|

市場調查報告書

商品編碼

2066512

美國有機肥料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)United States Organic Fertilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

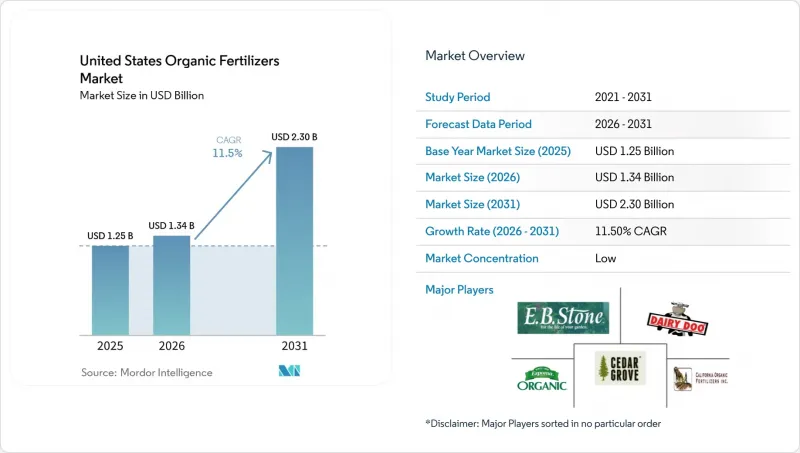

根據 Mordor Intelligence 預測,美國有機肥料市場規模將從 2025 年的 12.5 億美元成長到 2026 年的 13.4 億美元,到 2031 年達到 23 億美元,2026 年至 2031 年的複合年成長率為 11.5%。

本報告按形態(堆肥、穀粉肥料等)和作物類型(經濟作物、園藝作物等)分類。市場預測以貨幣價值(美元)和數量(公噸)兩種形式呈現。

美國有機肥料市場的趨勢與洞察

經認證的有機農地迅速擴張

根據美國農業部的數據,儘管受天氣影響導致認證延遲,但津貼的技術支援正在加速農地向有機農業的轉型。這項耗資3億美元的「有機轉型舉措」涵蓋高達75%的檢驗和審核費用,使中型農場以及已在有機材料審查協會(OMRI)註冊的農場都能負擔得起。新發布的有機進口協調關稅制度(HTS)編碼透過加強可追溯性法規和減少不公平競爭,間接惠及國內生產商。隨著每英畝農地逐步達到合規標準,禁止使用合成氮肥的政策將增加美國有機肥料市場的基本需求,從而促成多年採購協議的簽訂。

消費者對不使用化學品種植的農產品的需求日益成長。

據有機貿易協會 (OTA) 稱,儘管通貨膨脹給家庭預算帶來壓力,但2024年有機產品銷售額仍達到716億美元,比上年成長5.2%。如今,零售合約要求全年供應有機產品,迫使生產商確保獲得符合美國國家有機計劃 (NOP) 標準的可靠營養來源。有機產品的價格仍比傳統產品高出20%至50%,這使得農民能夠在不影響利潤率的情況下承擔更高的每英畝成本。這種強勁的消費需求使得化肥需求更受到消費者情緒而非商品週期的影響,從而保護了美國有機肥料市場免受全球合成肥料價格波動的影響。

與合成肥料相比,養分密度較低

典型的有機肥配方中氮磷鉀比例低於5-5-5,需要施用量是合成氮肥的10到15倍才能達到相同的效果。這增加了物流成本和勞動力負擔,尤其是在播種季節較短的時期。高濃度產品,例如血粉,可以提高施肥效率,但其零售價格是尿素的3到5倍,因此僅限於高階農場使用。在經濟高效的濃縮技術普及之前,這種濃度差距可能會阻礙美國有機肥料市場的整體成長。

細分市場分析

預計到2025年,畜禽糞便衍生產品將在美國有機肥料市場佔據46.9%的市場佔有率,並有望保持主導地位,在2026年至2031年間實現12.5%的最高複合年成長率。畜禽糞便營養密度低、有機質含量高,符合再生農業的標準,是土壤健康計畫的重要投入。為了解決運輸成本問題,生產商正在將畜禽糞便製成顆粒,這既能略微提高密度,又能維持有機材料評審協會(OMRI)的認證。

飼料粕基肥料、油籽粕和混合堆肥產品在零售市場中佔據主導地位。然而,飼料成本的上漲限制了原料的供應,並推高了價格上限。油籽粕產品因其關鍵營養成分比例均衡而受到蔬菜種植者的青睞,但其供應取決於油廠的特定產品產量,並受生質燃料需求波動的影響。添加了生物炭和微生物接種劑的專用堆肥混合物旨在滿足排碳權標準,進一步豐富了美國有機肥料市場。隨著對污染物監管力度的加大,垂直整合供應鏈的可追溯性優勢正在增強那些已在市場中佔據穩固地位的公司的競爭優勢。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

