|

市場調查報告書

商品編碼

2066491

耐用醫療設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Durable Medical Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

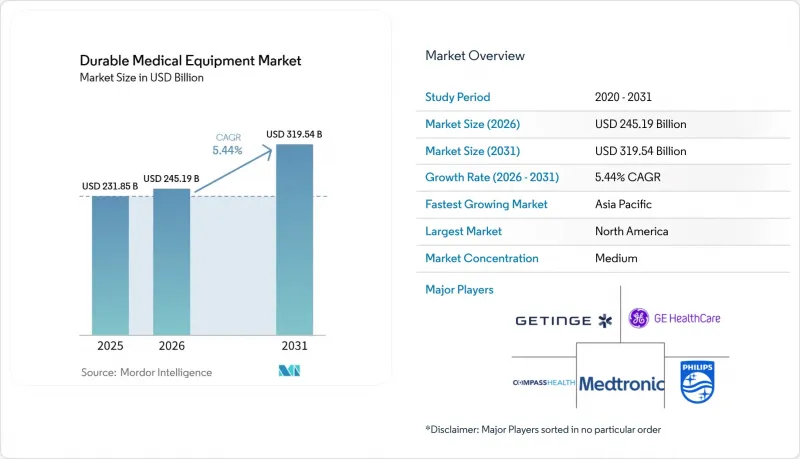

據 Mordor Intelligence 稱,2025 年耐用醫療設備市值為 2318.5 億美元,預計到 2031 年將達到 3195.4 億美元,而 2026 年為 2451.9 億美元,預測期內(2026-2031 年)的複合年成長率為 5.4%。

本報告按設備類型(個人行動輔助設備[輪椅等]、浴室安全設備和醫療家具、監測和治療設備)、最終用戶(醫院、診所等)、分銷管道(醫院和診所藥房等)以及地區(北美、歐洲、亞太地區等)進行細分。市場預測以美元計價。

全球耐用醫療設備市場趨勢及洞察

人口快速老化推動了對行動輔助設備和呼吸照護產品的需求。

在日本,到2025年,75歲及以上人口的比例將超過15%,這將刺激輪椅、助行器和氧氣濃縮機設備的購買,這些設備均可享受長期護理保險體系的補貼,最高補貼額可達設備成本的90%。歐盟統計局預測,到2050年,歐洲65歲及以上人口的比例將達到30%,將促使各國保險公司增加家庭呼吸治療和行動輔助設備的津貼。美國醫療保險和醫療補助服務中心(CMS)預測,到2030年,聯邦醫療保險(Medicare)的用戶人數將增至8000萬,這將擴大電動輪椅和持續氣道正壓通氣(CPAP)系統的潛在基本客群。德國已累計4,500億歐元用於2024年的醫療保健支出,其中越來越多的資金將用於社會保險體系下的輔助技術。 ISO 7176和IEC 60601等安全標準有助於確保提供給老年人的設備符合耐用性和電氣要求,並有助於降低供應商的法律責任。

物聯網設備生態系統正在推動治療依從性的提高和數據貨幣化。

連網血糖值儀、脈動式血氧監測儀系統和攜帶式人工呼吸器正擴大與智慧型手機連接,並將即時測量數據發送到雲端控制面板。雅培的FreeStyle Libre 2 Plus直接將血糖數據發送到Apple Health,讓醫生無需患者就診即可調整藥物劑量。瑞思邁的AirSense 11 CPAP呼吸器可將使用指標即時傳輸給臨床醫生,在2024年的一項多中心研究中,該呼吸器可將阻塞型睡眠呼吸中止症中止症的30天再入院率降低18%。 FDA的TEMPO模式允許突破性的連網型設備在獲得批准後兩天內自動獲得Medicare報銷資格,從而顯著縮短報銷時間並加快產品上市速度。然而,數據標準的不一致正在減緩跨平台分析的速度,因此HL7 FHIR的採用率不斷提高,以實現不同供應商生態系統之間的互通性。

高昂的初始成本和生命週期服務費用

配備物聯網感測器的先進電動輪椅價格在 15,000 美元至 40,000 美元之間,智慧病床的價格在 8,000 美元至 25,000 美元之間,這對第三方報銷有限的預算構成了重大挑戰。預防性保養和軟體更新通常會在五年內使擁有成本增加 20%,導致更換週期延長和停機風險增加。醫療設備技術人員短缺導致成熟市場的服務小時費率居高不下,美國勞工統計局預測到 2032 年,該產業的就業成長率僅為 5%。設備即服務 (EaaS) 供應商提供的訂閱方案透過將成本分攤到每月帳單中,減輕了前期成本的負擔。在歐洲,根據醫療設備法規 (MDR),每兩年一次的上市後監管更新費用在每個產品線 50,000 歐元至 200,000 歐元之間,這部分成本通常會轉嫁給買方。

