|

市場調查報告書

商品編碼

2066405

印尼塑膠市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Indonesia Plastics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

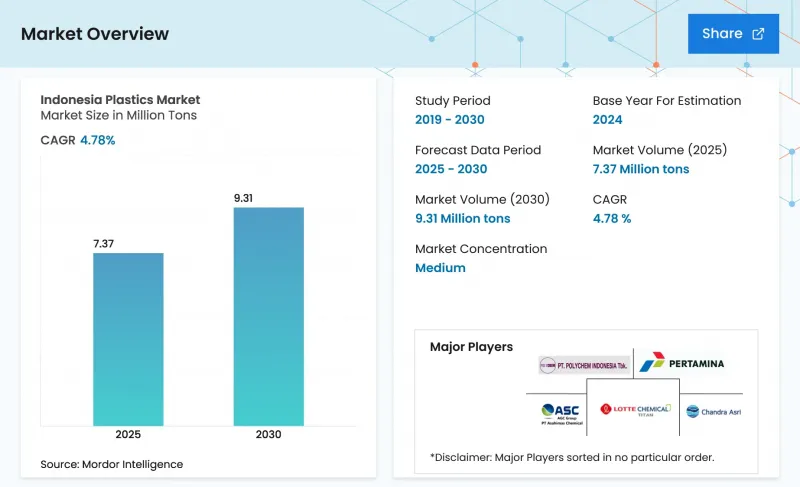

根據 Mordor Intelligence 預測,印尼塑膠市場規模將從 2025 年的 742 萬噸成長到 2026 年的 776 萬噸,然後在 2031 年達到 967 萬噸,2026 年至 2031 年的複合年成長率為 4.52%。

本報告按類型(傳統塑膠、工程塑膠、生質塑膠)、工藝(吹塑成型、擠出成型、射出成型及其他工藝)和應用(包裝、電氣電子、建築施工、汽車交通運輸、家具寢具及其他應用)進行分類。市場預測以噸為單位。

印尼塑膠市場趨勢與洞察

下游石化聯合裝置的擴建

一座年產100萬噸的乙烯裂解裝置和一座年產45萬噸的聚乙烯裝置計劃於2025年11月在芝勒貢運作,屆時將消除爪哇島對乙烯進口的依賴,降低管道物流成本,並可柔軟性使用高達50%的液化石油氣(LPG)作為原料,從而利用石腦油和液化石油氣之間的價格進行液化石油氣。修訂後的CAP-2計畫將於2027年新增氯鹼和二氯乙烷(EDC)的生產,緩解印尼乙烯基進口短缺的問題;一條年產72萬噸的聚對苯二甲酸乙二醇酯(PET)生產線計劃於2028年運作,這將降低印尼對飲料級PET進口的依賴。綜合來看,預計到2031年,這些因素將使印尼樹脂自給率達到70%,創造約20億美元的年經濟價值。此外,一體化佈局將集中熟練勞動力和共享公用設施,以鞏固爪哇島作為印尼塑膠市場核心的地位。雖然這些規模化措施可望緩解原物料價格波動,但要最大限度地節省物流成本,則需要解決梅拉克和蒂萊貢周邊電網的擁塞問題。

原始設備製造商採用輕量化汽車零件

汽車製造商的目標是將整車重量降低10%,從而提高6-8%的燃油效率,並正穩步從鋼材轉向工程塑膠,例如用於儀表板的PC-ABS共混物和用於引擎艙部件的聚醯胺。卡拉旺的一級供應商正在採購本地配製的塑膠,這縮短了進口前置作業時間,並保護汽車製造商(OEM)免受外匯波動的影響。隨著東協協調標準重視排放減排,在電動車廣泛普及之前,對阻燃和耐熱樹脂的需求正在成長。國內對聚對聚丁烯對苯二甲酸酯(PBT)等特種聚合物的生產能力有限,仍需從日本和韓國進口,但合資企業的討論正在推進,國內建設特種聚合物工廠的活動也日益活躍。儘管一般塑膠的利潤率有所下降,但這些發展正在增強印尼塑膠市場的整體附加價值創造。

