|

市場調查報告書

商品編碼

2044166

北美有機肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)North America Organic Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

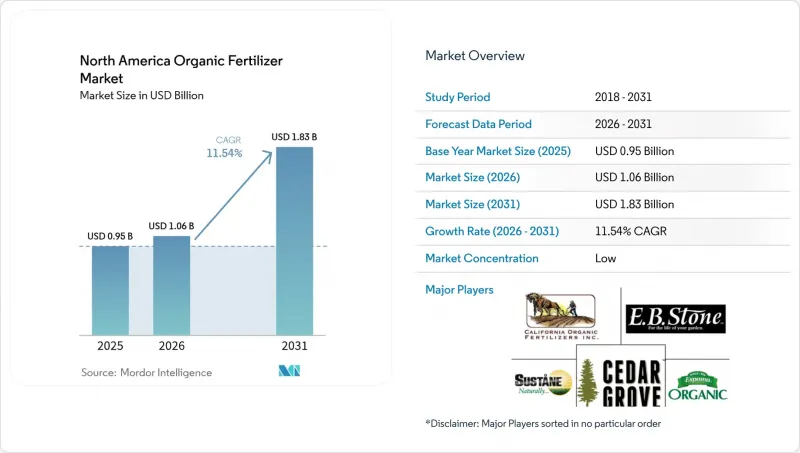

預計北美有機肥料市場將從 2025 年的 9.5 億美元成長到 2026 年的 10.6 億美元,到 2031 年將達到 18.3 億美元,2026 年至 2031 年的複合年成長率為 11.54%。

這一成長主要得益於經認證的有機農田面積擴大、精密農業用液態肥料的普及以及聯邦排碳權計劃(該計劃獎勵畜禽糞便轉化項目)。環境控制農場的快速擴張、強制使用本地食物廢棄物渣以及結合腐植酸和藻類提取物的生物聚合物包覆顆粒的推出,進一步提高了養分利用效率,並加速了市場滲透。政府補貼和私人投資縮短了新肥料和生物加工設施的投資回收期,加強了本地供應鏈,並降低了運輸成本。預計這些因素將使北美有機肥料市場在未來十年保持強勁的需求前景。

北美有機肥料市場的趨勢與洞察

擴大經認證的有機農田

隨著農民從合成肥料轉向美國農業部國家有機計畫 (NOP)核准的有機肥料,有機認證農地的面積持續擴大。加州擁有超過 213 萬英畝的認證農田,預計 2024 年有機產品銷售額將達到 140 億美元。墨西哥目前在全美 32 個州擁有 48,874 家認證生產商,並受益於與加拿大簽訂的等效協議,該協議有效期至 2027 年。每一英畝新增農地都需要使用經有機材料評審協會 (OMRI) 認證的有機肥料,這項要求為北美有機肥料市場的供應商創造了可預測的需求。此外,系統化的標準保護了遵守標準的生產商免受低品質進口產品的衝擊,並有助於維持高價。

精密農業液體噴灑系統促進了低黏度有機肥料的廣泛應用。

在北美,超過60%的壟作作物種植面積採用了可變容量噴灑參與企業、衛星導航和基於雲端的決策工具。這些平台最適合低黏度有機液體肥料,因為這種肥料不易堵塞噴嘴。基於即時土壤檢測數據的精準施肥能夠提高養分利用率,並降低面積收穫面積的成本。由於這些設備已安裝在農場,種植者無需進行大量資本投資即可改用相容的有機肥料,從而加速了北美有機肥料市場的普及。

不同批次營養成分分析結果的差異

有機肥料的氮、磷、鉀含量往往有差異,因為原料的成分會隨季節和加工方法而改變。這種差異使得精準施肥變得困難,延誤了監管核准,並需要進行額外的分析測試,而小規模種植者可能無法負擔這些費用。聯邦和州層級缺乏統一的品質標準,意味著生產商面臨分散的合規要求,這延緩了產品上市,並限制了北美有機肥料市場的規模成長。

