and Large) and by Geography (North America, Europe, Asia-Pacific, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Autonomous Tractors Market Trends and Insights

Farm labor shortages and operator scarcity

The farm labor deficit remains the most durable demand driver for the autonomous tractor market. In fiscal year 2025, the United States Department of Labor certified more than 317,000 H-2A temporary agricultural positions in the first 3 quarters alone, which showed that the domestic labor supply still fell short of seasonal farm demand. The workforce pipeline is also narrowing as the average age of foreign-born farmworkers has continued to rise, weakening long-term labor availability. That makes adoption in the autonomous tractor market less about optional efficiency and more about maintaining field operations when operators are hard to secure. This setting favors farms that already run guidance-enabled fleets, because upgrades from supervised functions to higher autonomy can happen faster than full fleet replacement. It also supports the autonomous tractor market in regions where seasonal labor dependence has become a recurring operating risk.

Precision agriculture and connected guidance stack adoption

Precision agriculture has become the operating base on which the autonomous tractor market now builds higher-value automation. AGCO Corporation introduced the PTx FarmENGAGE platform in August 2025 to connect guidance, field data, and autonomy management across mixed-brand fleets, which showed that software integration is becoming as important as tractor hardware. Farms that already use automated steering, digital boundaries, and field records are better positioned to adopt autonomous workflows with less disruption. That lowers switching friction and strengthens the value of connected ecosystems over standalone machines. It also means the autonomous tractor market is moving toward platform competition, where data continuity and fleet compatibility matter as much as mechanical performance. As a result, manufacturers with broad digital tools can extend customer retention well beyond the initial tractor sale.

High upfront cost and uncertain return on investment for smaller farms

High initial cost remains one of the clearest limits on the autonomous tractor market, especially for farms below commercial scale. A full autonomous package usually includes the tractor, perception hardware, software, and ongoing platform costs, which stretches payback periods beyond what many smaller operations can accept. This keeps early adoption concentrated among larger grain farms and well-capitalized specialty operators that can spread fixed costs across more acres and more machine hours. The pressure becomes stronger when crop prices are volatile and cash flow visibility weakens. Subscription models and retrofit options are starting to reduce the entry burden, but broad mid-market penetration still depends on cheaper hardware and more standardized financing. Until then, cost will continue to slow the autonomous tractor market in regions dominated by smaller holdings.

Other drivers and restraints analyzed in the detailed report include:

- Government support for smart and low-emission farm equipment

- Productivity gains from 24-hour field operations and multi-machine supervision

- Safety, liability, and regulatory ambiguity for unattended field operations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 31 to 100 HP segment held 38.9% market share in 2025, and its share of the autonomous tractor market reflected the broad installed base of mid-range row-crop tractors already used across large field crops. This band remains the largest because many farms in North America and Europe already operate guidance-ready models in this range, making retrofit upgrades more practical than a complete fleet replacement. These tractors are well-suited for common sowing, spraying, and light tillage tasks that are repetitive and easier to automate under commercial conditions. That keeps demand steady even as higher-power platforms gain attention. The autonomous tractor industry still depends heavily on this range because it forms the bridge between assisted steering adoption and broader autonomy.

Above 100 HP is the fastest-growing horsepower segment and is projected to expand at 23.4% CAGR from 2026 to 2031 as very large farms shift more tillage and grain-cart operations toward driverless workflows. AGCO Corporation launched the Fendt 1000 Vario Gen4 series in late 2025 with factory-integrated OutRun autonomy, and commercial deliveries began in 2026 for models spanning 400 to 520 horsepower. Deere and Company also expanded compatibility for autonomous tillage on 8R, 8RX, 9R, and 9RX tractors, which supports higher-power field work on large commercial farms.

Semi-autonomous systems are projected to account for 67.6% of the market share in 2025. This dominance in the autonomous tractor market is attributed to the continued reliance on operators in supervisory roles for most commercial deployments. This segment includes automated steering, headland turning, and section control that dealers can install and support using familiar tools and established interfaces. Farmers also view these systems as lower-risk because responsibility remains closer to the machine operator. That makes the segment the largest commercial pathway in the autonomous tractor market today. It also fits better with current insurance and regulatory conditions in most countries.