對一次性塑膠袋徵收30%的消費稅。

消費稅草案提案對薄型高密度聚乙烯(HDPE)和低密度聚乙烯(LDPE)塑膠袋徵收每公斤3萬印尼幣的課稅。如果該稅項於2026年實施,可能會導致薄膜樹脂供應商的銷售量下降5%至8%。零售商可能會轉而使用可重複使用的托特包或更厚的HDPE塑膠袋來規避重量限制,從而削弱其真正的環境效益。各市的執法能力參差不齊,先前在班賈爾馬辛和茂物實施的禁令執行情況不佳。由於這些不確定性,對新的LDPE生產能力的投資已經停滯,加工商正在等待最終稅率確定後再簽署長期採購協議。因此,政策的明確性對於印尼塑膠市場的穩定成長至關重要。

細分市場分析

2025年,傳統塑膠佔印尼塑膠市場75.12%的佔有率,其中聚乙烯和聚丙烯是薄膜、瓶子和射出成型製品的主要原料。隨著電商包裝和建築管道需求的成長,這些塑膠品類的印尼市場規模也隨之擴大。聚乙烯受益於Tilegon新運作生產線帶來的高產量,而聚丙烯的成長則與汽車保險桿和拉菲草袋的訂單趨勢密切相關。儘管一些加工商為了符合氯含量法規而嘗試用聚烯取代PVC,但PVC在管道和電纜領域的應用仍然強勁。

儘管工程塑膠產量較低,但由於其在電子設備機殼和汽車引擎艙部件等領域的高價,推動了其銷售。 PET方面,隨著一座年產72萬噸的工廠於2028年投產,預計產能將運作,從而提高瓶級PET的供應穩定性並降低進口成本。以海藻衍生樹脂為代表的生質塑膠目前產量仍然較小,但預計在預測期(2025-2031年)內將以6.12%的複合年成長率實現最高成長,這反映了全球對一次性化石基塑膠的禁令。印尼生物聚合物級塑膠市場的規模取決於成本趨同和稅額扣抵的潛力,而這些仍在考慮之中。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 下游油田擴建(芝勒貢、圖班)

- 原始設備製造商採用輕量化汽車零件

- 電子商務物流的快速發展需要耐用的二次包裝。

- 強制性生產者責任延伸制度和廢棄物分類試點計畫正在推動對可再生樹脂的需求。

- 東爪哇海藻衍生生質塑膠叢集

- 市場限制因素

- 從2026年起,對一次性塑膠袋徵收30%的銷售稅。

- 碳定價機制推高了能源成本

- 內陸地區鐵路基礎設施的匱乏推高了樹脂物流成本。

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 按類型

- 傳統塑膠

- 聚乙烯(PE)

- 聚丙烯(PP)

- 聚氯乙烯(PVC)

- 聚苯乙烯(PS)

- 工程塑膠

- 聚對苯二甲酸乙二醇酯(PET)

- 聚醯胺

- 聚碳酸酯

- 苯乙烯共聚物(ABS 和 SAN)

- 聚丁烯對苯二甲酸酯(PBT)

- 氟聚合物

- 聚甲醛(POM)

- 聚甲基丙烯酸甲酯(PMMA)

- 其他工程塑膠

- 生質塑膠

- 傳統塑膠

- 透過技術

- 吹塑成型

- 擠壓

- 射出成型

- 其他技術

- 透過使用

- 包裝

- 電氣和電子設備

- 建築/施工

- 汽車和運輸業

- 家具和床上用品

- 其他用途

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- Asahimas Chemical Company

- Chandra Asri Group

- Dow

- LOTTE CHEMICAL TITAN HOLDING BERHAD

- LyondellBasell Industries NV

- Mitsubishi Chemical Group Corporation

- PT Indonesia Nanya Indah Plastics

- PT Pertamina(Persero)

- PT Polychem Indonesia Tbk

- PT Standard Toyo Polymer(Tosoh Corporation)

- PTT Global Chemical Public Company Limited

- Sulfindo Adiusaha

- TORAY INDUSTRIES, INC.

第7章 市場機會與未來展望

According to Mordor Intelligence, the indonesia plastics market size is expected to grow from 7.42 million tons in 2025 to 7.76 million tons in 2026 and is forecast to reach 9.67 million tons by 2031 at 4.52% CAGR over 2026-2031.

This report is Segmented by Type (Traditional Plastics, Engineering Plastics, and Bioplastics), Technology (Blow Molding, Extrusion, Injection Molding, and Other Technologies), and Application (Packaging, Electrical and Electronics, Building and Construction, Automotive and Transportation, Furniture and Bedding, and Other Applications). The Market Forecasts are Provided in Terms of Volume (Tons).

