|

市場調查報告書

商品編碼

1939075

東南亞塑膠市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)South-East Asia (SEA) Plastics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

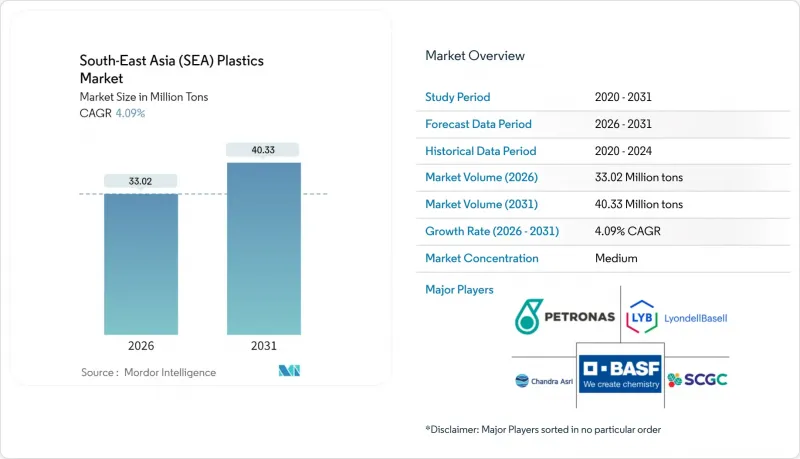

預計東南亞塑膠市場將從 2025 年的 3,170 萬噸成長到 2026 年的 3,302 萬噸,到 2031 年將達到 4,033 萬噸,2026 年至 2031 年的複合年成長率為 4.09%。

消費支出增加、出口導向製造業擴張以及基礎設施運轉率持續穩定,推動了加工廠的高速運轉,從而促進了產業成長。本地產能的提升有助於降低進口依賴,確保原料供應穩定;同時,監管部門大力推動循環經濟,鼓勵生產商投資創新和回收。印尼投資的蓬勃發展和越南工廠的快速建設支撐了生產成長,而所有主要東協成員國都在為下游石化產業提供優惠待遇,以確保區域供應鏈的安全。從即時製程監控到預測性維護,數位化製造舉措也在擴大生產力差距,並增強大型整合商的成本優勢。

東南亞塑膠市場趨勢與展望

食品和飲料包裝行業的需求不斷成長

城市生活節奏加快和中產階級持續壯大,推動了對簡便食品和即飲飲料的需求,促使加工商增加多層薄膜和硬質PET容器的產量。自2024年以來,越南包裝產業吸引了大量外商直接投資(FDI),全球品牌商紛紛在越南建立面向東協和出口市場的供應基地。監管機構正在收緊食品接觸標準,在泰國,所有食品接觸包裝都必須獲得ISO 22000認證。這促使加工商轉向使用高性能阻隔樹脂和抗菌添加劑。延長保存期限的舉措正在零售鏈中蔓延,推動了對具有更強氧氣和防潮性能的聚丙烯和聚乙烯產品的需求。生鮮電商的快速發展,使得相關人員對輕質且抗穿刺包裝的需求日益成長,推動了高模量共混材料的快速替代,這種材料能夠在不犧牲強度的前提下實現更薄的壁厚。

印尼和越南下游業務快速擴張

2023年至2025年間運作投產的大型裂解裝置和聚合物裝置將重塑區域貿易格局。越南龍山綜合體於2023年底新增165萬噸乙烯產能,為越南國內加工商提供穩定的原料供應,此前這些原料主要依賴東北亞地區。在印尼,TPPI正在對其芳烴生產線進行產能最佳化,而樂天化學預計將於2025年下半年投產一座年產100萬噸的裂解裝置,屆時將運作超過200萬噸的單體年產量。這些計劃恰逢中國石化產能過剩之際,使東南亞塑膠市場成為尋求關稅多元化的全球加工商的替代供應平台。政府的激勵措施,例如對超過5億美元的計劃給予稅收減免以及簡化經濟特區內的核准程序,正在縮短建設週期並降低核准門檻,從而鼓勵區域加工商簽訂長期承購協議。

嚴格的塑膠法規和禁令

泰國的塑膠袋法規(將於2025年3月生效)強制要求使用可生物分解添加劑並設定最低厚度標準,這將使購物袋製造商的原料成本增加15%至20%。新加坡於2025年1月擴大了塑膠廢棄物進口禁令,給依賴跨境廢棄物流通的本地回收商帶來了壓力。馬來西亞的生產者延伸責任制(EPR)法案計劃於2026年生效,該法案將把收集和回收的經濟責任轉移到製造商身上。這項義務有利於能夠承擔遵循成本的大型企業。這些措施威脅到一次性產品類型,迫使加工商轉向可重複使用和可堆肥的產品以維持貨架空間。

