|

市場調查報告書

商品編碼

2066514

基因合成:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Gene Synthesis - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

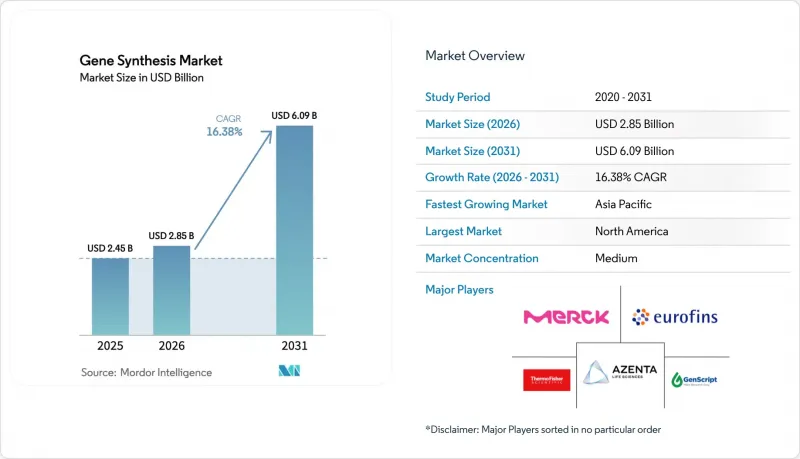

據 Mordor Intelligence 稱,2025 年基因合成市值為 24.5 億美元,預計到 2031 年將達到 60.9 億美元,而 2026 年為 28.5 億美元,預測期(2026-2031 年)的複合年成長率為 16.38%。

本報告按合成方法(化學寡核苷酸合成和基因組裝[PCR介導和連接介導])、服務類型(抗體DNA合成等)、應用(基因和細胞療法開發等)、最終用戶(生物製藥公司等)以及地區(北美、歐洲、亞太等)進行細分。市場規模和預測均以美元計價。

全球基因合成市場趨勢與洞察

基因組學和新一代定序技術推動開發平臺激增。

目前,北美已有超過900項正在進行的臨床試驗使用合成DNA構建體,凸顯了次世代定序(NGS)技術如何推動實驗室對更高通量建構能力的需求。流行病防範創新聯盟(CEPI)已撥款470萬美元用於DNA Script公司模板生產的自動化,使疫苗研發人員能夠在幾天內而非幾週內完成從設計到實驗的過渡。學術界的進展也進一步推動了這個趨勢。夏威夷大學的研究人員使用高保真模板實現了96%的編輯成功率,證明了合成DNA品質與治療效果之間存在直接關聯。此外,美國國家人類基因組研究所(NHGRI)提供的220萬美元津貼用於多寡核苷酸合成,進一步鞏固了合成DNA作為關鍵研究基礎設施的地位。這些因素共同導致了日益成長的樣本積壓,並為能夠按需保證無錯測序的供應商創造了極具吸引力的商業機會。

生物製藥領域對合成基因的需求不斷成長

目前,生物製藥研發管線主要依賴細胞療法、mRNA疫苗和用於抗體藥物複合體(ADC)的客製化基因。美國食品藥物管理局(FDA)在2024年批准了五種基因治療方法,其中包括首個CRISPR基因編輯治療方法,這些療法都凸顯了對高精度、與病毒載體相容的插入片段的商業性需求。葛蘭素史克(GSK)向Elegen投資3,500萬美元,以獲取適用於其mRNA疫苗組合的線性DNA。在臨床試驗中, 鐮狀使93.5%的鐮狀細胞病患者避免了嚴重的血管閉塞危象,這表明精確的模板設計是治療成功的關鍵。投資者情緒也反映了這一需求,Constructive Bio公司在A輪資金籌措中籌集了5,800萬美元,因為合成基因組學有望緩解全球胜肽藥物短缺的問題。這些進展正在縮短研發週期,同時也加劇了對可靠合成合作夥伴的競爭。