Fully Autonomous systems are the fastest-growing segment and are forecast to rise at 22.5% CAGR from 2026 to 2031 as software, perception, and fleet management tools improve. AGCO Corporation has stated a goal of enabling a full-cycle autonomous crop production system by 2030, extending autonomy beyond tillage into seeding, spraying, and harvest coordination. The adoption path is gradual because many farms first build field boundaries, digital records, and trust through semi-autonomous use. That means the current installed base of supervised systems also serves as the feeder pipeline for later driverless upgrades. In the autonomous tractor market, this structural transition matters more than a simple comparison between current share and future growth.

Geography Analysis

Asia-Pacific held 45.8% of the autonomous tractor market share in 2025, which made it the largest region by value. Japan supports this position through advanced farm robotics development and a policy environment that has steadily moved toward the use of autonomous machinery. China benefits from broad mechanization priorities, while India adds scale through its large annual tractor sales base, even though smallholding patterns and uneven infrastructure slow the pursuit of full autonomy. YANMAR HOLDINGS CO., LTD. has continued to develop agricultural work-support technologies using artificial intelligence and edge computing, reflecting the region's push toward practical remote and autonomous farm operations. South Korea and Australia also remain important because aging farm populations and large operational footprints support adoption in different ways.

North America is the fastest-growing regional segment in the autonomous tractor market, projected to expand at a 22.6% CAGR from 2026 to 2031. The region benefits from large field sizes, high labor costs, and farm structures that can justify autonomous tillage, spraying, and grain-cart workflows. Deere & Company is scaling its autonomous tillage offering through 2026, which will support the first meaningful commercial installed base in large-scale agriculture. Canada is also supporting cleaner and more automated farm technology through public funding for the Canadian Agri-Food Automation and Intelligence Network. Mexico remains earlier in adoption because smaller farm structures reduce the immediate economics of full autonomy.

Europe remains an important part of the autonomous tractor market because it combines strong precision agriculture maturity with strict safety and regulatory oversight expectations. The European Union's climate and machinery policy is supporting investment in low-emission, digitally managed farm equipment, even though unattended use cases still face tighter compliance requirements than in some other regions. Germany, France, and the United Kingdom lead regional demand, while the Middle East and Africa remain earlier-stage markets centered on pilot activity and commercial estate farming. South America has strong long-run potential in Brazil and Argentina, but import costs, connectivity gaps, and correction reliability issues still restrain faster rollout.

- Deere & Company

- AGCO Corporation

- CNH Industrial N.V.

- Kubota Corporation

- Mahindra & Mahindra

- Monarch Tractor

- AutoNext Automation

- YANMAR HOLDINGS CO., LTD.

- CLAAS KGaA mbH

- TYM Corporation

- SDF Group

- ZETOR TRACTORS a.s. (HTC Corporation)

- Sonalika

- Kioti (daedong)

- ISEKI & Co., Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Farm labor shortages and operator scarcity

- 4.2.2 Precision agriculture and connected guidance stack adoption

- 4.2.3 Government support for smart and low-emission farm equipment

- 4.2.4 Productivity gains from 24-hour field operations and multi-machine supervision

- 4.2.5 Retrofit autonomy kits and autonomy-ready tractor platforms

- 4.2.6 Specialty-crop mechanization in orchards and vineyards

- 4.3 Market Restraints

- 4.3.1 High upfront cost and uncertain return on investment for smaller farms

- 4.3.2 Safety, liability, and regulatory ambiguity for unattended field operations

- 4.3.3 GNSS reliability, connectivity gaps, and cyber risk in connected fleets

- 4.3.4 Implement interoperability and dealer-service readiness bottlenecks

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Horsepower

- 5.1.1 Up to 30 HP

- 5.1.2 31 - 100 HP

- 5.1.3 Above 100 HP

- 5.2 By Automation Level

- 5.2.1 Semi-Autonomous

- 5.2.2 Fully Autonomous

- 5.3 By Drive Type

- 5.3.1 Diesel

- 5.3.2 Hybrid

- 5.3.3 Battery-Electric

- 5.4 By Application

- 5.4.1 Tillage

- 5.4.2 Sowing

- 5.4.3 Harvesting

- 5.4.4 Orchard and Vineyard Operations

- 5.5 By Component

- 5.5.1 GPS/GNSS

- 5.5.2 Sensors and Vision Systems

- 5.5.3 LiDAR and Radar Modules

- 5.5.4 Control and Navigation Software

- 5.6 By Farm Size

- 5.6.1 Small ( Less than 100 ha)

