|

市場調查報告書

商品編碼

2019227

2026-2035年自動駕駛曳引機市場機會、成長要素、產業趨勢分析及預測Autonomous Tractors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

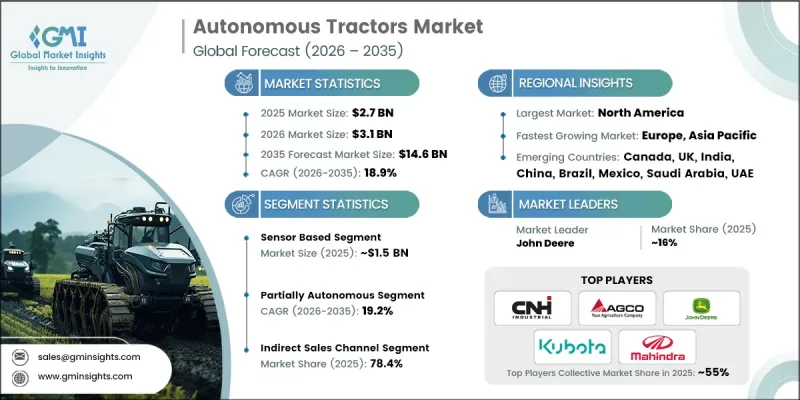

2025 年全球自動駕駛曳引機市場價值為 27 億美元,預計到 2035 年將達到 146 億美元,年複合成長率為 18.9%。

這種快速成長正在改變現代農業,其主要驅動力是勞動力短缺和對更有效率農場管理日益成長的需求。在許多地區,尤其是在已開發國家,農業勞動力正在老化,而進入該行業的年輕農民卻越來越少。自動駕駛曳引機透過減少對人力的依賴來應對這些挑戰。這使得機器運作而不疲勞,並能處理重複性或單調的任務,從而幫助農民更有效率地管理大規模農場。隨著人事費用的上升和勞動力短缺,自動駕駛曳引機對於及時播種、施肥和收割至關重要,同時也有助於提高生產力和資源管理效率。

| 市場規模 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 27億美元 |

| 預測金額 | 146億美元 |

| 複合年成長率 | 18.9% |

精密農業的普及是另一個重要的成長要素。農民們正在加速採用先進的GPS、人工智慧和感測器系統等技術,這些技術能夠使曳引機運作高精度作業。自動駕駛曳引機利用這些技術來最佳化作物產量、減少浪費,並確保水、種子和肥料的高效利用。

預計到2025年,基於感測器的系統市場規模將達到15億美元,並在2026年至2035年間以19.5%的複合年成長率成長。諸如雷射雷達、超音波、紅外線和接近感測器等系統能夠即時監測土壤狀況和作物生長情況,進行障礙物檢測,並在複雜的田間環境中安全地引導曳引機作業。隨著數位農業的擴展,對能夠分析環境數據並自主調整作業的智慧系統的需求激增。

到2025年,部分自動駕駛曳引機將佔據57%的市場佔有率,預計2026年至2035年將以19.2%的複合年成長率成長。這些車型結合了GPS輔助轉向、自動速度控制和導航引導,並輔以人工決策,為全自動駕駛曳引機提供了經濟高效的替代方案。與現有基礎設施和農業實踐的兼容性降低了推廣門檻,縮短了培訓時間,使其成為預算有限的發展中地區農民的理想選擇。

美國自動駕駛曳引機市場預計到2025年將達到7億美元,並在2035年之前以19.2%的複合年成長率成長。美國農民率先採用者自動化和精密農業技術,以提高生產力、減少對勞動力的依賴並最佳化資源利用。一個強大的農業技術供應商生態系統,包括將人工智慧、物聯網、GPS和數據分析技術整合到自動駕駛曳引機中的公司,正在推動智慧農業的普及和創新。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 農業部門勞動力短缺

- 對精密農業的需求日益成長

- 提高農業生產力和效率

- 永續性和環境議題

- 產業潛在風險與挑戰

- 高昂的初始投資成本

- 技術複雜性與技能差距

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 透過技術

- 監理情勢

- 標準和合規要求

- 區域法規結構

- 認證標準

- 貿易統計

- 主要進口國

- 主要出口國

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依技術分類,2022-2035年

- GPS導航

- 感測器基座

- 遙控

第6章 市場估算與預測:依自動化程度分類,2022-2035年

- 完全自動駕駛

- 半自動駕駛

- 進階自動駕駛

第7章 市場估計與預測:依產量分類,2022-2035年

- 輕載(小於50馬力)

- 中型(50-100馬力)