熟練的合成生物學家短缺

合成生物學是一個融合了分子生物學、工程學和計算科學的領域,然而許多學術課程仍然強調傳統的濕實驗室技能。美國國家人類基因組研究所(NHGRI)已撥款525萬美元用於促進人才多樣性,顯示人才短缺問題已獲得機構層級的認可。歐洲生技產業對GDP的貢獻高達310億歐元,但目前已面臨人才瓶頸,阻礙了新創企業的規模化發展。與美國相比,日本的創業融資仍然較低,部分原因是其創業人才儲備有限。與磷基化學相比,酵素平台需要一套全新的技能,因此持續的再培訓至關重要。如果沒有足夠的合格人員,生產線運轉率可能會降低,進而可能減緩基因合成市場的成長。

細分市場分析

由於數十年的製程最佳化和可靠的供應鏈,化學寡核苷酸合成在2025年仍將佔據基因合成市場54.82%的佔有率。對於短鏈合成,固相亞磷醯胺反應仍然是標準方法,而基於微晶片的方法則提高了批量處理能力。然而,基因合成市場正在經歷一場變革,預計到2031年,組裝技術將以17.06%的複合年成長率成長,這主要受CRISPR和病毒載體中對更長構建體的需求不斷成長的推動。

DNA Script公司的SYNTAX等酵素平台可在數小時內產生多達96個寡核苷酸,無需使用有毒溶劑即可立即供實驗室使用。 Molecular Assemblies公司的全酶流技術在延長讀取長度的同時,進一步降低了錯誤率,使其有望挑戰現有方法。目前,結合化學合成(用於短引子)和酶促組裝(用於長基因)的混合策略正在湧現,可以肯定的是,基因合成市場將繼續多元化發展,而不是趨向於單一技術。

預計到2025年,抗體DNA合成將占基因合成市場規模的47.76%,主要得益於抗體藥物複合體(ADC)研發管線的不斷擴充以及人們對CAR-T細胞療法日益成長的興趣。病毒基因合成預計將以17.06%的複合年成長率成長,因為mRNA平台和病毒載體在疫苗和基因治療領域佔據主導地位。

CEPI對自動化模板製造的資助凸顯了縮短疫苗研發週期的策略緊迫性。強生公司和金斯瑞公司在已通過核准的CAR-T療法上的合作,正是專有抗體序列如何帶來持續訂單的絕佳例子。能夠提供序列設計、酶合成和基於人工智慧的最佳化等服務供應商,有望獲得高價值契約,並為基因合成市場的收入成長做出貢獻。

區域分析

預計到2025年,北美將佔據基因合成市場規模的41.88%,這主要得益於大量創業投資的湧入、成熟的生物製藥產業叢集以及有利的法規環境。美國國家人類基因組研究所(NHGRI)每年向平台技術投入150萬美元,促進了公私合營,而美國食品藥物管理局(FDA)協調一致的基因治療審查流程則降低了監管方面的不確定性。私人企業也對這些政策充滿信心,例如賽默飛世爾科技(Thermo Fisher)計劃投資20億美元,以期在2028年前擴大其國內產能。

預計到2031年,亞太地區基因合成市場將以17.29%的複合年成長率成長,成為成長最快的地區。中國已將生物技術定位為戰略支柱,並大力投資合成遺傳學企業。印度的「BioE3」政策優先發展精準生物製藥,並致力於扶持本土生物製藥企業服務全球客戶。日本計劃在2028年將私人藥物研發投資加倍,而誘導多功能細胞(iPS細胞)計畫正在尋求長鏈合成序列。韓國在細胞治療領域的努力也進一步推動了該地區的發展動能。

歐洲持續保持穩健成長的驅動力,歐盟生物經濟戰略等協調一致的政策框架推動了工業生物技術的發展。 SYNBEE津貼支持新創公司將人工智慧與 DNA 設計相結合,而歐洲製藥巨頭也獲得了源源不絕的訂單。中東、非洲和南美洲尚處於基因合成引進週期的早期階段,但由於醫療保健支出不斷增加以及對農業生物技術的需求日益成長,基因合成市場的潛在基本客群正在擴大。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 快速發展的基因組學和新一代定序主導的開發平臺

