|

市場調查報告書

商品編碼

2066447

石墨烯:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Graphene - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

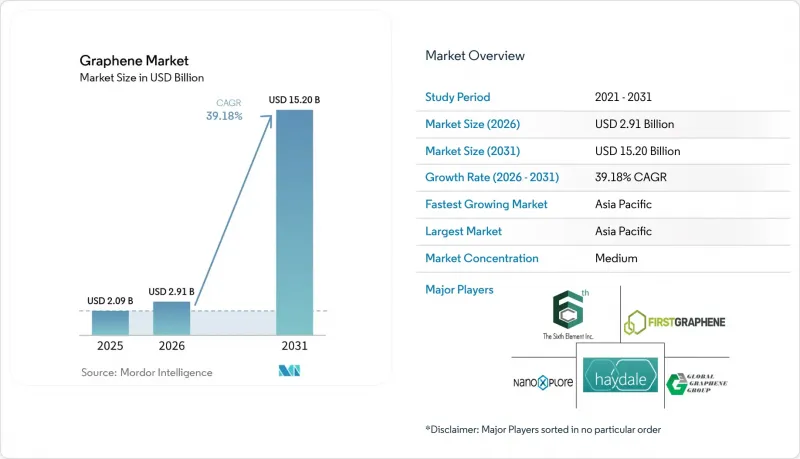

據 Mordor Intelligence 稱,2025 年石墨烯市值為 20.9 億美元,預計到 2031 年將從 2026 年的 29.1 億美元成長到 152 億美元,預測期(2026-2031 年)的複合年成長率為 39.18%。

本報告按產品類型(石墨烯薄片和薄膜、奈米片及其他)、應用領域(複合材料、生物醫學和醫療保健及其他)、終端用戶行業(電子通訊、生物醫學和醫療保健及其他)以及地區(亞太地區、北美地區、歐洲地區、南美地區、中東和非洲)進行細分。市場預測以美元計價。

全球石墨烯市場趨勢及洞察

石墨烯在航太領域的應用日益廣泛

飛機製造商正將石墨烯奈米微片嵌入碳纖維預浸料中,以減輕15-20%的結構重量,這是將燃油效率提升25%(與傳統寬體飛機相比)的必要閾值。波音公司在2025年供應商文件中強制要求在777X的二級結構中使用石墨烯複合材料,理由是其抗雷擊性能比鋁蜂巢材料高出40%。空中巴士公司正在A350的控制面板上試用氧化石墨烯表面塗層,以抑制潮濕沿海氣候下的電流腐蝕,這是長途航空公司長期面臨的維護難題。國防相關合約也在推動這一趨勢。 2025年,美國空軍研究實驗室津貼1,800萬美元,用於開發雷達吸波石墨烯層壓板,以降低第六代戰鬥機原型機在X波段的雷達反射面積。然而,基於 AS9100 協議的認證週期平均需要 18 到 24 個月,這意味著中小型供應商的收入累計將會延遲,並且將被迫維持較高的價格範圍。

利用石墨烯拓展儲能應用

電力公司正將2018年至2022年安裝的鋰離子電池組維修為石墨烯增強型負極。這將使電池的充電接受能力提高35%,從而在電力市場自由化的情況下提供更盈利的頻率調節服務。 NanoXplore公司於2025年3月簽署了一份價值4200萬美元的供應契約,涵蓋美國五個州共計500兆瓦時的此類升級,這是迄今為止規模最大的商業部署。同時,智慧型手機廠商也積極尋求利潤成長。將石墨烯超級電容與100瓦充電器結合使用,可消除室溫下熱失控的風險。三星計劃在2026年將其應用於旗艦機型。美國能源局(DOE)的Battery500聯盟正在進行一項長期研究,目標是研發能量密度為500瓦時/公斤的電池,是目前基準值的兩倍,這使得石墨烯成為後鋰化學系統發展的關鍵橋樑。