- 大型(超過100馬力)

第8章 市場估算與預測:依作物類型分類,2022-2035年

- 糧食

- 田間作物

- 特種作物

- 飼料作物

第9章 市場估計與預測:依應用領域分類,2022-2035年

- 農業

- 犁地和土壤準備

- 種植和播種

- 作物監測與管理

- 收割工作

- 礦業

- 物料輸送和運輸

- 場地準備和維護

- 廢棄物管理

- 收集和分類

- 場地維護和運營

第10章 市場估價與預測:依通路分類,2022-2035年

- 直接地

- 間接

第11章 市場估價與預測:按地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 印尼

- 馬來西亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

第12章:公司簡介

- AGCO

- Argo Tractors

- AutoNext Automation

- Autonomous Tractor Corporation

- CNH Industrial

- Dutch Power Company

- John Deere

- Kubota Corporation

- Mahindra and Mahindra Ltd

- Raven Industries

- SDF Group

- Trimble

- TYM Corporation

- Yanmar Co. Ltd

- Zimeno Inc.

The Global Autonomous Tractors Market was valued at USD 2.7 billion in 2025 and is estimated to grow at a CAGR of 18.9% to reach USD 14.6 billion by 2035.

The rapid growth is reshaping modern agriculture, driven largely by labor shortages and the increasing demand for efficient farming operations. In many regions, particularly in developed economies, the farming workforce is aging, and fewer young farmers are entering the industry. Autonomous tractors address these challenges by reducing dependence on human labor, allowing machinery to operate long hours without fatigue, manage repetitive or tedious tasks, and enable farmers to oversee large-scale farms more efficiently. Rising labor costs and scarce workforce availability make autonomous tractors essential for timely planting, fertilizing, and harvesting operations, while also improving productivity and resource management.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.7 Billion |

| Forecast Value | $14.6 Billion |

| CAGR | 18.9% |

The adoption of precision agriculture is another key growth factor. Farmers are increasingly integrating technologies such as advanced GPS, artificial intelligence, and sensor systems, which allow tractors to operate with high accuracy. Autonomous tractors use these technologies to optimize crop yields, reduce waste, and ensure efficient use of water, seeds, and fertilizers.

The sensor-based systems segment reached USD 1.5 billion in 2025, are expected to grow at a CAGR of 19.5% from 2026 to 2035. Sensors such as LiDAR, ultrasonic, infrared, and proximity systems enable real-time monitoring of soil conditions, crop health, and obstacle detection, guiding tractors safely through complex field environments. As digital farming expands, demand for intelligent systems capable of interpreting environmental data and autonomously adjusting operations is rising sharply.

The partially autonomous tractors segment held 57% share in 2025 and is projected to grow at a CAGR of 19.2% from 2026 to 2035. These models combine GPS-assisted steering, auto-speed control, and guided navigation with human oversight for decision-making, offering a cost-effective alternative to fully autonomous units. Their compatibility with existing infrastructure and farming practices reduces adoption barriers and shortens the learning curve, making them especially attractive to farmers in developing regions where budgets are constrained.

U.S. Autonomous Tractors Market captured USD 0.7 billion in 2025, and is expected to grow at a CAGR of 19.2% through 2035. U.S. farmers are early adopters of automation and precision farming technologies to enhance productivity, lower labor dependence, and optimize resource usage. A strong ecosystem of agri-tech providers, including companies that integrate AI, IoT, GPS, and data analytics into autonomous tractors, facilitates adoption and drives innovation in smart farming.

Prominent players in the Global Autonomous Tractors Market include AGCO, Argo Tractors, AutoNxt Automation, Autonomous Tractor Corporation, CNH Industrial, Dutch Power Company, John Deere, Kubota Corporation, Mahindra and Mahindra Ltd, Raven Industries, SDF Group, Trimble, TYM Corporation, Yanmar Co. Ltd, and Zimeno Inc. (DBA Monarch Tractor). Companies in the autonomous tractor market strengthen their position by focusing on continuous R&D and technology integration, offering partially and fully autonomous models to cater to varying farm sizes and budgets, and providing end-to-end solutions combining hardware, software, and data analytics. Partnerships and strategic collaborations with tech firms enable rapid innovation and adoption of AI, sensor, and IoT technologies. Firms also expand through geographical diversification, targeting emerging markets with customized offerings suitable for local agricultural practices. Enhancing customer support, training programs, and providing flexible financing options further improve accessibility, building trust and long-term customer loyalty while sustaining market growth.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Technology

