|

市場調查報告書

商品編碼

2066431

伴隨診斷:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Companion Diagnostics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

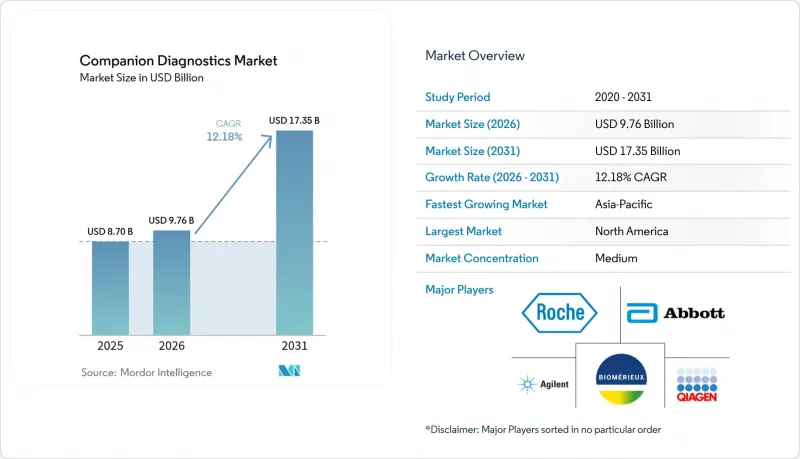

據 Mordor Intelligence 稱,2025 年伴隨診斷市場價值為 87 億美元,預計到 2031 年將達到 173.5 億美元,而 2026 年為 97.6 億美元,預測期(2026-2031 年)的複合年成長率為 12.18%。

本報告按技術(免疫組織化學、聚合酵素鏈鎖反應(PCR) 等)、適應症(肺癌、乳癌等)、產品類型(檢測和試劑盒、儀器和分析儀等)、檢體類型(組織切片檢查、液態生物檢體等)、最終用戶(製藥和生物技術公司、合約研究組織 (CRO) 等)和地區進行分類。

全球伴隨診斷市場趨勢與洞察

伴隨診斷市場趨勢與洞察:液態生物檢體伴隨診斷在腫瘤臨床實踐中的快速普及

液態生物檢體伴隨診斷正在重新定義癌症治療管理,它提供了一種微創、可重複的檢測方法,能夠即時捕捉腫瘤的異質性。臨床醫生現在可以透過循環腫瘤DNA追蹤疾病進展,並動態調整治療方法,而不是依賴靜態的組織切片。由此,醫院檢查室需要重新考慮其檢測能力和低溫運輸物流,以應對血液檢測量的增加,這將影響整個腫瘤科的資金分配計畫。 FoundationOne Liquid CDx於2024年獲得多項FDA批准,這清楚地展現了監管力度推動其市場滲透的勢頭。然而,由於液態生物檢體的敏感性仍然會因癌症分期和腫瘤釋放機制的不同而有所差異,醫療機構不得不採用“組織和血液檢測相結合的混合策略”,以在保持診斷準確性的同時,最大限度地減少重複檢測。

個人化醫療和精準腫瘤學的進展

伴隨診斷不再只是可選項,它已成為許多標靶治療獲得治療的法定必要條件。美國食品藥物管理局(FDA)已列出168種與已通過核准檢測相關的生物標記-藥物組合,這意味著保險報銷機構將逐步停止支付未進行分子水平確認的治療療程費用。這種關聯促使製藥公司在I期臨床試驗早期階段就與藥物研發團隊合作開發檢測方法,從而縮短整體研發週期,但同時也增加了臨床前研究的複雜性。由此直接導致合約研究組織(CRO)正在擴展其生物標記檢驗能力,以確保獲得多年戰略外包契約,從而在生物製藥研發管線中確立了自身事實上的「分子水平安全隔離網閘」地位。