高昂的製造成本

以化學氣相沉積 (CVD) 法製備的石墨烯片成本高昂,每公斤售價 200 至 500 美元,而奈米碳管每公斤售價僅 10 至 20 美元,炭黑每公斤售價僅 2 至 5 美元,這成為許多大規模應用面臨的經濟障礙。液相剝離法是製備奈米片的主要工藝,僅溶劑回收一項就需消耗 40 至 60 千瓦時/公斤的能源,使工業能源成本增加 80 至 120 美元。 Fast Graphene 公司預測,到 2025 年,石墨烯的平均毛利率僅為 38%,低於特種化學品 55% 至 65% 的水平,這限制了對產能的再投資。雖然擴大生產規模可以帶來部分成本降低,但產能倍增也只能使每公斤成本降低 12% 至 15%,遠低於鋰離子電池和太陽能等領先應用案例所展現的學習曲線。由於需求預測不確定,年產能超過 500 噸的反應器設備供應商仍保持 18 至 24 個月的前置作業時間,供應側的韌性改善緩慢。

細分市場分析

2025年,石墨烯奈米微片(GNPs)的銷售額佔比達56.14%。這反映了其能夠無縫整合到聚合物混煉商常用的雙螺桿擠出機和三輥煉膠機中。這一優勢構成了石墨烯產品市場規模的基礎。隨著中國單價降至80美元/公斤以下,預計到2031年,其市場滲透率將以44.63%的複合年成長率成長。濃度為1-3wt%的奈米片可將拉伸模量提高高達300%,使汽車製造商能夠在滿足2027年碰撞安全標準的前提下,將底盤護板的品質降低12-15%。常州六元科技有限公司2025年奈米片銷售額累計8,500萬美元,較去年同期成長62%。這凸顯了中國在石墨烯市場的成本優勢。功能化衍生物將進一步拓展其應用範圍。 Perpetuus 公司推出的羧基化變體可使環氧樹脂的強度提高 35%,並減少航太蜂窩芯材的分層。

儘管薄膜和片材仍屬於高階小眾市場,價格在每平方公尺800 至 1200 美元之間,但其光學透明度(98%)和導電性(超過 10^6 S/m)正吸引折疊式顯示器的 OEM 製造商。 LG Display 預計到 2027 年將實現每年 10 萬平方公尺的產能,相當於 5,000 萬塊 7 吋螢幕。這將使透明導電材料成為石墨烯市場中一個價值十位數的細分市場。氧化物薄片雖然市佔率仍然較小,但正在為生物醫學領域的創新奠定基礎,例如與抗體共用合,從而支持飛莫耳級生物感測器的靈敏度。量子點和氣凝膠仍處於研發階段,但津貼重點正轉向光催化氫氣和吉赫吸收,預計未來價值集中度可能會改變。

區域分析

預計到2025年,亞太地區將佔全球石墨烯銷售額的45.23%,並將在2031年之前以45.69%的複合年成長率持續成長,這使其穩居石墨烯市場最大區域中心地位。中國從黑龍江省天然石墨開採到常州每年生產3000噸奈米片分散液的「從搖籃到大門」一體化體系,已將供應成本降低至每公斤60-80美元,僅為歐洲平均價格的一半,加速了聚合物化合物和電池添加劑的商品化進程。台灣台積電已檢驗其石墨烯互連技術,該技術在2奈米測試晶圓上可將訊號延遲降低18%,這表明半導體需求不斷成長,為該地區的投資提供了支撐。印度已撥款 500 億印度盧比(約 6000 萬美元)用於一項“國家石墨烯計劃”,該計劃旨在 2025 年開發水質淨化淨化膜,這表明印度的政策與適應氣候變遷的基礎設施相一致。