- 2.2.3 Automation

- 2.2.4 Power output

- 2.2.5 Crop type

- 2.2.6 Application

- 2.2.7 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Labor shortages in agriculture

- 3.2.1.2 Rising demand for precision agriculture

- 3.2.1.3 Increasing farm productivity and efficiency

- 3.2.1.4 Sustainability and environmental concerns

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial investment costs

- 3.2.2.2 Technical complexity and skill gaps

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By technology

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Technology, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 GPS guidance

- 5.3 Sensor based

- 5.4 Remote control

Chapter 6 Market Estimates & Forecast, By Automation, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Fully autonomous

- 6.3 Partially autonomous

- 6.4 Highly autonomous

Chapter 7 Market Estimates & Forecast, By Power Output, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Light duty (<50 HP)

- 7.3 Medium-duty (50-100 HP)

- 7.4 Heavy-duty (>100 HP)

Chapter 8 Market Estimates & Forecast, By Crop Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Cereal crops

- 8.3 Row crops

- 8.4 Specialty crops

- 8.5 Forage crops

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Agriculture

- 9.2.1 Tillage and soil preparation

- 9.2.2 Planting and seeding

- 9.2.3 Crop monitoring and management

- 9.2.4 Harvesting operations

- 9.3 Mining

- 9.3.1 Material handling and transport

- 9.3.2 Site preparation and maintenance

- 9.4 Waste management

- 9.4.1 Collection and sorting

- 9.4.2 Site maintenance and operations

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Direct

- 10.3 Indirect

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.4.6 Indonesia

- 11.4.7 Malaysia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 Saudi Arabia

- 11.6.2 UAE

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 AGCO

- 12.2 Argo Tractors

- 12.3 AutoNext Automation

- 12.4 Autonomous Tractor Corporation

- 12.5 CNH Industrial

- 12.6 Dutch Power Company

- 12.7 John Deere

- 12.8 Kubota Corporation

- 12.9 Mahindra and Mahindra Ltd

- 12.10 Raven Industries

- 12.11 SDF Group

- 12.12 Trimble

- 12.13 TYM Corporation

- 12.14 Yanmar Co. Ltd

- 12.15 Zimeno Inc.

2026年全球自動駕駛曳引機市場報告

2026年全球自動駕駛曳引機市場報告 自動駕駛曳引機市場:按產品、移動性、推進類型、導航技術、應用和最終用戶分類-2026-2032年全球市場預測自主和半自動自主曳引機市場:按產品、曳引機類型、組件、自主程度、功率輸出、推進類型、應用和最終用戶分類-全球預測,2026-2032年

自動駕駛曳引機市場:按產品、移動性、推進類型、導航技術、應用和最終用戶分類-2026-2032年全球市場預測自主和半自動自主曳引機市場:按產品、曳引機類型、組件、自主程度、功率輸出、推進類型、應用和最終用戶分類-全球預測,2026-2032年 自動駕駛曳引機市場規模、佔有率和成長分析:按自動駕駛等級、組件、功率輸出、驅動系統、應用、技術和地區分類-2026-2033年產業預測

自動駕駛曳引機市場規模、佔有率和成長分析:按自動駕駛等級、組件、功率輸出、驅動系統、應用、技術和地區分類-2026-2033年產業預測 自動駕駛曳引機:市佔率分析、產業趨勢與統計、成長預測(2026-2031)

自動駕駛曳引機:市佔率分析、產業趨勢與統計、成長預測(2026-2031) 自動曳引機市場規模、佔有率、趨勢和預測:按組件、產量、作物類型、應用和地區分類,2026-2034年

自動曳引機市場規模、佔有率、趨勢和預測:按組件、產量、作物類型、應用和地區分類,2026-2034年 2026-2034年全球自動駕駛曳引機市場規模、佔有率、趨勢和成長分析報告2026年全球自動播種機市場報告

2026-2034年全球自動駕駛曳引機市場規模、佔有率、趨勢和成長分析報告2026年全球自動播種機市場報告 自動駕駛曳引機市場預測:至 2034 年-全球分析(按自動駕駛等級、馬力、組件、農場規模、農場類型、驅動系統、應用和地區分類)

自動駕駛曳引機市場預測:至 2034 年-全球分析(按自動駕駛等級、馬力、組件、農場規模、農場類型、驅動系統、應用和地區分類) 2035年自動駕駛曳引機市場分析及預測:按類型、產品類型、技術、組件、應用、最終用戶、功能、安裝類型、解決方案和模式分類

2035年自動駕駛曳引機市場分析及預測:按類型、產品類型、技術、組件、應用、最終用戶、功能、安裝類型、解決方案和模式分類