- 生物製藥領域對合成基因的需求日益成長。

- 政府對基因組研究的資助政策

- DNA合成成本大幅降低,前置作業時間縮短

- 一種新型的基於酵素的DNA合成平台

- 大量創業投資湧入生物鑄造廠和雲端實驗室。

- 市場限制因素

- 合成生物學領域熟練人才短缺

- 大型合成設備的高昂資本投資成本

- 關於De Novo結構相關智慧財產權所有權的不確定性

- 生物安全和兩用性方面的監管審查

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 透過合成方法

- 化學寡核苷酸合成

- 固相亞磷醯胺法

- 基於微晶片的寡核苷酸合成

- 基因組裝

- PCR

- 連接介導

- 化學寡核苷酸合成

- 按服務類型

- 抗體DNA合成

- 病毒基因合成

- 其他

- 透過使用

- 基因和細胞治療的發展趨勢

- 疫苗研發

- 疾病診斷

- 其他

- 最終用戶

- 生物製藥公司

- 學術機構及政府機構

- CRO 和 CDMO

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他亞太國家

- 中東和非洲

- GCC

- 南非

- 其他中東和非洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 市佔率分析

- 公司簡介

- ATUM(DNA2.0 Inc.)

- Bio Basic Inc.

- Beijing SBS Genetech Co.

- Eurofins Genomics

- Azenta Life Sciences(Genewiz)

- GenScript Biotech

- Merck KGaA(Sigma GeneArts)

- OriGene Technologies

- Thermo Fisher Scientific(GeneArt)

- Integrated DNA Technologies

- Twist Bioscience

- DNA Script

- Ansa Biotechnologies

- Evonetix

- Telesis Bio

- Synbio Technologies

- Bioneer

- ProteoGenix

- Bio-Synthesis Inc.

- ATLATL Innovations

第7章 市場機會與未來展望

According to Mordor Intelligence, the gene synthesis market size was valued at USD 2.45 billion in 2025 and is estimated to grow from USD 2.85 billion in 2026 to reach USD 6.09 billion by 2031, at a CAGR of 16.38% during the forecast period (2026-2031).

This report is Segmented by Synthesis Method (Chemical Oligonucleotide Synthesis and Gene Assembly[PCR-Mediated and Ligation-Mediated), Service Type (Antibody DNA Synthesis and More), Application (Gene and Cell Therapy Developments and More), End User (Biopharmaceutical Companies and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market and Forecasts are Provided in Terms of Value (USD).

Global Gene Synthesis Market Trends and Insights

Surging Genomics & NGS-Driven R&D Pipelines

More than 900 active clinical trials in North America now incorporate synthetic DNA constructs, underscoring how next-generation sequencing pushes laboratories toward higher-throughput build capabilities. CEPI has committed USD 4.7 million to automate DNA Script's template production so vaccine developers can move from design to bench in days rather than weeks . Academic progress supports the driver: University of Hawaii researchers achieved 96% editing success when using high-fidelity templates, demonstrating direct links between synthesis quality and therapeutic efficacy . NHGRI's USD 2.2 million grant for multiplex oligo synthesis further embeds synthetic DNA as critical research infrastructure. Together, these elements enlarge sample backlogs and create premium opportunities for providers able to guarantee error-free sequences on demand.

Expanding Biopharma Demand for Synthetic Genes

Biopharmaceutical pipelines now depend on custom genes for cell therapies, mRNA vaccines, and antibody-drug conjugates. The FDA cleared five gene therapies in 2024, including the first CRISPR-edited treatment, and each approval validates commercial need for precise, viral-vector-ready inserts. GSK invested USD 35 million in Elegen to secure linear DNA that fits its mRNA vaccine portfolio. Clinically, Casgevy prevented severe vaso-occlusive crises in 93.5% of treated sickle-cell patients, proving that accurate template design translates into therapeutic success. Investor sentiment mirrors demand; Constructive Bio attracted USD 58 million in Series A funding as synthetic genomics promises to ease global peptide shortages. These developments shorten development timelines and intensify competition for trustworthy synthesis partners.