細分市場分析

到2025年,監測和治療設備將佔據耐用醫療設備市場38.55%的佔有率,預計到2031年將以8.25%的複合年成長率成長,超過行動輔助設備和浴室安全產品。雅培的FreeStyle Libre 2 Plus和德康的Stelo等非處方血糖監測儀,由於無需指尖採血校準且可與行動醫療應用程式同步,在北美市場實現了兩位數的銷量成長。在飛利浦偉康(Philips Respironics)經歷了多年的召回事件後,睡眠呼吸中止症相關產品的需求轉向了瑞思邁(ResMed)。該公司的行動電話網路版AirSense 11在試驗計畫中幫助患者再入院率降低了18%,從而鞏固了其市場地位。

隨著保險公司開始報銷居家醫療計劃中使用的遠距生命徵象監測器的費用,耐用醫療設備監測設備市場規模持續擴大,成長動能依然強勁。然而,由於減肥藥的普及,胰島素幫浦的銷售面臨壓力,迫使幫浦製造商將重點轉向兒童和第一型糖尿病等細分市場。氧氣濃縮機和CPAP系統受益於行動行動醫療連接,實現了對用藥依從性的遠端追蹤。相較之下,個人行動輔助設備的成長速度正在放緩。為了彌補銷售下滑,電動輪椅供應商正透過整合跌倒偵測感測器和姿勢調整演算法,並收集有價值的臨床數據,來加強其在基於價值的醫療保健路徑中的作用。

區域分析

北美仍然是最大的區域市場,預計到2025年將佔據41.13%的市場佔有率,這得益於聯邦醫療保險(Medicare)用戶人數的成長以及美國醫療保險和醫療補助服務中心(CMS)擴大居家醫療報銷範圍的政策。美國食品藥物管理局(FDA)對突破性醫療設備的快速核准縮短了產品上市時間,並加速了物聯網監視器和人工智慧氧氣濃縮機的普及。亞馬遜食品藥物管理局的物流基礎設施支援設備的快速配送,從而促進了線上銷售的成長。同時,加拿大的「輔助設備計畫」為目標產品提供高達75%的津貼,擴大了這些設備的普及範圍。在墨西哥,社會保險系統正在農村地區試行攜帶式氧氣服務,減少了住院人數。

亞太地區預計將成為成長最快的市場,到2031年複合年成長率將達到8.51%,這主要得益於日本被稱為「2025問題」的人口結構變化以及中國民眾希望「在熟悉的地方安享晚年」的願望。印度的「阿尤斯曼·巴拉特數位醫療計畫」(Ayushman Bharat Digital Mission)已為5億公民發放了唯一的健康ID,並促進了遠端醫療處方箋,以便為家庭監測設備提供醫療服務。在韓國,攜帶式氧氣設備的租賃費用最高可報銷80%,而澳洲的國家殘障人士保險計劃(NDIS)則為超過60萬名用戶提供輔助技術的資助。

在歐洲,人口老化和ESG(環境、社會和治理)採購目標是主要的驅動力。德國正利用社會保險購買輔助器具,英國國家醫療服務體系(NHS)承諾實現淨零排放採購,法國的「銀髮經濟」舉措則為居家醫療套裝提供補貼。所有這些舉措都在推動低碳設備在其整個生命週期中成為主流需求。歐盟範圍內的醫療設備法規強制要求進行上市後監管,這提高了合規標準,同時提升了安全性,並增強了消費者對構成耐用醫療設備市場基礎的長壽命設備的信心。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 人口快速老化推動了對行動輔助設備和呼吸照護的需求。