細分市場分析

截至2025年,聚乙烯、聚丙烯和聚氯乙烯等傳統塑膠將佔東南亞塑膠市場63.05%的佔有率,這主要得益於包裝和消費品應用領域的規模經濟效益。印尼和越南現有生產線的擴建將提升該地區聚烯的整體名義產能,使樹脂價格保持與進口產品的競爭力。

工程塑膠雖然在銷售上仍屬小眾市場,但其戰略意義重大,在汽車引擎室零件和電子設備外殼等領域佔據重要訂單,而耐熱性和尺寸穩定性是這些領域的關鍵指標。本地複合材料生產商正投資研發玻璃纖維增強尼龍和PBT共混物,以幫助原始設備製造商(OEM)實現在地採購目標。為支持電動車的廣泛應用而訂定的更嚴格的法規,可能會加速符合UL 94 V-0標準的阻燃等級材料的需求成長。

生質塑膠在東南亞塑膠市場以4.42%的複合年成長率快速成長,但成本溢價和工業堆肥基礎設施的缺乏限制了其應用。 SCG Chemicals位於泰國的木薯生物乙烯工廠向加工商供應符合EN 13432堆肥標準的生物聚乙烯(bio-PE),為尋求差異化永續性認證的品牌所有者拓展了材料選擇。馬來西亞棕櫚油創新基金正在支持PHA和PBS,但商業化時間表取決於歐盟森林砍伐法規下的原料認證標準。

東南亞塑膠市場報告按類型(傳統塑膠、工程塑膠、生質塑膠等)、技術(射出成型、吹塑成型等)、應用(包裝、電氣電子、建築施工、汽車交通運輸等)和地區(印尼、泰國、馬來西亞、越南等)進行細分。市場預測以噸為單位。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 食品和飲料包裝行業的需求不斷成長

- 印尼和越南下游產能快速擴張

- 電子商務主導了對軟性包裝的需求激增

- 基礎建設促進建築塑膠的發展

- 政府支持的石化經濟特區管道

- 市場限制

- 嚴格的塑膠法規和禁令

- 原物料價格波動

- 工程塑膠業技術純熟勞工短缺

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 按類型

- 傳統塑膠

- 工程塑膠

- 生質塑膠

- 透過技術

- 射出成型

- 吹塑成型

- 擠出成型

- 其他技術

- 透過使用

- 包裝

- 電氣和電子設備

- 建築/施工

- 汽車和運輸設備

- 家居用品

- 家具和床上用品

- 其他用途

- 按地區

- 印尼

- 泰國

- 馬來西亞

- 越南

- 菲律賓

- 新加坡

- 東南亞及其他地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- 塑膠樹脂製造商

- AGC Chemicals Vietnam Co., Ltd.

- BASF

- Dow

- DuPont

- Indorama Ventures

- JG Summit Petrochemical Corp

- Kaneka(Malaysia)Sdn Bhd

- LyondellBasell

- Nan Ya Plastics(Formosa)

- NPC Alliance Corp

- PETRONAS Chemicals Group Berhad

- Philippine Resins Industries

- PRefChem

- 塑膠製品製造商

- Ampac Holdings

- An Phat Holdings

- An Trung Industries

- Binh Minh Plastic

- Cholon Plastic Co. Ltd.

- City Long(Cambodia)Co., Ltd.

- Dongsung

- Duy Tan Plastics Corporation

- LOTTE Chemical Titan

- Polyplastics Co., Ltd.

- PT Chandra Asri Petrochemical Tbk

- SCG Chemicals PCL

- Thai Formosa Plastic Industry Co., Ltd.

- 塑膠樹脂製造商

第7章 市場機會與未來展望

The South-East Asia Plastics market is expected to grow from 31.70 million tons in 2025 to 33.02 million tons in 2026 and is forecast to reach 40.33 million tons by 2031 at 4.09% CAGR over 2026-2031.

Growth rests on rising consumer spending, expanding export-oriented manufacturing, and steady infrastructure outlays that keep processors operating at high utilization rates. Local capacity additions trim import dependence and feedstock security, while regulatory momentum toward circular-economy practices forces producers to upgrade technology and invest in recycling. Indonesia's investment boom and Vietnam's rapid factory build-out underpin volume gains, but all major ASEAN members are channeling incentives into downstream petrochemicals to secure regional supply chains. Digital manufacturing initiatives-from real-time process monitoring to predictive maintenance-are also widening productivity differentials, reinforcing the cost advantages of large, integrated operators.