高昂的開發成本

伴隨診斷的研發可能需要5,000萬至1億美元的投資,耗時3至5年,因此診斷是長期資本項目。中小企業越來越依賴與大型製藥企業的合作,透過股權轉讓換取研發資金。由此產生的一個次要後果是知識產權組合的整合。隨著大型公司吸收醫療設備的專利權,新參與企業的經營自由度正在下降。這種充滿挑戰的智慧財產權環境促使創業投資人更傾向於投資擁有可擴展檢測項目的平台型公司,而非單一標誌物概念,創業投資資金的重心也正悄悄從利基生物標記轉向擴充性的、資訊科學主導的解決方案。這些結構性變化正在重塑伴隨診斷市場。

細分市場分析

即使到了2025年,PCR仍將佔據伴隨診斷市場21.8%的最大佔有率,但NGS預計將超越所有其他技術。 NGS在伴隨診斷領域的市場規模預計將超過基於PCR的替代方案,並在2026年至2031年間以13.85%的複合年成長率成長。醫院採購委員會擴大進行總體擁有成本(TCO)分析,結果表明,高樣本處理能力可以在三年攤銷期內抵消NGS耗材成本的增加。因此,儀器供應商現在將分析軟體與試劑合約捆綁銷售,這種機制將收入確認方式從一次性硬體銷售轉向持續服務收入,並重塑了季度收入預測。

隨著聯合治療免疫療法的日益普及,黑色素瘤伴隨診斷的市場佔有率預計將在2031年之前以13.22%的複合年成長率成長。這將需要皮膚科檢查室和分子實驗室之間密切合作,以確保快速進行Reflex檢測,從而有效地融合兩個先前各自獨立的臨床領域。這種整合要求電子健康記錄供應商調整其醫囑輸入模組,以支援Reflex分子檢測專案。雖然這種IT調整表面上看起來微不足道,但實際上卻代表著整個醫療保健系統一項巨大的行政投入。

區域分析

截至2025年,北美將佔據39.95%的市場。聯合健康保險公司(UnitedHealthcare)的政策是,當FDA批准的伴隨診斷試劑與相應藥物聯合使用時,保險公司會為其提供保險覆蓋。這項政策獲得了其他保險公司的支持,直接影響了這些試劑的普及速度。因此,預計聯合健康保險公司以外的其他私人保險公司也可能效仿這項政策,以保持自身競爭力。這將引發連鎖反應,從而穩定整個產業的檢測報銷率。

預計2026年至2031年,亞太地區的複合年成長率將達到12.45%。日本政府支持的癌症基因組分析(CGP)計畫預計到2035年市場規模將達到540億日圓,將推動日本國內檢測實驗室定序能力的提升。這項政府措施將為鄰國樹立先例,協調監管預期,促進跨境臨床試驗的參與,並加速對研究不足的亞洲人群的數據累積。

歐洲體外醫療設備法規 (IVDR) 的環境正迫使企業重新思考其產品上市策略。認證實驗室有限的處理能力增加了市場風險,導致診斷設備製造商考慮將集中檢測模式作為臨時解決方案。然而,這種集中化可能會無意中強化某些參考實驗室的地位,並形成準寡占,從而在檢測量高峰期影響定價。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 液態生物檢體(CDx)在腫瘤治療領域的快速普及。

- 個人化醫療和精準腫瘤學的進展

- 診斷工具的技術創新

- 慢性病盛行率增加

- 以抗體藥物偶聯物(ADC)為中心的腫瘤產品線需要多重伴隨診斷平台

- 製藥公司加大投資

- 市場限制因素

- 高昂的開發成本

- FDA的上市後證據提交要求正在推高生命週期成本。

- 嚴格的監理政策

- 新興國家基礎設施匱乏

- 供應鏈分析

- 監理展望

- 波特五力分析

第5章 市場規模與成長預測

- 透過技術

- 免疫組織化學(IHC)

- 聚合酵素鏈鎖反應(PCR)

- 即時PCR(RT-PCR)

- 原位雜合反應(ISH)

- 次世代定序(NGS)

- 其他技術

- 適應症

- 肺癌

- 乳癌

- 結腸癌

- 白血病

- 黑色素瘤

- 胃癌

- 攝護腺癌

- 其他改編

- 按產品/服務

- 檢測和試劑盒

- 測量儀器和分析設備

- 軟體服務

- 依樣本類型

- 組織切片檢查

- 液態生物檢體

- 細胞學塗片

- 最終用戶

- 製藥和生物技術公司

- 受託研究機構(CRO)

- 臨床實驗室

- 醫院和癌症中心

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他亞太國家

- 中東

- GCC

- 南非

- 其他中東國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Abbott

- Agilent Technologies Inc.