- 調查方法

第2章:執行摘要和主要發現

第3章:本報告的內容

第4章:主要產業趨勢

- 有機耕作面積

- 人均有機產品支出

- 法律規範

- 價值鍊和通路分析

- 市場促進因素

- 經認證的有機農地迅速擴張

- 消費者對不使用化學品種植的農產品的需求日益成長。

- 聯邦政府為農業企業轉型提供成本分擔激勵措施

- 擴大有機畜牧業經營

- 透過堆肥利用實現排碳權貨幣化

- 各州正在實施推薦使用有機土壤改良劑的土壤健康法規。

- 市場限制因素

- 有限營養密度與合成替代品的比較

- 原物料供應價格波動

- 緩釋特性不適用於某些經濟作物。

- 各州對病原體的嚴格監管增加了合規成本。

第5章 市場規模與成長預測

- 按形式

- 堆肥

- 粉狀肥料

- 油籽粕

- 其他有機肥料

- 按作物類型

- 經濟作物

- 園藝作物

- 一排作品

第6章 競爭情勢

- 關鍵策略趨勢

- 市佔率分析

- 公司簡介

- Cedar Grove Composting Inc.

- EB Stone & Son Inc.

- The Espoma Company

- California Organic Fertilizers Inc.

- Morgan Composting Inc.

- Atlas Organics(Generate Upcycle)

- Sustane Natural Fertilizer Inc.

- Cascade Agronomics LLC

- The Richlawn Company LLC

- Walts Organic Fertilizers Co.

- Darling Ingredients(Nature Safe)

- Midwestern BioAg

- BioFlora

- Perfect Blend LLC

- Synagro Technologies, Inc.

第7章 農業生物技術領域執行長面臨的關鍵策略挑戰

According to Mordor Intelligence, the united states organic fertilizers market size is anticipated to increase from USD 1.25 billion in 2025 to USD 1.34 billion in 2026 and reach USD 2.30 billion by 2031, growing at a CAGR of 11.5% over 2026-2031.

This report is Segmented by Form (Manure, Meal-Based Fertilizers, and More) and by Crop Type (Cash Crops, Horticultural Crops, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

United States Organic Fertilizers Market Trends and Insights

Rapid Growth of Certified Organic Farmland

United States Department of Agriculture data confirm that grant-funded technical support is accelerating acreage conversion despite weather-related certification backlogs. The USD 300 million Organic Transition Initiative covers up to 75% of testing and audit fees, making Organic Materials Review Institute-listed inputs financially accessible for midsize farms. Newly issued Harmonized Tariff Schedule codes for organic imports tighten traceability rules, which indirectly benefit domestic growers by reducing fraudulent competition. As each acre enters compliance, baseline demand for the United States organic fertilizers market rises because synthetic nitrogen is prohibited, locking in multi-year purchasing commitments.

Rising Consumer Demand for Chemical-Free Produce

The Organic Trade Association reported a 5.2% year-over-year sales increase to USD 71.6 billion in 2024, even as inflation constrained household budgets Retail contracts now require year-round organic supply, forcing growers to secure reliable nutrient sources that meet National Organic Program standards. Because price premiums remain 20%-50% over conventional equivalents, farmers can absorb the higher per-acre cost of organic products without eroding margins. This spending resilience ties fertilizer demand more tightly to consumer sentiment than to commodity cycles, insulating the United States organic fertilizers market from global synthetic price swings.

Limited Nutrient Density Versus Synthetic Alternatives

Typical organic formulations offer NPK ratios under 5-5-5, forcing 10-15 times greater application volumes to match synthetic nitrogen delivery. The logistics burden inflates hauling costs and strains labor during tight planting windows. Higher-density options such as blood meal improve efficiency but retail for three to five times the cost of urea, restricting adoption to premium operations. Until cost-effective concentration technologies scale, density gaps will moderate growth across the United States organic fertilizers market.

Other drivers and restraints analyzed in the detailed report include:

- Federal Cost-Share Incentives for Transitioning Farms

- Expansion of Organic Livestock Operations

- Slow-Release Profile Unsuitable for Certain Cash Crops

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Manure-based products secured the largest United States organic fertilizers market share of 46.9% in 2025 and are projected to maintain their leadership position, registering the fastest CAGR of 12.5% during 2026-2031. Although manure has a low nutrient density, its contribution of organic matter aligns with regenerative agriculture standards, making it a key input for soil health programs. To address transportation costs, producers are pelletizing manure, which slightly increases its density while maintaining Organic Materials Review Institute (OMRI) approval.