South-East Asia (SEA) Plastics Market Trends and Insights

Rising Demand from Food and Beverage Packaging

Accelerating urban lifestyles and sustained middle-class growth are intensifying demand for convenience foods and ready-to-drink beverages, prompting converters to raise runs of multi-layer films and rigid PET containers. Vietnam has attracted FDI since 2024 in packaging as global brand owners establish supply hubs to serve ASEAN and export markets. Regulators are tightening food-contact norms-Thailand now requires ISO 22000 certification on all packaging that touches edibles-nudging processors toward higher-spec barrier resins and antimicrobial additives. Shelf-life extension initiatives cascade through retail chains, boosting polypropylene and polyethylene grades engineered for oxygen and moisture resistance. With grocery e-commerce swelling, stakeholder pressure for lightweight yet puncture-resistant formats is spurring rapid material substitution toward high-modulus blends that enable downgauging without compromising integrity.

Rapid Downstream Capacity Additions Across Indonesia and Vietnam

Large-scale crackers and polymer plants coming online between 2023-2025 redraw intraregional trade flows. Vietnam's Long Son complex added 1.65 million t/y of ethylene capacity in late 2023, providing domestic processors with feedstock security previously sourced from Northeast Asia. Indonesia is seeing more than 2 million t/y of extra monomer output as TPPI debottlenecks its aromatics train and Lotte Chemical inaugurates a 1 million t/y cracker in 2H 2025. Coinciding with China's petrochemical overcapacity, these projects position the South-East Asia plastics market as an alternative supply platform for global converters seeking tariff diversification. State incentives-tax holidays on projects exceeding USD 500 million and streamlined permitting inside special economic zones-have shortened build-out schedules and lowered hurdle rates, encouraging regional processors to lock in long-term offtake contracts.

Stringent Anti-Plastic Regulations and Bans

Thailand's plastic bag decree, effective March 2025, mandates biodegradable additives and minimum thickness thresholds, raising input costs for shopping-bag producers by 15-20%. Singapore widened its plastic-waste import ban in January 2025, squeezing regional recyclers that relied on cross-border scrap inflows. Malaysia's forthcoming Extended Producer Responsibility (EPR) law shifts financial responsibility for collection and recycling to manufacturers starting in 2026, an obligation that favors scale players able to absorb compliance spend. These measures threaten single-use categories, forcing converters to pivot toward reusable and compostable options to keep shelf space.

Other drivers and restraints analyzed in the detailed report include:

- Surge in E-Commerce-Led Flexible Packaging Needs

- Infrastructure Push Boosting Construction Plastics

- Feedstock Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Traditional grades-polyethylene, polypropylene, and PVC-held a 63.05% share of the South-East Asia plastics market in 2025, supported by scale economics in packaging and consumer goods applications. Several brownfield line extensions in Indonesia and Vietnam lift aggregate regional polyolefin nameplate capacity and keep resin pricing competitive versus imports.

Engineering plastics remain niche in volume terms yet strategically important, capturing contracts in automotive under-the-hood parts and electronics housings where heat resistance and dimensional stability drive specification. Local compounders are investing in glass-fiber reinforced nylon and PBT blends to satisfy OEM localization targets. Regulatory push for electric vehicle adoption could accelerate demand for flame-retardant grades compliant with UL 94 V-0 standards.

Bioplastics are climbing at a 4.42% CAGR, the fastest within the South-East Asia plastics market, yet cost premiums and limited infrastructure for industrial composting temper penetration. Thailand's cassava-based bio-ethylene plant, built by SCG Chemicals, supplies converters with bio-PE that meets EN 13432 compostability, widening material choice for brand owners seeking differentiated sustainability credentials. Malaysia's palm oil innovation fund backs PHAs and PBS, though commercialization schedules hinge on feedstock certification thresholds under EU deforestation rules.

The South-East Asia Plastics Market Report is Segmented by Type (Traditional Plastics, Engineering Plastics, and Bioplastics), Technology (Injection Molding, Blow Molding, and More), Application (Packaging, Electrical and Electronics, Building and Construction, Automotive and Transportation, and More), and Geography (Indonesia, Thailand, Malaysia, Vietnam, and More). The Market Forecasts are Provided in Terms of Volume (Tons).