Scarcity of Skilled Synthetic-Biology Workforce

Synthetic biology blends molecular biology, engineering, and computation, yet most academic curricula still emphasize traditional wet-lab skills. NHGRI earmarked USD 5.25 million to boost workforce diversity, signalling institutional recognition of the shortage. European biotechnology contributes EUR 31 billion to GDP but already suffers talent bottlenecks that curtail start-up scaling. Japan's venture funding remains low relative to the United States, partly because of limited entrepreneurial depth. Continuous retraining is essential because enzymatic platforms require new skill sets compared with phosphorus-based chemistry. Without enough qualified staff, production lines risk under-utilization, slowing revenue accrual for the gene synthesis market.

Other drivers and restraints analyzed in the detailed report include:

- Government Genomics-Funding Initiatives

- Rapid Drop in DNA-Synthesis Cost & Turnaround

- High Capital Cost for Large-Scale Synthesis Capacity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Chemical oligonucleotide synthesis retained 54.82% gene synthesis market share in 2025 thanks to decades of process optimization and reliable supply chains. Solid-phase phosphoramidite reactions remain standard for short strands, and microchip-based approaches improve batch throughput. Yet the gene synthesis market is pivoting as assembly technologies post a 17.06% CAGR through 2031, propelled by the need for longer constructs in CRISPR and viral vectors.

Enzymatic platforms such as DNA Script's SYNTAX produce up to 96 oligos within hours, offering laboratories instant access without toxic solvents. Molecular Assemblies' fully enzymatic flow technology further reduces error rates while extending read length, positioning it to steal share from incumbent methods. Hybrid strategies that combine chemical speed for short primers with enzymatic assembly for long genes are emerging, ensuring the gene synthesis market continues to diversify rather than converge on a single technique.

Antibody DNA synthesis contributed 47.76% of the gene synthesis market size in 2025 because of rising antibody-drug conjugate pipelines and CAR-T cell interest. Viral gene synthesis is set for a 17.06% CAGR as mRNA platforms and viral vectors dominate vaccine and gene-therapy arenas.

CEPI funding of automated template production confirmed strategic urgency to shorten vaccine R&D cycles. Johnson & Johnson's collaboration with GenScript on approved CAR-T therapies exemplifies how proprietary antibody sequences generate recurring orders. Service providers capable of bundling sequence design, enzymatic synthesis, and AI-based optimization stand to capture premium contracts, expanding overall revenue for the gene synthesis market.

Geography Analysis

North America commanded 41.88% of the gene synthesis market size in 2025 because of strong venture capital flows, mature biopharmaceutical clusters, and supportive regulation. The NHGRI's USD 1.5 million annual commitment to platform technologies fosters public-private partnerships, while the FDA's coordinated gene-therapy review pathway removes regulatory uncertainty. Private firms mirror policy confidence; Thermo Fisher is spending USD 2 billion on domestic capacity expansions through 2028.

Asia-Pacific is projected to log a 17.29% CAGR through 2031 and is the fastest-growing region in the gene synthesis market. China classifies biotechnology as a strategic pillar and channels generous subsidies into synthetic genetics ventures. India's BioE3 policy prioritizes precision biotherapeutics and positions local biofoundries to serve global clients. Japan plans to double private drug-discovery investment by 2028, with induced pluripotent stem-cell projects demanding long synthetic sequences. South Korea's cell-therapy initiatives further reinforce regional momentum.

Europe remains a steady growth contributor as coordinated policy frameworks such as the EU Bioeconomy Strategy back industrial biotechnology. SYNBEE grants help startups combine AI and DNA design, while the continent's pharmaceutical giants deliver consistent order volumes. Middle East and Africa along with South America are early in adoption cycles, yet rising healthcare spending and agricultural biotech needs are widening the addressable base for the gene synthesis market.

- ATUM

- Bio Basic

- Beijing SBS Genetech Co.