- F. Hoffmann-La Roche Ltd

- bioMerieux SA

- QIAGEN NV

- Siemens Healthineers AG

- Thermo Fisher Scientific Inc.

- Danaher Corp.(Beckman Coulter)

- Illumina Inc.

- Myriad Genetics Inc.

- Guardant Health Inc.

- Sysmex Corp.

- Abnova Corp.

- Biogenex Laboratories Inc.

- Tempus Labs Inc.

- Foundation Medicine Inc.

- Exact Sciences Corp.

- PerkinElmer Inc.

- Invivoscribe Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the companion diagnostics market size was valued at USD 8.70 billion in 2025 and estimated to grow from USD 9.76 billion in 2026 to reach USD 17.35 billion by 2031, at a CAGR of 12.18% during the forecast period (2026-2031).

This report is Segmented by Technology (Immunohistochemistry, Polymerase Chain Reaction, and More), Indication (Lung Cancer, Breast Cancer, and More), Product Type (Assays and Kits, and Instruments and Analyzers, and More), Sample Type (Tissue Biopsy, Liquid Biopsy, and More), End-User (Pharmaceutical and Biotechnology Companies, Contract Research Organizations (CROs), and More), and Geography.

Global Companion Diagnostics Market Trends and Insights

Companion Diagnostics Market Trends & Insights Rapid Adoption of Liquid-Biopsy CDx in Oncology Practices

Liquid biopsy companion diagnostics are redefining cancer management by providing a minimally invasive route for repeat testing that captures tumor heterogeneity in real time. Clinicians now track disease evolution through circulating tumor DNA, dynamically adjusting therapy rather than relying on static tissue snapshots. A second-order implication is that hospital laboratories must recalibrate throughput and cold-chain logistics to accommodate larger volumes of blood-based assays, affecting capital-allocation timelines across the entire oncology service line. FoundationOne Liquid CDx, granted multiple FDA approvals in 2024, illustrates the regulatory momentum that is quickening market uptake . Yet liquid biopsy sensitivity still varies by cancer stage and by tumor shedding biology, meaning providers are pressured to adopt hybrid tissue-plus-blood strategies that preserve diagnostic accuracy while controlling test redundancy.

Advancements in Personalized Medicine and Precision Oncology

Companion diagnostics have moved beyond optional add-ons; they are codified prerequisites for access to many targeted drugs. The FDA lists 168 biomarker-drug pairings linked to approved tests, signaling that reimbursement agencies will progressively withhold payment for therapy courses lacking molecular confirmation. This linkage is steering pharmaceutical companies to co-develop tests earlier in Phase I trials, compressing total program timelines but increasing preclinical complexity. An immediate knock-on effect is that contract research organizations (CROs) are expanding biomarker-validation benches to secure multi-year strategic outsourcing contracts, positioning themselves as de facto molecular gatekeepers for biopharma pipelines.

High Development Costs

Developing a companion diagnostic can require USD 50-100 million and 3-5 years, framing diagnostics as long-cycle capital projects. Smaller firms increasingly tie their fortunes to big-pharma alliances, trading equity stakes for developmental funding. The second-order consequence is a consolidation of intellectual-property portfolios: as large companies absorb device rights, freedom-to-operate for newcomers narrows. This tightening IP landscape nudges venture investors to favor platform companies with expandable assay menus rather than single-marker concepts, subtly migrating venture dollars away from niche biomarkers toward scalable informatics-driven solutions, these structural shifts are shaping the companion diagnostic market.