北美地區的銷售主要得益於美國能源局(DOE) 資助的負極材料生產線以及對航太複合材料的需求。兩黨共同通過的《基礎建設法案》撥款 1.4 億美元用於石墨烯基鋰離子電池的生產,保障了國內電池製造商的供應鏈安全。 NanoXplore 公司計劃於 2025 年第三季將其蒙特利爾工廠的產能擴建至每年 4000 噸,這將降低電動車電池供應方圓 500 英里內的物流成本。同時,加拿大戰略創新基金正向 Grafoid 公司的醫用氧化石墨烯試點計畫投資 3,000 萬加元(約 2,200 萬美元),顯示渥太華政府對高利潤醫療細分市場的重視。墨西哥作為印刷電子中心正蓬勃發展,Vorbeck 公司位置墨西哥的 200 萬平方米油墨工廠為跨境汽車行業客戶提供服務。

2025年,歐洲市場銷售強勁,這得益於石墨烯旗艦計畫提供的10億歐元資金支持,以及航太複合材料和海水淡化塗料領域的強勁成長勢頭。 Versarien的英國試點計畫獲得了旗艦基金800萬歐元的資助,正在為空中巴士A350的控制面開發一種樹脂,以抑制電流腐蝕。德國弗勞恩霍夫研究所正在共同開發一種石墨烯導熱介面材料,可將電池式電動車逆變器接頭溫度降低20%,進而提高動力系統的耐久性。 REACH法規的預先註冊促使中型企業進行整合,導致15家企業退出或合併,區域石墨烯市場集中度日益提高。南美和中東地區發展滯後,但對特定應用領域的興趣正在成長。在沙烏地阿拉伯,一家海水淡化廠透過使用石墨烯塗層減少了 70% 的腐蝕;巴西米納斯吉拉斯州的一家研究機構正在進行石墨烯加固尾礦壩的試驗操作,以減輕礦區崩壞的風險。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 石墨烯在航太領域的應用日益廣泛

- 在海水淡化基礎設施中採用石墨烯防腐蝕塗層

- 利用石墨烯拓展儲能應用

- 電子和半導體產業需求不斷成長

- 石墨烯電磁干擾屏蔽泡棉在5G基礎設施的商業化應用

- 市場限制因素

- 高昂的生產成本

- 替代方案的可用性

- 奈米毒理學與監管不確定性

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 依產品類型

- 石墨烯薄片和薄膜

- 石墨烯奈米微片(GNP)

- 氧化石墨烯(GO)

- 奈米片

- 其他

- 透過使用

- 複合材料

- 能量儲存和回收

- 印刷電子和軟性電子

- 生物醫學和醫療保健

- 塗料和油漆

- 其他

- 按最終用戶行業分類

- 電子與通訊

- 航太/國防

- 能源與電力

- 生物醫學和醫療保健

- 其他(汽車、化工、油漆)

- 按地區

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 埃及

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- ACS Material

- Cabot Corporation

- Cheap Tubes

- Directa Plus SpA

- First Graphene Ltd

- G6 Materials Corp.

- Global Graphene Group

- Grafoid Inc

- Graphene Manufacturing Group Ltd

- Graphenea

- Haydale Graphene Industries plc

- NanoXplore Inc.

- Perpetuus Advanced Materials

- Talga Group

- The Sixth Element(Changzhou)Materials Technology Co.,Ltd

- Thomas Swan & Co. Ltd

- Universal Matter Inc

- Versarien plc

- Vorbeck Materials Corp.

第7章 市場機會與未來展望

According to Mordor Intelligence, the graphene market size was valued at USD 2.09 billion in 2025 and is estimated to grow from USD 2.91 billion in 2026 to reach USD 15.20 billion by 2031, at a CAGR of 39.18% during the forecast period (2026-2031).