細分市場分析

到2025年,由粉料殘渣製成的產品將佔總銷售額的48.50%,成為北美有機肥料市場最大的佔有率。這是因為蒸氣滅菌處理的原料營養成分穩定,符合監管審核標準。加工過程能夠去除病原體並延長保存期限,從而增強經銷商的庫存規劃信心。製造商正在將大豆粕、骨粉和羽毛粉混合,並根據精密農業的處方箋客製化氮釋放曲線。肥料類產品成長最快,複合年成長率達11.76%。這得歸功於市政法規對農場消化殘渣和施肥項目的監管,從而確保了原料的穩定供應。強制通風堆肥和生物炭接種等技術投資正在最大限度地減少異味,加快成熟速度,並縮小與粉料產品之間的品質差距。生物炭顆粒和微藻類粉等新興子類別正吸引高價值園藝企業的小眾需求,這些企業尋求富含碳的土壤改良劑。形態學領域的創新已成為供應商在北美有機肥料市場拓展市場佔有率的主要競爭領域。

在北美有機肥料市場,以粕類產品為主的市場規模預計將持續成長至2031年,這顯示在作物輪作中,該細分市場的重要性日益凸顯,因為可靠性和穩定性比養分密度更為重要。生產商正著力研發易於審核的配方,以減輕有機認證所需的文件負擔。同時,以畜禽糞便為原料的產品線正利用其成本優勢,由於當地畜禽廢棄物資源豐富,原料成本幾乎為零,並有望從排碳權中獲得收益。以楝樹籽和蓖麻籽產品為主導的油籽粕,因其氮釋放緩慢、生長週期長,在特種水果和堅果作物中佔據獨特的市場地位。加州資源回收局(CalRecycle)津貼撥款1.3億美元用於從原料到肥料的基礎設施建設,加工商正不斷擴大產能,從而增加北美有機肥料市場的總供應量。

《北美有機肥料市場報告》按形態(肥料、粕肥、油籽粕)、作物類型(經濟作物、園藝作物、溝施作物)和地區(美國、加拿大、墨西哥)進行細分。市場預測以價值(美元)和數量(噸)表示。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

- 調查方法

第2章:報告徵集

第3章:執行摘要和主要發現

第4章 主要產業趨勢

- 有機耕作面積

- 人均有機產品支出

- 法律規範

- 加拿大

- 墨西哥

- 美國

- 價值鍊和通路分析

- 市場促進因素

- 有機認証取得面積の拡大

- 精密農業液體噴灑系統正在促進低黏度有機肥料的採用。

- 美國農業部的排碳權試點計畫鼓勵將牲畜糞便轉化為肥料的計畫。

- 美國和加拿大受控環境農業(CEA)的快速擴張

- 地方政府強制提供食物廢棄物消化劑,正在創造本地供應來源。

- 含有腐植酸和藻類萃取物的生物聚合物包覆顆粒可提高營養吸收效率。

- 市場限制因素

- 不同批次產品的營養成分分析值有差異。

- 在氣候溫暖的地區,高水分液體的保存期限較短。

- 緩釋特性不適用於短期作物生長條件。

- 某些再生廢物流中的重金屬殘留標準

第5章 市場規模及成長預測(價值及數量)

- 形式

- 肥料

- 酒糟基肥料

- 油籽粕

- 其他

- 作物類型

- 經濟作物

- 園藝作物

- 行栽作物

- 國家

- 加拿大

- 墨西哥

- 美國

- 北美其他地區

第6章 競爭情勢

- 重大策略舉措

- 市佔率分析

- 企業趨勢

- 公司簡介

- Sustane Natural Fertilizer Inc.

- The Espoma Company

- Scotts Miracle-Gro Company

- BioFert Manufacturing Inc.

- California Organic Fertilizers Inc.

- Cascade Agronomics LLC

- Cedar Grove Composting Inc.

- EB Stone and Sons Inc.

- Morgan Composting Inc.

- True Organic Products Inc.

- Nutrien Ag Solutions(Nutrien Ltd.)

- Midwestern BioAg

- Nature Safe(Darling Ingredients Inc.)

- EnviroKure Inc.

- Pacific Biochar Benefit Corporation

第7章 執行長需要思考的關鍵策略問題

The North America organic fertilizer market size is expected to grow from USD 0.95 billion in 2025 to USD 1.06 billion in 2026 and is forecast to reach USD 1.83 billion by 2031 at 11.54% CAGR over 2026-2031.