- 由物聯網設備組成的生態系統,可以提高治療依從性並實現數據貨幣化。

- 向居家慢性病照護過渡,並擴大報銷範圍。

- 人工智慧驅動的預測性維護可降低服務提供者的總擁有成本 (TCO)。

- 透過電子商務和DTP履約降低通路成本

- 與環境、社會和治理 (ESG) 相關的醫院資本投資正在推動設備向節能型設備替換。

- 市場限制因素

- 高昂的初始成本和整個生命週期內的整體服務成本

- GLP-1類減肥藥的廣泛使用導致行動輔助設備的銷售下降。

- 熟練的生物醫學技術人員短缺,導致服務週期延長。

- 售後資料標準的差異阻礙了互通性。

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 依設備類型

- 個人行動裝置

- 輪椅

- 拐杖和手杖

- 助行器和輪椅

- 其他個人行動裝置

- 浴室安全設備和醫療家具

- 醫用床和床墊

- 馬桶

- 其他浴室安全和醫療家具

- 監測和治療設備

- 血糖值儀

- 氧氣供應設備

- 生命徵象監測

- 其他監測和治療設備

- 個人行動裝置

- 最終用戶

- 醫院和診所

- 居家醫療設施

- 門診手術中心

- 其他最終用戶

- 透過分銷管道

- 醫院/診所藥局/醫療設備(DME)供應商

- 零售藥局和醫療設備零售商

- 線上和直接面向病患的銷售管道

- 企業對企業 (B2B) 交易

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他亞太國家

- 中東和非洲

- GCC

- 南非

- 其他中東和非洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 市佔率分析

- 公司簡介

- Abbott Laboratories

- Arjo AB

- Baxter International Inc.(Hillrom & Welch Allyn)

- Becton, Dickinson and Company

- Cardinal Health, Inc.

- Coloplast A/S

- Compass Health Brands

- ConvaTec Group plc

- Drive DeVilbiss Healthcare

- GE HealthCare Technologies Inc.

- Getinge AB

- Invacare Corporation

- Koninklijke Philips NV

- Masimo Corporation

- Medtronic plc

- Nihon Kohden Corporation

- OMRON Corporation

- Permobil(Patricia Industries)

- Pride Mobility Products Corp.

- ResMed Inc.

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd.

- Siemens Healthineers AG

- Stryker Corporation

- Sunrise Medical LLC

第7章 市場機會與未來展望

According to Mordor Intelligence, the durable medical equipment market size was valued at USD 231.85 billion in 2025 and is estimated to grow from USD 245.19 billion in 2026 to reach USD 319.54 billion by 2031, at a CAGR of 5.44% during the forecast period (2026-2031).

This report is Segmented by Device Type (Personal Mobility Devices [Wheelchairs, and More], Bathroom Safety Devices & Medical Furniture, and Monitoring & Therapeutic Devices), End-User (Hospitals & Clinics, and More), Distribution Channel (Hospital & Clinic Pharmacies, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Durable Medical Equipment Market Trends and Insights

Rapidly Ageing Population Sustaining Mobility and Respiratory Demand

Japan's share of citizens aged 75 years and older surpassed 15% in 2025, pushing purchases of wheelchairs, walkers, and oxygen concentrators covered by the long-term care insurance program that reimburses up to 90% of device costs . Eurostat forecasts Europe's population aged 65 and above to reach 30% by 2050, prompting national payers to subsidize home-based respiratory therapy and mobility aides. CMS projects Medicare enrollment to rise to 80 million by 2030, enlarging the addressable base for powered wheelchairs and CPAP systems. Germany allocated EUR 450 billion in 2024 health spending, with a rising share earmarked for assistive technology under social insurance rules. Safety standards such as ISO 7176 and IEC 60601 help ensure devices supplied to seniors meet durability and electrical requirements, reducing liability for providers.

IoT-Enabled Device Ecosystems Improving Adherence and Data Monetization

Connected glucose monitors, pulse oximeters, and portable ventilators increasingly pair with smartphones, transmitting real-time readings to cloud dashboards. Abbott's FreeStyle Libre 2 Plus transmits glucose data directly to Apple Health, allowing physicians to adjust dosing without clinic visits. ResMed's AirSense 11 CPAP streams usage metrics to clinicians, cutting 30-day readmissions for obstructive sleep apnea by 18% in a 2024 multi-site study. The FDA's TEMPO model grants automatic Medicare coverage for breakthrough connected devices within two days of approval, slashing time-to-reimbursement and encouraging rapid commercial launches. However, heterogeneous data standards slow cross-platform analytics, motivating adoption of HL7 FHIR for interoperability across vendor ecosystems.

High Upfront and Lifecycle Service Costs

Advanced power wheelchairs with IoT sensors list between USD 15,000 and USD 40,000, while smart hospital beds range from USD 8,000 to USD 25,000, challenging budgets where third-party reimbursement is thin. Preventive maintenance and software updates frequently add 20% to ownership expenses over five years, extending replacement cycles and increasing downtime risk. Biomedical technician shortages keep hourly service rates high across mature markets, with the U.S. Bureau of Labor Statistics expecting only 5% employment growth through 2032. Subscription bundles from equipment-as-a-service vendors absorb the upfront hit by spreading costs over monthly invoices. In Europe, MDR post-market surveillance updates every two years add EUR 50,000-200,000 per product line, expenses generally passed to buyers.

