|

市場調查報告書

商品編碼

2066516

威脅情報:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)Threat Intelligence - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

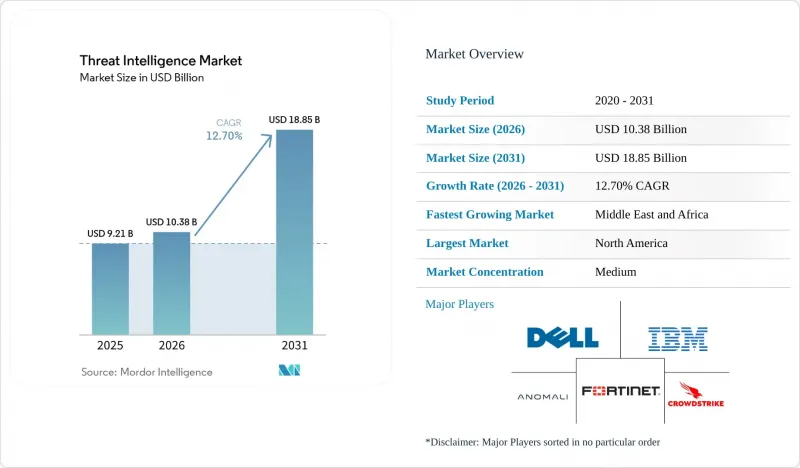

據 Mordor Intelligence 稱,威脅情報市場預計到 2026 年價值 103.8 億美元,高於 2025 年的 92.1 億美元,預計到 2031 年將達到 188.5 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 12.7%。

本報告按組件(解決方案和服務)、部署模式(本地部署、雲端部署、混合部署)、威脅情報類型(策略、戰術性、營運、技術)、組織規模(大型企業、中小企業)、最終用戶產業(銀行、金融服務和保險 (BFSI)、IT 和電信、其他)以及地區進行細分。市場預測以美元 (USD) 為單位。

全球威脅情報市場趨勢與洞察

針對雲端原生工作負載的AI驅動型多型惡意軟體

人工智慧產生的多態惡意軟體可以動態重寫程式碼,使傳統的基於特徵碼的工具失效,迫使防禦者依賴行為分析。 IBM 的研究表明,此類惡意軟體現在無需人工干預即可進行勒索談判,並根據雲端配置切換策略,這使得事件回應更加複雜。美國司法部最近破獲了一個犯罪組織,該組織利用人工智慧漏洞竊取了價值 2.63 億美元的加密貨幣,凸顯了其中存在的金融風險。北美企業正在增加基於機器學習的偵測預算,這使得威脅情報市場對於保護雲端工作負載至關重要。

關鍵基礎設施營運商的歐盟-NIS2合規支出

將於2024年10月生效的NIS2指令將強制要求歐洲約30萬家營業單位進行風險評估、事件通報和供應鏈審查。由於罰款最高可達1000萬歐元,相當於全球營業額的2%,各公司董事會將被迫優先考慮即時情報。歐盟以外的跨國公司在服務歐盟客戶時也需要遵守該指令,這為提供符合審計要求的情報資料的供應商創造了商機。

傳統 SOC 中 STIX/TAXII互通性所面臨的挑戰

儘管 STIX 和 TAXII 已於 2021 年成為 OASIS 標準,但許多傳統平台仍使用各自的專有格式,阻礙了資料的無縫共用。初步研究表明,整合複雜性和不一致的表示方法是主要障礙。因此,各組織正推遲平台升級,導致短期支出減少。

細分市場分析

到2025年,解決方案將佔全球整體收入的55.40%,平台將在威脅情報市場佔據主導地位。光是微軟Defender威脅情報每天就能處理78兆個訊號,凸顯了其規模優勢。這種主導地位也解釋了為什麼平台相關的市場規模預計將持續成長至2031年。領先的供應商正在將人工智慧融入行為分析,以減輕分析師的工作量並提高偵測準確率。

託管服務和專業服務以14.12%的複合年成長率 (CAGR) 超過產品成長,反映出人才短缺和業務複雜性的日益加劇。 SANS 的研究表明,許多公司正在將威脅情報搜尋業務外包,以彌補技能缺口。將部署與培訓相結合的夥伴關係能夠幫助客戶更快地獲得價值,從而推動服務採用率的提高,尤其是在威脅情報產業的中端市場。