Growth is fueled by expanding certified organic acreage, wider use of precision-ag liquid applicators, and federal carbon-credit programs that reward manure conversion projects. Rapid scale-up of controlled-environment farms, local food-waste digestate mandates, and the launch of biopolymer-coated granules that pair humic acids with algae extracts are further improving nutrient-use efficiency and driving uptake. Investments from both government grants and private capital shorten payback periods for new composting and bio-processing facilities, which strengthens regional supply chains and keeps freight costs contained. These converging factors sustain a robust demand outlook for the North America organic fertilizer market through the decade.

North America Organic Fertilizer Market Trends and Insights

Expanding Certified Organic Acreage

Certified organic farmland keeps growing as farmers switch from synthetics to inputs approved under the United States Department of Agriculture National Organic Program. California leads with more than 2.13 million certified acres that generated USD 14.0 billion in organic sales during 2024. Mexico now counts 48,874 certified operators spanning all 32 states and benefits from an equivalence agreement with Canada that remains in force until 2027. Every new acre needs Organic Materials Review Institute-listed nutrients, and that requirement funnels predictable demand toward North America organic fertilizer market suppliers. Structured standards also shield compliant producers from lower-grade imports, supporting premium pricing.

Precision-ag Liquid Application Systems Boost Adoption of Low-viscosity Organics

Variable-rate sprayers, satellite guidance, and cloud-based decision tools are used on more than 60% of North American row-crop acres. These platforms work best with low-viscosity organic liquids that move through nozzles without clogging. Real-time soil testing data guide exact placement, which raises nutrient-use efficiency and lowers cost per harvested acre. Because the equipment is already on farms, growers can switch to compatible organics without large capital outlays, accelerating usage within the North America organic fertilizer market.

Inconsistent Nutrient Analysis Across Batches

Organic fertilizers often show variable nitrogen, phosphorus, and potassium content because feedstock composition changes with season and processing method. This inconsistency complicates precision application, slows regulatory approvals, and forces extra laboratory tests that small producers cannot always afford. Without harmonized quality metrics across federal and state lines, manufacturers face fragmented compliance requirements that delay product launches and limit scalable growth for the North America organic fertilizer market.

Other drivers and restraints analyzed in the detailed report include:

- USDA Carbon-credit Pilots Rewarding Manure-to-fertilizer Projects

- Biopolymer-Coated Granules Integrating Humic Acids with Algae Extracts Boost Nutrient Uptake Efficiency

- Short Shelf-life for High-moisture Liquids in Warmer States

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Meal-based products captured 48.50% of total sales in 2025, the largest slice of the North America organic fertilizer market share, because steam-sterilized ingredients yield predictable nutrient profiles that pass regulatory audits. Processing removes pathogens and extends shelf life, giving distributors confidence in inventory planning. Manufacturers blend soybean meal, bone meal, and feather meal to customize nitrogen release curves that align with precision agriculture prescriptions. Manure-based fertilizers are growing fastest at a 11.76% CAGR as municipal digestate rules and on-farm composting projects deliver steady feedstock streams. Technology investments such as forced-air static piles and biochar inoculation minimize odor and speed maturation, closing the quality gap with meals. Emerging sub-categories like biochar-enhanced pellets and micro-algae powders find niche demand among high-value horticulture operators looking for carbon-rich amendments. Innovations across the form segment make it a central battleground for suppliers aiming to raise share in the North America organic fertilizer market.

The North America organic fertilizer market value for meal-based products is expected to grow steadily through 2031, highlighting the segment's increasing importance in row-crop rotations, where reliability and consistency are prioritized over nutrient density. Producers highlight audit-ready formulations that lower documentation burdens under organic certification. In parallel, manure-based lines ride cost advantages where local livestock waste offers negative feedstock costs and carbon-credit upside. Oilcakes, led by neem and castor seed products, maintain niche status for specialty fruit and nut crops because slow nitrogen release matches long growing cycles. Processors continue to expand capacity as CalRecycle grants unlock USD 130 million for feedstock-to-fertilizer infrastructure in California, adding to total supply available to the North America organic fertilizer market.

The North America Organic Fertilizer Market Report is Segmented by Form (Manure, Meal-Based Fertilizers, and Oilcakes), Crop Type (Cash Crops, Horticultural Crops, and Row Crops), and Geography (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

List of Companies Covered in this Report:

- Sustane Natural Fertilizer Inc.

- The Espoma Company

- Scotts Miracle-Gro Company

- BioFert Manufacturing Inc.

- California Organic Fertilizers Inc.

- Cascade Agronomics LLC

- Cedar Grove Composting Inc.