Other drivers and restraints analyzed in the detailed report include:

- Shift to Home-Based Chronic Care Supported by Reimbursement Expansion

- AI-Driven Predictive Maintenance Lowering TCO for Providers

- Uptake of GLP-1 Obesity Drugs Reducing Mobility-Aid Volumes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Monitoring and therapeutic devices held a 38.55% share of the durable medical equipment market in 2025 and are on track to expand at an 8.25% CAGR to 2031, outperforming mobility aids and bathroom-safety products. OTC glucose monitors like Abbott FreeStyle Libre 2 Plus and Dexcom Stelo remove finger-stick calibration and sync to mobile health apps, spurring double-digit unit growth across North America . Philips Respironics' multi-year recall shifted sleep-apnea demand to ResMed, whose cellular-enabled AirSense 11 helped reduce hospital readmissions by 18% in pilot programs, strengthening its foothold.

Growth momentum continues as payers reimburse remote vital-sign monitors used in home-health programs, helping the durable medical equipment market size for monitoring devices widen. Yet insulin-pump volumes face pressure from obesity-drug uptake, pushing pump makers to concentrate on pediatric and Type 1 diabetes niches. Oxygen concentrators and CPAP systems benefit from mHealth connectivity that supports remote adherence tracking. In contrast, personal mobility devices confront slower growth; to offset volume headwinds, power-chair vendors now embed fall-detection sensors and posture-adjustment algorithms that collect usable clinical data, reinforcing their role in value-based care pathways.

Geography Analysis

North America remains the largest regional contributor at 41.13% share in 2025, buoyed by rising Medicare enrollment and CMS policy that lifts home-health reimbursement. The FDA's expedited coverage for breakthrough devices shrinks commercialization timelines, accelerating adoption of IoT monitors and AI-enhanced oxygen concentrators. Amazon Pharmacy's logistics backbone supports rapid equipment delivery, helping online sales climb, while Canada's Assistive Devices Program funds up to 75% of eligible product costs, expanding access. Mexico's social insurance pilots portable oxygen services in rural areas, cutting hospital admissions.

Asia-Pacific is the fastest-growing arena at an 8.51% CAGR to 2031, propelled by Japan's "2025 problem" demographic shift and China's preference for aging in place. India's Ayushman Bharat Digital Mission created unique health IDs for half a billion citizens, smoothing telemedicine prescriptions for home-use monitors. South Korea reimburses up to 80% of portable oxygen rentals, while Australia's National Disability Insurance Scheme funds assistive technology for more than 600,000 participants.

Europe carries substantial weight behind aging demographics and ESG procurement goals. Germany channels social insurance toward assistive devices, the NHS commits to net-zero procurement, and France's Silver Economy initiative subsidizes home-medical kits, pushing lifecycle-low-carbon equipment into mainstream demand. EU-wide medical device regulation mandates post-market surveillance that raises compliance barriers but uplifts safety, reinforcing buyer confidence in long-lasting equipment that anchors the durable medical equipment market.

- Abbott Laboratories

- Arjo AB

- Baxter International Inc. (Hillrom & Welch Allyn)

- Beckton Dickinson

- Cardinal Health

- Coloplast

- Compass Health

- ConvaTec Group plc

- Drive DeVilbiss Healthcare

- GE HealthCare Technologies Inc.

- Getinge

- Invacare

- Koninklijke Philips

- Masimo

- Medtronic

- Nihon Kohden

- OMRON

- Permobil (Patricia Industries)

- Pride Mobility Products

- Resmed

- Mindray

- Siemens Healthineers

- Stryker

- Sunrise Medical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapidly ageing population sustaining mobility & respiratory demand

- 4.2.2 IoT-enabled device ecosystems improving adherence & data monetisation

- 4.2.3 Shift to home-based chronic-care supported by reimbursement expansion

- 4.2.4 AI-driven predictive maintenance lowering TCO for providers

- 4.2.5 E-commerce & DTP fulfilment compressing channel costs

- 4.2.6 ESG-linked hospital cap-ex boosting energy-efficient equipment refresh

- 4.3 Market Restraints

- 4.3.1 High upfront & lifecycle service costs

- 4.3.2 Uptake of GLP-1 obesity drugs reducing mobility-aid volumes

- 4.3.3 Skilled biomedical-tech labour shortages lengthening service cycles

- 4.3.4 Fragmented post-sale data standards hampering interoperability

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers/Consumers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Device Type