- 5.6.2 Medium (100-500 ha)

- 5.6.3 Large ( More than 500 ha)

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.1.4 Rest of North America

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Spain

- 5.7.3.5 Russia

- 5.7.3.6 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 India

- 5.7.4.3 Japan

- 5.7.4.4 Australia

- 5.7.4.5 South Korea

- 5.7.4.6 Rest of Asia-Pacific

- 5.7.5 Middle East

- 5.7.5.1 Saudi Arabia

- 5.7.5.2 UAE

- 5.7.5.3 Turkey

- 5.7.5.4 Rest of Middle East

- 5.7.6 Africa

- 5.7.6.1 South Africa

- 5.7.6.2 Rest of Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for Key companies, Products and Services, and Recent Developments)

- 6.4.1 Deere & Company

- 6.4.2 AGCO Corporation

- 6.4.3 CNH Industrial N.V.

- 6.4.4 Kubota Corporation

- 6.4.5 Mahindra & Mahindra

- 6.4.6 Monarch Tractor

- 6.4.7 AutoNext Automation

- 6.4.8 YANMAR HOLDINGS CO., LTD.

- 6.4.9 CLAAS KGaA mbH

- 6.4.10 TYM Corporation

- 6.4.11 SDF Group

- 6.4.12 ZETOR TRACTORS a.s. (HTC Corporation)

- 6.4.13 Sonalika

- 6.4.14 Kioti (daedong)

- 6.4.15 ISEKI & Co., Ltd

7 Market Opportunities and Future Outlook

自主和半自動自主曳引機市場:按產品、曳引機類型、組件、自主程度、功率輸出、推進類型、應用和最終用戶分類-全球預測,2026-2032年

自主和半自動自主曳引機市場:按產品、曳引機類型、組件、自主程度、功率輸出、推進類型、應用和最終用戶分類-全球預測,2026-2032年 自動駕駛曳引機市場規模、佔有率和成長分析:按自動駕駛等級、組件、功率輸出、驅動系統、應用、技術和地區分類-2026-2033年產業預測自動駕駛曳引機市場:按運輸方式、應用程式和最終用戶分類-2026-2032年全球市場預測

自動駕駛曳引機市場規模、佔有率和成長分析:按自動駕駛等級、組件、功率輸出、驅動系統、應用、技術和地區分類-2026-2033年產業預測自動駕駛曳引機市場:按運輸方式、應用程式和最終用戶分類-2026-2032年全球市場預測 自動曳引機市場規模、佔有率、趨勢和預測:按組件、產量、作物類型、應用和地區分類,2026-2034年

自動曳引機市場規模、佔有率、趨勢和預測:按組件、產量、作物類型、應用和地區分類,2026-2034年 2026-2034年全球自動駕駛曳引機市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球自動駕駛曳引機市場規模、佔有率、趨勢和成長分析報告 2026年全球自動播種機市場報告

2026年全球自動播種機市場報告 2026-2035年自動駕駛曳引機市場機會、成長要素、產業趨勢分析及預測

2026-2035年自動駕駛曳引機市場機會、成長要素、產業趨勢分析及預測 自動駕駛曳引機市場預測:至 2034 年-全球分析(按自動駕駛等級、馬力、組件、農場規模、農場類型、驅動系統、應用和地區分類)

自動駕駛曳引機市場預測:至 2034 年-全球分析(按自動駕駛等級、馬力、組件、農場規模、農場類型、驅動系統、應用和地區分類) 2035年自動駕駛曳引機市場分析及預測:按類型、產品類型、技術、組件、應用、最終用戶、功能、安裝類型、解決方案和模式分類

2035年自動駕駛曳引機市場分析及預測:按類型、產品類型、技術、組件、應用、最終用戶、功能、安裝類型、解決方案和模式分類 自動曳引機市場:按組件、應用、功率和地區分類

自動曳引機市場:按組件、應用、功率和地區分類