- E.B. Stone and Sons Inc.

- Morgan Composting Inc.

- True Organic Products Inc.

- Nutrien Ag Solutions (Nutrien Ltd.)

- Midwestern BioAg

- Nature Safe (Darling Ingredients Inc.)

- EnviroKure Inc.

- Pacific Biochar Benefit Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Organic Cultivation

- 4.2 Per Capita Spending On Organic Products

- 4.3 Regulatory Framework

- 4.3.1 Canada

- 4.3.2 Mexico

- 4.3.3 United States

- 4.4 Value Chain and Distribution Channel Analysis

- 4.5 Market Drivers

- 4.5.1 Expanding certified organic acreage

- 4.5.2 Precision-ag liquid application systems boost adoption of low-viscosity organics

- 4.5.3 USDA carbon-credit pilots rewarding manure-to-fertilizer projects

- 4.5.4 Rapid scale-up of controlled-environment agriculture (CEA) in the U.S. and Canada

- 4.5.5 Municipal food-waste digestate mandates create local supply pools

- 4.5.6 Biopolymer-coated granules integrating humic acids with algae extracts boost nutrient uptake efficiency

- 4.6 Market Restraints

- 4.6.1 Inconsistent nutrient analysis across batches

- 4.6.2 Short shelf-life for high-moisture liquids in warmer states

- 4.6.3 Slow-release profile mismatched to short-season row crops

- 4.6.4 Persistent heavy-metal limits in some recycled waste streams

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Form

- 5.1.1 Manure

- 5.1.2 Meal Based Fertilizers

- 5.1.3 Oilcakes

- 5.1.4 Other Organic Fertilizer

- 5.2 Crop Type

- 5.2.1 Cash Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Row Crops

- 5.3 Country

- 5.3.1 Canada

- 5.3.2 Mexico

- 5.3.3 United States

- 5.3.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Sustane Natural Fertilizer Inc.

- 6.4.2 The Espoma Company

- 6.4.3 Scotts Miracle-Gro Company

- 6.4.4 BioFert Manufacturing Inc.

- 6.4.5 California Organic Fertilizers Inc.

- 6.4.6 Cascade Agronomics LLC

- 6.4.7 Cedar Grove Composting Inc.

- 6.4.8 E.B. Stone and Sons Inc.

- 6.4.9 Morgan Composting Inc.

- 6.4.10 True Organic Products Inc.

- 6.4.11 Nutrien Ag Solutions (Nutrien Ltd.)

- 6.4.12 Midwestern BioAg

- 6.4.13 Nature Safe (Darling Ingredients Inc.)

- 6.4.14 EnviroKure Inc.

- 6.4.15 Pacific Biochar Benefit Corporation

7 KEY STRATEGIC QUESTIONS FOR AGRICULTURAL BIOLOGICALS CEOS

有機農藥市場-2026-2032年全球市場預測有機肥料市場:2026-2032年全球市場預測(依原料、產品形態、混合、作物類型、應用、最終用戶和銷售管道分類)

有機農藥市場-2026-2032年全球市場預測有機肥料市場:2026-2032年全球市場預測(依原料、產品形態、混合、作物類型、應用、最終用戶和銷售管道分類) 有機堆肥肥料市場機會、成長促進因素、產業趨勢分析及2026-2035年預測。

有機堆肥肥料市場機會、成長促進因素、產業趨勢分析及2026-2035年預測。 美國有機肥料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

美國有機肥料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 有機肥料市場:依原料、形態、應用和地區分類

有機肥料市場:依原料、形態、應用和地區分類 2026年全球有機肥料市場報告2026年全球綠肥市場報告

2026年全球有機肥料市場報告2026年全球綠肥市場報告 全球有機肥料市場規模、佔有率、趨勢和成長分析報告(2026-2034年)富磷有機肥市場:依作物類型、形態、應用通路-2026-2032年全球預測

全球有機肥料市場規模、佔有率、趨勢和成長分析報告(2026-2034年)富磷有機肥市場:依作物類型、形態、應用通路-2026-2032年全球預測 全球有機肥料市場:市場規模、佔有率和趨勢分析(按產品、形態、應用和地區分類),細分市場預測(2026-2033 年)

全球有機肥料市場:市場規模、佔有率和趨勢分析(按產品、形態、應用和地區分類),細分市場預測(2026-2033 年)