Indonesia Plastics Market Trends and Insights

Expansion of Downstream Petro-Complexes

The November 2025 start-up of a 1 million ton ethylene cracker and 450,000 ton polyethylene unit in Cilegon eliminates the need for imported ethylene on Java, cuts pipeline logistics, and leverages up to 50% LPG (liquefied petroleum gas) feedstock flexibility that arbitrages naphtha-LPG spreads. A re-scoped CAP-2 project adds chlor-alkali and ethylene dichloride (EDC) output in 2027, shrinking Indonesia's vinyl import gap, while a planned 720,000 tons polyethylene terephthalate (PET) line set for 2028 lowers beverage-grade reliance on foreign supply. Together, these builds lift projected domestic coverage of overall resin demand to 70% by 2031 and unlock roughly USD 2 billion in annual economic value. Integrated layouts also concentrate skilled labor and shared utilities, reinforcing Java's status as the nucleus of the Indonesia Plastics market. The combined scale is expected to soften feedstock price volatility, though grid congestion around Merak and Cilegon must still be eased to fully capture logistics savings.

Lightweight Auto-Parts Adoption by OEMs

Automotive assemblers are targeting 10% curb-weight cuts that can translate into 6-8% fuel savings, prompting a steady switch from steel to engineering plastics such as PC-ABS blends for dashboards and polyamide for under-hood parts. Tier-1 suppliers in Karawang source locally compounded grades, which reduces import lead time and ring-fence original equipment manufacturers (OEMs) from forex swings. ASEAN harmonized standards reward lower CO2 output, intensifying demand for flame-retardant, high-temperature resins ahead of rising electric-vehicle penetration. Limited domestic capacity for niche polymers like polybutylene terephthalate (PBT) continues to pull in imports from Japan and South Korea, yet joint-venture talks signal momentum toward onshore specialty polymer plants. These moves fortify value capture across the Indonesia Plastics market, even as commodity margins tighten.

30% Excise on Single-Use Plastic Bags

Draft excise legislation proposes IDR 30,000 per kg for thin HDPE and LDPE bags, threatening a 5-8% volume hit for film-grade resin suppliers if enacted in 2026. Retailers could pivot to reusable totes or thicker HDPE bags that dodge weight thresholds, softening true environmental gains. Municipal enforcement capacity varies, as past bans in Banjarmasin and Bogor suffered compliance gaps. The uncertainty already stalls new LDPE capacity investments, with converters waiting for final tax brackets before signing long-term offtake deals. Policy clarity is therefore critical for stable growth in the Indonesia Plastics market.

Other drivers and restraints analyzed in the detailed report include:

- E-Commerce Logistics Boom

- Mandatory EPR and Waste-Segregation Pilots

- Carbon-Pricing Scheme Raising Energy Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Traditional Plastics secured 75.12% of Indonesia Plastics market share in 2025, with polyethylene and polypropylene making up the bulk of film, bottle, and injection molded items. The Indonesia Plastics market size for these grades rose in tandem with e-commerce packaging and construction pipe demand. Polyethylene benefits from high output at newly commissioned Cilegon lines, and polypropylene growth tracks automotive bumper and raffia sack orders. PVC usage in pipe and cable remains resilient, though some converters experiment with polyolefin substitution to navigate chlorine scrutiny.

Engineering Plastics, though smaller in tonnage, command premium pricing in electronics housings and under-hood auto parts, lifting their revenue footprint. PET is set for a capacity burst once a 720,000-ton plant starts in 2028, improving bottle-grade security and trimming import bills. Bioplastics, led by seaweed resins, hold a thin volume but are expected to grow with the fastest CAGR of 6.12% during the forecast period (2025-2031), mirroring global bans on single-use fossil plastics. The Indonesia Plastics market size for biopolymer grades hinges on cost convergence and potential tax credits that are still on the policy table.

List of Companies Covered in this Report:

- Asahimas Chemical Company

- Chandra Asri Group

- Dow

- LOTTE CHEMICAL TITAN HOLDING BERHAD

- LyondellBasell Industries N.V.