到2025年,本地部署將佔總支出的54.30%,因為受嚴格監管的行業更傾向於將資料儲存在本地。然而,雲端託管平台的成長速度最快,複合年成長率高達16.25%,反映出雲端服務供應商安全性的提升以及市場對FedRAMP擴展的信心增強,例如微軟Defender威脅情報已獲得「高」級認證。產業分析師預測,在預測期的後半段,雲端交付威脅情報市場的規模將超過本地部署市場。

這種將傳統感測器與基於SaaS的分析相結合的混合方法,對那些希望按自身節奏進行現代化改造的組織來說極具吸引力。隨著金融監管機構發布安全雲採用藍圖(其中特別提到了持續智慧整合),這一趨勢正在加速發展。

區域分析

預計到2025年,北美將佔全球收入的37.50%,共用其成熟的雲端運算應用、公私合作模式以及強大的廠商實力。立法機構持續加強資訊揭露法律,聯邦機構也支持即時資料交換平台,從而促進了威脅情報市場的發展。針對雲端工作負載的人工智慧惡意軟體仍然是該地區面臨的最大挑戰,推動了相關平台的強勁支出。

在NIS2的推動下,歐洲的前景一片光明。 NIS2將覆蓋範圍從2萬個實體擴大到30萬個營業單位,顯著擴大了威脅情報市場。諸如《網路彈性法案》等配套法規進一步提升了整個供應鏈對持續漏洞資訊的需求。能夠提供可審計報告和多語言威脅資料的供應商將佔據有利地位。

預計中東地區將成為成長最快的地區,到2031年年複合成長率(CAGR)將達到15.35%。阿拉伯聯合大公國和沙烏地阿拉伯的國家機構正在投資建造專注於特定領域的整合中心,而大型能源公司則因獲得與即時威脅情報資訊掛鉤的網路保險而享受折扣。該地區日益緊張的地緣政治局勢正在提升威脅情報市場對公共和私營部門的戰略價值。

在亞太地區,網路攻擊數量正以兩位數的速度成長,其中印尼每周遭受的網路攻擊事件超過3300起。快速的數位化進程和多樣化的主權法規導致需求分散。日本、韓國和澳洲正在主導「零信任」先導計畫,將即時情報融入存取控制;而中國和印度的資料本地化法律則促使用戶更傾向於使用本國雲端節點。

在南美洲,中型銀行、金融和保險(BFSI)公司透過外包威脅狩獵來彌補自身技能不足,從而推動了威脅狩獵技術的普及。雖然用戶群體規模較小,但它對全球收入做出了貢獻。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 針對北美雲端原生工作負載的AI驅動型多型惡意軟體

- 關鍵基礎設施營運商為遵守歐盟NIS2法規而進行的支出

- 亞太地區大型企業零信任實施

- RaaS卡特爾推動了對加密貨幣錢包監控的需求

- 南美一家中型銀行、金融服務和保險 (BFSI) 公司將威脅狩獵外包

- 網路保險保費折扣與即時威脅情報掛鉤(中東能源)

- 市場限制因素

- 傳統 SOC 中的 STIX/TAXII互通性差距

- 訂閱實用情報數據的成本不斷上漲。

- 資料主權面臨的障礙(例如,中國的CSL、印度的DPDP)

- 在資源有限的團隊中,分析師疲勞和過度產生警報的問題日益突出。

- 監理展望

- 技術展望

- 波特五力分析

- 評估宏觀經濟因素對市場的影響

第5章 市場規模與成長預測

- 按組件

- 解決方案

- 威脅情報平台

- 安全資訊和事件管理 (SIEM) 資訊來源

- 威脅狩獵/分析工具

- 服務

- 託管/外包服務

- 專業諮詢

- 培訓和支持

- 解決方案

- 不同的發展

- 現場

- 雲

- 混合

- 威脅情報的類型

- 策略

- 戰術性的

- 手術

- 科技

- 按組織規模

- 大公司

- 小型企業

- 按最終用戶行業分類

- BFSI

- 資訊科技/通訊

- 零售與電子商務

- 製造業

- 醫療保健和生命科學

- 政府/國防

- 能源公用事業

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 秘魯

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 澳洲

- 紐西蘭

- 其他亞太國家

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- Strategic Developments

- Vendor Positioning Analysis

- 公司簡介

- IBM Corporation

- Cisco Systems Inc.