Other drivers and restraints analyzed in the detailed report include:

- Technological Innovations in Diagnostic Tools

- Growing Prevalence of Chronic Diseases

- Stringent Regulatory Policies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

PCR still owns the largest 2025 slice at 21.8% of the companion diagnostic market share, yet NGS is expected to outpace all other technologies. NGS market size in companion diagnostics is forecast to outpace PCR-based alternatives, expanding at 13.85% CAGR between 2026-2031. Hospital procurement committees increasingly run total-cost-of-ownership analyses that reveal high sample throughput offsets higher NGS consumable costs over a three-year amortization window. Consequently, instrument vendors now bundle analytics software into reagent contracts, an arrangement that shifts revenue recognition from one-time hardware sales to recurring service streams-reshaping quarterly earnings visibility.

Melanoma companion diagnostics will capture a market share acceleration to 13.22% CAGR through 2031 as immunotherapy combinations proliferate. The downstream impact is that dermatology clinics must coordinate closely with molecular labs to ensure rapid reflex testing, effectively blending two historically separate clinical silos. This integration forces electronic medical record vendors to adapt order-entry modules to accommodate reflex molecular panels, an IT adjustment that, although minor on the surface, represents a notable administrative investment across health systems.

Geography Analysis

North America holds 39.95% market share in 2025. UnitedHealthcare's policy to cover FDA-approved companion diagnostics when matched with the corresponding drug signals payer endorsement that directly influences adoption velocity. An inferred outcome is that private insurers outside the UnitedHealthcare umbrella may emulate the policy to remain competitive, leading to a cascade that can stabilize test reimbursement rates industry-wide.

Asia-Pacific is projected to log a 12.45% CAGR from 2026-2031. Japan's government-supported cancer genome profiling (CGP) program forecasts a 54 billion-yen CGP market by 2035, prompting domestic labs to scale sequencing capacity. This governmental commitment sets a precedent that neighboring countries may replicate, harmonizing regulatory expectations and spurring cross-border clinical-trial enrollment that accelerates data accumulation in under-studied Asian populations.

Europe's In Vitro Diagnostic Regulation environment is prompting companies to reexamine launch strategies. The limited capacity of notified bodies amplifies time-to-market risk, causing diagnostic firms to consider centralized testing models as interim solutions. Such centralization may inadvertently strengthen select reference laboratories, creating a quasi-oligopoly that could sway pricing dynamics once test volumes peak.

- Abbott Laboratories

- Agilent Technologies

- Roche

- bioMerieux

- QIAGEN

- Siemens Healthineers

- Thermo Fisher Scientific

- Danaher Corp. (Beckman Coulter)

- Illumina

- Myriad Genetics

- Guardant Health

- Sysmex Corp.

- Abnova Corp.

- BioGenex

- Tempus Labs Inc.

- Foundation Medicine Inc.

- Exact Sciences Corp.

- PerkinElmer

- Invivoscribe Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid adoption of liquid-biopsy CDx in oncology practices

- 4.2.2 Advancements in Personalized Medicine and Precision Oncology

- 4.2.3 Technological Innovations in Diagnostic Tools

- 4.2.4 Growing Prevalence of Chronic Diseases

- 4.2.5 ADC-focused oncology pipeline requiring multiplex CDx platforms

- 4.2.6 Rising Investment from Pharmaceutical Companies

- 4.3 Market Restraints

- 4.3.1 High Development Costs

- 4.3.2 FDA post-market evidence obligations raising lifecycle costs

- 4.3.3 Stringent Regulatory Policies

- 4.3.4 Limited infrastructure in Emerging Countries

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Technology

- 5.1.1 Immunohistochemistry (IHC)

- 5.1.2 Polymerase Chain Reaction (PCR)

- 5.1.3 Real-Time PCR (RT-PCR)

- 5.1.4 In-Situ Hybridization (ISH)

- 5.1.5 Next-Generation / Gene Sequencing (NGS)

- 5.1.6 Other Technologies

- 5.2 By Indication

- 5.2.1 Lung Cancer

- 5.2.2 Breast Cancer

- 5.2.3 Colorectal Cancer

- 5.2.4 Leukemia

- 5.2.5 Melanoma

- 5.2.6 Gastric Cancer

- 5.2.7 Prostate Cancer

- 5.2.8 Other Indications

- 5.3 By Product & Service

- 5.3.1 Assays & Kits

- 5.3.2 Instruments & Analyzers

- 5.3.3 Software & Services

- 5.4 By Sample Type

- 5.4.1 Tissue Biopsy

- 5.4.2 Liquid Biopsy

- 5.4.3 Cytology Smears

- 5.5 By End-user

- 5.5.1 Pharmaceutical & Biotechnology Companies

- 5.5.2 Contract Research Organizations (CROs)

- 5.5.3 Clinical Reference Laboratories

- 5.5.4 Hospital & Cancer Centers

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Abbott

- 6.4.2 Agilent Technologies Inc.