- 5.1.1 Personal Mobility Devices

- 5.1.1.1 Wheelchairs

- 5.1.1.2 Crutches & Canes

- 5.1.1.3 Walkers & Rollators

- 5.1.1.4 Other Personal Mobility Devices

- 5.1.2 Bathroom Safety Devices & Medical Furniture

- 5.1.2.1 Medical Beds & Mattresses

- 5.1.2.2 Commodes & Toilets

- 5.1.2.3 Other Bathroom Safety & Medical Furniture

- 5.1.3 Monitoring & Therapeutic Devices

- 5.1.3.1 Blood Glucose Monitors

- 5.1.3.2 Oxygen Equipment

- 5.1.3.3 Vital-sign Monitors

- 5.1.3.4 Other Monitoring & Therapeutic Devices

- 5.1.1 Personal Mobility Devices

- 5.2 By End-User

- 5.2.1 Hospitals & Clinics

- 5.2.2 Home-Healthcare Settings

- 5.2.3 Ambulatory Surgical Centres

- 5.2.4 Other End-Users

- 5.3 By Distribution Channel

- 5.3.1 Hospital & Clinic Pharmacies / DME Suppliers

- 5.3.2 Retail Pharmacies & DME Stores

- 5.3.3 Online & Direct-to-Patient Channels

- 5.3.4 Business-to-business (B2B)

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 Arjo AB

- 6.3.3 Baxter International Inc. (Hillrom & Welch Allyn)

- 6.3.4 Becton, Dickinson and Company

- 6.3.5 Cardinal Health, Inc.

- 6.3.6 Coloplast A/S

- 6.3.7 Compass Health Brands

- 6.3.8 ConvaTec Group plc

- 6.3.9 Drive DeVilbiss Healthcare

- 6.3.10 GE HealthCare Technologies Inc.

- 6.3.11 Getinge AB

- 6.3.12 Invacare Corporation

- 6.3.13 Koninklijke Philips N.V.

- 6.3.14 Masimo Corporation

- 6.3.15 Medtronic plc

- 6.3.16 Nihon Kohden Corporation

- 6.3.17 OMRON Corporation

- 6.3.18 Permobil (Patricia Industries)

- 6.3.19 Pride Mobility Products Corp.

- 6.3.20 ResMed Inc.

- 6.3.21 Shenzhen Mindray Bio-Medical Electronics Co., Ltd.

- 6.3.22 Siemens Healthineers AG

- 6.3.23 Stryker Corporation

- 6.3.24 Sunrise Medical LLC

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment

醫療耐用設備市場:2026-2032年全球市場預測(按產品類型、最終用戶、分銷管道和購買方式分類)

醫療耐用設備市場:2026-2032年全球市場預測(按產品類型、最終用戶、分銷管道和購買方式分類) 耐用醫療設備(DME)市場規模、佔有率、趨勢和預測:按產品、最終用途和地區分類,2026-2034年

耐用醫療設備(DME)市場規模、佔有率、趨勢和預測:按產品、最終用途和地區分類,2026-2034年 2026年全球耐用醫療設備市場報告

2026年全球耐用醫療設備市場報告 2026-2034年全球耐用醫療設備市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球耐用醫療設備市場規模、佔有率、趨勢和成長分析報告 全球耐用醫療設備市場:市場規模、佔有率和趨勢分析(按產品、最終用途和地區分類),細分市場預測(2026-2033 年)美國呼吸系統耐用醫療設備市場規模、佔有率和趨勢分析報告:按產品供應、分銷/服務管道、主要州和細分市場預測,2026-2033年美國耐用醫療設備市場規模、佔有率和趨勢分析報告:按產品、最終用途和細分市場預測(2026-2033 年)

全球耐用醫療設備市場:市場規模、佔有率和趨勢分析(按產品、最終用途和地區分類),細分市場預測(2026-2033 年)美國呼吸系統耐用醫療設備市場規模、佔有率和趨勢分析報告:按產品供應、分銷/服務管道、主要州和細分市場預測,2026-2033年美國耐用醫療設備市場規模、佔有率和趨勢分析報告:按產品、最終用途和細分市場預測(2026-2033 年) 耐用醫療設備市場規模、佔有率和成長分析(按產品、支付方、最終用途和地區分類)-2026-2033年產業預測

耐用醫療設備市場規模、佔有率和成長分析(按產品、支付方、最終用途和地區分類)-2026-2033年產業預測 耐用醫療設備市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)

耐用醫療設備市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年) 全球耐用醫療設備市場:洞察、競爭格局、市場預測:2030年

全球耐用醫療設備市場:洞察、競爭格局、市場預測:2030年