- Dell Technologies Inc.

- CrowdStrike Holdings Inc.

- Check Point Software Technologies Ltd.

- Trend Micro Incorporated

- Palo Alto Networks Inc.

- Fortinet Inc.

- Rapid7 Inc.

- Secureworks Inc.

- FireEye-Trellix

- Recorded Future Inc.

- Anomali Inc.

- LookingGlass Cyber Solutions Inc.

- LogRhythm Inc.

- McAfee LLC

- Broadcom Inc.(Symantec)

- Juniper Networks Inc.

- F-Secure Corporation

- SentinelOne Inc.

- Microsoft Corp.(Defender Threat Intelligence)

第7章 市場機會與未來展望

According to Mordor Intelligence, threat intelligence market size in 2026 is estimated at USD 10.38 billion, growing from 2025 value of USD 9.21 billion with 2031 projections showing USD 18.85 billion, growing at 12.7% CAGR over 2026-2031.

This report is Segmented by Component (Solutions, and Services), Deployment (On-Premise, Cloud, and Hybrid), Threat-Intelligence Type (Strategic, Tactical, Operational, and Technical), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (BFSI, IT and Telecommunications, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Threat Intelligence Market Trends and Insights

AI-driven Polymorphic Malware Targeting Cloud-Native Workloads

AI-generated polymorphic malware can rewrite its code on the fly, defeating traditional signature tools and forcing defenders to rely on behavioural analytics. IBM research shows such malware now negotiates ransoms without human contact and pivots tactics based on cloud configuration, complicating incident response. The U.S. Department of Justice recently dismantled a ring that stole USD 263 million in cryptocurrency through AI-enabled exploits, underscoring the financial risk. North American enterprises are boosting budget for machine-learning detection, making the threat intelligence market essential for cloud workload protection.

EU-NIS2 Compliance Spend by Critical Infrastructure Operators

Effective October 2024, the NIS2 directive subjects roughly 300,000 European entities to mandatory risk assessments, incident reporting, and supply-chain scrutiny. Penalties can reach EUR 10 million or 2% of global turnover, pushing boards to prioritise real-time intelligence. Multinationals outside the bloc must also comply when serving EU customers, widening opportunity for vendors that package ready-to-audit intelligence feeds.

STIX/TAXII Interoperability Gaps in Legacy SOCs

Although STIX and TAXII became OASIS standards in 2021, many legacy platforms still process proprietary formats, preventing seamless data sharing. An exploratory study identified integration complexity and inconsistent notation as primary hurdles. As a result, organisations delay platform upgrades, restraining short-term spending.

Other drivers and restraints analyzed in the detailed report include:

- Zero Trust Roll-outs in APAC Large Enterprises

- RaaS Cartels Fuelling Crypto-Wallet Monitoring Demand

- Escalating Subscription Costs for Actionable Intel Data

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions generated 55.40% of global revenue in 2025, giving platforms an outsized hold on the threat intelligence market. Microsoft Defender Threat Intelligence alone processes 78 trillion signals per day, highlighting scale advantages. This dominance underlines why the market size attached to platforms is expected to keep rising through 2031. Leading vendors incorporate AI for behaviour analytics, easing analyst workload and improving detection fidelity.

Managed and professional services are outpacing product growth with a 14.12% CAGR, reflecting talent shortages and rising complexity. SANS surveys show many enterprises outsource hunting duties to close skill gaps. Partnerships that wrap training around deployments allow buyers to derive quicker value, propelling service uptake, especially across the threat intelligence industry's mid-market segment.