- 6.4.3 F. Hoffmann-La Roche Ltd

- 6.4.4 bioMerieux SA

- 6.4.5 QIAGEN N.V.

- 6.4.6 Siemens Healthineers AG

- 6.4.7 Thermo Fisher Scientific Inc.

- 6.4.8 Danaher Corp. (Beckman Coulter)

- 6.4.9 Illumina Inc.

- 6.4.10 Myriad Genetics Inc.

- 6.4.11 Guardant Health Inc.

- 6.4.12 Sysmex Corp.

- 6.4.13 Abnova Corp.

- 6.4.14 Biogenex Laboratories Inc.

- 6.4.15 Tempus Labs Inc.

- 6.4.16 Foundation Medicine Inc.

- 6.4.17 Exact Sciences Corp.

- 6.4.18 PerkinElmer Inc.

- 6.4.19 Invivoscribe Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

伴隨診斷市場機會、成長要素、產業趨勢分析及2026-2035年預測

伴隨診斷市場機會、成長要素、產業趨勢分析及2026-2035年預測 伴隨診斷市場:2026-2032年全球市場預測(按交付方式、技術、檢體類型、生物標記分類、應用、最終用戶和分銷管道分類)

伴隨診斷市場:2026-2032年全球市場預測(按交付方式、技術、檢體類型、生物標記分類、應用、最終用戶和分銷管道分類) 全球伴隨診斷市場(至 2031 年):按產品(檢測、試劑盒和試劑、儀器和軟體)、技術(PCR、NGS、ISH、IHC)、適應症(乳癌、肺癌、大腸癌、心血管疾病、感染疾病)和藥物類型(單株抗體、細胞和基因療法)分類

全球伴隨診斷市場(至 2031 年):按產品(檢測、試劑盒和試劑、儀器和軟體)、技術(PCR、NGS、ISH、IHC)、適應症(乳癌、肺癌、大腸癌、心血管疾病、感染疾病)和藥物類型(單株抗體、細胞和基因療法)分類 伴隨診斷市場規模、佔有率和趨勢分析報告:按產品/服務、適應症、技術、檢體類型、最終用途、地區和細分市場預測(2026-2033 年)

伴隨診斷市場規模、佔有率和趨勢分析報告:按產品/服務、適應症、技術、檢體類型、最終用途、地區和細分市場預測(2026-2033 年) 伴隨診斷市場預測至2034年-按產品和服務、技術、適應症、檢體類型、應用、最終用戶和地區分類的全球分析

伴隨診斷市場預測至2034年-按產品和服務、技術、適應症、檢體類型、應用、最終用戶和地區分類的全球分析 伴隨診斷市場報告:按產品/服務、技術、適應症、最終用戶和地區分類(2026-2034 年)

伴隨診斷市場報告:按產品/服務、技術、適應症、最終用戶和地區分類(2026-2034 年) 伴隨診斷服務的合作與授權協議(2010-2026 年)

伴隨診斷服務的合作與授權協議(2010-2026 年) 伴隨診斷全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)伴隨診斷市場:按應用、技術、使用者、產品和國家分類的診斷未來發展趨勢-132家公司的策略分析,以及高階主管和顧問的指南(2026-2030):第五版

伴隨診斷全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)伴隨診斷市場:按應用、技術、使用者、產品和國家分類的診斷未來發展趨勢-132家公司的策略分析,以及高階主管和顧問的指南(2026-2030):第五版 伴隨診斷市場:按技術、應用、最終用戶和地區分類

伴隨診斷市場:按技術、應用、最終用戶和地區分類