This report is Segmented by Product Type (Graphene Sheets and Films, Nanoplatelets, and Others), Application (Composites, Biomedical and Healthcare, and Others), End-User Industry (Electronics and Telecommunications, Biomedical and Healthcare, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and the Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Graphene Market Trends and Insights

Increasing Usage of Graphene in the Aerospace Industry

Aircraft OEMs embed graphene nanoplatelets into carbon-fiber prepregs to secure 15-20% structural weight reductions, a threshold needed to reach 25% fuel-burn improvements over legacy wide-body fleets. Boeing's 2025 supplier documents mandate graphene composites in the 777X secondary structures, citing lightning-strike dissipation that exceeds aluminum honeycomb by 40%. Airbus is piloting graphene oxide surface coatings on A350 control panels to curb galvanic corrosion in humid coastal climates, a persistent maintenance driver for long-haul operators. Defense contracts reinforce the trend: the US Air Force Research Laboratory awarded USD 18 million in 2025 to develop radar-absorbing graphene laminates that lower X-band signatures on sixth-generation fighter prototypes. Qualification cycles, however, average 18-24 months under AS9100 protocols, delaying revenue recognition for smaller suppliers and sustaining premium pricing.

Expansion of Energy-Storage Applications Utilizing Graphene

Utilities are retrofitting lithium-ion arrays installed between 2018 and 2022 with graphene-enhanced anodes that raise charge acceptance by 35%, enabling lucrative frequency-regulation services in deregulated power pools. A USD 42 million supply deal inked by NanoXplore in March 2025 covers 500 MWh of such upgrades across five US states, the largest commercial deployment to date. Smartphone vendors pursue parallel gains: graphene supercapacitors paired with 100-watt chargers eliminate thermal-runaway risks at room temperature, a feature Samsung plans to commercialize in 2026 flagships. Longer-term research from the DOE's Battery500 Consortium targets 500 Wh/kg cells, double present benchmarks, positioning graphene as a vital bridge to post-lithium chemistries.

High Production Cost

Chemical-vapor-deposition sheets command USD 200-500 /kg, compared with USD 10-20 for carbon nanotubes and USD 2-5 for carbon black, keeping many high-volume uses financially out of reach. Liquid-phase exfoliation, the workhorse process for nanoplatelets, consumes 40-60 kWh/kg in solvent recovery alone, adding USD 80-120 in energy overheads at industrial tariffs. First Graphene's 2025 results revealed average 38% gross margins versus 55-65% for specialty chemicals, constraining reinvestment in capacity. Scaling offers partial relief-doubling throughput shaves merely 12-15% off cost per kilogram-far below learning-curve precedents set by lithium-ion or photovoltaics. Equipment suppliers, facing uncertain demand visibility, maintain 18-24 month lead times on reactors exceeding 500 tpa, delaying supply-side elasticity.

Other drivers and restraints analyzed in the detailed report include:

- Growing Demand in Electronics and Semiconductors

- Commercialisation of Graphene EMI-Shielding Foams for 5G Infrastructure

- Availability of Substitutes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Graphene Nanoplatelets (GNP) captured 56.14% of 2025 revenue, reflecting their seamless integration into twin-screw extruders and three-roll mills long familiar to polymer compounders. This dominance anchors the graphene market size at the product level, with forecast penetration expanding at a 44.63% CAGR to 2031 as unit pricing slides below USD 80/kg in China. Nanoplatelets dispersed at 1-3 wt% lift tensile modulus by up to 300%, enabling automakers to shave 12-15% off underbody shield mass while meeting 2027 crash standards. Sixth Element (Changzhou) booked USD 85 million in nanoplatelet sales in 2025, up 62% year-over-year, underscoring China's cost leverage in the graphene market. Functionalized derivatives extend utility: carboxylated variants launched by Perpetuus strengthen epoxies by 35%, reducing delamination in aerospace honeycomb cores.

Films and sheets remain a premium niche, priced at USD 800-1,200/m2, yet their optical clarity (98%) and conductivity (more than 10^6 S/m) attract foldable display OEMs. LG Display expects to convert 100,000 m2 per year by 2027, adequate for 50 million 7-inch screens, positioning transparent conductors as a 10-figure sub-segment of the graphene market. Oxide flakes, though holding a smaller slice, anchor biomedical innovations where covalent bonding with antibodies underpins femtomolar biosensor sensitivity. Quantum dots and aerogels linger in R&D, but grant funding focuses on photocatalytic hydrogen production and gigahertz-wave absorption, hedging against future value-pool shifts.