- Eurofins

- Azenta Life Sciences (Genewiz)

- GenScript Biotech

- Merck KGaA (Sigma GeneArts)

- OriGene Technologies

- Thermo Fisher Scientific (GeneArt)

- Integrated DNA Technologies

- Twist Bioscience

- DNA Script

- Ansa Biotechnologies

- Evonetix

- Telesis Bio

- Synbio Technologies

- Bioneer

- ProteoGenix

- Bio-Synthesis

- ATLATL Innovations

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging genomics & NGS-driven R&D pipelines

- 4.2.2 Expanding biopharma demand for synthetic genes

- 4.2.3 Government genomics-funding initiatives

- 4.2.4 Rapid drop in DNA-synthesis cost & turnaround

- 4.2.5 Emerging enzymatic DNA-synthesis platforms

- 4.2.6 Venture-capital rush into bio-foundries & cloud labs

- 4.3 Market Restraints

- 4.3.1 Scarcity of skilled synthetic-biology workforce

- 4.3.2 High capital cost for large-scale synthesis capacity

- 4.3.3 IP-ownership uncertainty for de-novo constructs

- 4.3.4 Biosecurity & dual-use regulatory scrutiny

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porters Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Synthesis Method

- 5.1.1 Chemical Oligonucleotide Synthesis

- 5.1.1.1 Solid-Phase Phosphoramidite

- 5.1.1.2 Microchip-based Oligonucleotide Synthesis

- 5.1.2 Gene Assembly

- 5.1.2.1 PCR-mediated

- 5.1.2.2 Ligation-mediated

- 5.1.1 Chemical Oligonucleotide Synthesis

- 5.2 By Service Type

- 5.2.1 Antibody DNA Synthesis

- 5.2.2 Viral Gene Synthesis

- 5.2.3 Others

- 5.3 By Application

- 5.3.1 Gene and Cell Therapy Developments

- 5.3.2 Vaccine Development

- 5.3.3 Disease Diagnosis

- 5.3.4 Others

- 5.4 By End User

- 5.4.1 Biopharmaceutical Companies

- 5.4.2 Academic & Government Institutes

- 5.4.3 CROs and CDMOs

- 5.4.4 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 ATUM (DNA2.0 Inc.)

- 6.3.2 Bio Basic Inc.

- 6.3.3 Beijing SBS Genetech Co.

- 6.3.4 Eurofins Genomics

- 6.3.5 Azenta Life Sciences (Genewiz)

- 6.3.6 GenScript Biotech

- 6.3.7 Merck KGaA (Sigma GeneArts)

- 6.3.8 OriGene Technologies

- 6.3.9 Thermo Fisher Scientific (GeneArt)

- 6.3.10 Integrated DNA Technologies

- 6.3.11 Twist Bioscience

- 6.3.12 DNA Script

- 6.3.13 Ansa Biotechnologies

- 6.3.14 Evonetix

- 6.3.15 Telesis Bio

- 6.3.16 Synbio Technologies

- 6.3.17 Bioneer

- 6.3.18 ProteoGenix

- 6.3.19 Bio-Synthesis Inc.

- 6.3.20 ATLATL Innovations

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

基因合成市場:全球市場預測(2026-2032)

基因合成市場:全球市場預測(2026-2032) 2026-2035 年魚貝類和肉類DNA 條碼認證的市場機會、成長要素、產業趨勢和預測。

2026-2035 年魚貝類和肉類DNA 條碼認證的市場機會、成長要素、產業趨勢和預測。 DNA條碼服務市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、方法、應用、最終用途、地區和競爭格局分類,2021-2031年

DNA條碼服務市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、方法、應用、最終用途、地區和競爭格局分類,2021-2031年 基因合成市場:按產品類型、應用、技術和地區分類

基因合成市場:按產品類型、應用、技術和地區分類 DNA與RNA合成研究綜述:2025年

DNA與RNA合成研究綜述:2025年 蛋白質合成研究綜述:2025

蛋白質合成研究綜述:2025 基因合成市場報告:趨勢、預測與競爭分析(至2035年)酵素DNA合成市場:依產品、技術、應用和最終用戶分類-2026年至2032年全球市場預測

基因合成市場報告:趨勢、預測與競爭分析(至2035年)酵素DNA合成市場:依產品、技術、應用和最終用戶分類-2026年至2032年全球市場預測 DNA條碼服務市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、最終用戶、流程、解決方案和階段分類高通量DNA合成市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、形式、最終用戶及製程分類

DNA條碼服務市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、最終用戶、流程、解決方案和階段分類高通量DNA合成市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、形式、最終用戶及製程分類