On-premise deployments held 54.30% of spending in 2025 as heavily regulated sectors prefer local data residency. Even so, cloud-hosted platforms are the fastest riser at 16.25% CAGR, signalling confidence in provider hardening and FedRAMP expansions such as Microsoft Defender Threat Intelligence gaining High attestation. Segment observers see the threat intelligence market size for cloud deliveries eclipsing on-premise totals late in the forecast window.

Hybrid approaches blend legacy sensors with SaaS analytics, appealing to organisations modernising at their own pace. Financial regulators now publish blueprints for secure cloud adoption that specifically mention continuous intelligence integration, accelerating momentum.

Geography Analysis

North America commanded 37.50% of 2025 revenue owing to mature cloud uptake, joint public-private information sharing, and deep vendor presence. Legislators continue to refine disclosure laws, while federal bodies sponsor real-time data-exchange platforms that reinforce the threat intelligence market. AI-enabled malware against cloud workloads remains the top regional concern, keeping platform spending buoyant.

Europe's outlook brightens under NIS2, which scales mandatory coverage from 20 000 to 300 000 entities, greatly enlarging the addressable threat intelligence market. Complementary legislation such as the Cyber Resilience Act furthers demand for continuous vulnerability context across supply chains. Vendors that package audit-ready reporting with multi-lingual threat data are well positioned.

The Middle East shows the fastest CAGR at 15.35% through 2031. National agencies in the UAE and Saudi Arabia invest in sector-focused fusion centres while energy majors receive cyber-insurance discounts tied to live feeds. Rising geopolitical tension in the region elevates the strategic value of the threat intelligence market for both public and private sectors.

Asia-Pacific sees a double-digit attack uptick, notably in Indonesia where weekly incidents top 3,300. Rapid digitalisation, paired with diverse sovereignty rules, produces fragmented demand. Japan, South Korea, and Australia lead Zero Trust pilots that embed live intelligence into access decisions, while China and India's data-localisation laws create preferences for in-country cloud nodes.

South America's adoption is spurred by mid-tier BFSI outsourcing threat-hunting to overcome skills shortages, adding to global revenue even if from a smaller base.

- IBM Corporation

- Cisco Systems Inc.

- Dell Technologies Inc.

- CrowdStrike Holdings Inc.

- Check Point Software Technologies Ltd.

- Trend Micro Incorporated

- Palo Alto Networks Inc.

- Fortinet Inc.

- Rapid7 Inc.

- Secureworks Inc.

- FireEye - Trellix

- Recorded Future Inc.

- Anomali Inc.

- LookingGlass Cyber Solutions Inc.

- LogRhythm Inc.

- McAfee LLC

- Broadcom Inc. (Symantec)

- Juniper Networks Inc.

- F-Secure Corporation

- SentinelOne Inc.

- Microsoft Corp. (Defender Threat Intelligence)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI-Driven Polymorphic Malware Targeting Cloud-Native Workloads in North America

- 4.2.2 EU-NIS2 Compliance Spend by Critical Infrastructure Operators

- 4.2.3 Zero-Trust Roll-outs in APAC Large Enterprises

- 4.2.4 RaaS Cartels Fueling Crypto-Wallet Monitoring Demand

- 4.2.5 Outsourced Threat-Hunting by South-American Mid-Tier BFSI

- 4.2.6 Cyber-Insurance Premium Discounts Tied to Live Threat Feeds (Middle East Energy)

- 4.3 Market Restraints

- 4.3.1 STIX/TAXII Interoperability Gaps in Legacy SOCs

- 4.3.2 Escalating Subscription Costs for Actionable Intel Data

- 4.3.3 Data-Sovereignty Barriers (China CSL, India DPDP, etc.)

- 4.3.4 Analyst Fatigue and Alert Overload in Resource-Constrained Teams

- 4.4 Regulatory Outlook

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Assessment of the Impact of Macroeconomic Factors on the Market

5 Market Size and Growth Forecasts (Value)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.1.1 Threat Intelligence Platforms