Meal-based fertilizers, oilcakes, and blended compost products occupy premium positions in the retail market. However, rising feed costs are limiting raw material availability and pushing price ceilings higher. Oilcake products offer balanced macronutrient ratios and appeal to vegetable growers, but their supply depends on byproduct volumes from crush plants, which are influenced by fluctuations in biofuel demand. Specialty compost blends, incorporating biochar and microbial inoculants, are designed to meet carbon-credit protocols, further diversifying the organic fertilizer market in the United States. As regulatory scrutiny on contaminants increases, the traceability benefits of vertically integrated supply chains enhance the competitive advantage of established market players.

List of Companies Covered in this Report:

- Cedar Grove Composting Inc.

- EB Stone & Son Inc.

- The Espoma Company

- California Organic Fertilizers Inc.

- Morgan Composting Inc.

- Atlas Organics (Generate Upcycle)

- Sustane Natural Fertilizer Inc.

- Cascade Agronomics LLC

- The Richlawn Company LLC

- Walts Organic Fertilizers Co.

- Darling Ingredients (Nature Safe)

- Midwestern BioAg

- BioFlora

- Perfect Blend LLC

- Synagro Technologies, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 EXECUTIVE SUMMARY AND KEY FINDINGS

3 REPORT OFFERS

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Organic Cultivation

- 4.2 Per Capita Spending on Organic Products

- 4.3 Regulatory Framework

- 4.4 Value Chain and Distribution Channel Analysis

- 4.5 Market Drivers

- 4.5.1 Rapid growth of certified organic farmland

- 4.5.2 Rising consumer demand for chemical-free produce

- 4.5.3 Federal cost-share incentives for transitioning farms

- 4.5.4 Expansion of organic livestock operations

- 4.5.5 Carbon-credit monetization for compost use

- 4.5.6 Emerging state soil-health mandates favoring organic amendments

- 4.6 Market Restraints

- 4.6.1 Limited nutrient density versus synthetic alternatives

- 4.6.2 Volatility in feedstock supply prices

- 4.6.3 Slow-release profile unsuitable for certain cash crops

- 4.6.4 Stringent state-level pathogen regulations increasing compliance costs

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Form

- 5.1.1 Manure

- 5.1.2 Meal-Based Fertilizers

- 5.1.3 Oilcakes

- 5.1.4 Other Organic Fertilizer

- 5.2 By Crop Type

- 5.2.1 Cash Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Row Crops

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.3.1 Cedar Grove Composting Inc.

- 6.3.2 EB Stone & Son Inc.

- 6.3.3 The Espoma Company

- 6.3.4 California Organic Fertilizers Inc.

- 6.3.5 Morgan Composting Inc.

- 6.3.6 Atlas Organics (Generate Upcycle)

- 6.3.7 Sustane Natural Fertilizer Inc.

- 6.3.8 Cascade Agronomics LLC

- 6.3.9 The Richlawn Company LLC

- 6.3.10 Walts Organic Fertilizers Co.

- 6.3.11 Darling Ingredients (Nature Safe)

- 6.3.12 Midwestern BioAg

- 6.3.13 BioFlora

- 6.3.14 Perfect Blend LLC

- 6.3.15 Synagro Technologies, Inc.

7 KEY STRATEGIC QUESTIONS FOR AGRICULTURAL BIOLOGICAL CEOS

有機肥料市場:2026-2032年全球市場預測(依配方、產品形式、原料、應用、最終用戶及銷售管道分類)

有機肥料市場:2026-2032年全球市場預測(依配方、產品形式、原料、應用、最終用戶及銷售管道分類) 有機肥料市場:依原料、形態、應用和地區分類有機農藥市場:2026-2032年全球市場預測(依產品類型、作物類型、配方、應用及通路分類)

有機肥料市場:依原料、形態、應用和地區分類有機農藥市場:2026-2032年全球市場預測(依產品類型、作物類型、配方、應用及通路分類) 2026年全球有機肥料市場報告2026年全球綠肥市場報告

2026年全球有機肥料市場報告2026年全球綠肥市場報告 全球有機肥料市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球有機肥料市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 北美有機肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)富磷有機肥市場:依作物類型、形態、應用通路-2026-2032年全球預測

北美有機肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)富磷有機肥市場:依作物類型、形態、應用通路-2026-2032年全球預測 全球有機肥料市場:市場規模、佔有率和趨勢分析(按產品、形態、應用和地區分類),細分市場預測(2026-2033 年)全球有機農藥市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球有機肥料市場:市場規模、佔有率和趨勢分析(按產品、形態、應用和地區分類),細分市場預測(2026-2033 年)全球有機農藥市場規模、佔有率、趨勢和成長分析報告(2026-2034年)