Geography Analysis

Asia-Pacific anchored 45.23% of 2025 revenue and is on track for a 45.69% CAGR through 2031, ensuring it remains the largest regional node of the graphene market. China's cradle-to-gate integration, from natural-graphite mining in Heilongjiang to 3,000 tpa nanoplatelet dispersion in Changzhou, cuts delivered cost to USD 60-80/kg, half European averages, catalyzing commoditization in polymer compounding and battery additives. Taiwan's TSMC validated graphene interconnects that lower signal delay by 18% in 2 nm test wafers, demonstrating semiconductor pull that anchors regional investment. India earmarked INR 500 crore (USD 60 million) in 2025 for a National Graphene Mission focused on water purification membranes, illustrating policy alignment with climate-adaptation infrastructure.

North America's revenue is buoyed by DOE-funded anode lines and aerospace composite demand. The Bipartisan Infrastructure Law assigns USD 140 million to graphene-enhanced lithium-ion manufacturing, creating a protected corridor for domestic cell makers. NanoXplore's Montreal expansion to 4,000 tpa in Q3 2025 lowers logistics costs within a 500-mile EV-battery supply radius, while Canada's Strategic Innovation Fund injected CAD 30 million (USD 22 million) into Grafoid's biomedical-graphene oxide pilot, signaling Ottawa's tilt toward high-margin healthcare niches. Mexico gains traction as a printed-electronics hub, hosting Vorbeck's 2 million m2 ink plant that services cross-border automotive customers.

Europe's revenue in 2025 was retained with momentum in aerospace composites and desalination coatings supported by the Graphene Flagship's EUR 1 billion funding envelope. Versarien's UK pilot lines, backed by EUR 8 million of Flagship funds, target Airbus A350 control-surface resins to tame galvanic corrosion. Germany's Fraunhofer Institute co-develops graphene thermal interfaces that promise 20% inverter-junction-temperature cuts in battery electric vehicles, chasing extended drivetrain durability. REACH pre-registration triggered a mid-tier shakeout, prompting 15 exits or consolidations and nudging the regional graphene market size toward higher concentration. South America and the Middle East trail yet signal application-specific interest: Saudi Arabia's desalination plants logged 70% corrosion reductions using graphene coatings, and Brazil's Minas Gerais institute pilots graphene-reinforced tailings dams to mitigate collapse risk in mining regions.

- ACS Material

- Cabot Corporation

- Cheap Tubes

- Directa Plus S.p.A.

- First Graphene Ltd

- G6 Materials Corp.

- Global Graphene Group

- Grafoid Inc

- Graphene Manufacturing Group Ltd

- Graphenea

- Haydale Graphene Industries plc

- NanoXplore Inc.

- Perpetuus Advanced Materials

- Talga Group

- The Sixth Element (Changzhou) Materials Technology Co.,Ltd

- Thomas Swan & Co. Ltd

- Universal Matter Inc

- Versarien plc

- Vorbeck Materials Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing usage of graphene in the aerospace industry

- 4.2.2 Adoption of graphene anti-corrosion coatings in desalination infrastructure

- 4.2.3 Expansion of energy-storage applicationsutilizing graphene

- 4.2.4 Growing demand in electronics and semiconductors

- 4.2.5 Commercialisation of graphene EMI-shielding foams for 5G infrastructure

- 4.3 Market Restraints

- 4.3.1 High production cost

- 4.3.2 Availability of substitutes

- 4.3.3 Nanotoxicology & regulatory uncertainty

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Graphene Sheets and Films

- 5.1.2 Graphene Nanoplatelets (GNP)

- 5.1.3 Graphene Oxide (GO)