List of Companies Covered in this Report:

- Plastic Resin Manufacturers

- Plastic Product Manufacturers

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand from food and beverage packaging

- 4.2.2 Rapid downstream capacity additions across Indonesia and Vietnam

- 4.2.3 Surge in e-commerce-led flexible packaging needs

- 4.2.4 Infrastructure push boosting construction plastics

- 4.2.5 Government-backed petro-chemical SEZ pipelines

- 4.3 Market Restraints

- 4.3.1 Stringent anti-plastic regulations and bans

- 4.3.2 Feedstock price volatility

- 4.3.3 Shortage of skilled labor in engineering-grade plastics

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 Traditional Plastics

- 5.1.2 Engineering Plastics

- 5.1.3 Bioplastics

- 5.2 By Technology

- 5.2.1 Injection Molding

- 5.2.2 Blow Molding

- 5.2.3 Extrusion

- 5.2.4 Other Technologies

- 5.3 By Application

- 5.3.1 Packaging

- 5.3.2 Electrical and Electronics

- 5.3.3 Building and Construction

- 5.3.4 Automotive and Transportation

- 5.3.5 Housewares

- 5.3.6 Furniture and Bedding

- 5.3.7 Other Applications

- 5.4 By Geography

- 5.4.1 Indonesia

- 5.4.2 Thailand

- 5.4.3 Malaysia

- 5.4.4 Vietnam

- 5.4.5 Philippines

- 5.4.6 Singapore

- 5.4.7 Rest of South-East Asia

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Plastic Resin Manufacturers

- 6.4.1.1 AGC Chemicals Vietnam Co., Ltd.

- 6.4.1.2 BASF

- 6.4.1.3 Dow

- 6.4.1.4 DuPont

- 6.4.1.5 Indorama Ventures

- 6.4.1.6 JG Summit Petrochemical Corp

- 6.4.1.7 Kaneka (Malaysia) Sdn Bhd

- 6.4.1.8 LyondellBasell

- 6.4.1.9 Nan Ya Plastics (Formosa)

- 6.4.1.10 NPC Alliance Corp

- 6.4.1.11 PETRONAS Chemicals Group Berhad

- 6.4.1.12 Philippine Resins Industries

- 6.4.1.13 PRefChem

- 6.4.2 Plastic Product Manufacturers

- 6.4.2.1 Ampac Holdings

- 6.4.2.2 An Phat Holdings

- 6.4.2.3 An Trung Industries

- 6.4.2.4 Binh Minh Plastic

- 6.4.2.5 Cholon Plastic Co. Ltd.

- 6.4.2.6 City Long (Cambodia) Co., Ltd.

- 6.4.2.7 Dongsung

- 6.4.2.8 Duy Tan Plastics Corporation

- 6.4.2.9 LOTTE Chemical Titan

- 6.4.2.10 Polyplastics Co., Ltd.

- 6.4.2.11 PT Chandra Asri Petrochemical Tbk

- 6.4.2.12 SCG Chemicals PCL

- 6.4.2.13 Thai Formosa Plastic Industry Co., Ltd.

- 6.4.1 Plastic Resin Manufacturers

7 Market Opportunities and Future Outlook

- 7.1 White-space and unmet-need assessment

塑膠紙托盤市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、產品、分銷管道、地區和競爭格局分類,2021-2031年

塑膠紙托盤市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、產品、分銷管道、地區和競爭格局分類,2021-2031年 塑膠研究展望:2025

塑膠研究展望:2025 磁性塑膠市場:2026-2032年全球市場預測(按類型、樹脂類型、形狀、製造程序和磁性塑膠應用分類)

磁性塑膠市場:2026-2032年全球市場預測(按類型、樹脂類型、形狀、製造程序和磁性塑膠應用分類) 2026-2030年全球塑膠市場

2026-2030年全球塑膠市場 塑膠市場規模、佔有率、趨勢和預測:按類型、應用、最終用戶和地區分類,2026-2034年塑膠市場:依形狀、等級、製造流程、類型、應用和分銷管道分類-2026-2032年全球市場預測

塑膠市場規模、佔有率、趨勢和預測:按類型、應用、最終用戶和地區分類,2026-2034年塑膠市場:依形狀、等級、製造流程、類型、應用和分銷管道分類-2026-2032年全球市場預測 塑膠市場分析及預測(至2035年):類型、產品、應用、材料類型、技術、最終用戶、製程、組件、安裝類型

塑膠市場分析及預測(至2035年):類型、產品、應用、材料類型、技術、最終用戶、製程、組件、安裝類型 泰國塑膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南塑膠市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

泰國塑膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南塑膠市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2026-2034年全球塑膠分解細菌市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球塑膠分解細菌市場規模、佔有率、趨勢和成長分析報告