- 5.1.1.2 Security Information and Event Management (SIEM) Feeds

- 5.1.1.3 Threat Hunting/Analytics Tools

- 5.1.2 Services

- 5.1.2.1 Managed/Outsourced Services

- 5.1.2.2 Professional and Consulting

- 5.1.2.3 Training and Support

- 5.1.1 Solutions

- 5.2 By Deployment

- 5.2.1 On-premise

- 5.2.2 Cloud

- 5.2.3 Hybrid

- 5.3 By Threat-Intelligence Type

- 5.3.1 Strategic

- 5.3.2 Tactical

- 5.3.3 Operational

- 5.3.4 Technical

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium-Sized Enterprises

- 5.5 By End-user Industry

- 5.5.1 BFSI

- 5.5.2 IT and Telecommunications

- 5.5.3 Retail and E-commerce

- 5.5.4 Manufacturing

- 5.5.5 Healthcare and Life Sciences

- 5.5.6 Government and Defense

- 5.5.7 Energy and Utilities

- 5.5.8 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Peru

- 5.6.2.5 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.4.5 Australia

- 5.6.4.6 New Zealand

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Rest of Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Strategic Developments

- 6.2 Vendor Positioning Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.3.1 IBM Corporation

- 6.3.2 Cisco Systems Inc.

- 6.3.3 Dell Technologies Inc.

- 6.3.4 CrowdStrike Holdings Inc.

- 6.3.5 Check Point Software Technologies Ltd.

- 6.3.6 Trend Micro Incorporated

- 6.3.7 Palo Alto Networks Inc.

- 6.3.8 Fortinet Inc.

- 6.3.9 Rapid7 Inc.

- 6.3.10 Secureworks Inc.

- 6.3.11 FireEye - Trellix

- 6.3.12 Recorded Future Inc.

- 6.3.13 Anomali Inc.

- 6.3.14 LookingGlass Cyber Solutions Inc.

- 6.3.15 LogRhythm Inc.

- 6.3.16 McAfee LLC

- 6.3.17 Broadcom Inc. (Symantec)

- 6.3.18 Juniper Networks Inc.

- 6.3.19 F-Secure Corporation

- 6.3.20 SentinelOne Inc.

- 6.3.21 Microsoft Corp. (Defender Threat Intelligence)

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

人工智慧語意智慧市場預測至2034年:按組件、部署模式、技術、應用、最終用戶和地區分類的全球分析人工智慧驅動的威脅情報市場預測至2034年:按組件、安全類型、部署模式、組織規模、最終用戶和地區分類的全球分析

人工智慧語意智慧市場預測至2034年:按組件、部署模式、技術、應用、最終用戶和地區分類的全球分析人工智慧驅動的威脅情報市場預測至2034年:按組件、安全類型、部署模式、組織規模、最終用戶和地區分類的全球分析 威脅建模工具:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年)

威脅建模工具:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年) 威脅建模工具市場規模、佔有率和趨勢分析報告:按組件、部署類型、企業規模、行業、地區和細分市場預測(2026-2033 年)

威脅建模工具市場規模、佔有率和趨勢分析報告:按組件、部署類型、企業規模、行業、地區和細分市場預測(2026-2033 年) 威脅情報市場:依組件、威脅情報類型、應用、部署模式和組織規模分類-2026年至2032年全球市場預測威脅建模工具市場:按組件、部署模式、用例、組織規模和產業分類-2026-2032年全球市場預測

威脅情報市場:依組件、威脅情報類型、應用、部署模式和組織規模分類-2026年至2032年全球市場預測威脅建模工具市場:按組件、部署模式、用例、組織規模和產業分類-2026-2032年全球市場預測 威脅建模工具市場分析及預測(至 2035 年):類型、產品類型、服務、技術、組件、應用、部署模式、最終用戶、功能、解決方案威脅情報市場分析及預測(至 2035 年):類型、產品類型、服務、技術、組件、應用、部署模式、最終用戶、解決方案、交付模式

威脅建模工具市場分析及預測(至 2035 年):類型、產品類型、服務、技術、組件、應用、部署模式、最終用戶、功能、解決方案威脅情報市場分析及預測(至 2035 年):類型、產品類型、服務、技術、組件、應用、部署模式、最終用戶、解決方案、交付模式 2026年全球威脅欺騙平台市場報告2026年全球人工智慧驅動威脅情報市場報告

2026年全球威脅欺騙平台市場報告2026年全球人工智慧驅動威脅情報市場報告