- Mitsubishi Chemical Group Corporation

- PT Indonesia Nanya Indah Plastics

- PT Pertamina (Persero)

- PT Polychem Indonesia Tbk

- PT Standard Toyo Polymer (Tosoh Corporation)

- PTT Global Chemical Public Company Limited

- Sulfindo Adiusaha

- TORAY INDUSTRIES, INC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of downstream petro-complexes (Cilegon, Tuban)

- 4.2.2 Lightweight auto-parts adoption by OEMs

- 4.2.3 E-commerce logistics boom needing durable secondary packs

- 4.2.4 Mandatory EPR and waste-segregation pilots fueling recyclable resin demand

- 4.2.5 Sea-weed based bioplastics clusters in East Java

- 4.3 Market Restraints

- 4.3.1 30 % excise on single-use plastic bags (from 2026)

- 4.3.2 Carbon-pricing scheme raising energy costs

- 4.3.3 Rail-infrastructure gaps inflating inland resin logistics

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 Traditional Plastics

- 5.1.1.1 Polyethylene (PE)

- 5.1.1.2 Polypropylene (PP)

- 5.1.1.3 Polyvinyl Chloride (PVC)

- 5.1.1.4 Polystyrene (PS)

- 5.1.2 Engineering Plastics

- 5.1.2.1 Polyethylene Terephthalate (PET)

- 5.1.2.2 Polyamides

- 5.1.2.3 Polycarbonates

- 5.1.2.4 Styrene Copolymers (ABS and SAN)

- 5.1.2.5 Polybutylene Terephthalate (PBT)

- 5.1.2.6 Fluoropolymers

- 5.1.2.7 Polyoxymethylene (POM)

- 5.1.2.8 Polymethyl Methacrylate (PMMA)

- 5.1.2.9 Other Engineering Plastics

- 5.1.3 Bioplastics

- 5.1.1 Traditional Plastics

- 5.2 By Technology

- 5.2.1 Blow Molding

- 5.2.2 Extrusion

- 5.2.3 Injection Molding

- 5.2.4 Other Technologies

- 5.3 By Application

- 5.3.1 Packaging

- 5.3.2 Electrical and Electronics

- 5.3.3 Building and Construction

- 5.3.4 Automotive and Transportation

- 5.3.5 Furniture and Bedding

- 5.3.6 Other Applications

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Asahimas Chemical Company

- 6.4.2 Chandra Asri Group

- 6.4.3 Dow

- 6.4.4 LOTTE CHEMICAL TITAN HOLDING BERHAD

- 6.4.5 LyondellBasell Industries N.V.

- 6.4.6 Mitsubishi Chemical Group Corporation

- 6.4.7 PT Indonesia Nanya Indah Plastics

- 6.4.8 PT Pertamina (Persero)

- 6.4.9 PT Polychem Indonesia Tbk

- 6.4.10 PT Standard Toyo Polymer (Tosoh Corporation)

- 6.4.11 PTT Global Chemical Public Company Limited

- 6.4.12 Sulfindo Adiusaha

- 6.4.13 TORAY INDUSTRIES, INC.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

塑膠市場預測至2034年—按類型、樹脂類型、加工技術、形狀、應用、最終用途產業和地區分類的全球分析

塑膠市場預測至2034年—按類型、樹脂類型、加工技術、形狀、應用、最終用途產業和地區分類的全球分析 塑膠紙托盤市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、產品、分銷管道、地區和競爭格局分類,2021-2031年

塑膠紙托盤市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、產品、分銷管道、地區和競爭格局分類,2021-2031年 食品塑膠市場規模、佔有率和趨勢分析報告:按聚合物類型、應用、地區和細分市場預測(2026-2033 年)

食品塑膠市場規模、佔有率和趨勢分析報告:按聚合物類型、應用、地區和細分市場預測(2026-2033 年) 塑膠研究展望:2025

塑膠研究展望:2025 磁性塑膠市場:2026-2032年全球市場預測(按類型、樹脂類型、形狀、製造程序和磁性塑膠應用分類)

磁性塑膠市場:2026-2032年全球市場預測(按類型、樹脂類型、形狀、製造程序和磁性塑膠應用分類) 2026-2030年全球塑膠市場

2026-2030年全球塑膠市場 塑膠市場規模、佔有率、趨勢和預測:按類型、應用、最終用戶和地區分類,2026-2034年塑膠市場:依形狀、等級、製造流程、類型、應用和分銷管道分類-2026-2032年全球市場預測

塑膠市場規模、佔有率、趨勢和預測:按類型、應用、最終用戶和地區分類,2026-2034年塑膠市場:依形狀、等級、製造流程、類型、應用和分銷管道分類-2026-2032年全球市場預測 塑膠市場分析及預測(至2035年):類型、產品、應用、材料類型、技術、最終用戶、製程、組件、安裝類型

塑膠市場分析及預測(至2035年):類型、產品、應用、材料類型、技術、最終用戶、製程、組件、安裝類型 東南亞塑膠市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

東南亞塑膠市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)