- 5.1.4 Nanoplatelets

- 5.1.5 Others

- 5.2 By Application

- 5.2.1 Composites

- 5.2.2 Energy Storage and Harvesting

- 5.2.3 Printed and Flexible Electronics

- 5.2.4 Biomedical and Healthcare

- 5.2.5 Coatings and Paints

- 5.2.6 Others

- 5.3 By End-user Industry

- 5.3.1 Electronics and Telecommunications

- 5.3.2 Aerospace and Defense

- 5.3.3 Energy and Power

- 5.3.4 Biomedical and Healthcare

- 5.3.5 Others(automotive, Chemical and Coatings)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 South Korea

- 5.4.1.4 India

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 NORDIC Countries

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Egypt

- 5.4.5.5 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 ACS Material

- 6.4.2 Cabot Corporation

- 6.4.3 Cheap Tubes

- 6.4.4 Directa Plus S.p.A.

- 6.4.5 First Graphene Ltd

- 6.4.6 G6 Materials Corp.

- 6.4.7 Global Graphene Group

- 6.4.8 Grafoid Inc

- 6.4.9 Graphene Manufacturing Group Ltd

- 6.4.10 Graphenea

- 6.4.11 Haydale Graphene Industries plc

- 6.4.12 NanoXplore Inc.

- 6.4.13 Perpetuus Advanced Materials

- 6.4.14 Talga Group

- 6.4.15 The Sixth Element (Changzhou) Materials Technology Co.,Ltd

- 6.4.16 Thomas Swan & Co. Ltd

- 6.4.17 Universal Matter Inc

- 6.4.18 Versarien plc

- 6.4.19 Vorbeck Materials Corp.

7 Market Opportunities & Future Outlook

- 7.1 Development of graphene nanodevices for DNA sequencing

- 7.2 Adoption of graphene into photodetectors

- 7.3 White-space & Unmet-need Assessment

全球2D材料市場規模、佔有率、趨勢和成長分析報告(2026-2034):超越石墨烯

全球2D材料市場規模、佔有率、趨勢和成長分析報告(2026-2034):超越石墨烯 石墨烯市場預測至2034年-全球分析(依產品類型、製造方法、原料、應用、終端用戶產業、形態、通路、功能及地區分類)石墨基材市場預測(2034 年)-按材料類型、形態、性能、應用、產業和地區分類的全球市場分析全球石墨烯市場(2027-2037 年)

石墨烯市場預測至2034年-全球分析(依產品類型、製造方法、原料、應用、終端用戶產業、形態、通路、功能及地區分類)石墨基材市場預測(2034 年)-按材料類型、形態、性能、應用、產業和地區分類的全球市場分析全球石墨烯市場(2027-2037 年) 無石墨烯2D材料市場:依材料、應用、合成方法、最終用戶、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測

無石墨烯2D材料市場:依材料、應用、合成方法、最終用戶、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測 石墨烯市場機會、成長要素、產業趨勢分析及2026-2035年預測。

石墨烯市場機會、成長要素、產業趨勢分析及2026-2035年預測。 石墨烯市場規模、佔有率、趨勢和預測:按類型、應用、終端用戶產業和地區分類,2026-2034年石墨烯基材料市場預測至2034年-材料類型、形態、製造方法、應用、最終用戶和地區分類的全球分析

石墨烯市場規模、佔有率、趨勢和預測:按類型、應用、終端用戶產業和地區分類,2026-2034年石墨烯基材料市場預測至2034年-材料類型、形態、製造方法、應用、最終用戶和地區分類的全球分析 石墨烯導熱材料市場分析及預測(至2035年):類型、產品、技術、應用、形式、最終用戶與功能石墨烯和2D材料電子市場:預測(至2034年)-按材料、應用、最終用戶和地區分類的全球分析

石墨烯導熱材料市場分析及預測(至2035年):類型、產品、技術、應用、形式、最終用戶與功能石墨烯和2D材料電子市場:預測(至2034年)-按材料、應用、最終用戶和地區分類的全球分析